Timing & trends

Analysis

Analysis

Despite the recent scrutiny surrounding autonomous vehicles, the technology seems to be picking up speed. After three months of testing on the streets of Pittsburgh, Uber has announced that its fleet of self-driving Volvo XC90s will go live later in August. Customers in downtown Pittsburgh will be able to summon a self-driving car, which, for now, will still be manned by an Uber driver who can intervene in the car’s operation if need be. And Volvo may soon have competition.

also:

Michaels take on the economic impact:

We know why Britons voted to leave the EU and what the UK’s options outside the EU are. Now, let’s analyze how Brexit could affect the gold market. We covered this topic in the latest edition of the Market Overview, as well as the daily updates of the Gold NewsMonitor, but today we will examine how the shiny metal performed during the past disintegrations of economic unions.

There are many examples of break-ups or exits from monetary unions (since 1945, more than sixty distinct countries or territories left a currency union), but these cases are not especially relevant for us, as Britain is not in the Eurozone. History also witnessed several break-ups of economic and political unions, like the collapse of the Austria-Hungary, Yugoslavia, the Soviet Union and Czechoslovakia. The Austro-Hungarian Empire ended in the very specific context of the First World War, when the gold market looked very differently, so we will confine ourselves to the last three cases.

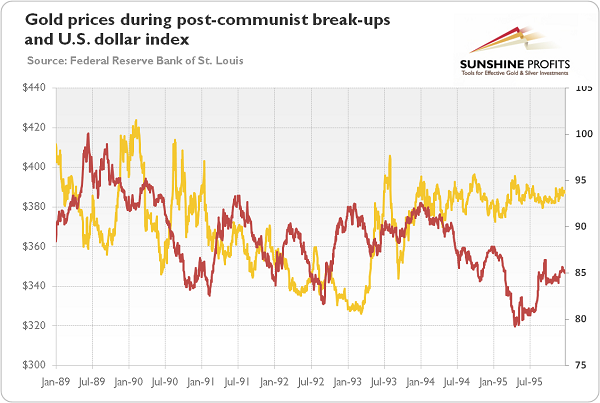

As one can see in the chart below, gold was in the downward trend in the beginning of the 1990s, despite the turmoil in the Soviet Union, violent break-up of Yugoslavia and peaceful dissolution of the Czechoslovakia. There were big rallies in 1989 and 1990, but they were associated with the weakness of the U.S. dollar and American stocks (in 1990-1991, there was a recession in the U.S.). But these rises were temporary and gold quickly returned to the long-term downward trend. This behavior suggests that the price of gold does not react significantly to the political or economic break-ups. However, investors have to be cautious in drawing conclusions from this comparison. While Yugoslavia and Czechoslovakia were not globally significant unions, Brexit means an element of disintegration of the European Union, which would increase the risk of a full break-up of the biggest economic and political bloc in the world. The Soviet Empire was a major geopolitical player, but its dissolution actually diminished risk connected with the Cold War and increased the position of the Western world. Brexit, on the contrary, would increase uncertainty and diminish the role of West. This is why Brexit would be a real precedent even for the global economy and the gold market.

Chart 1: Gold prices during post-communist break-ups in the 1990s.

Now, let’s focus on the previous exits from the European Union, as the Brexit – contrary to some popular claims – would not be the first withdrawal from the European Union. Indeed, in 1962, Algeria gained its independence from France and left the European Economic Community, the EU’s predecessor. However, since the gold market was not free at the time, we cannot examine the impact of this breakup for the yellow metal.

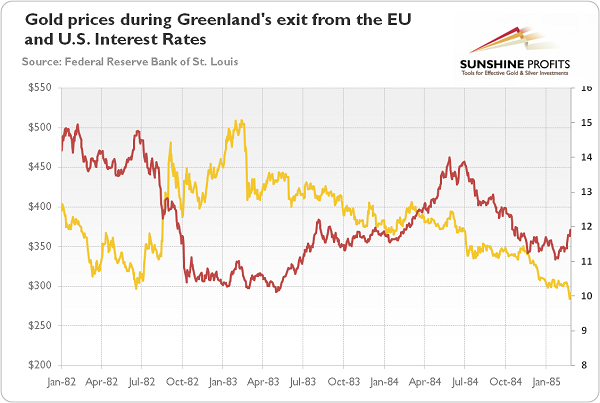

The next withdrawal from the EU happened in the 1980s, when Greenland, a part of Denmark, left the EU. It was an interesting case, as  Greenland held a referendum in 1982, but the exit was formalized only in 1985 by the Greenland Treaty. We shall add that the only controversial issue was fishing, and eventually the country did not fully exit from the EU, but adopted Overseas Country and Territory status, instead (it means that it remains subject to the EU treaties). If negotiations with Greenland (which is economically and politically less important that the UK) lasted three years, imagine how long Brexit might take (it could be great news for gold if the process increases anxiety and uncertainty, but it can be bearish for gold if the additional time makes investors think that there will be no Brexit after all or the final result will be close to Bremain anyway)!

Greenland held a referendum in 1982, but the exit was formalized only in 1985 by the Greenland Treaty. We shall add that the only controversial issue was fishing, and eventually the country did not fully exit from the EU, but adopted Overseas Country and Territory status, instead (it means that it remains subject to the EU treaties). If negotiations with Greenland (which is economically and politically less important that the UK) lasted three years, imagine how long Brexit might take (it could be great news for gold if the process increases anxiety and uncertainty, but it can be bearish for gold if the additional time makes investors think that there will be no Brexit after all or the final result will be close to Bremain anyway)!

As one can see in the chart below, the Greenland’s exit from the EU did not trigger a boost in the gold prices. Actually, the shiny metal entered into bear market in 1983. There was a rally in the summer of 1982, but it was caused by the recession in the U.S., the cuts in the Fed’s fund rate, and the fall in the U.S. interest rates.

Chart 2: Gold prices (yellow line, left axis) and the U.S. nominal interest rates (red line, right axis, in %, 10-year Treasury Constant Maturity rate) from January 1982 to February 1985.

The third withdrawal from the EU occurred in 2012, when Saint-Barthélemy, a small Caribbean island, left the EU and became one of the EU’s Overseas Countries and Territories. It would not come as a surprise that this small change did not shock the world and the gold market.

The review of the past withdrawals from the EU shows that the Brexit could be really unique. So far, only dependent territories exited from the EU, and since they were certainly not as economically and politically important as UK, they are not the best to guide how the UK departure might look. And the famous Article 50 of the Treaty on European Union, which set out the rules for exit, has not been tested yet. Hence, Brexit would be a whole new ball game, which should have much greater influence on the gold market.

Thank you.

Arkadiusz Sieron

Have patience. All things are difficult before they become easy.

Have patience. All things are difficult before they become easy.

Saadi

For the past few months, we continued to Google the Term, Dow 19K, Dow 20K and Dow 21K. We got the most hits on the search term Dow 20,000, but the noise was not enough for us to take these developments too seriously. However, when we noticed that CNBC published two similar titled articles within a time span of 30 days, it was time to take note.

It is a known fact that when sites such as CNBC take a stance, your best bet is to take an opposing position or move to the sidelines. Too many sites are calling for Dow 20,000, and the Dow has not even traded past 19,000 which means that the markets are more likely to head lower than higher.

All top sites like Barons, moneypress.com, Cnn.com, etc. have an uncanny knack of being in the wrong camp and precisely the right time. The chatter calling for Dow 20, 0000 has hit a level that is too much for us to ignore.

Dow 20,000 is coming this year, and here’s why: Strategist CNBC July 16, 2016

Dow 20,000? Don’t laugh. Bulls are alive and well Money.CNN Jul 15, 2016

Dow To Hit 20,000? ETFs To Play Yahoo Finance July 18, 2016

Dow hitting 20,000 soon? Wall Street says it will happen CNBC Aug 6, 2016

Wall Street’s New Target: Dow 20000 Wall Street Journal Aug 10, 2016

The Dow at 20,000 in a year is now the consensus forecast Market watch Aug11, 2016

Dow 20,000 in 2017? Maybe Kiplinger Aug 16, 2016

The Dow Could Reach 19,000 or Even 20,000 The Street Aug 18, 2016

In a very recent article, titled crude oil bottom likely to propel Dow higher we made the following comment

The consolidation in oil appears to be over and given their relationship, the Dow together with Crude oil could be gearing up to trade to new highs. Ideally, (but it is not necessary) the Dow would test the 17,800-18,000 ranges before making a break for 19,000.

This surge in bullish sentiment might provide the necessary impetus for the markets to let out some steam before attempting to trade to and past 19,000.

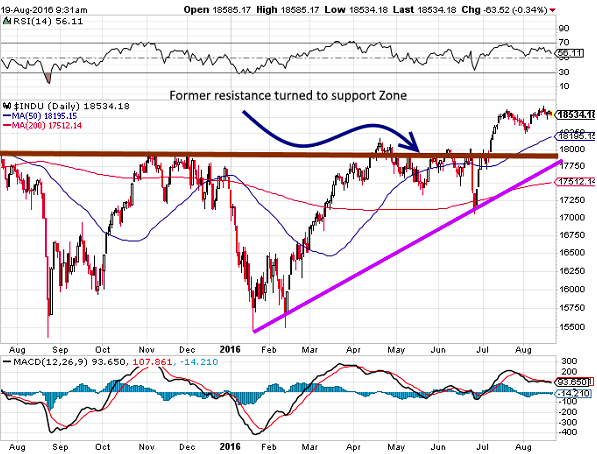

When mainstream media starts to jump on the bandwagon, we start to get nervous and so it is more likely that the Dow will test 17,800-18,000 ranges before surging to 20,000. This zone represents former resistance that has turned into support as indicated in the chart above.

Conclusion

Popular media outlets are just too bullish, and they are turning bullish after the market has surged to new highs; from a contrarian perspective, this is a negative development. The trend in all the indices is up, so the longer term outlook is still bullish. Forget Dow 20,000 for now; the Dow is more likely to trade lower than surging to new highs.

Consider the hour-glass; there is nothing to be accomplished by rattling or shaking; you have to wait patiently until the sand, grain by grain, has run from one funnel into the other.

John Christian Morgenstern

Economics is far simpler than most in academics or government would have you believe. To make accurate predictions all you really need is an honest appreciation of the self-interest that is at the heart of free market transactions and an ability to understand how regulations that attempt to “correct” these realities don’t work. This is certainly the case with the completely predictable slow-motion train wrecks that are the signature U.S. domestic policy experiments of the last eight years: Obamacare and Federal Reserve stimulus. From the start, I issued countless commentaries on why both would fail spectacularly. The jury has started to come back on Obamacare, and the results are a disaster. And while the verdict on the Fed’s policies has yet to arrive in similarly stark terms, I believe that its failure is just as certain.

Economics is far simpler than most in academics or government would have you believe. To make accurate predictions all you really need is an honest appreciation of the self-interest that is at the heart of free market transactions and an ability to understand how regulations that attempt to “correct” these realities don’t work. This is certainly the case with the completely predictable slow-motion train wrecks that are the signature U.S. domestic policy experiments of the last eight years: Obamacare and Federal Reserve stimulus. From the start, I issued countless commentaries on why both would fail spectacularly. The jury has started to come back on Obamacare, and the results are a disaster. And while the verdict on the Fed’s policies has yet to arrive in similarly stark terms, I believe that its failure is just as certain.

As I explained in my July 30, 2012 commentary “Justice Roberts is Right: The Plan Won’t Work,” the central flaw (among many others) in Obamacare is that it incentivizes younger, healthier people to drop out of insurance coverage while encouraging older, sicker people to sign up. The result would be a pool of insurance participants that would guarantee losses for those providing coverage. That’s exactly what we are seeing.

After only four years of operation, there is now wholesale defection by insurance companies to abandon the Obamacare marketplace because they are hemorrhaging money faster than just about anyone predicted. To believe that any other outcome was possible would have been the equivalent of believing in the Tooth Fairy.

According to the Wall Street Journal, the four biggest U.S. health insurance companies, Anthem, Aetna, UnitedHealth and Humana are losing hundreds of millions of dollars on their Obamacare plans. And since these companies can’t be compelled to operate a business that loses money, all four have significantly scaled back their offerings. UnitedHealth has already exited 31 of the 34 states where it sells ACA policies. Humana is now offering coverage in just 156 counties of the 1,351 counties in which it was active a year ago. The latest shoe to drop came this week when Aetna said it would stop selling Obamacare plans in 11 of the 15 states where it is currently active (Bloomberg Businesweek, 8/17/16).

It’s no secret why the companies are losing so much money. Enrollees into the new plans take out far more money in benefits than they pay in premiums, despite the fact that premiums have increased substantially. That’s because the pool of insures in the Obamacare plans differ sharply from those that exist in the private marketplace. Why this has happened should have been stunningly obvious to anyone. To quote from my 2012 commentary:

“…the ACA makes it illegal for insurance providers to deny coverage to anyone for any reason. This allows healthy people to drop insurance until they actually need it without incurring any risk. It’s like allowing homeowners to buy fire insurance after their houses burn down.” Given the high cost of insurance, the law allowed millions to take a free ride.

I argued then that penalties that would hit those who remained uninsured were insufficient to compel them to make an uneconomic decision. This was the same rational that was used by Chief Justice Roberts when he ruled that the plan was constitutional. He argued that since the penalties were not high enough to compel behavior, they should be seen as constitutional “taxes,” not unconstitutional “penalties.”

Similarly, by guaranteeing that no one could be denied insurance for any reason, and that the sick would pay the same premiums as the healthy, the plans have sucked in lots of people guaranteed to take out more in benefits than they pay in premiums. Add these factors together and you get the recipe for guaranteed losses. In retrospect, it is simply incredible that supposedly smart people argued against this outcome while the law was being drafted and passed.

At this rate, there may essentially be no private companies offering insurance through the exchanges within a few years. This will mean that unless president Clinton (Trump has promised to repeal Obamacare) passes a new law requiring companies to lose money for the good of the country (not too outlandish a possibility), or if the Supreme Court allows massive increases in the penalties for not buying insurance (thereby creating the coercive force that Justice Roberts argued was absent in the original law), then the government itself will have to step in and absorb the losses that are currently hitting the private insurers. At that point, Obamacare will become just what its critics always thought it was: an enormous new unfunded and open-ended government entitlement.

While the flaws of Obamacare were incredibly easy to see, so too are the flaws in the Federal Reserve’s stimulus policy. What’s amazing to me is that more people aren’t able to see through it as easily.

Although few realized it while it was occurring, everyone now sees that the dotcom mania of the late 1990’s was a bubble that had to end badly. Most also realize now, as they didn’t realize then, that the housing bubble of the early years of the 21st Century (which took us out of the 2001 Recession) was a bubble created by the Federal Reserve’s unprecedented low interest rates in those years.

But while we have gotten better at recognizing bubbles after they have burst, we are still totally blind to the ones that are currently forming. Ever since the Recession of 2008, the Federal Reserve has held interest rates at zero and has injected trillions of dollars into the financial markets through its quantitative easing policies. These moves have clearly inflated prices in the bond, stock, and real estate markets, an outcome that was an expressed aim of the policies. There is also clear evidence that these asset prices will come under intense pressure if interest rates were allowed to rise.

Recent history confirms this. Back in January of this year, just a few weeks after the Federal Reserve delivered the first rate increase in nearly a decade, the stock market entered a free fall. We had the worst opening two weeks of the calendar year in stock market history. The bleeding stopped only when the Fed backed off significantly from its prior rate hike projections. Since then, the market action has been clear to see: stocks rally when they believe the Fed will keep rates low, and then fall when they think they will rise. And so the Fed has played a continuous game of footsy with the market…forever hinting that hikes are possible but never actually raising them.

But given how close the economy could be trending toward recession, can anyone seriously believe that the Fed will risk kicking a potential recession into high gear by actually delivering another rate increase? It should be clear that it won’t, but somehow the best and brightest on Wall Street appear convinced that it will. Perhaps this explains why hedge funds have so consistently underperformed the market thus far in 2016.

To me, the fate of the Fed’s stimulus policy is as clear as that of President Obama’s failed experiment in healthcare. It’s a disaster hiding in plain sight. The stimulus itself has so crippled the U.S. economy that it can now barely survive without it. As it limps along the crutch must grow ever larger, as the support it provides weakens the economy to the point where it becomes too small to provide adequate support. But rather than acknowledging that the Fed’s policies have failed (an admission that any honest proponent of Obamacare should make), the proponents of stimulus are doubling down.

Earlier this week, John Williams, the president of the San Francisco Fed and widely believed to be a close confidant of Chairwoman Janet Yellen, issued an economic letter on the FRBSF website that lays the foundation for much greater stimulus for years to come. The centerpiece of Williams’ suggestions is that he would like to see the Fed raise its inflation target past the current 2%, and that the government be prepared to run much larger deficits to combat persistent economic weakness. In other words, ramp up the dosage of the medicine we have been taking for years, even though that medicine hasn’t worked. This shows a stunning inability to recognize a failed policy when it is staring at them in the face.

Absent from his analysis is any understanding that the stimulus policies of the past two decades may have actually created the conditions that have locked our economy into a perpetually weakened state. By preventing needed contractions, debt reductions, investment re-allocations and rebalancing, perennial stimulus has frozen in place a listless economy dependent on monetary support just to tread water. Just as Federal tax policy and healthcare regulations raised the costs of healthcare to the point where another bold (and ultimately futile) regulatory framework was launched to solve the problem, new forms of stimulus are being conjured to fix problems created by prior stimulants. But since Williams does not realize the stimulus he and his fellow quacks at the Fed have prescribed actually acts as a sedative, he has misdiagnosed the resulting condition of slower economic and productivity growth and as being the new normal.

Proof of this circular logic is Williams expressed desire to use monetary policy to push up “nominal GDP,” which is simply the GDP figures that are not adjusted for inflation. What good will it do for the average citizen if we get a higher GDP number that results merely from rising prices rather than actual economic growth? While the stimulus crowd likes to suggest that rising prices are a required ingredient for real growth because they encourage people to go out and spend before prices rise further, their asinine theory is completely unfounded. The entire purpose of deflating nominal GDP is to separate actual growth from rising prices. Pretending the economy is growing by targeting nominal GDP will only stifle real economic growth that might actually solve the problems the Fed still has no idea it created.

It is somewhat heartening that there is a greater recognition now of the inherent flaws in Obamacare. Hopefully such realizations will soon be widely raised about our current stimulus experiments, and that these insights will arrive in time to change course. However, confidence should be extremely low on that front.

Read the original article at Euro Pacific Capital

…related: The ‘Deep State’ Is Becoming Increasingly Desperate

Google, Ford and GM are all agressively looking to enter the ride sharing scene using self driving cars but the current king has beat them to it. Uber announced that later this month In Philadelphia, users can phone for a fully automated ride.

More on change from Mike: List of Rapid Technological Changes Here Now!

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair