Timing & trends

In their latest announcement, the FED attempted to prop up the stock market. They attempted to sound hawkish, however, the market paid not any heed to it. The FED annulment was reflected in a manner that lead the way to the dollar tanking and precious metals rising. Silver has industrial uses as well as monetary ones, which will come to the forefront as the gold bull market progresses.

In their latest announcement, the FED attempted to prop up the stock market. They attempted to sound hawkish, however, the market paid not any heed to it. The FED annulment was reflected in a manner that lead the way to the dollar tanking and precious metals rising. Silver has industrial uses as well as monetary ones, which will come to the forefront as the gold bull market progresses.

“The Fed has had numerous opportunities to normalize rates over the past two years and have squandered them all,” said Peter Hug, global trading director at Kitco Metals Inc. in an emailed note after the FED statement, reports Market Watch.

Although a few analysts believe that the FED has kept hopes alive for a September 2016 rate hike, the market does NOT believe so. The FED funds futures points to a status quota the next meeting, as a majority (88%) of traders believe that the FED will NOT move in the next meeting of September 2016.

In my opinion, the judgment of FED members notwithstanding, what choice do they have but to leave the possibility of a rate hike on the table? They would look like total buffoons, if they reversed course now. This sudden spike in the price of silver has definitely caught a lot of analysts off guard. I am suggesting that the fact that the FED is now less likely to raise rates after the Brexit and the fact that the dollar has been slipping a bit lately are the primary reasons for silver’s rise…

The dollar bulls, who were optimistic on the FED had pushed prices above the 97 levels, however, after the FED’s decision, prices tanked and rightly so.

Another reason for an increase in silver prices is the surge in demand due its “industrial” application. “Silver has (more room to run) because silver is increasingly used in solar panels now. Something like 10 percent of demand comes from solar panels. Solar panels are a growing source of demand for silver, so you have got an additional attraction for silver as well, as a commodity investment and also industrial usage,” Jeremy Wrathall, mining team leader at Investec, told CNBC on Monday, July 4th.,2016

The chart of the dollar index shows that for more than a month, it has remained in an uptrending channel. However, recently the dollar broke down the channel, signifying that the traders do not buy the hawkish derrick.

The break of the channel has a target of close to 95.2, which also coincides with the 50% retracement of the total rise from the lows of 93. However, if the dollar continues to tumble, it has a small support at 94.7 levels, post which, it will retrace the complete move.

The fall in the dollar will reflect in the rise of silver. I believe that silver is on the cusp of a rally and hence, we shall concentrate on the silver charts.

The silver bulls have seen a stupendous run from the lows of around $13.73 during the start of the year to the highs of $21.2 in early July 2016. However, I believe that the bull run in silver will continue after a small consolidation.

The chart of silver shows that it is consolidating in a range of 19.3 on the lower side and 21.2 on the higher side. If silver manages to break above the range, its pattern target is 23. However, I believe that silver will scale the level of 23 and thereafter, reach the levels of 26 by the end of this year.

Historically, August has been a rough month for stock investors. In the last 20 years, the stock market’s performance has been down -1.3% in August, according too Bespoke.

“I would expect August to be mediocre or weak,” said Don Townswick, director of equities at Conning.

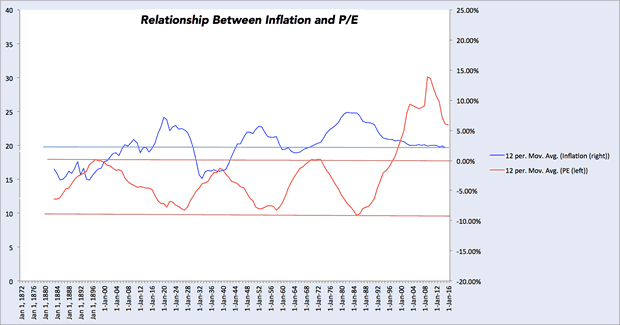

Similarly, David Kostin, Chief equity strategist at Goldman Sachs is bearish on the markets. The current price-to-earnings (P/E) ratio expansion cycle has reached the third largest, ever, in history.

Consider that the current rise in stocks has come on the back of poor earnings, dismal growth and huge financial risks on the horizon. The crash is imminent, and I believe that the fall this August 2016 and September 2016 will sow the seeds for the larger decline, that I have been talking about.

I expect the equity markets to follow their negative record of August and September and I believe that the decline, which will be moderate in the beginning will end with a sharp slide.

Conclusion

I believe that as “The Global Financial Reset” of the ‘monetary system’ begins, there will be an increase in the demand for silver relative to the increase in the demand for gold. Gold is an ‘Establishment’ metal relative to silver. There are no Central Bank that are ‘hoarders’ of silver, anywhere or anymore. There is no one in the ‘Establishment’ who considers silver, as money, as of yet!

History is going to repeat itself in August and we will see a sharp fall in the months of August 2016 and September 2016. The traders are accepting that the FED will not raise rates anymore this year and they are placing their bets accordingly.

Our short call on the dollar was timed to perfection, and I believe that the short call we give on the stock market will also produce similar results. Get ready for more such profitable trades in the following months.

Get my analysis and trades at: www.TheGoldAndOilGuy.com

related:

A clear, concise and gripping interview between Michael Campbell and the highly praised Greg Weldon – On The Brink of Soaring Move Up In Gold & Silver

The U.S. electric power sector burned through a record amount of natural gas in recent weeks, a sign of the shifting power generation mix and also a signal that natural gas supplies could get tighter than many analysts had previously expected.

The EIA reported a surprise drawdown in natural gas inventories for the week ending on August 3. The reduction of 6 billion cubic feet (Bcf) was the first summertime drawdown since 2006. Natural gas spot prices shot up following the data release on August 4, although they fell back again shortly after.

Natural gas consumption patterns are much more seasonal than for oil. Demand tends to spike in the winter due to heating needs, and then drops substantially in the intervening months, particularly in the spring and fall. Between March/April and October/November, natural gas inventories build up as people need less heating, and that stockpiled gas is then used in the next winter.

So it comes as a surprise that after a record buildup in inventories this past winter, the summer has seen a much lower-than-expected buildup in storage. And last week’s drawdown, the first in over a decade during summertime, says quite a bit about the shifting energy landscape. The EIA says this is the result of two factors: higher consumption from electric power plants, and a drop off in production.

The U.S. is and has been in the midst of an epochal transition from coal-fired electricity to natural gas and renewables, a switch that will take many more years to play out. But the effects are already showing up in the power generation mix. Utilities have rushed to build more natural gas power plants over the past decade, and now with so many online, demand for gas has climbed to new levels.

Just a few weeks ago, on July 21, the U.S. burned through 40.9 billion cubic feet, the highest volume on record, according to the EIA. And in late July, the power burn exceeded 40 Bcf/d three times due to a hot weather. Nine of the ten highest power burn days on record took place last month, with the other one occurring in July 2015. Average consumption of 36.1 Bcf/d in July of this year was 2.7 Bcf/d higher than a year earlier, and 1.5 Bcf/d higher than the previous high reached in July 2012.

The high rates of consumption from the electric power sector are contributing to tepid growth in inventories this summer. This comes on the heels of a massive buildup in inventories last winter, and heading into summer the expectation was that huge storage levels would keep natural gas prices at rock bottom levels, perhaps for years. But that doesn’t look like it will come to pass.

While high demand is keeping natural gas from being diverted into storage in large amounts, the other main reason that natural gas inventories are not building up as much as previously thought is because of a supply-side issue: natural gas production is actually falling after years of steady increases. Natural gas prices have traded below $3 per million Btu since the beginning of 2015. U.S. gas drillers continued to ratchet up production through 2015, however, creating this past winter’s inventory glut. But the resulting downturn in prices has now made drilling unprofitable in many areas. On top of that, the oil price crash has ground oil drilling to a halt, which means that the natural gas produced in association with oil has also come to a standstill. The upshot is that natural gas production is now falling in the United States. The Marcellus Shale, the most prolific shale gas basin in the country, saw production peak in February at 18.5 Bcf/d. Since then output has declined 3 percent. In August, the EIA expects gas production from the Marcellus to fall by another 26 million cubic feet per day.

Of course, this stuff is cyclical. The first summer drawdown in inventories in a decade means that natural gas markets are now tighter than many analysts thought only a few months ago. Falling production and rising demand could lead to steeper drawdowns in inventories this coming winter. The effect of that will be to push up spot prices, which could induce more drilling once again.

By Nick Cunningham of Oilprice.com

...also: A clear, concise and gripping interview between Michael Campbell and the highly praised Greg Weldon – On The Brink of Soaring Move Up In Gold & Silver

Our leaders hate to talk about them and the media doesn’t ask but that doesn’t stop the time bomb of unfunded pensions from ticking.

…also: A clear, concise and gripping interview between Michael Campbell and the highly praised Greg Weldon – On The Brink of Soaring Move Up In Gold & Silver

The First Rebuttal website has coined a term that gets to the heart of an increasingly dysfunctional system: The too-big-to-fail stock market. The general thesis is that most major countries are over-leveraged to that point of maybe being unable to survive a garden variety equities bear market – and are doing their best to avoid finding out. Here’s First Rebuttal on the effects of such a prop-up-asset-prices-at-any-cost policy:

The structural economic problems of stalled incomes, peaked debt and welfare make operational expansion i.e. sustainable growth extremely difficult, which has led to investment concentration in secondary equity markets. And that means the higher valuations simply represent higher risks.

The offshoot is that as such a large concentration of total asset value is dependent on the market, it becomes necessary to maintain the market at all costs. The market has become too systemically important to allow it to fail. And that means policymakers have changed the function of the market. The market left to its own devices is a consequence of the underlying economy. Today, however, the market is being used as a (false) portrayal of the underlying economy. It is intentionally using the logical fallacy of confusing cause and effect.

That is, the thermostat is no longer meant to reflect the temperature inside the house, its only use is to convince you the house is warm. That means policies are being targeted at manipulating the thermostat rather than keeping the furnace hot. The consequence is a spiraling of resource misallocation, furthering the structural breakdown of economic activity making it ever more important to keep the market looking strong. The market is no longer a market as we understand the term.

The upshot: Markets no longer serve their intended purpose of efficiently allocating capital. Since capitalist wealth creation depends on that function, today’s world can no longer be called “free” or “market-based” in any meaningful sense.

The article illustrates this phase change with a chart showing equity P/E ratios over the past century-and-a-half which reveals a dramatic spike beginning in the 1990s – that is, when Alan Greenspan and his successors at the Fed decided that the big banks had to be protected from the folly of their own mistakes.

So what does this mean? First, while headlines continue to convey a sense of normality, under the surface the system is rotting away. Good jobs are becoming scarce and capital is being directed towards things that will never generate enough cash flow to pay off the related debt. (Rising) financial asset prices are increasingly disconnected from the (falling) value of underlying assets.

The evidence of this is everywhere, from pension plans that lie about their funding levels, to corporations that report non-gap earnings and are rewarded with higher share prices, to governments that report plunging unemployment rates while citizens leave the workforce in droves.

It’s no longer possible, in short, for most people to tell what’s real and what’s not. And since markets’ main function is to reveal underlying truths, it’s not a surprise that governments have decided to hijack the message.

…also: A clear, concise and gripping interview between Michael Campbell and the highly praised Greg Weldon – On The Brink of Soaring Move Up In Gold & Silver

Is Real Estate shakey Ozzie Jurock reveals all the numbers behind the real estate markets, volume, prices and trends…. plus Hot Properties!

Don’t miss Mike’s Editorial – Coming Soon: Another Quick Fix For Our Economic Mess

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair