Gold & Precious Metals

This could be the year that the mainstream investor finally pushes the gold market over the edge. While a fraction of investors continue to acquire a lot of physical gold, the mainstream investor is the key to driving the gold market and price going forward.

Why? Because the diehard precious metal investors don’t have the sort of leverage as do the mainstream investors, which account for 99% of the market. I have stated several times in articles and interviews that it will be the surge of gold buying by the mainstream investor that will finally overwhelm the gold market.

This next chart shows just how much leverage the mainstream investor has on the gold market. When the Dow Jones Index fell a lousy 2,000 points during the first quarter of 2016, mainstream investors flooded into Gold ETF’s & Funds. This continued into the second quarter, including the surge in buying after the BREXIT “Leave Vote” this past Friday:

According to the data put out by Nick Laird at Sharelynx.com, total transparent global gold holdings increased nearly 20 million oz (Moz) since the beginning of 2016. Nearly half of that figure, 9.7 Moz (supposedly) went into the GLD ETF. This is an amazing amount of gold as it represents 41% of total global mine supply.

For those investors who don’t trust the amount of gold backing these Gold ETF’s, I don’t either.

also:

Michael’s Shocking Stat show the amazing numbers of guns, ammo and body armor non- military bureaucrats are buying – Mind Blowing Gun Stats

We are on the precipice of a food fight among 7 billion people, and potash will be right at the center of it.

If you can add 200,000 people every day to the global population and account for a significant loss of farmland at the same time, you can begin to understand the dire food situation facing the planet. This is why potash is so important: It’s the fundamental element that everyone takes for granted, despite the fact that a projected 7.7 billion lives will depend upon it by 2020.

No commodity is more fundamental than potash — and there is a lot of pressure riding on an element that many people aren’t even familiar with. Of the key commodities taken for granted, potash is on the top of the list.

The challenge for farmers — and for the world — is to increase crop yields on less land, which is being lost to climate change and increasing urbanization. This means not only steady demand for the three main elements of fertilizer — potash, phosphate and nitrogen — but significantly higher demand.

“A growing population needing to be fed from a limited amount of arable land makes fertilizer and particularly potash a robust commodity,” Potash Ridge President and CEO Guy Bentinck told Oilprice.com. “Additionally, as the middle class grows, the demand for higher-end food increases, and with that the demand for potash and related fertilizers increases.”

For such a critical element, it’s hard to believe that potash remains so elusive. It took a high-profile US$40-billion hostile takeover attempt of Saskatchewan’s Potash Corp., which failed, by major miner BHP Billiton in 2010 for even the Wall Street Journal to decide to figure out what all the fuss was about.

Potash, and various potassium-containing compounds are used to fertilize crops as a necessary resource for the growth of plants. In many regions of the world, there are large potash-bearing deposits from ancient sea beds that dried up millions of years ago. Most potash comes from these sources and is separated from the salt and other minerals and then graded into a form that can be used to make fertilizer.

So even if you haven’t heard of it, Potash is so big that it eludes radar — until the giant miners start aggressively positioning themselves for bigger pieces of this pie.

If you’re still not sold on potash, consider this: As far as commodities go, though it’s been a tough couple of years, Potash outperformed gold, silver, copper and oil and gas in 2015, and this year, as its cycle comes full circle, it’s back by popular demand.

The Potash Playing Field

This is a huge playing field with some of the biggest miners in the world — all vying for market share.

Russia, Belarus, China, Germany, the U.S., Israel, Jordan and China are all major potash miners, with Canada currently holding the top position for the commodity–producing 11 million tons last year and the year before, compared to Number 2 producer Russia’s 7.4 million tons.

Canada is also home to the world’s largest fertilizer company by capacity — Potash Corporation of Saskatchewan, or Potash Corp. — the target of BHP Billiton’s long-running covetousness.

The U.S. came in at 770,000 tons of potash production in 2015, mostly from New Mexico and Utah, which have a total of seven potash mines. Most of the U.S. potash goes to the fertilizer industry, while small amounts are diverted to the chemical industry. The four mines in New Mexico are controlled by two companies — Intrepid Potash (NYSE:IPI) and Mosaic (NYSE:MOS). In Utah, it’s Intrepid again, Compass Minerals (NYSE:CMP), and Canadian explorer Potash Ridge (TSX:PRK) with its Blawn Mountain project. Potash Ridge’s Valleyfield project in Quebec is projected to produce 40,000 tons of SOP (sulfate of potash) annually, with construction slated to begin later this summer.

The movements among the big potash players make huge market ripples. In 2015, a US$500-million loan deal from the Industrial and Commercial Bank of China and China Construction Bank with Russian potash major Uralkali, effectively gave China greater control over global potash production. Uralkali accounts for about 20 percent of the world’s potash production.

China — a major demand center for potash — now has immense influence in the potash market, and is both a major producer and a major importer because demand is far greater than domestic supply. The Chinese potash contracts that are typically made in February every year — but delayed this year — are a critical annual point for producers.

Not all Potash is Equal: Some Potash is Posh

As Mr Bentinck has noted above, the middle class is growing, and they want higher-quality, healthier food, which means cash crops. This demographic change is leading to a health food revolution for which potash is the primary element. But not all fertilizers are equal in this game.

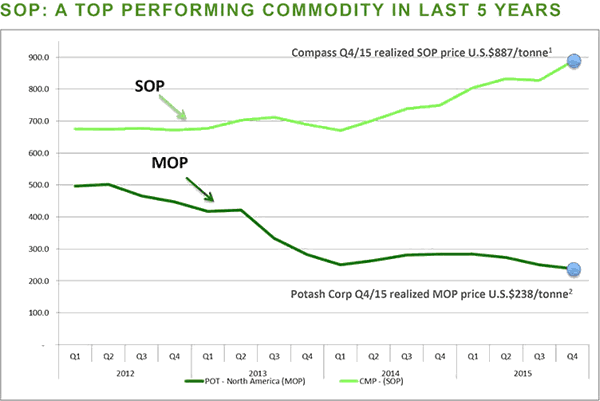

The two most common forms of fertilizer are MOP (muriate of potash) and SOP (sulfate of potash). Right now, MOP is the most common; but while it’s good for some crops, it’s not good for others, and it can create environments that are detrimental to some crops, primarily due to high levels of chloride.

SOP, on the other hand, is the premium end of potash. It’s the posh potash. It improves both the quality and yield of a crop, while at the same time making them more drought, frost, insect and disease-resistant. It’s been said that SOP also improves the taste of the food by improving its ability to absorb nutrients.

The other problem with MOP today is that the market is temporarily over-supplied and prices have dropped, which has prompted some more junior miners — such as Potash Ridge in Quebec and Utah–to swoop in to take advantage of the opportunity for the less common SOP. Potash Ridge, which is one of the fastest-growing juniors on the posh potash scene, says SOP “continues to be one of the best performing commodities across all sectors, which realized prices in North America exceeding US$880 per ton in the fourth quarter of 2015.”

Riding the Cycles: The Potash Catalysts Are Already Visible

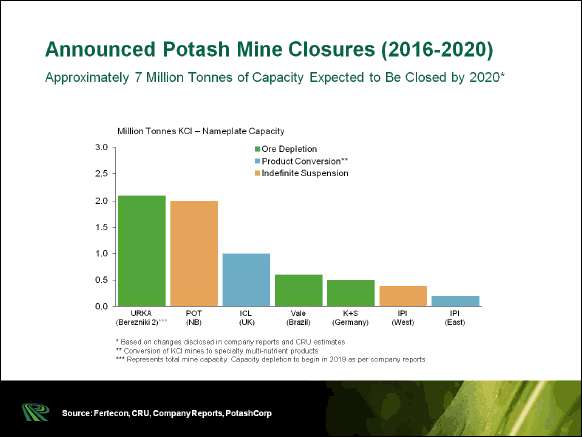

Fertilizer demand is set to increase over the long-term. While globally we consumed 35.5 million tons of potash in 2015, the next four years should see this rise to 39.5 million tons.

The catalysts for potash are already clear and present. The grain cycles that affect fertilizer are coming back around now; the long overdue, but now occurring monsoon season in India should relieve several quarters of slumping demand in this major demand venue; a health food boom is increasing demand for the SOP form of potash; long-term global population figures stand starkly against plummeting farmland figures; and major potash production is coming offline in the near-term, making even more room for the juniors to break in.

Remember — grain crops are cyclical, so buying when they are down is when the big investors make all their money. Just because corn and other key crops that rely on potash have been down, adversely affecting fertilizer revenues — doesn’t mean they’re out. Corn has many booms and busts; buy on the bust, right before the next cycle boom.

One of the biggest immediate-term catalysts will be the planned moves by giant Potash Corp., it’s Canadian competitor Agrium (NYSE:AGU) and Mosaic to take potash production offline in order to rebalance the supply side of the market — something everyone’s been trying to get OPEC to do with oil to no avail. This means that in the next few months we should see potash prices recover, so the window to get in on the downside here is only open a crack.

The last great cycle for potash was 2004-2008, but prices for MOP have dropped 60 percent since then, while prices for SOP have doubled since then.

Image Source : https://oilprice.com/images/tinymce/2016/Pash1.jpg

{kind=link}

While MOP is experiencing a glut right now that could soon be rebalanced, supply for SOP is tight, making the margins for SOP increasingly attractive, and the juniors breaking into a high-reward versus risk bargain.

“The global SOP market appears to be under-supplied, with current tightness of the market demonstrating demand for additional global capacity outside China,” according to Neil Fleishman, Director of Research for Green Markets.

To Re-Cap: This is Why We Like Potash

There is massive opportunity here in the uncertainty of this market, for which the fundamentals absolutely must re-balance in the medium-term.

And while the MOP fundamentals might take a bit longer to fully rebalance as the global supply-demand picture recovers, the premium-priced posh potash, SOP, is the emerging darling that gives us cause to look more bullishly at the break-out juniors here.

By James Stafford of Oilprice.com

also:

Josef Schachter on Next Crude Pric Plunge Has Commenced

Quotable

“The decentralization of power away from hubristic central planners is exactly what the world needs more of. The centralization of power is the source of the very risky environment we’re in, not the decentralization.”

Mark Spitznagel

Commentary & Analysis

Abandon Ship – Brexit implications

Well, the Brits decided to leave. Those of us who prefer smaller government to bigger; prefer more liberty to less; prefer greater economic freedoms than fewer; prefer entrepreneurism to big business cronyism; and prefer sovereign nation states to supra-national authorities are very happy right now. Once this transitionary phase (of elite panic, which is just priceless to watch) and market volatility is behind us, the UK economy will most likely rock and roll; freed from the shackles of 13,000 edicts and regulations drawn up by wine and cheese eaters inside labyrinth in Brussels—aka EU headquarters; it’s a Franz Kafka wet dream for feckless bureaucrats.

Return of the UK fishing fleet might be good for jobs. A Cambridge/Oxford research park to challenge Silicon Valley would be a nice start. Five and ten man manufacturing shops across the UK freed from the burden of regulation and massive overhead could lead to something extraordinary. The realization there is no reason for the talented financial people of London to climb aboard the Frankfurt-Titanic will surprise. I think you get where I am going here…

The rationales for the UK leaving have been hashed over pretty well, especially now with the gift of hindsight. Despite seemingly the entire staff of the Financial Times still in denial, with commentary bordering on bitter, there is a clear broad rational for all of this; I return to a commentary from Citron Zoakos once again, from May 2016:

In recent years, economists have debated fruitlessly over the importance or lack thereof of financial imbalances and excessive debt. To no avail, they have sought answers to the question of what happens if these problems are not addressed by policymakers. Now we know: Voter insurgencies happen; revolts happen that topple the established policymaking elites.

In short, the inability of authorities to deal with the credit crisis (not to suggest an easy task) and their decision to “save” the global financial system through massive injections of liquidity (at the expense of rising public debt) to save legacy (read: crony capital protected assets) and apply severe financial repression (zero and negative interest rates) has benefited owners of capital through the massive inflation of financial assets; yet those owners of labor (regular people who do real things for money—build stuff and serve) have wallowed with high unemployment, no return on savings, a decline of their largest asset (their home), and loss of real income. The UK lesson is a microcosm of this strident difference in world view between the elites and the average guy on the street (in every developed country it seems)—those in London (insert New York) love the EU (insert US Federal power); those serfs in the Northern England hinterlands (insert US fly-over country) do not.

Here’s the rub, again from Mr. Zoakos, and it dovetails on those who are urging the EU to re-invent itself immediately [my emphasis]…

In Europe at the moment, both the owners of capital and the owners of labor oppose vigorously these types of structural reforms (severe entrepreneurial structural changes) But without such reform, the politics of introducing Brady-style debt relief conferences will be reduced to struggles between those two groups over who will to pay for debt relief: the owners of capital or the owners of labor. The only outcome of debt relief without revolutionary, entrepreneurial structural reforms in the markets for goods and services (rather than in the labor market) will be the typical European class struggle. History has shown how dangerous this can be.

Is this message clear to the one who matters most, German President Angela Merkel? And even if it is, is it too late to reform given the turmoil inflicted on the lives and cultures of the EU states? How does one trust President Merkel given the debacle she magnified with her unconditional support of refugees who are destroying thousands of years of Western culture in very short order?

A list of some off the cuff implications of Brexit (this is far from exhaustive):

- Germany lost a key ally in helping reform the EU with more market-based solutions.

- German will likely have to take up the fiscal slack after losing the UK’s estimated 18 billion dollar euro per year commitment to the EU.

- The EU loses its military muscle with the UK exit. Rebuilding that will be costly.

- Henry Kissinger’s comment about Germany becomes increasingly apt: “Germany is too big for Europe and too small for the world.”

- The EU loses clout to help shape world affairs with the UK gone.

- Regardless of Germany’s honest and proper attempts to right the ship with appropriate reform, it will be sniped at by others inside the zone who will complain the Germans are exerting too much “control.”

- Anti-EU forces in many other countries (e.g. France, Italy, Spain, Netherlands, Austria, Sweden, and Denmark) have been emboldened. Italy’s constitutional referendum in October will be a major test.

- The pan-European capital markets project will most likely be abandoned without UK involvement. Thus, the ECB will have to continue its stop-gap measures. How much more can the German government expose German taxpayers?

- The euro loses a significant amount of status as a world reserve currency challenger to the US dollar; we will likely see a big shift in structural reserve allocations among global central banks away from the euro.

“In the wrong hands,” Leto said, “monolithic centralized power is a dangerous and volatile instrument [Frank Herbert].” So more than likely it’s unraveling can be expected to be equally dangerous and volatile.

At the very least we should expect elevated levels of market volatility in the months ahead. And we shouldn’t be surprised if the whole single currency experiment comes unglued. At some point, it will no longer be in Germany’s best interest to hold this thing together.

Stay tuned.

Jack Crooks

President, Black Swan Capital

Also, don’t miss Jack Crook’s post Brexit vote interview wih Michael Campbell:

It Was Incredible, Extraordinary, How To Take Advantage of Exciting Currency Volatility

If you think Britain’s exit from the European Union is going to be a shock to the economy, wait till you see the potential dire straits of Europe’s most vulnerable banks.

I can discuss this topic with precision because today’s the day that our Weiss Ratings division has updated the first-ever, independent and objective safety ratings of the largest global banks in the world.

We are independent because, unlike Moody’s, S&P or Fitch, we accept no compensation whatsoever from the rated institutions. Unlike those Big Three agencies, we also never give the institutions a “preview” of their ratings, never allow them to “appeal” ratings they disagree with, and never suppress publication at their request.

That’s why the U.S. Government Accountability Office (GAO) found that the Weiss Ratings of insurance companies greatly outperformed those of Moody’s, Standard & Poor’s, A.M. Best and others in warning consumers of future failures.

It’s also probably why a study reported in The Wall Street Journal demonstrated that the Weiss Stock Ratings outperformed those of all major Wall Street banks and research organizations.

Average Rating of Eurozone Banks: Absolutely Astounding

We apply these same principles — conflict-free research and accuracy — to our global bank ratings, and here are the big-picture results, based on March 31, 2016 data …

-

Among banks in North America, the average Weiss Safety Rating is C+.On our rating scale, which is similar to school grades, that’s “fair,” a passing grade.

-

In the Asia and Asia/Pacific region, the average rating is C+ (“fair”).

-

And surprisingly, big banks in the Middle East and Africa, despite troubles in certain regions, merit an average grade of B (“good”).

-

But …

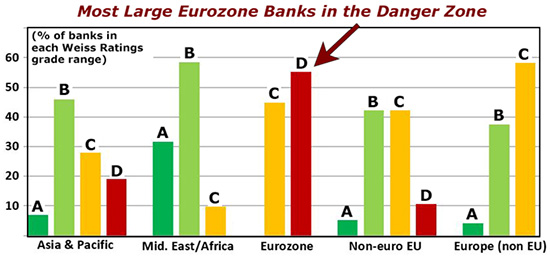

In the eurozone countries, the average Weiss Safety Rating of the institutions we cover is D+ (weak) — a red-light warning, especially in the wake of last week’s Brexit vote.

The chart below shows exactly how the grades are distributed among banks outside of the Americas:

The eurozone has the most astounding concentration of large weak banks I’ve ever seen in all the 45 years since I founded my research and ratings company:

Among the banks we cover in the region, 55.3% get a Weiss Safety Rating in the D range (D+, D or D-), while the balance (44.7%) get no better than Cs.

This contrasts with Asia and the Asia-Pacific, where 46% of the institutions are in the B range and only 19% are Ds. And it contrasts even more sharply with the Middle East and Africa where 58.5% are Bs and there are no Ds.

What’s most illuminating of all, however, is the contrasts inside Europe itself:

-

If a bank is based in an EU country that does not use the euro (such as the U.K., Sweden and Poland), it’s less likely to have financial weaknesses than eurozone countries like Spain, Italy, France or even Germany.

-

And if a bank is based in European countries outside of the European Union entirely, such as Switzerland or Norway, it’s even less likely to have problems. (You can see this in the last group of bars in the chart above.)

Evidently, the European Union has not been good for the financial stability of most banks. And the euro currency has been even more damaging.

I repeat: The eurozone has the worst concentration of large, weak banks I’ve seen since we began scrutinizing bank financials back in 1971.

What About Prior Banking Crises?

No, it’s not the first time I’ve seen many banks in the danger zone. In the 1980s, for example, almost one-third of the U.S. banks and S&Ls we rated were in that category. And in the years that followed, 3,700 failed.

Nor is it the first time that megabanks have been vulnerable to failure. In 2007, for instance, we issued D ratings for some of America’s largest … we got frequent flack for our low grades … and later, after they failed, occasional accolades.

Rather, what’s so surprising in this instance is that the AVERAGE grade, including ALL of the institutions in the eurozone that we cover, is so low.

Of course, the preponderance of Ds doesn’t mean that dozens of banks will start failing tomorrow. Nor does it mean that every single one with a bad grade will ultimately go under. But it does signal three things:

-

A higher-than-average probability of failure among large eurozone banks.

-

Systemic, eurozone-wide financial weakness that could cripple Europe’s economy, with far-reaching global consequences.

-

Major vulnerabilities to a political or external shock, such as Brexit.

Why Isn’t This Headline News?

Yes, I know. All the headlines right now are about the Brexit vote. That’s what has lit the fires, stirred the markets and padded media company revenues.

But the Brexit story could eventually die down. This one will not. Quite to the contrary, it could emerge as one of the biggest threats to the global economy, starting from Europe, spreading to Asia, and then to the Americas.

The likely shock waves follow a path that’s similar to what my colleague Larry Edelson has described regarding the future financial difficulties of highly indebted governments: First Europe. Then Japan. And ultimately the United States.

And now, this data reveals a side of the debt pyramid that’s often out of the spotlight, hidden behind inflated ratings, or simply covered up. Our goal is to break through those unfortunate barriers to your knowledge and to give you the tools you need to make prudent, informed decisions for your money.

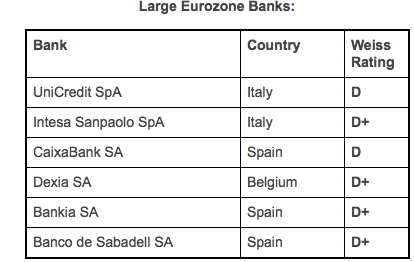

The 6 Weakest Among Large Eurozone Banks

So let me start by naming some names. Among the largest eurozone banks, here are the six weakest:

All six of these institutions merit a rating of D+ or lower, which we consider to be a danger zone.

All have at least $200 billion in total assets.

And all have multiple reasons for their weaknesses …

Low liquidity, especially in the case of UniCredit SpA, Intesa Sanpaolo SpA, CaixaBank SA and Bankia SA.

Large bad loans almost across the board, except perhaps for Dexia SA.

Poor asset growth, also nearly across the board, with the possible exception of Intesa Sanpaolo SpA and Banco de Sabadell SA. Plus …

Operating losses at one of the six banks — Dexia SA.

So many troubles! And despite a seemingly never-ending series of capital infusions from governments that are, themselves, still mired in excess debts!

Which Eurozone Countries

Have the Weakest Banks?

Five of these six banks are based in Italy and Spain. One is in Belgium.

Meanwhile, most people think that German banks are very strong. But that’s rarely the case.

Deutsche Bank merits a Weiss Safety Rating of only C+; both Commerzbank and Deutsche Postbank get a C-; and IKB Deutsche Industriebank, a D-.

According to the German financial watchdog Bafin, this is especially worrisome in the wake of the Brexit vote. “The biggest banks would have the biggest problems,” says Bafin President Felix Hufeld. “They have the most activities in, and with, London.”

Specifically, Deutsche Bank and Commerzbank are the German banks with the largest business dealings in Britain.

Your Action Plan:

-

Be sure to find out the Weiss Safety Rating of the institutions you rely on to safeguard your money and your finances, including not only banks but also credit unions and insurance companies.

-

Find out which ones are among the safest in your state.

-

If your money is in the danger zone, seriously consider moving it to a safer place. This applies to major regions in trouble like the eurozone as well as individual institutions.

-

Also look up the Weiss Investment Ratings for your stocks, ETFs and mutual funds.

To have all of these resources at your fingertips, plus much more, go here.

Plus, as always, continue to build cash reserves to help prepare for unexpected black swan events that can be very disruptive to global financial markets — and very destructive to your investments.

Best wishes,

Martin D. Weiss, Ph.D.

with Gavin Magor,

Weiss Ratings Senior Analyst

Jack Crooks of Black Swan Capital calmly walks us through the run-up to, and the aftermath of one of the wildest currency moves in history as the Brexit panic wipes $2 trillion off world markets – Jack’s advice on how to handle this dramatic, volatile and frightening markets for some is a must.

Don’t miss Michael Campbell’s blunt energetic comment on why Brexit is just another domino and not the main event.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair