Currency

Quotable

“Panics do not destroy capital. They merely reveal the extent to which it has been previously destroyed by its betrayal into hopelessly unproductive works.”

John Stuart Mill

Commentary & Analysis

Mr. Xi Jinping’s Deflation

Today’s short story starts with China’s investment overhang…or malinvestment for lack of a better term…

In the chart below from Morgan Stanley, it suggests China hasn’t changed much, i.e. it is still trying to keep growth alive through its tried and true capital investment model.

The chart above reveals each new dollar invested has a decreasing stimulative impact on GDP; i.e. the efficiency of capital employed in China has fallen dramatically. Is it a classic case of malinvestment?

“Malinvestment is a mistaken investment in wrong lines of production, which inevitably lead to wasted capital and economic losses, subsequently requiring the reallocation of resources to more productive uses. Austrians believe systemic malinvestments occur because of unnecessary and counterproductive intervention in the free market, distorting price signals and misleading investors and entrepreneurs. For Austrians, prices are an essential information channel through which market participants communicate their demands and cause resources to be allocated to satisfy those demands appropriately. If the government or banks distort, confuse or mislead investors and market participants by not permitting the price mechanism to work appropriately, unsustainable malinvestment will be the inevitable result.”

Wickipedia

Given the secular decline in both consumer demand and globalization itself, recent attempts by the Chinese authorities to revive its capital investment growth model (stimulate exporters), evidenced by another massive surge of credit, seems likely to fail.

Source: Leto Postcripts, Criton Zoakos

[Note: The G-7 is concerned; but the latest pronouncements suggest our heroes don’t believe much can be done on a coordinated basis. It brings to mind the “rats scurrying off a sinking ship” analogy. If trade growth continues to plummet there is little doubt trade tensions and currency manipulations will grow.]

…it would be silly to try to predict China’s political future, or suggest there will be some major crisis, but there is a roadmap for Leninist party states past. China is approaching a critical stage…

“…revolution and seizure of power →transformation and mobilization of society → consolidation of state power and extension over all aspects of society → extraction of resources and capital from society for state purposes → bureaucratization and “Brezhnevization” of state power → adaptation and limited pluralism to cope with stagnation and ossification → ?”

David Shambaugh, China’s Future

…the case for increasing pluralism anytime soon does seem on the horizon given the massive malinvestment and increasing authoritarian rule by Chinese President Xi Jingping…

“Since Xi Jinping came to power at the Eighteenth CCP Congress in November 2012, the reign of the Conservatives has continued. Xi has proven to be a very anti-liberal leader and he has overseen an even greater intensification of the repression evident since 2009. There has been an unremitting crackdown on all forms of dissent and social activists; the internet and social media have been subjected to much tighter controls (see chapter 3); Christian crosses and churches are being demolished; Uighurs and Tibetans have been subject to ever-greater persecution; hundreds of rights lawyers have been detained and put on trial; public gatherings are restricted; a wide range of publications are censored; foreign textbooks have been officially banned from university classrooms; intellectuals are under tight scrutiny; foreign and domestic NGOs have been subjected to unprecedented governmental regulatory pressures and many have been forced to leave China; attacks on “foreign hostile forces” occur with regularity; and the “stability maintenance” security apparatchiks have blanketed the country. A swath of intrusive new regulations and laws concerning national security, cyber security, terrorism, and nongovernmental organizations have been drafted and enacted. China is today more repressive than at any time since the post-Tiananmen 1989–1992 period.”

“Many members of Jiang Zemin’s factional network, and a rising number of Hu Jintao’s, have been brought down—yet none of Xi’s own princeling associates have been touched.”

“The regime’s repression is symptomatic of its deep and profound insecurity.”

David Shambaugh, China’s Future

…a wrong turn here by China’s leaders can threaten, or at least postpone, China’s development into a normally functioning modern state…

“The key issue for nations like China at this stage of development is not just the economic growth model and its declining efficacy, but precisely the relationship between economics and politics. For economies to transition up the added-value ladder, break through the developmental ceiling, and make the kinds of qualitative transitions necessary to become truly modern and developed, political institutions must be facilitative. They must cease being ‘extractive’ states and become what scholars Daron Acemoglu and James Robinson describe in their insightful book Why Nations Fail as “inclusive states.” This requires tolerance— even facilitation— of autonomous actors within society.”

David Shambaugh, China’s Future

…more muddling through decreases the chance China will escape the “middle income trap” which has plagued developing economies in the past? Just and FYI: The theory of convergence so talked about by emerging market mutual fund salesman is more the exception than the rule. [Does anyone remember the acronym BRICs?] …the probability of “Japanification” of the Chinese economy is rising. Consider the similarities…

“During the 1980s it appeared Japan as the Creditor Superpower was going to gobble up the world with their powerful export machine and massive current account surpluses rolling in. Then a little thing called the US stock market crash in 1987 changed the game. Dollar credit flowed from the global system triggering an improvement in the US current account balance (first gold box left in chart below) which was followed by a US recession. This came as the Japanese yen was appreciating in value, thanks to the G-7 Plaza Accord to pressure the yen higher because of all those Japanese exports.

“The litany:

1) Japan’s very hot stock market broke in 1989.

2) Then its extremely over-priced real estate bubble started its collapse (remember when the Imperial Palace in Tokyo was worth more than the entire state of California).

3) Japanese authorities did all they could in the form of stimulus to try to keep air in the bubble.

a. They pumped more money into the stock and property markets in order to revive the wealth effect for domestic consumers.

b. They subsidized export companies to keep exports flowing (but the world’s major consumer—the US economy—was entering recession and not there to buy).

c. They lowered interest rates to zero.

d. They continued massive fiscal stimulus by building infrastructure across the country.

“But, it didn’t work. The massive dislocations caused by artificial channeling of credit within the Japanese economy in order to focus almost entirely on building a global export machine created the malinvestment that has taken years to work off precisely because the Japanese economy was so imbalanced—production versus consumption. Attempts to change this model were scant at best; instead they kept morbid companies alive, and forced its consumers to save thanks to artificially low interest rates. “

Jack Crooks, “The Japanese-China Parallel: Eerie and Scary Combined,” Forex Journal July 2010

At the very least, we would expect another wave of deflation to flow out of Asia. Directly impacting the emerging markets in terms of trade through falling commodity prices and leading to another flow of capital from the periphery (developing world economies) to the center (developed world economies); it would be a negative reinforcing feedback loop for the emerging markets (risk off and possibly contagion)…

The deflationary impact to the developed world from China would be more implicit (as the brunt of falling commodities prices has already been discounted to a large degree) seen through falling final goods and material prices. Interestingly, despite negative interest rates in Japan and Europe, those countries should receive their fair share of money flow from Asia because increased deflation will push up real yields in both places; i.e. nominal yield minus inflation rate.

But given the estimated $3 trillion emerging market dollar denominated debt, the dollar will likely win the global money flow game: 1) a risk bid for the world reserve currency; and 2) yield on the premise the Fed will be the only major world central bank to hike in 2016.

So, to summarize potential takeaways:

1. Increased Chinese stimulus will most likely increase deflationary pressures down the road.

2. Increased repression and external belligerence (Can you say: South China Sea?) from Chinese President Xi will likely prolong the downturn in the Chinese economy.

3. Despite the excitement about oil being back at $50 per barrel, the global macro environment may not be a fertile backdrop for a continued run in commodity prices.

4. The currency order under this scenario: Dollar is most favored; other developed economies second; commodity currencies third; emerging market currencies last

Editor’s Note: I am preparing a detailed special report and specific trading/investing ideas as related to the scenario summarized in today’s missive; along with a voiced-over PowerPoint presentation. It will be used as a promotion for our new service: Key Market Strategies. I should have that available early next week.

Jack Crooks

President, Black Swan Capital

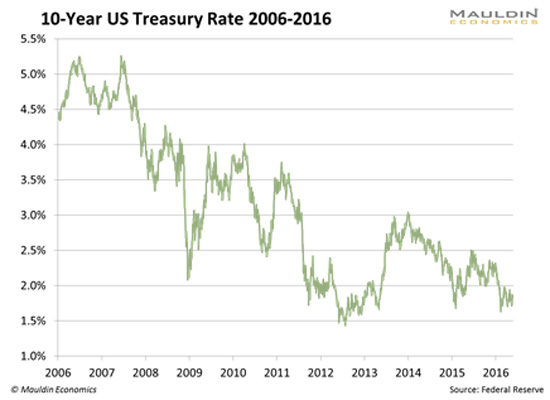

This one is going to cause some cognitive dissonance, because many of the people you trust and rely upon for financial insights are bullish on bonds and think that interest rates will go even lower.

I do not.

I think they will go higher, and I have a fairly well-reasoned case.

First, a chart of 10-year yields over the last 10 years:

And going back a lot further than that:

Let’s step through this bit by bit.

Inflation

If you are a bondholder, what is your greatest enemy?

Inflation.

Think about it. If you own a 10-year piece of paper yielding 2% and inflation is running at 3%, you actually have a real yield of -1%. That doesn’t sound very good. As it stands right now, real interest rates in the 10-year space are just slightly above zero.

For those of you who have a little bit of background in this, interest rates have a nominal and a realcomponent. The nominal component compensates you for inflation. The real component reflects the supply and demand for loanable funds.

When there is an excess supply of loanable funds (like after the Fed has printed a lot of money), interest rates will be depressed, as they are now. When there is an excess demand for loanable funds, like when there are lots of investment opportunities, interest rates will rise.

This is all academic. But the academic stuff works sometimes, too.

So here is a chart of inflation (CPI):

You can see that it is starting to turn up. Yes, inflation is low, but it’s the direction that counts.

So why would you buy a bond when inflation is getting ready to ramp up?

Worse, there are plenty of indications that inflation is going to run further. 10 years ago, inflation was running about 3–4%, but people were saying that we didn’t really have inflation, because we didn’t have wage inflation.

Well, guess what: now we are starting to have wage inflation. People are very noisy about this with respect to the minimum wage, and by the way, after the last year or two, almost nobody pays the minimum wage of $7.25 an hour anymore. Walmart, TJ Maxx, and many others have all raised wages on the low end.

This feeds into expectations, where people come to expect more and more pay increases. And when people demand and receive pay increases, they have more disposable income and drive up the price of goods and services.

So if we didn’t have “real” inflation before, do we have “real” inflation now?

Supply

Leaving aside the anti-immigration stuff for a moment, I’m not a fan of Donald Trump. For one reason and one reason only: the debt.

A few weeks ago, in Forbes, I argued that a President Trump would be very bad for the bond market. Let’s talk this through.

Donald Trump wants to cut taxes. He wants to cut the top marginal rate from 39.6% to 25%, and all the other tax rates as well. He wants to make it so most people don’t pay taxes at all. The “cost” of this tax plan is about $1.3 trillion, but if we dynamically score this and say that there will be economic growth as a result of it and the government will take in more revenue (the supply-side argument, which I agree with), let’s just assume it’s a trillion-dollar tax cut.

Trump also wants to…

- Build a wall

- Deport people

- Build infrastructure

- Have Trumpcare

- Increase defense spending (exclusive of military adventures)

Let’s say that on the expense side, this costs an additional $1 trillion (Trump is not a small-government conservative).

So the deficit, which is currently at about a half-trillion, goes to $2.5 trillion, or about 15% of GDP, the highest in history.

The debt is little more than an abstraction to most people, but the mechanics of what happens when a government runs a large deficit is that the treasury will increase the size of its bond offerings. So if the US Treasury is offering $20 billion of bonds every quarter, and the deficit doubles, it will be offering $40 billion of bonds every quarter. There’s an increase of supply, and without a corresponding increase in demand, investors will demand price concessions and interest rates will rise.

This is the argument Robert Rubin was making about the debt in the 1990s. And he was right.

Under a Trump regime, the volume of bonds that would be offered for sale would skyrocket. Never mind Trump’s creditworthiness in general, and the fact that he’s made an entire career of screwing creditors. I would not want to lend money to the US government under such circumstances.

Under Hillary Clinton, the situation would be better, but only marginally, because over time, our entitlement programs will grow more and more expensive (and untenable).

Conclusion

I have about eight other bullet points to make, but I try to keep The 10th Man succinct. Let’s be clear—the bond market is as overpriced as it has ever been, right at the moment that the fundamentals have completely broken down.

Where does the exposure live? With you, the retail investor.

There are hundreds of billions in household assets in fixed-income mutual funds, retirement and nonretirement. After a 1% rise in interest rates, people will discover what the meaning of “duration” is.

But that is a topic for another time.

Jared Dillian

Click here for anintroductory offer

related from Larry Edelson: “Something Has Radically Changed”

“It seems wise to consider the possibility of a substantial S&P 500 Index drop in coming months”

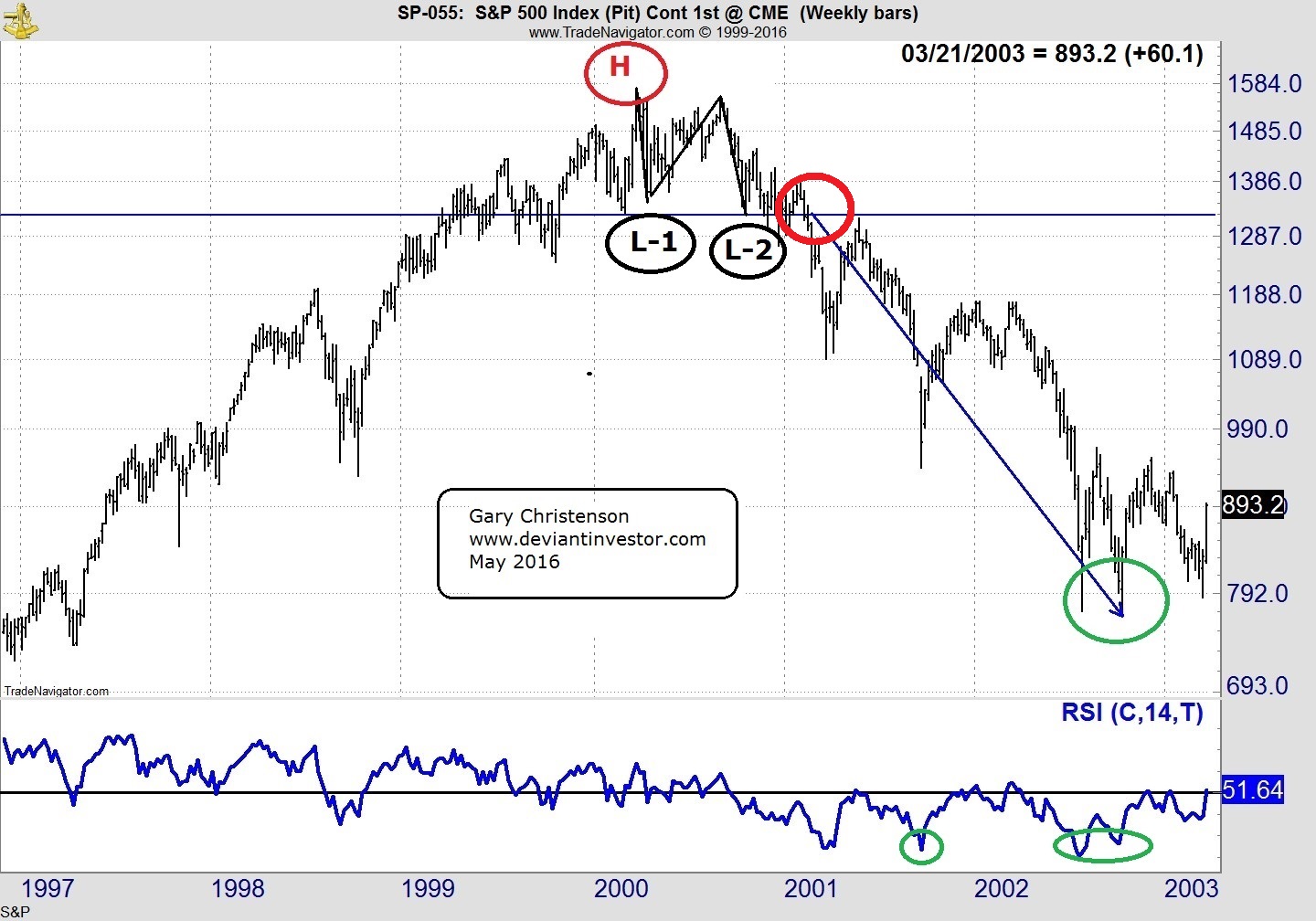

There are patterns in markets. Yes, the Fed and High Frequency Traders influence markets, but we can learn from past patterns in the S&P 500 Index.

Using weekly data, the S&P made a high in March 2000, fell to an initial low in April, rose, and fell to a second low in October 2000. It rallied and fell below the second low in February 2001 – never to look back. From high to final low took 931 calendar days and price fell about 51%.

Examine the following chart and note the H, L-1, L-2 and a final low.

A similar pattern is visible after the 2007 top. Using weekly data, the S&P made a high in October 2007, fell to an initial low in November, rose, and fell to a second low in January 2008. It rallied and fell steeply below the second low in September 2008 – never to look back. From high to final low took 511 calendar days and price fell about 58%.

Examine the chart for the 2015 version of the S&P high to low progression.

A high is clearly visible, along with a first low and a second low. The S&P has not yet fallen below L-2 at about 1804, but when it does, look out below. Of course this time could be different, our central banks might “save” the S&P, market corrections might have been banished into the dustbin of history, the incredibly excessive global debt may not matter, and the Easter Bunny might be real, but none of those seem like good bets.

SPECULATION based on the last two cycles: These are not predictions – just possibilities based on history. As I said, this time might be different, the incredibly high S&P might be levitated until past the election so that a “status quo” friendly candidate can be elected President in November 2016, and the Easter Bunny …

Time from high to low in the 2000 cycle was 931 days – about 2.5 years. The 2007 cycle was deeper and quicker – 511 days or about 1.4 years. Assume the range for the 2015 cycle is longer than the last cycle, since it appears to have an extended and rounded top – so guess that high to low takes about 2 – 2.5 years – which suggests a low about 2017Q2 – 2017Q4.

Prices from high to low in the 2000 cycle declined 51%. The 2007 decline was slightly larger at 58%. Assume a 50 – 60% decline in this cycle. That puts the S&P in the vicinity of 850 to 1050. Of course this time might be different…

IN ADDITION:

Using the Relative Strength Index as shown at the bottom of the charts, we can see that the 2000 cycle bottomed with RSI readings (scale 0 – 100) in the 20s on the weekly charts and about 27 on the monthly chart.

Those RSI readings were as low as 16.45 weekly in October 2008, and 18.1 on the monthly in March 2009.

Those RSI readings in the 2015 cycle have only dropped to the 30s on the weekly and to about 49 on the monthly. Either this time is very different, or the RSI reading must drop far lower to indicate a lasting bottom. Expect to see monthly RSI readings around 20 in 2017 – 2018 at a much lower low in the S&P 500 Index.

Of course this time might be different, but it seems wise to consider the possibility of a substantial S&P 500 Index drop in coming months. Today – May 20 – is the one year anniversary of the S&P 500 market top last year.

Gary Christenson

The Deviant Investor

related – Martin Armstrong has a unique view: The Dow & The Confusion

Marc Faber is bullish on gold and oil and gas stocks.

Marc Faber is bullish on gold and oil and gas stocks.

Given the abundant speculation about the Federal Reserve and interest rates, Marc Faber told CNBC last week he believes the Fed is closely watching the market reaction to its intimations it may raise rates in June. If the market reacts very negatively, it could hold off raising rates, while a relatively stable market could signal the OK to the Fed to raise the rate by a quarter-point.

Generally, higher interest rates support a higher U.S. dollar and weaken demand for gold as gold does not pay any interest.

However, Faber says he believes that the Fed will not raise interest rates next month. “My view is that in June, they [the Fed] will not move; they will not increase rates,” Faber stated. “The market will begin to perceive that the Fed wants to support active markets, which they have stated on numerous occasions before,” he added.

In that environment, “gold, which from now on may correct, maybe 5% or so, will start to move up again,” Faber said.

Faber recommends a diversified portfolio. “To own some real estate makes sense, to own some equities makes sense, to own some cash and bonds probably makes sense, and to own some precious metal makes sense.”

But Faber’s view is some sectors will do better than others. “I can see more money printing in the future, which will lift some sectors,” Faber said and went on to name them: “The most attractive assets in my view are gold shares and oil and gas shares. I think they still have significant upside potential this year.”

Marc Faber is author of the Gloom Boom and Doom Report

related: Two Overlooked Streaming Stocks with Huge Upside Potential

“How many “emergency” “secret” meetings do the central planners around the world need to have before the citizens of the respective countries begin to fully understand and take notice that something is very, very wrong?” “The G-20 central planners have scheduled an “emergency” meeting for summer 2016.”

A Crisis Unlike We Have Seen In Human History

May 19, 2016

I sat down with John Rubino of Dollar Collapse to discuss the current state of our economic world. In a very lively conversation, we hit some of the more pressing items of the day. John has done a fantastic job of documenting the demise of the dollar since he co-authored ” The Collapse of the Dollar” with James Turk back in 2004. John’s insights and analysis are top shelf and he should be on everyone’s list of people to follow.

How many “emergency” “secret” meetings do the central planners around the world need to have before the citizens of the respective countries begin to fully understand and take notice that something is very, very wrong? This year alone there have been several off-calendar meetings with, at least, one more now added to the docket.

The G-20 central planners have scheduled an “emergency” meeting for summer 2016. What will the topics be? Could it possibly be the fact the global economy is on the verge of total collapse? With the Baltic Dry Index, Shanghai Containerized Freight Index, not to mention commodities, all spiraling out of control to the downside, do you think there may be a reason for these people to be concerned? My guess is they could care less and are simply meeting in order to determine how the remaining wealth, in their respective countries, will be divided as the global economy continues grinding to a halt.

If one simply looks at the following line-items, it is clear for anyone to see something is about to hit the fan and it’s not anything anyone wants hitting the fan.

- 45 million people in the U.S. on food stamps

- some estimates as high as 10 million refugees flooding into the European Union

- non-stop wars of aggression involving NATO, Russia, Syria and several other countries

- financial crisis that began in 2008 has not been addressed and the problems that started that year have grown larger and far deeper

- banking system in the European Union, especially Italy, is under enormous stress due to faulting/fraudulent accounting

- Federal Reserve balance sheet at $4 TRILLION – U.S. debt at $20 TRILLION and counting

- United Kingdom/Britain and the Brexit movement that is taking root

- U.S. Presidential candidates, Donald Trump and Bernie Sanders, garnering global attention as the citizens of the U.S. seek alternatives to the current embedded criminal politicians.

- Japan instituting a Negative Interest Rate Policy (NIRP) for their sovereign bonds – Japan has basically been in a recession for over 20 years

- China is manufacturer to the world and with economies slowing down or shutting down, there is no reason to manufacture products

These are just a few of the items that are currently hampering growth for individual citizens and individual Western nations. Currently, there are just too many holes that need to be filled and the central bankers are losing control and the people are losing faith in the narratives they are being fed. Once faith is lost, en masse, the show will become a lot more interesting and a lot more dangerous.

In order for the show to remain at arm’s length, people need to understand their role in what is happening. We must have certain items in our possession at all times in order to avoid being swept away in the wave of economic collapse. Will this be a wave like you would see on TeeVee? Of course not. The “wave” was launched in 2008 and has been gathering momentum ever since. It will simply wash over your remaining wealth and leave you even more destitute than in your current situation.

Silver, gold and lead are must-haves for the rising tide of uncertainty. Long term food storage and the usual storable items that make your house a home need to be at the top of the list. There is plenty of information to help you get your house in order and there has never been a better time to keep the shelves stocked than right now.

Will this implode tomorrow or next week or next month? Who’s to say? What can be said is this: it is happening – your wealth is being drained at this moment. The central planners are absolutely terrified of something, otherwise, the continual “emergency” “secret” meetings would stop.

When an animal senses danger, they become irrational, their behavior becomes erratic and their actions unpredictable. This is exactly what we are witnessing with the central planners around the world. It is time to begin taking these signs seriously and putting into place personal protection, at all levels, in order to weather the storm and don’t forget the popcorn.

related: The Inevitability Of Unintended Consequences

Rory Hall, Editor-in-Chief of The Daily Coin, has written over 700 articles and produced more than 200 videos about the precious metals market, economic and monetary policies as well as geopolitical events since 1987. His articles have been published by Zerohedge, SHTFPlan, Sprott Money, GoldSilver and Silver Doctors, SGTReport, just to name a few. Rory has contributed daily to SGTReport since 2012. He has interviewed experts such as Dr. Paul Craig Roberts, Dr. Marc Faber, Eric Sprott, Gerald Celente and Peter Schiff, to name but a few. Visit The Daily Coin website and The Daily Coin YouTube channels to enjoy original and some of the best economic, precious metals, geopolitical and preparedness news from around the world.

The author is not affiliated with, endorsed or sponsored by Sprott Money Ltd. The views and opinions expressed in this material are those of the author or guest speaker, are subject to change and may not necessarily reflect the opinions of Sprott Money Ltd. Sprott Money does not guarantee the accuracy, completeness, timeliness and reliability of the information or any results from its use.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair