Personal Finance

Today in Canada there is little doubt where the tenants are heading: straight into Alberta, Saskatchewan and, to a lesser extent, Manitoba, which form an economic powerhouse in the heart of our nation.

Today in Canada there is little doubt where the tenants are heading: straight into Alberta, Saskatchewan and, to a lesser extent, Manitoba, which form an economic powerhouse in the heart of our nation.

Real estate investing is a bit like duck hunting. You have to set your aim to “lead” the duck to allow for the distance the duck will fly while your shotgun pellets are getting to it. If you don’t, you’ll always be shooting where the duck was, not where the duck is.

It is similar in the real estate market. Knowing where your potential tenants will be in the future is vital. Values grow where people go and people go where the jobs grow.

Since your returns depend on people with jobs that are likely staying, it is important to find out about livability, vacancy rates and new job creation.

Multi-family real estate values thrive on fully tenanted buildings and, if you want capital appreciation, you need to know where the tenants are flocking. I stress capital appreciation because low capitalization rates today make it difficult to earn returns.

Vancouver’s expensive apartment-building market is (finally) seeing price resistance this year, as investors balk at paying record-high “per door” prices (the average price of a Vancouver rental apartment is now north of $220,000) and suffering cap rates in the 3 per cent range. As a result, first-half sales this year flatlined after years of growth.

But Vancouver investors have a ready option, and it is to the immediate east.

Today in Canada there is little doubt where the tenants are heading: straight into Alberta, Saskatchewan and, to a lesser extent, Manitoba, which form an economic powerhouse in the heart of our nation.

Big players in the multi-family market, such as real estate investment trusts (REITs), have already figured this out. For instance, Boardwalk REIT of Calgary and Toronto-based Canadian Apartment Properties REIT spent an average of $33 million a month in 2012 just in Western Canada, and they are not too picky about what they buy as long as it cash flows.

The reason is clear. Yield and return. According to the REALpac/IPD Canada Annual Property Index, over the past 12 months real estate outperformed public equities at 5.9 per cent, bonds at 4 per cent and inflation at 1 per cent. The total returns varied between six Canadian cities surveyed for the index, but the biggest returns were in Calgary, up 17.4 per cent; and Edmonton, up 17.1 per cent.

OK, where should you hunt in 2013 and beyond?

Well, certainly research where the big boys – and tenants – have gone and are likely to go. Here are three places that we have been recommending to our Jurock Real Estate Insider subscribers.

Calgary and Edmonton

Calgary and Edmonton currently have the lowest apartment vacancy rates in Canada, at 1.2 per cent. Calgary led all big cities with an average 7.2 per cent rent increase in the past year (Alberta has no rent controls). According to Statistics Canada’s quarterly population estimates, in-migration from other provinces and immigration totals about 68,000 persons per year arriving in Alberta, with most heading for the larger cities.

Interprovincial migration to Alberta in the first quarter of this year was the highest in nearly 40 years at 13,400, including 2,500 from B.C. and 6,000 people from Ontario.

The lure is jobs. Calgary’s unemployment rate is 5 per cent, and it is 4.6 per cent in Edmonton, second lowest in Canada after Regina and Saskatoon.

With stiff competition for apartment blocks investors can also look at buying condominiums and renting them out.

CMHC estimates that 32 per cent of Edmonton condos are being rented out, for example, a total of nearly 13,000 as of the last count. The vacancy rate for condos is 2.5 per cent and the typical rent for a two-bedroom is $1,268 per month – or about 20 per cent higher than the overall apartment market. Similar trends are seen in Calgary.

Think of the ducks: your tenants are flying into Alberta and that is where you should be investing.

Saskatoon

With an apartment rental vacancy rate of 2.6 per cent Saskatchewan’s biggest city is a prime landlord investment market.

Saskatoon is drawing a lot of young people – even from Vancouver – despite its wintry weather. With 6,100 migrants arriving last year – a record high – the city now has 272,000 residents. It also has the strongest economic growth of any city in Canada this year, as forecasted by the Conference Board of Canada, which pegs its growth at 3.7 per cent this year and 3.8 per cent in 2014. As a comparison, Vancouver will see about 2.3 per cent GDP growth both this year and next.

Saskatoon is bursting with jobs, with an unemployment rate at 3.9 per cent. Housing starts are at a 30-year high; building-permit values hit a record of $1.1 billion last year; and the average weekly wage is around $910, compared with $869 in much-more-expensive B.C.

West is best

Are there other cities to buy in? Absolutely. Western Canada is the place to be. The power shift east to west is seriously underway. We at Jurock predict the oil pipelines will be built. The LNG pipelines will be built. The LNG terminals will be built. More people will retire in the West. More immigrants, particularly business immigrants, will come to the West. So, buy Prairie properties with good cash flows, good “B” locations and caring tenants. Watch the vacancy rates, watch the big boys but, above all, watch where the ducks will be flying.

From the Western Investor, August 2013

Ozzie Jurock is a Vancouver-based real estate investor and publisher of the Jurock Real Estate Insider. He is a contributor in Donald Trump’s book, The Best Real Estate Advice I Ever Received. Reach Ozzie at oz@jurock.com or ozziejurock.com.

Is it the right time to buy Vancouver Real Estate or not?

This is a question that I am asked on a near daily basis by clients, friends, family, even my barista.

My answer has been consistent since day one; Yes, with strings attached.

In the case of an owner occupied property, which one plans to reside for at least the next 7-10 years; Yes, the right time to buy is today. Once you (& your Realtor) locate the property that works for you on all levels then what the market is doing on that specific day is of little consequence in the long term. Market values are like a small yo-yo oscillating on a very large escalator slowly and steadily moving upward.

Key considerations when buying an owner occupied property;

- Location

- Layout

- Age

- Size

- Condition (can you afford renovation)

- Room for growth

- Recreational amenities

- Schools

- Distance from workplace

- (potential) Suite revenue

- the list goes on…

If you are able to find the right property for yourself (& your family) that hits high notes on the variables above, Take Action!

Getting all of these variables aligned is something that takes dedication from not only yourself but also the team of industry professionals you surround yourself with. The process can often consume a few months or more, and for some of my past clients result in over 100 viewings. This is more than enough to juggle without also trying to ‘time the market’ on that perfect home.

The Vancouver market is sometimes referred to as a roller coaster, however the long steady climbs are rarely followed by as a large of a drop as folks tend to live in fear of. The historic numbers demonstrate that a detached home in Vancouver has risen from 13K 40 years ago to ~1.1M today. Not in a straight line mind you. However if you never leave the market straight-line appreciation is not a concern.

One must keep in mind a few keys things;

Very rarely is an accurate short term market prediction made.

The MLS #’s are a poor indicator of what is happening today in the market, as ‘today’ refers to sales that were negotiated on average 3 to 4 months prior. Take the MLS data with a grain of salt. It is part of the picture for sure, but not the exclusive indicator.

Where then to get the most accurate data?

The front lines; Realtors, Mortgage Brokers, Appraisers, etc.

If you suspect industry insiders may be biased…well perhaps we are; This would largely be due to our intimate knowledge of the numbers, and influenced further by positive personal experiences with our own homes and investment properties. Many of us are also invested for the long haul, i.e. a 20yr timeline for a single property.

I suggest that concerns about short term price fluctuation not be a key factor in your own decision to buy. In the long run you will win by owning, not by sitting on the sidelines.

Real Estate is a get-rich-slow program.

It is all about finding a place you can call home for the duration and weaving your family into the fabric of a community. Perhaps the timing will prove poor initially – whether you buy this month, next year or three years from now. However 7-10 years from the date of purchase you will most likely be glad that you bought into whatever market you did. It is difficult to find many homeowners who regret buying in 2003, just as in 2003 it was hard to find those with regrets over buying in 1993.

Hindsight is significantly simpler than foresight. Focus on the big picture, know that time fixes pretty well every Real Estate mistake as far as values are concerned, and having a place to call home in a community that works for you is perhaps the more important short term and long term goal.

Thank you.

Dustan Woodhouse – dustan@ourmortgageexpert.com

For regular market updates follow me on twitter @DustanWoodhouse

Confidence among U.S. consumers unexpectedly declined in November to a seven-month low as Americans grew more pessimistic about the labor-market outlook.

The Conference Board’s index fell to 70.4 from a revised 72.4 a month earlier that was stronger than initially estimated, the New York-based private research group said today. The median forecast in a Bloomberg survey of 78 economists called for a November reading of 72.6.

The drop in sentiment helps explain why some retailers such as Best Buy Co. see a need to match competitors’ discounts this holiday-shopping season. More employment opportunities and wage gains would help lay the groundwork for a pickup in household purchases that make up about 70 percent of theU.S. economy.

“The economy just has not performed very well this year and has been disappointing relative to what most people were hoping for and expecting through the course of the year,” saidStephen Stanley, chief economist at Pierpont Securities LLC inStamford, Connecticut. “It’s one thing when you have one or two years into the recovery and things aren’t progressing in the job market, but here we are four-plus years in.”

Estimates (CONCCONF) of consumer sentiment ranged from 65 to 81 in the Bloomberg survey after a previously reported October reading of 71.2. The Conference Board’s measure averaged 53.7 in the recession that ended in June 2009.

Other reports today showed applications for new-home construction increased in October and property values rose in September.

Building Permits

Building permits increased 6.2 percent to a 1.03 million annualized rate following September’s 974,000 pace, according to the Commerce Department. Housing starts data for September and October were postponed until Dec. 18 due to the government shutdown.

The S&P/Case-Shiller index of property prices in 20 cities increased 13.3 percent from September 2012 after a 12.8 percent gain in the year ended in August, a report from the group showed in New York.

Stocks fluctuated, after the Standard & Poor’s 500 Index fell from a record yesterday, as investors weighed the data. The S&P 500 rose 0.1 percent at 1,804.25 at 11:02 a.m. in New York.

The Conference Board’s barometer of consumer expectations for the next six months declined to 69.3, the lowest since March, from 72.2 a month earlier. A gauge of present conditions dropped to 72 from 72.6 in October.

Labor Outlook

The proportion of Americans who said jobs would become more plentiful in the next six months declined to 12.7 percent, the lowest since November 2011, from 16 percent.

The share of respondents who said they expected a pickup in their incomes declined to an eight-month low of 14.9 percent in November from 15.7 percent a month earlier.

“When looking ahead six months, consumers expressed greater concern about future job and earning prospects, but remain neutral about economic conditions,” Lynn Franco, director of economic indicators at the Conference Board, said in a statement.

Consumer assessment of current labor-market conditions held up. More said jobs were plentiful and fewer said positions were harder to get.

Hiring picked up last month, with employers adding 204,000 workers, topping the most optimistic projection in a survey of 91 economists. Payrolls have averaged 186,300 so far in 2013, compared with 182,750 last year.

Job Openings

Job openings climbed in September to the highest level in more than five years, Labor Department figures showed last week.

Progress in the labor market will be a focus for Federal Reserve policy makers meeting Dec. 17-18 as they weigh when, and by how much, to reduce their unprecedented $85 billion in monthly bond-buying.

The central bankers “generally expected that the data would prove consistent with the committee’s outlook for ongoing improvement in labor market conditions and would thus warrant trimming the pace of purchases in coming months,” according to the record of the Federal Open Market Committee’s Oct. 29-30 gathering.

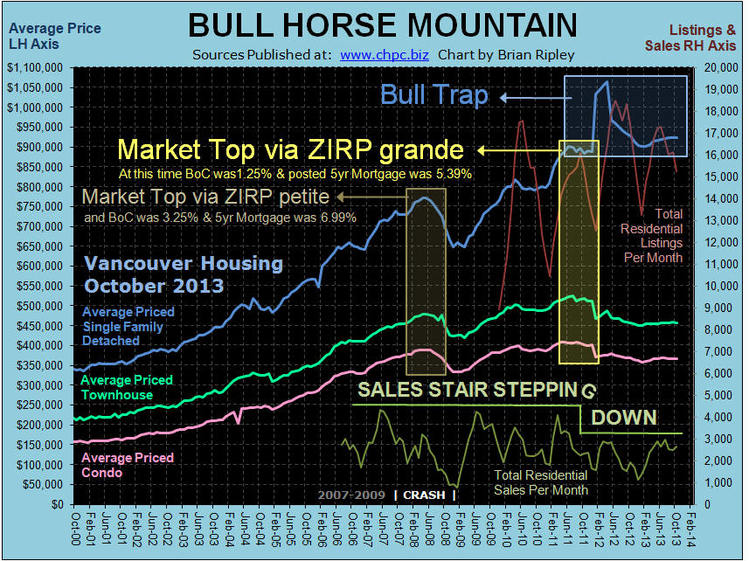

Since the blow off in April 2012, total market sales have tried and failed several times to break above the new lower stair tread of declining sales. Bulls now have to wait until the spring of 2014 before they can try to bring the rest of us along for another ride, because seasonally, the peak sales window is in late spring, early summer.

One other observation is that the ZIRP petite market top in the spring of 2008 was accomplished with a Bank of Canada Bank Rate set at 3.25% and retail banks posting a consumer 5 Year Fixed rate mortgage at 6.99%; but the sales crash was already in motion and headed towards the March 2009 pit of gloom. To get the housing market not to collapse because well over 10% of Canadian GDP is a result of the construction industry (twice the U.S. reliance) Chart Here; the BoC moved to ZIRP grande with a Bank of Canada Bank Rate set at 1.25% and the retail banks posted their consumer 5 Year Fixed rate mortgage at 5.39%. This policy of price controls on the cost of credit has not stopped sales from stair stepping lower. If you want to remove the mask from asset price discovery, do what a good appraiser does; an income approach. Imagine what a small increase in mortgage rates, say back to ZIRP petite will do to your disposable income.

Wikipedia defines a BULL TRAP as “an inaccurate signal that shows a decreasing trend in a stock or index has reversed and is now heading upwards, when in fact, the security will continue to decline. It is seen as a trap because the bullish investor purchases the stock, thinking it will increase in value, but is trapped with a poor performing stock whose value is still falling.”

“The Condo Game”

Herd mentality can be as frustrating as it is inexplicable. Once a crowd starts moving, momentum can be all that matters and clear signs and warnings are often totally ignored. Financial markets are currently following this pattern with respect to the unshakable belief that the Federal Reserve is ready, willing, and most importantly, able, to immediately execute a wind down of its quantitative easing program. How this notion became so deeply entrenched is a mystery, but the stampede it has sparked is getting more violent, and irrational, by the day.

Herd mentality can be as frustrating as it is inexplicable. Once a crowd starts moving, momentum can be all that matters and clear signs and warnings are often totally ignored. Financial markets are currently following this pattern with respect to the unshakable belief that the Federal Reserve is ready, willing, and most importantly, able, to immediately execute a wind down of its quantitative easing program. How this notion became so deeply entrenched is a mystery, but the stampede it has sparked is getting more violent, and irrational, by the day.

The release last week of the minutes of the October Fed policy meeting was a case study in dangerous collective delusion. Although the report did not contain a shred of hard information about the certainty or timing of a “tapering” campaign, most observers read into it definitive proof that the Fed would jump into action by December or March at the latest.

But while the Fed was gaining much attention by saying nothing, the Chinese made a blockbuster statement that was summarily ignored. Last week, a deputy governor of the People’s Bank of China said that buying foreign exchange reserves was now no longer in China’s national interest. The implication that China may no longer be accumulating U.S. government debt would amount to the “mother of all tapers” and could create a clear and present danger to the American economy. But the story barely rated a mention in the American media.

Instead, the current environment is all about the imminent Fed taper: the process of winding down the Fed’s monthly purchases of $85 billion of treasury debt and mortgage-backed securities. However, the crowd fails to grasp that the Fed has embarked on an impossible mission. The herd is blissfully unaware that the Fed may not be able to reverse, or even slow, the course of QE without immediately sending the economy back into recession.

In an interview this week, outgoing Fed Chairman Ben Bernanke likened the QE program to the first stage in a multiple stage rocket that gets the spacecraft off the ground and accelerates it to the point where it is close to achieving permanent orbit. Like a first stage that has spent its fuel and has become dead weight, Bernanke seems to concede that QE is no longer capable of providing positive thrust, and as a result can now be jettisoned (like a first stage) so that the remainder of the spacecraft/economy can now move higher and faster. The Chairman’s nifty metaphor provides some inspiring visuals, but is completely flawed in just about every way imaginable.

In real rocketry, when the first stage separates, it falls back to earth and is no longer a burden to the remainder of the ship. Subsequent booster rockets (which in economic terms Bernanke imagines would be continuation of zero interest rate policies) build on the gains made by the first stage. But the almost $4 trillion in assets that the Fed has accumulated as a result of the QE program will not simply vaporize into the stratosphere like a discarded rocket engine. In fact it will remain tethered to the rest of the economy with chains of solid lead.

In the process of accumulating the world’s largest cache of Treasuries, the Fed has become the most important player in that market. I believe the Fed can’t stop accumulating and dispose of its inventory without creating major market disruptions that will drag the economy down.

This would be true even if the economic rocket were actually approaching escape velocity. In reality, we are still sitting on the launch pad. By keeping interest rates far below market levels and by channeling newly created dollars directly into the financial markets, the QE program has resulted in major gains in the stock, real estate, and bond markets. Many have argued that all three are currently in bubble territory. Yet to the casual observer, these gains are proof of America’s surging economic vitality.

But things look very different on Main Street, where the employment picture has not kept pace with the rising prices of financial assets. The work force participation rate continues to shrink (recently falling back to levels last seen in 1978),real wages have declined, and since the end of 2009 the temporary workforce has grown at a pace that is 14 times faster than those with permanent jobs. Americans are driving less, vacationing less, and switching to lower quality products and services in order to deal with falling purchasing power.

But the herd is closely watching the Fed’s rocket show and does not understand that stocks and housing will likely fall, and bond yields rise steeply, once the QE is removed. The crowd is similarly ignoring the significance of the Chinese announcement.

Over the past decade or so, the People’s Bank of China has been one of the largest buyers of U.S. Treasuries (after various U.S. government entities that are essentially nationalizing U.S. debt). China currently sits on $1 trillion or more in U.S. bond obligations.

So, just as many expect that the #1 buyer of Treasuries (the Fed) will soon begin paring back its purchases, the top foreign holder may cease buying, thereby opening a second front in the taper campaign. This should cause any level-headed observer to conclude that the market for such bonds will fall dramatically, causing severe upward pressure on interest rates. But the possibility is not widely discussed.

Also left out of the discussion is the degree to which remaining private demand for Treasuries is a function of the Fed’s backstop (the Greenspan put, renewed by Bernanke, and expected to be maintained by Yellen). The ultra-low yields currently offered by long-term Treasuries are only acceptable to investors so long as the Fed removes the risk of significant price declines. If the private buyers, the Fed, China (and other central banks that may likely follow China’s lead) refuse to buy Treasuries, who will take on the slack? Absent the Fed’s backstop, prices will likely have to fall considerably to offer an acceptable risk/reward dynamic to investors. The problem is that any yield high enough to satisfy investors may be too high for the government or the economy to afford.

Little thought seems to be given to how the economy would react to 5% yields on 10 year Treasuries (a modest number in historical standards). The herd assumes that our stronger economy could handle such levels. In reality, 5% rates would likely deeply impact the financial sector, prick the bubbles in housing and stocks, blow a hole in the federal budget, and cause sizable losses in the value of the Fed’s bond holdings. These developments would require the Fed to devise a rocket with even more power than the one it is now thinking of discarding.

That is why when it comes to tapering, the Fed is all bark and no bite. In fact, toward the end of last week, Dennis Lockhart, President of the Federal Reserve Bank of Atlanta, said that the Fed “won’t taper its bond-buying until the economy is ready.”He must know that the economy will never be ready. It’s like a drug addict claiming that he’ll stop using when he no longer needs them to stay high.

But the market understands none of this. Instead it is operating under dangerous delusions that are creating sky-high valuations for the latest social media craze, undermining the investment case for gold and other inflation hedges, and encouraging people to ignore growing risks that are hiding in plain sight.

This is not unusual in market history. When the spell is finally broken and markets wake up to reality, we will scratch our heads and wonder how we could ever have been so misguided.

Peter Schiff is the CEO and Chief Global Strategist of Euro Pacific Capital, best-selling author and host of syndicated Peter Schiff Show.

Subscribe to Euro Pacific’s Weekly Digest: Receive all commentaries by Peter Schiff, John Browne, and other Euro Pacific commentators delivered to your inbox every Monday!

Don’t forget to sign up for our Global Investor Newsletter.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair