Personal Finance

“The greatest economic boom in history”

I often feel like Archie Bunker.

The “All in the Family” TV character greeted Walter Cronkite’s news with raspberry snorts, frustration and contempt. I do the same thing when I hear politicians and commentators glumly bewail the end of the United States.

Many of the doomsayers are what I call “Flat-Earthers.” They deny human evolution, ignore scientific evidence and rail against technology with religious fervor. Most are angry men who long for the good old days and would rather live in a bubble than face the real world.

While this frustrates me sometimes, I take comfort in knowing that these people will sink into political, social and economic irrelevance in the next decade or two.

In other words, they cannot stop the accelerating pace of scientific discovery and technological innovation sweeping across our great nation.

Across the United States, in kids’ bedrooms, garages, dens, dorm rooms and classrooms, in every part of the country, American genius is building the foundation for the next great leap.

They will create the greatest economic boom in history, making us more-prosperous than any civilization in human history.

Mini-Supercomputers

The revolution’s next chapter is beginning right now. Processing power that was unfathomable just a few years ago is now commonplace. The newest supercomputers in the laps of America’s brightest children and teens will become the catalyst for trillions of dollars of new wealth.

The revolution’s next chapter is beginning right now. Processing power that was unfathomable just a few years ago is now commonplace. The newest supercomputers in the laps of America’s brightest children and teens will become the catalyst for trillions of dollars of new wealth.

Last week Apple (AAPL) unveiled a desktop Mini-Supercomputer that is EXPONENTIALLY faster and more powerful than you can imagine.

For decades, these “supercomputers” were available only to a few governments, universities and large pharmaceutical and technology companies. In fact, the United States still enforces export restrictions to keep them from the hands of many foreign governments.

Now you can buy these powerful supercomputers via hundreds of websites and thousands of retail stores from Hoboken to Anchorage. The genie of computer power and processing speed is out of the bottle and in the imaginative hands of American kids and young adults.

The newest Apple supercomputers will be the first generation of faster, more powerful and eventual sentient computers that will accelerate science and innovation in giant leaps.

The great leap of computing power will create entire new industries, amazing economic efficiencies, and expand the limits of science.

Get Ready For Future Shock!

Change that would once take a century will soon unfold in a decade or less. Armed with supercomputers, a new and larger generation of geniuses will replace Steve Jobs, Bill Gates and Elon Musk. Utopian science fiction will become reality.

• Nanotechnologies will alter our minds, our intelligence, our memories, our metabolisms, our personalities and even extend our lifespans.

• Creative medical technology will vanquish illness, disease, starvation and poverty.

• New fuel technologies make the United States 100% energy-independent.

America’s next great leap will also help investors — like you and me — retire with security and wealth.

When I share my belief in America’s coming leap, friends ask how I can still be a gold bug. They ask me,

“James, don’t you preach buying gold and precious metals as a hedge against economic crisis and social chaos?”

Yes, buying precious metals to hedge against economic crisis and social chaos makes sense — but I recommend precious metals as only 10%-15% of any investment portfolio.

I also recommend gold because $150 trillion will flow into the world’s financial markets by the end of the next decade — while the supply of gold and precious metals grows just incrementally.

This vast new wealth will chase essentially the same amount of gold, silver and platinum. I buy gold and precious metals as a hedge but also as a long-term play on worldwide wealth creation.

I believe the bulk of your investment dollars should be solid technology, biotechnology, science and energy stocks.

Every Investor Should Read This Book …

My wife says I must have recommended Ray Kurzweil’s 2005 New York Times bestselling book, “The Singularity is Near,” to every person I’ve met since reading it.

Ray Kurzweil is America’s leading futurist. He is an author, inventor, and a director of engineering at Google (GOOG). Kurzweil is involved in fields like optical character recognition, text-to-speech synthesis, and speech recognition technology like Apple’s Siri.

The Singularity is Near isn’t an investment book or even an economics book — but I consider it essential reading for every investor. Kurzweil describes the world to come and America’s next great leap.

The Singularity is Near isn’t an investment book or even an economics book — but I consider it essential reading for every investor. Kurzweil describes the world to come and America’s next great leap.

As you read this book written eight years ago, you will see how some of Ray Kurzweil’s uncannily accurate predictions are already coming true. You will better understand his predictions for the next 40+ years.

Kurzweil describes “The Singularity,” a future utterly different from anything we can imagine. Supercomputers will accelerate change, making centuries of progress happen in only a few years. The remarkably rapid innovation Kurzweil predicts will change the world and enrich our country.

Kurzweil’s “The Singularity is Near” gives investors a broad outline of what is coming. Apple is a counterweight to the skeptics who dominate the stuff of our news media and political discourse.

Artificial intelligence, fantastic innovation, new wealth and much healthier, longer lives are right around the corner. Those who invest in this bright future now will be the ones who prosper.

Read Kurzweil’s book — then reflect and invest accordingly. Your life will never be the same.

James DiGeorgia

P.S. In just 12 hours, you will have missed out on 3 huge opportunities:

1. First, Tony Sagami is taking his new video, “How to Build a Bullet-Proof Portfolio,” offline, where you can learn how a simple scientific-investing formula can generate remarkable returns.

2. Second, this indicator just uncovered 2 new exciting opportunities … and he just released these newest recommendations a few hours ago.

3. Third, this is your last chance to claim your $1,105 gift just for watching my new video.

Here’s the thing — you only have until TONIGHT at 11:59 p.m. Eastern to take advantage of these profit-boosting opportunities.

There’s no guarantee that they will be available again anytime soon. So don’t wait — click this link to get in on Tony’s newest recommendations Today!

Confessions of a Wall Street Whiz Kid

Confessions of a Wall Street Whiz Kid

Chapter 12

What Three Decades In and Around Wall Street

Has Taught Me about Investing

You’ve heard the old saying, if I only knew then what I know now? How true that really is. When I think of how I was promoted to head of investment strategy in 1987 with less than three years experience, I wonder how I managed. I spent most of my energies buying and selling stocks and foolishly believing I could continuously predict what the stock market would do, and I spent little time on learning and appreciating how money really works. It was not until I met Frank Congilose in 1998 that I was shown the real truth about money and that traditional financial planning, a process 98 percent of all investors employ (and one which is steered by “professional advisors”), is a horribly flawed process.

Back in the 80s, most professionals used a simple legal pad to show clients how to set up their “financial plans.” Nowadays, firms use fancy computer applications with all sorts of interactive charts and graphs. But in the end, whether on a legal pad or high-tech computer model, all of these “plans” do the same thing: They guess.

First, they seek a dollar number the client believes (or is shown) he or she will need to live happily ever after. This is the first absolute guess. Once that is agreed upon, the professional advisor picks a product or products—most involve stocks, mutual funds, etc. —and, based on past performance, projects similar returns for the future in order to reach that magical happily-ever-after figure. This is the second raw guess—a total shot in the dark as to how high or low future returns will be.

What’s wrong with this very unscientific method? Four economic factors have a major impact on any financial plan, and unless you have a crystal ball you’re simply guessing where they’ll be at any given time. They are:

- Interest rates

- Tax rates

- Inflation rates

- Rates of return

I’m going to let you in on a little secret: I can’t accurately predict the course of all four of theseand neither can anyone else except Almighty God. Therefore, despite the average plan having hypothetical assumptions of these four factors, one or more of them will not be accurately assumed. One could get lucky as some did in the 1990s when everything was doing well, but do you want to depend on good fortune to keep your fortune? This is simply a well-established guessing game with all the bells and whistles. Make no mistake about it: traditional financial planning is a guessing game—a high-stakes round of hangman, charades, or 20 questions.

I don’t know about you, but I don’t want to leave my family’s security to chance. That’s why I was so awestruck by the process Frank Congilose introduced to me; one that employs the two most important money facts:

- Lost Opportunity Cost

- Velocity of Money

Let me explain: If you had $20 and lost it, how much did you lose? Twenty dollars, right? Wrong. You lost the $20 plus whatever that 20 bucks could have earned if you had it. That is a Lost Opportunity Cost (LOC). Just about everyone and every business has LOCs. The key to financial success is identifying the LOCs and putting them back on the right side of the ledger—your side!

If you were to identify about $20 a week (a few cups of latte, perhaps?) you could save, that would add up to $1000 a year in savings. But it’s so much more when you take into consideration the LOCs. By saving that $1000 per year, over 25 years you would save $25,000 plus the lost earnings on that money of over $18,000 (that’s at the modest interest rate of only 4 percent) for a total LOC of over $43,000. At 5 percent interest, the number increases to over $50,000. That $50K becomes part of your cash flow.

Cash flow, in case you didn’t know, is nothing more than the money that comes in and the money that goes out. If you spend more than you make you have a negative cash flow. If make more than you spend (leaving some extra) you have a positive cash flow. Obviously, increasing the positive cash flow allows you to save more and accumulate more wealth.

No one knows more about money and cash flow than banks. They don’t produce anything yet they are able to turn one dollar into two or three or more. Here’s how it works: you deposit a dollar in the bank. The bank pays you interest on that dollar. The bank then lends your dollar out to someone else at a higher rate. How much higher depends on what type of loan the borrower takes. Not only is the rate they charge higher than they paid you, but they get to lend your dollar out two or three times on average. During the time your dollar is deposited in the bank, it may be loaned out for a car loan, personal loan, home equity loan, mortgage, or credit card. Each time the bank loans out your dollar they make money by way of charging the borrower more interest than they are paying you.

This is called the Velocity of Money, the average rate at which money is exchanged from one transaction to another. Velocity is the frequency with which a unit of money is spent over a specific time period. The bank has taken full advantage of the velocity of money and effectively made a dollar do the work of two or three or more. What I learned to do through the services of Frank and his associates is help people understand and take advantage of the velocity of money in their own finances just like banks do.

Another way to appreciate velocity of money is to take a penny and double it once a day. On day one you double a penny and end up with two cents. On day two you double your two cents and have four. On day three you double your four cents and have eight…and so on. How long before you have over a million dollars? It may shock you, but it’s only 27 days. That’s right: a penny doubled each day for 27 days is worth $1,342,177.20.

Without any out-of-pocket expenses or substantial risk, you can add hundreds of thousands of dollars to your worth over a lifetime by simply capturing LOCs and employing velocity of money strategies which in turn increase cash flow. The sooner you learn that the key to successful finances is cash flow (saving your money instead of trying to gamble on an asset’s appreciation in price to increase net worth), the better off you will be.

I have found that there are four basic ways most people approach money matters. In which group do you fall?

- The “No Planning” Approach

This is the person with absolutely no plan. Nothing. Nada. Wing and a prayer. Their entire plan is to worry about it tomorrow. Obviously, this is the worst-case scenario.

- The “Occasional Planning” Approach

This is the person who intermittently thinks about money matters and might put forth a half-hearted attempt at a plan, especially right after New Year’s, but soon the day-to-day grind of life takes over and they end up doing what the no planning group does; worry about it starting tomorrow. But tomorrow never comes.

- The “Needs Planning” Approach

This is the person who plans for specific events like college or a child’s wedding but does not have an overall, integrated financial plan. They at times actually progress on a specific goal only to find out they have let other important goals fall by the wayside and then try to catch up with some “Hail Mary” schemes.

- The True “Financial Planning” Approach

The infrequent person who seriously plans for the things life throws at us. Not just retirement, mind you, but life. Buying a home, taking vacations, saving for college and retirement, and a nest egg for those things that just crop up.

Even among those who do plan, there are speed bumps along the way. In my three decades on Wall Street, I have seen many of the same mistakes time and time again. Here, I have assembled my list of Top Ten Biggest Investment Mistakes.

Peter Grandich’s Top Ten Biggest Investment Mistakes:

10. “Hot Potato” buying – Buying the popular stocks of the day or the latest get-rich-quick scheme. Unless you have a crooked rabbit, the turtle always wins this race in investing.

9. Believing publications – You see it all the time. Some magazine headline that reads “Ten sure fire ways to riches,” or “Ten stocks to beat the market,” etc., all for the low, low price of a few bucks for that issue. While there are some really useful publications, magazines likeMoney who depend mostly on financial institutions for advertisement are, in my opinion, always tilted to the cup being half full and are not truly objective.

8. Failing to consider spouse’s views – Guilty as charged. Through my first making of millions then losing a good portion of it, my wife’s only regret was I didn’t take into account her desires and wishes. Family financial planning must be a team effort.

7. Believing money is evil – Yes, the love of money is evil, but money itself is not. It’s a necessity but not to the point where we literally lose our eternal life with the true owner of it. Some people are afraid of it and what owning a hefty sum of it may do to them. As stated earlier, if you truly come to understand you’re only a steward with it, you are likely to do much good with it.

6. Not fully understanding what you’re doing – The less you know, the more people who live off the less knowledgeable can thrive. God knew how important matters of money would be and dedicated a good portion of His life’s manual (the Bible) to it. Shouldn’t you make a similar effort?

5. Inability to judge worthiness of risk – Here’s a news flash; if it’s too good to be true, it’s too good to be true. If the banks are paying you 1 percent and someone says you can make 10 percent, you better know that there’s a certain degree of risk that comes with the potential. Many times the anguish of a loss far outweighs the dollar amount, and it lasts longer and impacts other areas of your life.

4. Trusting financial institutions – Despites decades of deceit and fraud throughout the financial industry, most people still place a large degree of blind trust in the financial institutions and the personnel with whom they deal. Any financial adviser worth his or her weight should have a well-documented and long track record of success or at least have numerous references. Wouldn’t you be glad to give a reference if your adviser did well for you? Run, don’t walk, from those who can’t provide them.

3. “Hope” is not an investment Strategy – When it comes to faith, hope is very good, but in investing it can be a killer. If I only had a dollar for every time I heard an investor say they’re “hoping” their stock goes back up so they can get their money back. Look, if you’re hoping the price will rise yet not willing to buy more at the reduced price, who do you expect to do so and pay up to the price you originally paid? Just hoping for these changes without sound fundamental reasons to back up that hope is a license for disaster.

2. No written financial strategy at all – Similar to the “No Planning” approach. Like anything else at which you want to succeed, you must write it down. In the landmark book The Magic of Thinking Big, author David J. Schwartz tells us to write down our goals—all of them. Financial goals are no different. Writing your plan down not only keeps you on track but acts as a benchmark as you achieve your financial goals. One of the first things to do is to take a 30-day account of every dime you spend—and I mean everything. Almost always, people are surprised how much they spend and on what. They soon realize they can either do without some things or spend less on them.

And the number one biggest investment mistake is…….

1. Procrastination – Without a doubt, putting off dealing with matters of finance is the single biggest investment mistake. Whether it’s by accident or on purpose, delaying dealing with finances can only hurt most.

~~~

Perhaps we can all take some advice from one of the richest men ever to walk this earth. No, not Donald Trump or Warren Buffet, but King Solomon. He was one of the Bible’s best investors. King Solomon has a fantastic track record based on three basic biblical principles:

Principle #1 – Diversification

Divide your portion to seven, or even to eight, for you do not know what misfortune may occur on the earth. – Ecclesiastes 11:2

King Solomon knew that you don’t put all your eggs in one basket. This is especially true for those people who put all of their 401(k) savings into their company’s stock.

Principle #2 – Good Counsel

Without consultation, plans are frustrated, but with many counselors they succeed. – Proverbs 15:22

There’s no one person who can give universal counsel. Not only do you need to develop a support team, but you need to find a diverse group of a few individuals because one team member is not always aware of what another is doing and having someone quarterback all the different team players is important.

Principle #3 – Ethical Investing

The conclusion, when all has been heard, is” fear God and keep His commandments. – Ecclesiastes 12:13

Not only should we be honest in our investments but make sure where we place our monies to be Godly. That’s different for every individual, but might include avoiding investing in businesses involved in alcohol, weapons, tobacco, or companies with questionable human rights practices.

SIDEBAR:

“Learn as if you were going to live forever.

Live as if you were going to die tomorrow.”

– Mahatma Gandhi

Remember this: on Wall Street there are bulls, bears, and pigs. The bulls and bears each have their day, but the pigs always end up at the slaughterhouse.

More from Peter:

Hitler on Obamacare

George Carlin is Right

How to Protect Your Money When the U.S. Debt Bill Comes Due

Ever heard of a wedding crasher? You know — that distant “cousin” who shows up uninvited, hangs around the open bar all night, chugs down double-everythings and falls on his butt on the dance floor — all before mysteriously vanishing and leaving his night of indulgence on the father of the bride’s tab.

You don’t want to be around when that bill comes due!

Well, as a quasi-government organization with the authority to suck down your hard-earned money through the act of inflation, the U.S. Federal Reserve is “that guy,” and you could be the responsible one left with its bill.

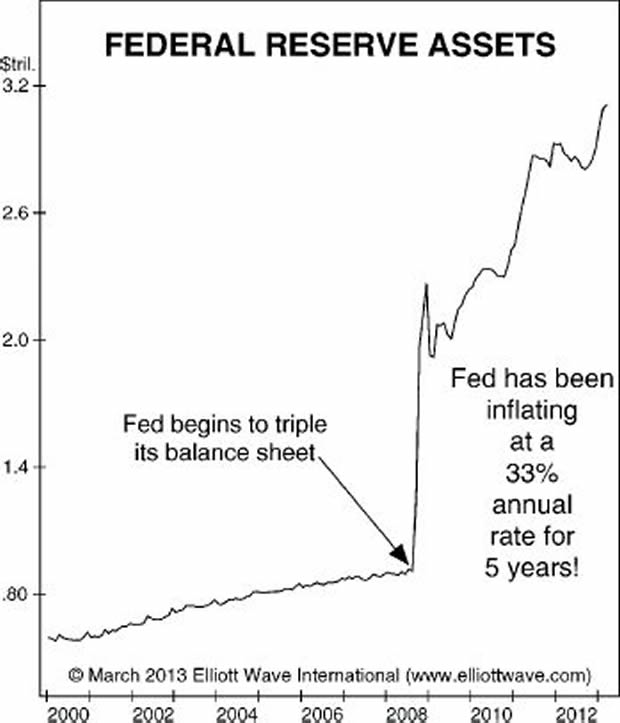

Did you know that the Fed has been inflating the supply of dollars at a stunning 33% annual rate over the past five years? Or that it plans to continue inflating the supply of dollars at least into 2014 and has kept open the possibility that it will do so indefinitely?

When the Fed’s party is over, who do you think will be left with the bill?

Not the Wall Street bankers! We’ve learned that lesson already.

It’s Main Street investors like you who get the bill.

But you can protect yourself — though your window of safety is closing rapidly.

Robert Prechter, market forecaster and leading opponent of the Federal Reserve, has just released a report that that will help you understand the risks of deflation that most mainstream sources cannot see because they are blinded by decades of inflationary Fed policy.

At just 8 pages, “How to Protect Your Money When the U.S. Debt Bill Comes Due” is a quick read — well worth any independent investor’s time.

Report Excerpt:

The Federal Reserve’s efforts to rescue the economy have been historically aggressive, starting with the initial round of quantitative easing in 2008 and continuing through 2013.

The central bank’s assets have skyrocketed due to the Fed’s bond purchases, which you can see clearly in this eye-opening report that Robert Prechter presented to the Market Technicians Association and his Elliott Wave Theorist subscribers.

The main reason investors are expecting runaway inflation is illustrated in , which shows the value of assets held at the Federal Reserve. The Fed has been inflating the supply of dollars at a stunning 33% annual rate over the past five years. … o wonder investors expect inflation and have aggressively positioned for it.

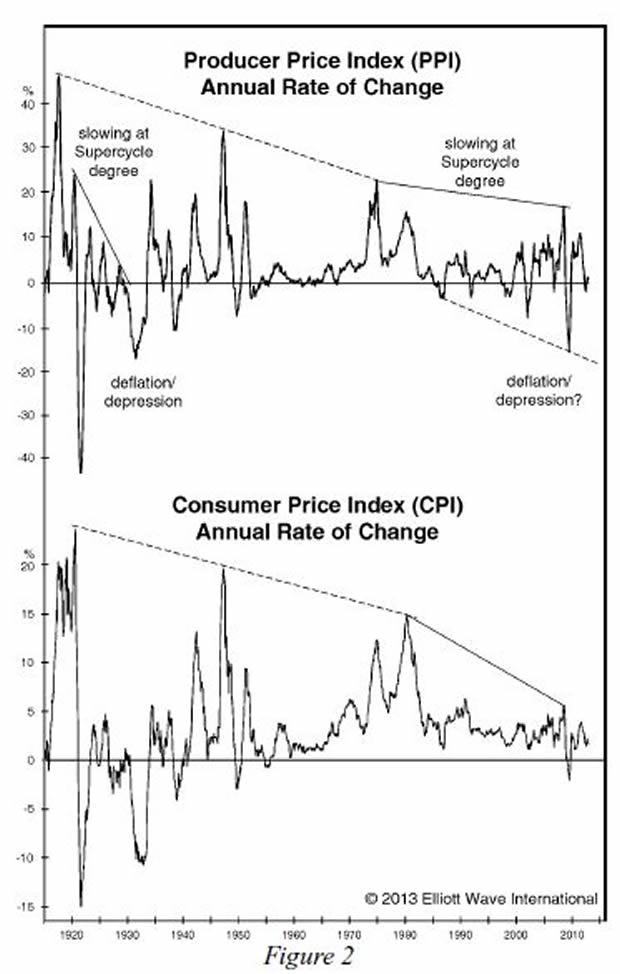

Look just about anywhere else, however, and you will see subtle evidence of deflationary pressures. Given knowledge only of the Fed’s inflating, many people would expect the Producer and Consumer Price Indexes to be rising at a rate of 33% annually. But, as you can see in Figure 2, the PPI’s annual rate of change is stuck at zero and the CPI has been rising at only a 2% rate.

In an interview at the recent San Francisco Money Show with financial author Jim Mosquera, EWI’s Chief Market Analyst Steven Hochberg explains why the Fed has gotten so little in return from its stimulus programs. Here’s a brief excerpt from the interview published on Aug. 18 on the Examiner.com website.

Question: The Fed wizards have been pushing buttons and pulling levers rather furiously since 2008. The discount rate is rock bottom, and the Fed balance sheet has swelled to the tune of trillions. What button is left for them to push?

Steve Hochberg: That is a really interesting question the way you phrased it because the fact that they have been pushing buttons and have gotten very little in return tells us … that the Fed is not in control. The Fed does not control the markets, and it doesn’t control the economy. Both are bigger than the Fed.

You say they have been doing this furiously. They have been doing this historically! Yet if you look at inflationary measures, such as the Personal Consumption Expenditures, which is the Fed’s favorite way of measuring inflation, it’s bumping along at 1%.

We have had historic fiscal and monetary stimulus and yet no inflation. Why? The forces of deflation are overwhelming the forces of inflation. The Fed dropped interest rates in 2000 to 2002 and that did not stop the Nasdaq from dropping 78%. The Fed dropped rates from 2007 to 2009 and it did not stop the Dow from going down 59%. There is historical evidence that the Fed does not control the markets but that the markets control the Fed.

As the next leg of the bear market starts unfolding, they are going to do more unconventional things. Things will accelerate to the downside when the public realizes the central banks aren’t in control.

For a limited time, you can read Robert Prechter’s 6-page report to prepare for what EWI sees ahead. In this report you’ll learn why the risk of deflation is mounting and how you can see it coming in the prices of gold, gas, real estate, crude oil and other markets. See below for full details.

Follow this link to download your free deflation-protection report now >>

About the Publisher, Elliott Wave International

Founded in 1979 by Robert R. Prechter Jr., Elliott Wave International (EWI) is the world’s largest market forecasting firm. Its staff of full-time analysts provides 24-hour-a-day market analysis to institutional and private investors around the world.

The United States of America are in a terrible, terrible situation. We are saddled with a government comprised of anti-American Marxists who hate our freedom and everything America used to stand for. This cadre of traitors seeks nothing less than to “fundamentally transform” America from a free nation of citizens into a slave nation of serfs. To do this, their every move since the Obama administration took office has been calculated to destroy the middle class backbone of our nation. A strong, vital middle class is a bulwark for any free nation, and therefore is an obstacle and impediment to the communistic goals of Obama and his gang of governmental thugs.

The United States of America are in a terrible, terrible situation. We are saddled with a government comprised of anti-American Marxists who hate our freedom and everything America used to stand for. This cadre of traitors seeks nothing less than to “fundamentally transform” America from a free nation of citizens into a slave nation of serfs. To do this, their every move since the Obama administration took office has been calculated to destroy the middle class backbone of our nation. A strong, vital middle class is a bulwark for any free nation, and therefore is an obstacle and impediment to the communistic goals of Obama and his gang of governmental thugs.

A good example of this is the ObamaCare debacle. The whole point to this program is to impoverish the middle clases by requiring them to spend onerous amounts of their money buying more expensive health insurance, while simultaneously subsidizing the “Free Stuff Army” half of the country that voted for Obama. Meanwhile, the calculated effort of the Left is toward the failure of ObamaCare, so that it can be replaced by something even worse—single payer socialized medicine in which the government completely controls health care access for most people and the only folks who can obtain “gold star” private health care are the very rich (i.e., like the “elite” in Washington and their buddies in the news media and Hollywood). Just look at the current issues with the Healthcare.gov website rollout, which has been an absolute disaster. I strongly suspect that this has been purposeful, intended to frighten people into demanding that ObamaCare be scrapped…to be replaced with the single-payer system the left-wingers have wanted all along. If the middle classes can be forced into a single-payer system, then they will be fleeced to pay for it, seeing their wealth frittered away, while the health care sword of Damocles is held over their heads lest they get out of line (“You’re a member of the Tea Party? I’m sorry, the doctor won’t be able to see you…”)

Yet, for American left-wingers, the relatively slow process of bilking the middle classes out of their aggregated wealth is not quick enough to solve the various “revenue deficit” problems that keep them from spending even more on expanded government projects to take away even more freedom. What would work much more quickly would simply be to directly confiscate the wealth of the middle classes by taking over their savings and investment. And that, while unthinkable for most of American history, appears like it may be on the horizon.

An astute reader sent me a link to an article that appeared last week in Natural News, in which the author warns us about impending changes to banking capital controls (i.e. how you can move your money around and where) are being put into place that appear calculated to allow the U.S. government to more easily nationalize private funds contained within our banking system,

“This is the beginning of the capital controls we’ve been warning about for years. Throughout history, when governments are on the brink of financial default, they begin limiting capital controls in exactly the way we are seeing here.

“Following that, governments typically seize government pension funds, meaning the outright theft of pensions for cops, government workers, etc., is probably just around the corner.

“Finally, the last act of desperation by governments facing financial default is to seize private funds from banks, Cyprus-style. The precedent for this has already been set in Cyprus, and when that happened, I was among many who openly predicted it would spread to the United States.

“This is happening, folks! The capital controls begin on November 17th. The bank runs may follow soon thereafter. Chase Bank is now admitting that you cannot use your own money that you’ve deposited there.”

The author of this piece, Mike Adams, is absolutely right in his warnings. As he pointed out, what is being proposed here is not some pie-in-the-sky, far out wacko conspiracy theory. Instead, it has already happened elsewhere, with Cyprus being the most recent and well-known example. Cypriots , who thought their money was safe in the banks, woke up to find one day that they could no longer access their own money, it was locked in the banks, and the reason for this was so that their government could grab it without worrying about people withdrawing it ahead of time.

…..continue article at Canada Free Press HERE

Stop listening to the whiners. The time to invest is when there’s blood in the streets. When your stocks have been doing well for a while and every moron decides that it’s time to buy equities, you’ll be in positions to “sell high.” You can’t really do that, however, if you neglect to buy low because you got caught up in the pessimism and lost faith in human ingenuity.

This is the same thing John Templeton did it back in 1939. Templeton started his investing career in 1939 by borrowing about $10,000, which was real money in those days. With war escalating in Europe and most investors in panicked despair, he didn’t buy gold, nor did he put all his money in Treasuries or other “safe havens.” He bought 100 shares in each of the 104 companies priced under a dollar on the New York and American stock exchanges. Almost all were innovative startups, and 34 were in bankruptcy. He then ignored his portfolio for four years. At that point, only four of the 104 were worthless, and he had quadrupled his money. It wasn’t luck. Templeton was one of the few who understood portfolio mathematics. It is axiomatic that a diversified portfolio of truly innovative companies held for the long run will pay off big. This is based on the simple assumption that human progress will continue and things will get better.

Most people forget that during the Great Depression, there was considerable growth in technological innovation. Necessity created a number of innovations that made our lives better and easier — the laundromat, copy machines, the car radio, the electric shaver and even the cotton tampon all came out of the 1930s. The first nylon material was introduced by DuPont. Improvements in existing technologies like the automobile and airplanes were constantly happening, even as the stock market flat-lined.

So at a time when the mainstream was too busy running scared from markets and hiding their money (to the detriment of the rest of the economy), innovative investors like John Templeton were quietly investing in emerging technologies and, over time, making a fortune. Templeton didn’t wait for the government or central banks to somehow stimulate us into success like most people then and now.

If you are waiting for policymakers to solve the market’s problems, you’re going to be waiting a long time. There are two kinds of people the world should really be looking to for solutions — scientists and the investors who fund their innovations. Scientists might toil away for years, and investors might sit and wait patiently, but inevitably, as progress is made, there is a payoff — and that payoff can, in some cases, lead to revolutions in entire industries. Schumpeter is the most important economist to investors: He coined a term “creative destruction.” If you really want to make money, look not for that which strikes at the margins and outputs of existing firms, but at their very foundations.

We are looking for investments that leave ruins behind. Capitalism is the very perennial gale of creative destruction. So if we want to seek out and profit from the real innovations in society, we have to look for technologies that aren’t just changing some things, but changing everything.

This moment of financial uncertainty, like all those before it, is a golden opportunity for investors with vision to buy emerging disruptive technologies at truly bargain prices.

I’m constantly amazed by the sort of sentiment I read in mainstream financial publications. When stocks are down, people decide they’re going to sell off and look elsewhere for profits. The market “stinks,” they say. Seriously, am I the only person who finds this sort of short-term thinking addled and absurd?

After all, we’ve seen financial cycles since… forever. We know they happen. We know that the best time to buy is when markets are depressed. So why are so many people acting as if the markets are broken?

Oh, wait. I know that one. It’s because most people are driven more by herd psychology than higher-order thought processes.

I’ve been reminded why I like the Austrian economist Joseph Schumpeter so much. One reason is that he considered big business cycles the inevitable consequence of innovation, as well as the resistance to innovative change that always exists within the old order.

This view, that cycles cannot be eliminated due to the biological imperative of human nature, sets Schumpeter apart from other economists, even of his own Austrian School. In fact, many of my friends of the Austrian persuasion who adhere more strictly to the banking theories of Mises and Hayek tend to irritate me. They’re. So. Whiny. They complain and complain about the stupid things that governments do and the fact that stupid people enable those stupid things… stupidly.

So what? If you can’t change it, accept it. And profit from it.

By this point in history, given that we’ve suffered through far more serious injuries to our economic system, and more than recovered every time, it should be obvious that human nature is not “repairable.” There’s not ever going to be some sort of global — or even societal — awakening, in which the vast majority of people suddenly realize that government is basically incapable of improving on free markets to any significant degree.

Societies do, however, respond to the pain caused by government-induced failures, just as B.F. Skinner’s pigeons learned complex behaviors without ever understanding them. We are, in fact, well on the road to recovery, though I admit that more people are going to have to suffer negative reinforcement (pain) before we are ready to make up for lost time. But we will.

I’m sure you know the Chinese curse, “May you live in interesting times.” We do, in fact, live in very interesting times. More importantly, we are in a period of historic opportunity, which we may never see again.

Regards,

Patrick Cox

For Tomorrow in Review

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair