Personal Finance

From Morgan Housel, here are several cognitive biases that cause you to do dumb things with your money. Be sure to check out the entire article.

From Morgan Housel, here are several cognitive biases that cause you to do dumb things with your money. Be sure to check out the entire article.

15 Biases That Make You Do Dumb Things With Your Money

1. Normalcy bias

2. Dunning-Kruger effect

3. Attentional bias

4. Bandwagon effect

5. Impact bias

6. Frequency illusion

7. Clustering illusion

8. Status quo bias

9. Belief bias

10. Curse of knowledge

11. Gambler’s fallacy

12. Extreme discounting

13. Ludic fallacy

14. Restraint bias

15. Bias bias

I like Nobel Prize winning cognitive psychologist Daniel Kahneman’s take on this: He once said, “I never felt I was studying the stupidity of mankind in the third person. I always felt I was studying my own mistakes.”

Source:

15 Biases That Make You Do Dumb Things With Your Money

Morgan Housel

When Bubbles Fail: Albert Edwards Explains What Happens When The Fed Can No Longer Contain The Fury Of The “99%”.

When Bubbles Fail: Albert Edwards Explains What Happens When The Fed Can No Longer Contain The Fury Of The “99%”.

The premise in Albert Edwards’ latest letter “Is the Fed blowing bubbles to cover up growing inequality… again” is simple: the unprecedented social inequality in the US (and the rest of the world – as pointed out here), and what it will ultimately lead to. Regarding what it will lead to, Edwards believes, is that “growing inequality drains the swimming pool dry. The crunch, when it comes, will be ugly.” Simple enough.

Digging a little deeper.

Ed Note: This article recommended by Peter Grandich can be read in full HERE

Live – Tomorrow at 10:15am Pacific

Live – Tomorrow at 10:15am Pacific

How to use ETFs in your portfolio

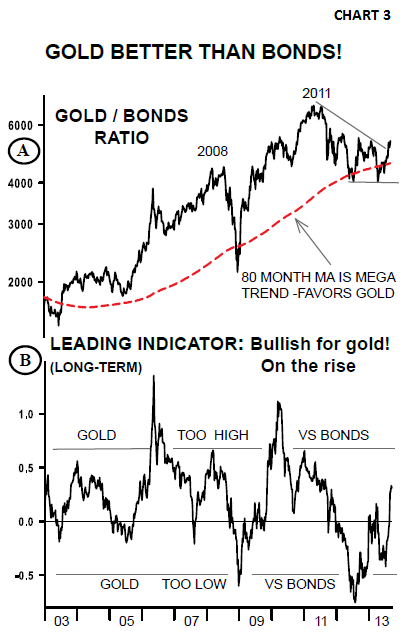

This chart is so important we really want you to take a hard look at what it’s telling us.

Very simply, this ratio chart compares gold to bonds. When it rises, gold is stronger than bonds. And when it declines, gold is weaker than bonds.

We call this our inflation-deflation barometer. Why?

Gold tends to rise during inflationary or generally good economic times. That’s why the ratio’s been rising over the past decade.

Ed Note: This is just a portion of this article, more charts and points made in the article Seeds of Change Growing

I received my credit card statement today. Here is what it said, in fine print: If you make only the Minimum Payment each month, we estimate it will take 81 year(s) and 5 month(s) to fully repay the outstanding balance. Our estimate is based on the New Balance shown on this statement and your current credit card account terms.

Wow. 81+ years if you make only the minimum payment !

Hence: pay off your credit card every month. I taught my kids a while ago that credit cards are not “credit” cards, they are debt cards or convenience cards.

Modern day-to-day life, for example to book a flight, to reserve a rental car or to buy goods online, require a “credit” card. As such have one, maybe two. I actually have 3 to make accounting easy: one for personal use, one for Prestigious Properties business and one for my holding company on non-Prestprop business. That’s it.

I carry & personally guarantee a lot of debt. Lots. Why can I sleep well at night ?

Because we own assets, with income producing characteristics. We are in the real estate investing business. Assets usually appreciate in value, in time due to inflation and property upgrades. That is why it makes sense to carry debt, at 2.8% for a CMHC insured mortgage to 3.5% for a conventional mortgage, to buy assets that yield 5 to 6%. That is also referred to as “good debt”, as opposed to “bad debt” for depreciating assets or life’s conveniences.

I pay the credit cards off every month, and so should you. If you are unable to pay off your credit card every month, it becomes a very expensive debt card very very quickly, as interest rates are routinely in the 18-22% range. This is very expensive “credit” especially in the current low interest rate environment. A good strategy is to use cheaper debt, say a secured LOC (line of credit) to pay off credit card debt. Or if you have poor money management habits get one linked to your bank account, i.e. it acts like a debit card. Or get pre-paid cards. The high interest is why banks or large retailers are so eager to give you such a card, as they can make a fortune off you. Don’t be fooled into it.

I also do not have a car loan, another expensive form of debt. When I was younger and our family had a lot less money we bought cars in cash, usually old used ones. Only once I did my first real estate flip in Canmore I bought a new car, in 2003 – only 10 years ago – in cash. Cars are very expensive habits, easily costing between $5000 to $10,000 a year if one counts gasoline, insurance, repairs, oil, tires and depreciation. 50 cents per kilometer is the rough true cost of a car. Thus, if you drive 10,000 km a year it is $5000/year; if you drive 20,000 km it is $10,000. A car loan at 7% coupled with the car’s depreciation can put you financially behind even if you have a decent wage. Don’t get a car loan. Lease a small car if you must, or better: get a used one, paid for in cash.

Instead of paying $40,000 for a new car, why not buy one for $10,000 and invest $30,000 into income producing real estate. In 5 years the $40,000 car is worth $20,000 at best, so you lost $20,000. With a $10,000 car, now worth $6000, and $30,000 invested in real estate your networth in 5 years might be $46,000 to $56,000 depending on the real estate, i.e. you are $26,000 to $36,000 ahead just by downsizing to a used car and investing into an appreciating asset, via TFSA or RRSP, or in cash.

Real estate investing beats car investment and “credit” cards by a wide wide margin !

Don’t be a debt-beat !

Thomas Beyer, President

Prestigious Properties Group

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair