Personal Finance

Let’s put another nail in the coffin of the “recovery” talk.

Bernanke and the Fed allege that the purpose of QE is to help housing recovery. But rising home prices do not actually equate to increased “wealth” for the average American.

Homes, unlike most purchases (well at least in the past), are financed via debt. In this regard the “homeowner” doesn’t actually “own” the home; the bank does. And anyone who looks at how much money banks make from mortgage lending can easily assess who comes out on top from that deal: hint it’s not the homeowner.

Homes, unlike most purchases (well at least in the past), are financed via debt. In this regard the “homeowner” doesn’t actually “own” the home; the bank does. And anyone who looks at how much money banks make from mortgage lending can easily assess who comes out on top from that deal: hint it’s not the homeowner.

Say I buy a home for $200K with a down payment of $40K. I only own $40K worth of home. And if the home rises in value to $220K, I still owe the bank $180K. Sure, you couldtechnically argue that I’ve made $20K off my initial $40K, but that would only count if I sold the house right then and there.

If I don’t sell the house, then technically I’m not wealthier, I’m just slightly less in debt (on paper). This fact becomes abundantly clear the minute I stop paying my mortgage and the bank comes knocking.

With that in mind, we need to ask, just who is wealthier as a result of the new housing bubble the Fed has created?

It’s not most Americans. According to the US census only 29% of us own our homes outright. Rather, it’s the banks and the large institutional investors who bought up thousands of homes in cash during the “recovery.”

This is not rocket science; it’s common sense. But the Fed keeps talking about a housing “recovery” like it’s helping Main Street. It’s doing no such thing. All of the Fed’s policies have been aimed at helping the large banks. They’re the ones who own the US’s homes.

About Gains Pains & Capital Gains

If you’re concerned about your portfolio taking a hit when the bubble bursts, I strongly urge you to consider an annual subscription to my Private Wealth Advisory newsletter.

Private Wealth Advisory specializes in helping individual investors profit from any market environment.

In 2008 the Private Wealth Advisory portfolio returned 7%.

In 2011 it returned 9% (the market was flat).

And from July 2011-July 2012, Private Wealth Advisory set a record for the investment newsletter industry, closing out 74straight winning investments.

During this entire 12 month period, we didn’t close a single loser.

In fact, we’re currently on another winning streak having locked in FOURTEEN winning trades in the last two months, including gains of 10%, 11%, 21% and 25%.

And our portfolio is on the move with winners number 15, 16, and 17 just waiting in the wings.

To take action to prepare for what’s coming… and start taking steps to insure that when this bubble bursts you don’t lose your shirt.

Yours in Profits,

Graham Summers

The call for this week: As expected, Bernanke did not taper last week. As not expected, most of the major market indices I monitor made new all-time highs, rendering another Dow Theory “buy signal.” However, last Wednesday’s upside explosion looked conspicuously like a short-covering, upside, exhaustion rally. That view was reinforced by the relatively quick “giveback” of Thursday/Friday. As stated, typically after a huge momentum move, like Wednesday’s “no taper” rally, the equity markets will trade sideways for a few days. That just didn’t happen as the S&P 500 pulled right back to its previous intraday high of 1709.67 (August 2, 2013). Historically, there is evidence that when you get a momentum move like last Wednesday’s, which is followed by a closing price below a previous high, it has resulted in more of a pullback. Therefore, it will be interesting to see how the SPX reacts off of the August 2nd pivot point of 1709.67 this week.

Brent Woyat, Portfolio Manager, CIM, CMT

brent.woyat@raymondjames.ca

www.ofip.ca

…for the last 4 years , the FED fund rate was essentially at zero and we have massive money printing , monetary inflation so it creates a huge pool of liquidity , the problem is that this liquidity will not flow evenly everywhere in every sector of the economy and in every country , it can flow first into the NASDAQ stocks until March 200 then in the US Housing market then in commodities and gold and then in emerging markets , then you have one bubble after the other ….that is the problem of the money printing by central banks.

MARC FABER EXPLAINS HOW BUBBLES ARE CREATED BY THE CENTRAL BANKS

In terms of Investment, there is nothing Safe anymore

In terms of investment, there is nothing safe anymore. The US money-printing has distorted all asset prices while cash in the bank has not given you any return when inflation is adjusted. Inflation in Thailand is running at 10 per cent per annum. I don’t look at the government’s statistics. All governments around the world lie.

Marc Faber on Buying Government Bonds

Marc Faber Biggest Mistake (WSJ)

- The Chicago Fed’s monthly National Activity Index is released at 8:30 AM ET. Economists expect the index to rise to -0.05 from last month’s -0.15 reading.

- Markets in Asia were mixed in overnight trading. The Japanese Nikkei fell 0.2%, the Hong Kong Hang Seng fell 0.6%, and the Shanghai Composite rose 1.3%. European markets are in the red across the board, led lower by London, Germany, and Spain, both down 0.5%. In the United States, futures point to a negative open.

….Read the other 8 HERE

Ed Note: With Europe in economic trouble and the USA struggling and Debt soaked (even though its Leader declared wednesday that “raising the debt ceiling, which has been done over a hundred times, does not increase our debt“), one has to wonder what drove the S&P 500 to hit an All-Time High this week.

Currently, buyers have to be found for Trillions in US Government Bonds over and above the 85 BILLION per month that the Federal Reserve continues to buy – after it essentially admitted Tuesday that the economy is too weak for it to reduce its pace of creating money out of thin air.

In spite of the troubled conditions US Stock Indexes continue to behave as if a Financial Boom had been, and would continue to be driving them higher. A scenario like this has happened before. Or at least so say newspapers back in the late 1920’s.

Martin Armstrong of Armstrong Economics explains what is driving them higher, and its not what Political leaders or the newspapers are telling you.

Martin’s answer below begins with a question that you can read HERE

It’s a Matter of Confidence

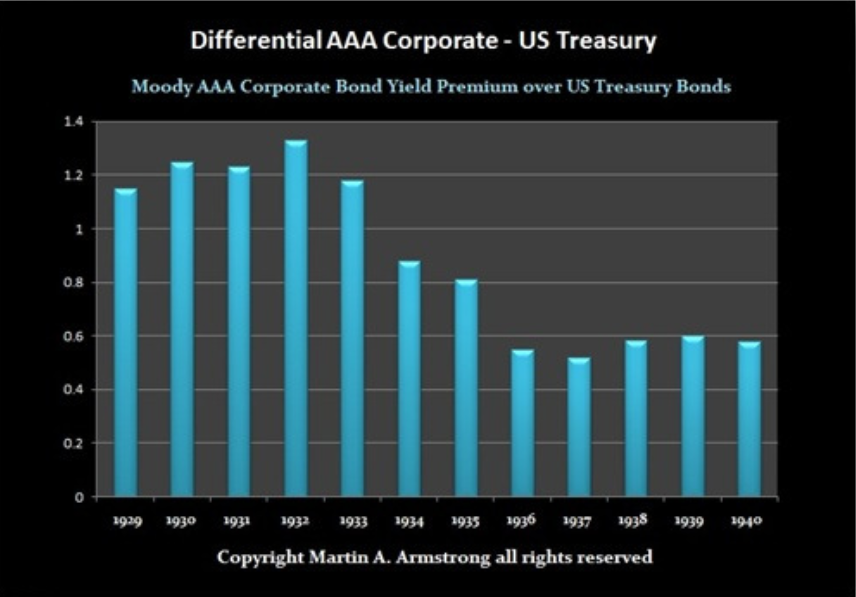

Prior to Great Depression in a PRIVATE WAVE, rising interest rates were seen as BULLISH because it meant people were still borrowing and bidding up rates. Rates crash in recessions because there is no bid.

The central banks have manipulated rates very low and capital has no choice but to shift. As confidence in government declines, rates will rise and people see alternative investments in the private sector exactly as we saw going into 1929. There is no relationship that is ever fixed BECAUSE there are other factors people may not be looking at.

Your statement there is a “high degree of confidence in the authorities to “manage” the situation without an accident” reflects this directional change. This is why gold declined. The Goldbugs only see their point of view. The MAJORITY disagree with them and ask the average person on the street do they think government will collapse or the dollar and they will look at you like you are a nut-job. We are not at the point of a collapse in general confidence yet. That comes after 2015.

Your statement “European bond market yields reflect complete confidence in the EU and ECB” does not reflect confidence but manipulation as is the case with rates in the USA. Governments are artificially setting them low to save money, but when the confidence shifts, rates will explode as the Fed was testing the marketplace.

The Pension Crisis is all about this confusion. They have been bond buyers. They earn nothing and the central banks are creating the next default – pensions. They do not have “confidence” but have no choice as do banks with requirements to buy government bonds for reserves.

Your statement: “The US stock market is exactly positively correlated to the belief that the Fed has things under control (see Wednesday’s reaction). Logically, loss in that confidence would obliterate stocks. Yet you suggest we are on the verge of a massive collapse in confidence in government and its agencies and that stocks will double. How do I reconcile?” Your assumption is incorrect. Stocks are not rising because of “confidence” in the Fed, the central banks have themselves been buying stocks lacking confidence in public debt. Money has NO CHOICE but to go to stocks. Pensions will go bust and stocks are becoming the ALTERNATIVE to government debt.

Armstrong Economics mission is provide a public service for the average person to comprehend the global economy and for professionals to access the most sophisticated international analysis possible (the computer to the right is what is used for analysis) We provide an integrated understandable global model approach that is free of personal bias, bravado, or other nonsense to enable you to see the inherent inner-workings of the world economy to grasp how everything is truly integrated to a single enterprise driven by international capital flows. Forecasting the World economy and markets becomes possible only when approached on a stoic unemotional basis from a international perspective. Trying to forecast a single market is dangerous for everything is interconnected on a global scale. Personal opinion has no place in forecasting. It was personal opinion that argued for centuries the world was flat and that the earth was the center of the universe with everything revolving around it. Galileo spent life in prison for daring to disagree with such opinions.

Armstrong Economics mission is provide a public service for the average person to comprehend the global economy and for professionals to access the most sophisticated international analysis possible (the computer to the right is what is used for analysis) We provide an integrated understandable global model approach that is free of personal bias, bravado, or other nonsense to enable you to see the inherent inner-workings of the world economy to grasp how everything is truly integrated to a single enterprise driven by international capital flows. Forecasting the World economy and markets becomes possible only when approached on a stoic unemotional basis from a international perspective. Trying to forecast a single market is dangerous for everything is interconnected on a global scale. Personal opinion has no place in forecasting. It was personal opinion that argued for centuries the world was flat and that the earth was the center of the universe with everything revolving around it. Galileo spent life in prison for daring to disagree with such opinions.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair