Personal Finance

TORONTO, ONTARIO — (Marketwired) — 07/27/13

With 83 per cent of Canadians planning on taking a summer vacation this year, BMO Insurance reminds travelers to keep safety and finances in mind when away from home.

According to BMO Insurance’s Annual Travel study, a quarter (24 per cent) of Canadians have, at some point, required medical attention for themselves or a travel companion while on vacation.

Meanwhile, despite the fact that required medical treatment could cost upwards of tens of thousands of dollars, forty-two per cent remain confident they could cover all of their medical costs if they required medical attention while abroad, even if uninsured.

“Receiving medical treatment outside of Canada without the proper travel insurance in-place can be very expensive, particularly if those costs are not budgeted for,” said Julie Barker-Merz, Vice-President and Chief Operating Officer, BMO Insurance. “We encourage Canadians to educate themselves on the potential financial risks they face when travelling without medical insurance, and to investigate what affordable options are available to them.”

Ms. Barker-Merz noted that, for example, treatment for a broken leg in Florida could cost up to US$20,000, while decompression sickness in Thailand could cost up to US$40,000 to treat.

Top Reasons Why Canadians Don’t Buy Travel Insurance

Further, according to the study, nearly a third (31 per cent) of Canadians either never or only sometimes purchase travel medical insurance when vacationing outside of Canada. Among those who do not always purchase insurance every time they leave the country, the top reasons identified were:

-- Already covered by a workplace or provincial healthcare plan -- Already covered by a credit card -- It costs too much money -- Unlikely to need medical attention

“Emergencies can happen anywhere and any time, so it’s critical that Canadians ensure they have the proper medical coverage before travelling,” said Ms. Barker-Merz. “While Canadians can sometimes be covered under the terms of their credit card or workplace healthcare plan, they need to do their research well in advance of their trip to be certain that they have insurance in place that is right for their trip.”

The online survey was conducted by Pollara with a random sample of 1,000 Canadians 18 years of age and over, between May 9 and May 13, 2013.

This is an automatically generated default main template – please do not edit.

Please note: the main template does not contain any fields.

It’s been a strange couple of weeks. US stocks are not far from all-time records, both nominally and adjusted for inflation. Home prices are soaring – up 33% y-o-y in the Bay Area, to take just one of many possible examples. A casual observer might assume that things are going great.

But one level down on the headline ladder it’s a very different story. The list of ominous events and trends has suddenly grown a lot longer. Among the bombs that went off last week:

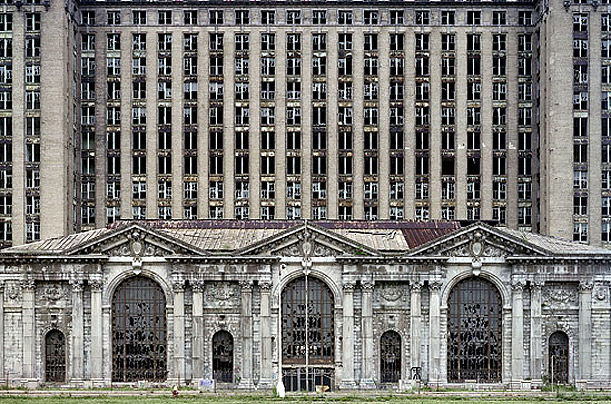

Detroit declares bankruptcy

Detroit declares bankruptcy

For years, analysts have been looking at the balance sheets and pension funds of dysfunctional entities like California, Illinois, Chicago, Detroit, and Oakland and wondering how much longer they could con the markets into believing that they were in any way capable of paying off their debts or making good on their pension obligations. Last week the first domino fell, as Detroit declared chapter 9 bankruptcy. The legal wrangling has just begun but initial bargaining positions have the city trying to eviscerate pension benefits and force massive haircuts on muni bond holders. If they succeed even partially, then the hundred or so other functionally-bankrupt cities may see this as the path of least resistance. The result: Turmoil in the muni market, which is generally considered a near-risk-free cash equivalent. See Avalanche of city debt downgrades and eventual bankruptcies coming up.

Corporate revenue growth stalls

Google and Microsoft both reported disappoinging revenue growth and their stocks tanked. Revenue is harder to fake than earnings, so it’s a more reliable indicator of big trends. Tech bellwethers reporting weak revenues implies that the economy is itself weaker than we’ve been led to believe. And corporate profits, which have provided much of the fuel for rising equity prices, can’t keep rising if revenues plateau. See The party may be over for tech stocks and Earnings season starting to look like a disaster.

Portugal and Spain descend into chaos

Both countries are finding it impossible to cope with life in a relatively-strong-currency regime. Unemployment is at capital “D” depression levels, home prices are plunging, voters are restless. Portugal’s government can’t pull together a working coalition, and the most popular party opposes the continuance of austerity. But the alternative to austerity is an exit from the eurozone. See Portugal political crisis: no end in sight.

Spain’s leaders, meanwhile, seem to have reacted to the economic crisis by trying to steal as much as possible while they could get away with it. Apparently they went to the well a few too many times and now the resulting scandal has reached all the way to the top. With much of the existing government implicated – but still in power – it’s not clear who will be left to do whatever it is that should be done about the economy. See Spain: scandals, lies, graft, and kickbacks

There’s more, including massive, insanely ill-timed layoffs in Greece and the IMF calling China’s policies “unsustainable”. But all of it points to slowing – and maybe negative — growth in the US in the coming year, which would make stock and real estate bubbles seem, in retrospect, a bit out of place.

One study of bull market peaks over the past 80 years finds eerie similarities with current conditions.

One study of bull market peaks over the past 80 years finds eerie similarities with current conditions.

We may be closer to a major market top than most investors think.

That at least is the conclusion that emerged when I compared the current market environment to what prevailed at major market tops of the past century.

To be sure, there are some dissimilarities as well. But that doesn’t necessarily mean we’re not peaking. No two tops are exactly alike. As Mark Twain famously said, even if history does not repeat itself, it does rhyme.

With that thought in mind, I examined all 35 bull market tops since the 1920s. I searched for patterns in the performance of not only the market itself, but of various internal market factors, such as earnings and price/earnings ratios. I was also interested in how small company stocks tend to perform in the months leading up to a top, both in their own right and relative to large-cap stocks. Likewise, I searched for patterns in the relative returns of growth and value stocks.

I relied on several extensive databases: Yale University Prof. Robert Shiller’s database of Standard & Poor’s 500 earnings and P/E ratios, as well as a database showing the relative performances of small- and large-cap stocks, as well as of the growth and value styles, maintained by Eugene Fama of the University of Chicago and Ken French of Dartmouth. To determine when bull and bear markets have begun and ended, I relied on the precise definitions employed by Ned Davis Research, the quantitative research firm.

Here’s what I found.

Market rises steeply before bull dies

The typical bull market comes to an end following a period of extraordinary performance. In other words, some of a bull market’s best returns are produced right before it dies.

This is important to know if you thought that this bull market would, before it breathes its last, begin to slow down and go through a period of modest performance. That’s not typically the case: On a price chart, the average market top looks more like a pointed mountain peak than a plateau.

While it is of course possible that the next market top is more like a plateau, it would be the exception rather than rule: Since the 1920s, the average bull market has gained more than 21% over the 12 months prior to a top — more than double the long-term average.

Interestingly, the stock market recently has produced a return that is quite similar to this average 12-month gain prior to market tops: The S&P 500 over this period is up nearly 23%.

Riskiest stocks shine before market tops

One of the most striking patterns about these months leading up to a market top is that the riskiest stocks far outperform the most conservative ones.

Profs. Fama and French have devised two proxies for risk. One is the relative performance of value stocks over growth issues; stocks with low price-to-book ratios are deemed value stocks, while those with high ratios are in the growth category. Their second risk proxy is the performance of small company stocks relative to the large-caps.

…..read page 2 HERE

I own equities, and I should thank Mr. Bernanke. The Fed has been flooding the system with money. The problem is the money doesn’t flow into the system evenly. It doesn’t increase economic activity and asset prices in concert. Instead, it creates dangerous excesses in countries and asset classes. Money-printing fueled the colossal stock-market bubble of 1999-2000, when the Nasdaq more than doubled, becoming disconnected from economic reality. It fueled the housing bubble, which burst in 2008, and the commodities bubble. Now money is flowing into the high-end asset market—things like stocks, bonds, art, wine, jewelry, and luxury real estate. The art-auction houses are seeing record sales. Property prices in the Hamptons rose 35% last year. Sandy Weill [the former head of Citigroup] bought a Manhattan condominium in 2007 for $43.7 million. He sold it last year for $88 million.

I own equities, and I should thank Mr. Bernanke. The Fed has been flooding the system with money. The problem is the money doesn’t flow into the system evenly. It doesn’t increase economic activity and asset prices in concert. Instead, it creates dangerous excesses in countries and asset classes. Money-printing fueled the colossal stock-market bubble of 1999-2000, when the Nasdaq more than doubled, becoming disconnected from economic reality. It fueled the housing bubble, which burst in 2008, and the commodities bubble. Now money is flowing into the high-end asset market—things like stocks, bonds, art, wine, jewelry, and luxury real estate. The art-auction houses are seeing record sales. Property prices in the Hamptons rose 35% last year. Sandy Weill [the former head of Citigroup] bought a Manhattan condominium in 2007 for $43.7 million. He sold it last year for $88 million.

Money-printing boosts the economy of the people closest to the money flow. But it doesn’t help the worker in Detroit, or the vast majority of the middle class. It leads to a widening wealth gap. The majority loses, and the minority wins. Although I have been a beneficiary of this policy, I can’t approve as an economist and social observer. – in Barron’s

Marc Faber – Sprott Money News Interview – Jul 22, 2013

Nathan McDonald of Sprott Money News interviews Marc Faber in the video report above. He begins asking Mark his view of the speech from Ben Bernanke and the Fed’s FOMC meeting minutes for June which have just been released,

Faber: in China without Huge Credit Expansion there would probably be no Growth at all

“The Chinese economy is growing at something like 4 per cent per annum, and without huge credit expansion there would probably be no growth at all.” – in South China Morning Post

You might also like:

Faber : The FED is Causing the Crisis with its very Expansionary Monetary Policy

Have the quantitative easing measures / stimulus by various central banks done an irreversible damage to the long-term prospects of global economy, markets (equity and commodity)? Why / why not?

Faber : There are people believe that Ben Bernanke and other central bankers have saved the world’s financial system. I am not saying that they are wrong but I am suggesting that the crisis occurred in the first place because of the expansionary monetary policy – principally by the US Federal Reserve since the 1990’s.

In other words, each time there was a crisis – be it S&L (savings and loans) crisis, LTCM Hedge Fund crisis, Mexican peso crisis which is also known as the Tequila crisis – ahead of Y2K, monetary policies were eased and liquidity injection occurred. And then we had the Nasdaq collapse in the year 2000.

The US Federal Reserve then again embarked on extremely expansionary monetary policy, which created a gigantic credit bubble and home prices surged.

When this came to an end, that’s when the crisis actually happened. Had the US Fed not pursued very expansionary monetary policies and paid attention to excessive credit growth, there would have been no crisis.

The Policy Decisions in Japan are quite Dangerous

In the case of Japan, we have had essentially very little growth and some deflationary pressures until last October after which the Bank of Japan (BoJ) embarked on monetary easing policies. Since then the Yen has weakened considerably and the stock market has risen sharply.

I think that the policy decisions in Japan are quite dangerous because it essentially gives a green signal to other countries regarding monetary easing. If there is have low economic growth and if the share market is not performing well, then most likely the currency will go down. This will help economy temporarily and lift asset prices.

FABER : The Euro-zone is not going to Grow

…..read more HERE

Marc Faber is an international investor known for his uncanny predictions of the stock market and futures markets around the world.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair