Personal Finance

THINGS THAT MAKE YOU GO HMMM…

THINGS THAT MAKE YOU GO HMMM…

Nigel Farage and Marina Hyde Go for A Pint

The Painful Truth: Greece Needs a Debt Haircut Now

Gold Futures Hiccup Indicates Demand Outpacing Supply

“Detroit Will Rise Again”: Glimmers Of Defiance After City’s Bankruptcy

Man With Plan

How an Airline Buyer’s Buddies Crashed, Burned

Now That Detroit’s Gone Bust, Is Your City Next?

How To Spot a Liar

Maybe It’s May?

Cooking the Numbers in Buenos Aires

CHARTS THAT MAKE YOU GO HMMM…

WORDS THAT MAKE YOU GO HMMM…

AND FINALLY

Another lazy summer day. The Dow sold off a few pennies on Friday. Gold rose $8.

Another lazy summer day. The Dow sold off a few pennies on Friday. Gold rose $8.

The airport in Paris must be the most efficient in the world. Our cab drove up at exactly 6 a.m. By 6:04, we were having a cup of coffee, waiting to board the plane. In just four minutes, we’d gotten our ticket, been inspected by security and made it to the gate.

Now we’re on the plane, flying over the Pyrenees… thinking…

Good As Gold

Over the last 10,000 years, humans have tried two different kinds of “money.” They began with exchanges based on credit – “You give me a chicken… I’ll pay you back later, maybe by helping you build a new wigwam.”

Then, when society became too large and extensive, they switched to gold and silver. The advantage of this was obvious: You didn’t have to remember who owed what to whom. You could settle up right away. “You give me a chicken. I give you a little piece of silver. Done deal.”

Periodically, governments were tempted to go back to credit systems. Essentially, they issued pieces of paper – IOUs – and declared them “money.” Usually, these hybrid systems began with some collateral backing up the paper. Issuers typically had gold in their vaults and agreed to exchange the paper for metal at a fixed rate. Holders of the paper money were told that it was “good as gold.”

In some cases, people believed the IOUs were better than gold. When John Law began modern central banking in France, he backed his paper money with shares in a profit-seeking business – the Mississippi Company. You could take his scrip and imagine that it would grow in value along with the profits of the company.

Trouble was, the Mississippi Company never made any profit. It was a failure… and a fraud. Great prospectus. Few real investments. When people realized, they wanted to get rid of their paper money as soon as possible. In 1720, the system collapsed, and John Law fled France.

Later in the 18th century, the French tried again. This time, the revolutionary government backed its new paper money with revenues from the church properties they had seized. This didn’t last very long, either. The system blew up in 1796. Napoleon Bonaparte, on the scene at the time, declared, “While I live, I will never resort to irredeemable paper money.”

Richard Milhous Nixon didn’t seem to get the memo. In 1971, he changed the world monetary system. Thenceforth, it would be based on irredeemable paper money. We are now in year 42 of this new experiment with modern, credit-based money.

All right so far? Well, yes… as long as you don’t look too carefully.

Nothing More Than Promises

When you have a system based on credit, rather than bullion, deals are never completely done. Instead, everything depends on the good faith and good judgment of counterparties – including everybody’s No. 1 counterparty: the US government. Its bills, notes and bonds are the foundation of the money system. But they are nothing more than promises – debt instruments issued by the world’s biggest debtor.

A credit system cannot last in the modern world. Because, as the volume of credit rises, the creditworthiness of the issuers declines. The more they owe, the less able they are to pay.

As time goes by, the web of credit spins out in all directions, entangling not just the present, but the future too. It stretches out over the entire society… one person owes another… who owes a third… whose debt has been pledged to a fourth… who now depends on it to pay a fifth… and all calibrated in the IOUs of sketchy value from a sixth. Have you got that?

Total debt in the US now measures more than twice what it was – in proportion to GDP – in 1971. And GDP itself has been goosed up by credit. Every time someone borrows money to spend… the spending shows up in GDP.

It looks great… on paper. There’s only so much gold. But there is no reasonable limit on how much of this new credit-based money you can create. As it increases, it gives people more spending power. GDP goes up. Employment goes up. Prices – especially asset prices – go up.

Naturally, everybody loves a credit system… until the credits go bad. Then they wish they had a little more of the other kind of money. Wise governments, if there are any, take no chances. They may feed the paper money to the people. But they hold onto gold for themselves. Throughout history, the most powerful governments were those with the most gold.

“Remember the golden rule,” they used to say. “He who has the gold makes the rules.”

When push comes to shove, governments need gold, not more IOUs with their presidents’ pictures on them.

Which brings us to the point of today’s Diary.

Unraveling an Unruly Skein

Britain famously and foolishly sold much of its gold at the very worst time, at the end of the 1990s, when gold was trading at a 20-year low.

But how about the US? Does it have any gold left? That is the question recently posed by Eric Sprott:

Central banks from the rest of the world (i.e., non-Western central banks) have been increasing their holdings of gold at a very rapid pace, going from 6,300 tonnes in Q1 2009 to more than 8,200 tonnes at the end of Q1 2013. At the same time, physical inventories have declined rapidly since the beginning of 2013 (or have been raided, as we argued in the May 2013 Markets at a Glance), and physical demand from large- and small-scale buyers remains solid.

As we have shown in previous articles, the past decade has seen a large discrepancy between the available gold supply and sales. The conclusion we have reached is that this gold has been supplied by central banks, which have replaced their holdings of physical gold with claims on gold (paper gold).

Analyzing the gold sales figures over the last 12 years, Sprott noticed that there was far more gold sold than mined. Where did it come from?

Some of it is easily accounted for in jewelry and private holdings. But, generally, the private sector is a buyer and an accumulator of gold, not a seller. And the quantities released to the market have been so great, Sprott believes they could have come only from central banks.

But if they have sold such massive quantities over the last 10 years, how much do they have left? Maybe not much.

Which wouldn’t be surprising. Western central banks are committed to their credit-money system. They intend to stick with it. And they know that unraveling this unruly skein of credit would be extremely painful.

Selling gold into the bull market of the last 12 years probably seemed like a very smart move. We’ll see how smart it was later, when the credit-based money system blows up.

Dear Readers are advised to hold onto their gold. It’s the kind of money that works.

Regards,

![]()

Bill

Smart Money and Public Investors Disagree – Again!

It’s not a surprise, or even unusual, to see public investors with a quite different take on the market than so-called ‘smart money’.

It’s not a surprise, or even unusual, to see public investors with a quite different take on the market than so-called ‘smart money’.

That divide has been quite obvious again in the current bull/bear market cycle. The bull market got underway in March, 2009 when Wall Street institutions, the trading departments of major banks, insurance companies, pension plans, and hedge funds began stepping back into the market, convinced the 2008-2009 financial meltdown had bottomed.

Meanwhile, the Investment Company Institute (ICI) says households are by far the largest group of investors in mutual funds. So if we use money flows into and out of mutual funds as a proxy for the activity of public investors, it was about that time, 2009, that public investors, distraught and devastated after holding on through the 2008 financial meltdown, finally began pulling money out of the market.

And that divergence between ‘smart money’ pouring money back into the market, while public investors pulled money out persisted as the bull market continued right up until last fall. At that time the Investment Company Institute reported money flows out of mutual funds had finally reversed to inflow.

The pace at which public investors had finally begun to pour money into mutual funds increased dramatically as we entered this year.

…..read more HERE

So how do these guys do it?

So how do these guys do it?

The Bottom Line:

Peter Lynch and Warren Buffett have both been extremely successful following a simple approach that any investor can emulate. George Soros has become successful using an approach that is impossible to emulate – predicting market moves and trading aggressively.

Curiously, many amateur investors appear to be taking the ‘impossible’ route, by trying to predict the market and making frequent trades.

Perhaps we should pay more attention to the simple lessons of Buffett and Lynch

…..read how each of these Great Investors does it HERE

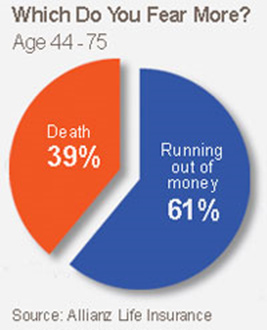

What is our biggest fear? Embarrassment? Death? Public speaking? According to an Allianz Life Insurance poll, the greatest fear of older Americans is outlasting their savings. We fear living longer than our bank accounts by a margin of 22

Death or Running out of money Stephen Pollan has an interesting solution to this problem. In his book Die Broke, he wrote something to the effect of: “The last check you should write should be to the undertaker, and it should bounce!” I wonder if people like that die because they know they are out of money.

Now, I can imagine a couple of ways to follow Pollan’s recommendation. One is to go skydiving, neglect to pull the parachute cord, and pay the skydiving company with a bad check. Or one could go on a massive spending spree, overdraw every account, and stay broke until death. In the latter case, one wouldn’t have to worry about running out of money in the least – you don’t have to worry about losing something you don’t have.

Not too long ago, I was quite pleased when my computer would ding and announce “You’ve got mail!” Now, after spending the day away from the computer, I am not surprised to return to 100 or so messages between the junk mail that makes it through the filters and the emails that actually require my attention.

Like most folks, I’ve developed a system for quickly scanning and prioritizing my inbox. Every day I get a few from my wife Jo (email from a spouse is a high priority for anyone interested in staying married), as she is forever on the lookout for things I might want to share with my readers. One headline Jo sent caught my eye: Running Out of Money Worse Than Death.

The short article published by AARP covered the results of the Allianz poll; while the poll of 3,257 people was taken about three years ago, my guess is the results would be similar today. Let’s take a look at a few of the highlights:

- Of people ages 44-75, more than three in five (61%) said they fear depleting their assets more than they fear dying.

- More than half (53%) of poll respondents said their net worth dropped significantly during the [2008] economic downturn. Of those, virtually all have cut back on entertaining and dining out, 47% have reduced their daily living expenses, and 11% have told their children to expect less financial support.

Honestly, this isn’t new news. Seniors and savers can no longer rely on Treasuries or FDIC-insured CDs to pay interest rates that will beat inflation, let alone make them any money. We are all having to put a greater portion of our nest eggs at risk to earn enough to supplement Social Security. But the headline still bothered me… a fear even greater than death?

Nevertheless, I started to pay attention to my closing thoughts at night, and I tried to recall what I dreamed about. I don’t remember ever dreaming about death or worrying about it late at night. On the other hand, I did find myself doing a lot of problem solving during the night, much of it financially related. Perhaps the survey was right; maybe I do worry more about running out of money than I do about dying.

I touched on this subject back in February, and since then two of my good friends have been diagnosed with medical problems for which there is currently no cure. I am amazed at how both friends quickly dealt with the news and set about reassuring their families that they were OK with the situation. One even went so far as to joke that his kids are being particularly nice, because they know he still has enough marbles to change his will if he wanted to. I admire both of these friends a great deal and hope that when my time comes I will handle my swan song with as much grace as they each have.

Then it hit me! And yes, it was actually in the middle of the night. My real problem with the Allianz survey is that I want to live until I die. I want to enjoy life while I’m here. I worked my tail off for many years to accumulate a nice nest egg. I’ve earned more than a few low-stress, worry-free golden years. Worry is for young folks with young families.

My kids roll their eyes when I remind them that in my 20s I worked three jobs and went to school at night… for a decade. The only thing I remember from my 20s was working to feed a young family; I had little time to worry about much else. When we reach our 60s, those stresses should be well in the past.

Nevertheless, just because certain worries should be in the past does not mean they are. Retirees need to figure out a way to not run out of money so they can stop worrying about it, sleep well at night, and enjoy the sort of retirement they imagined.

Retirement Success Is Possible

The fact is, the market has changed: investing is a lot more challenging than it was just a decade ago. If one has a nest egg but is worrying about making it last, he is well ahead of most folks. After all, he had the foresight and discipline to save while he was still in the workforce. Frankly, most of our readers fall into that boat.

As I wrote in my book Retirement Reboot, I was terrified in the fall of 2008. The banks had called in all of our CDs; I had a nest egg but was still in a panic regarding handling it. What should I do with it? Where could I find a good return? How do I know which investments are safe? What is a good allocation for a stock portfolio? I could have filled two pages with my list of fears at the time.

As I look back, the solution was really simple. I needed to learn – a lot. I needed to educate myself on investing and learn about issues I had not focused on during my business career. My goal was to invest my capital, earn good returns, not worry, and keep my fears under control. Most of all, I wanted to live life and enjoy the retirement Jo and I had dreamed about for a couple of decades.

A friend told me years ago that fear is a lack of knowledge. The more you learn and understand about a subject, the less fear you have surrounding it. I agree wholeheartedly. Financial fears will take a terrible toll on many of us if we are not careful. Fear not only affects us financially – often paralyzing us into indecision – it also eats away at our emotions and can even damage our physical health. I for one plan to have fun while I’m here and not worry myself to death.

Regards,

Dennis Miller

P.S. I’m sure we have all heard the old adage, “If you think education is expensive, try ignorance.” Most of our readers are like-minded folks who prefer to educate themselves rather than worry. If that sounds like you, I suggest taking a look at all of the educational resources Money Forever has to offer. Best of all, our 90-day trial subscription is 100% risk-free. Take it for a test drive, and if you find it’s not for you, just call or email within the first 90 days and we will refund 100% of the cost… no questions asked.

There’s no better way to start making sure you have enough money until you die. Click here to learn more about how Money Forever can help.

About Dennis Miller

Dennis Miller is the author of Miller’s Money Foreverand the free journal, Miller’s Money Weekly. Working with Casey Research analysts, Dennis advises subscribers on how to prepare a bulletproof retirement portfolio and ensure having their own money forever.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair