Personal Finance

Zurich is a delightful city. So much history! So much beauty! So much money!

Zurich is a delightful city. So much history! So much beauty! So much money!

You can barely throw a Kruggerand in any direction without hitting a rich banker or his model wife.

They stroll along the Limmatquai. They dine at the Kronenhalle. They shop on Bahnhofstrasse.

And what do they think of today’s markets?

“It’s crazy what is happening,” said our friend. “But crazy things happen. You just have to make sure you’re not doing something crazy too.”

What crazy thing happened yesterday? The Financial Times says stocks rose when investors got good news from the manufacturing sector.

Maybe.

We noticed a big bounce in gold. The metal was up $32 an ounce. And beaten-down gold miners showed even more gains.

Whassup? End of the correction in the gold market?

Only a fool would pretend to know where gold will come to a bottom. I guessed $1,100 yesterday. Colleague Chris Hunter (who will be providing us with our new Market Insightnotes every Monday, Wednesday and Friday) thinks it could be lower.

Nobody knows. But a lot of people think they know. And when people think they know something that they can’t really know, it is an opportunity for those who don’t know and who know they don’t know. Is that clear?

Gold – No Longer Necessary?

Our old friend Mark Hulbert at The Hulbert Financial Digest reports that independent financial advisors have never been more bearish on gold than they are today. Other indicators tell us that the public and the professionals are overwhelmingly against the yellow metal…

Even at the “top” – when gold was near $1,900 an ounce – few investors owned gold. It was considered kooky. Bizarre. Vaguely seditious.

Since so few people owned it, few were unhappy to see it go down. And when it did begin to correct, all those investors who had jumped into the gold market at the last minute, because they didn’t want to be left behind, thought they should get out immediately. Their rush for the open door is what brought about the sharp sell-off.

Meanwhile, serious investors are not speculating on the next move of the gold price. They’re accumulating gold… and measuring their wealth in it.

We’ve heard investment professionals recently tell us that gold is no longer necessary. It’s just a hedge against central banks going wild, they say. And, now that the Fed has demonstrated its willingness to “taper” its bond buying, there is no need for gold, especially when official consumer prices are rising at an annual rate of just 1.4%.

Anti-Wealth

But consumer prices aren’t the only kind of inflation…

Nor are they the first kind…

The first kind of inflation is the kind that raises values for the lucky 1%. People who own financial assets – stocks, mainly – see their wealth increase as a result of central bank manipulation.

That’s the kind of inflation that most people like. Even if they aren’t part of the 1%… and they don’t own stock… they are happy to see a bull market on Wall Street. They imagine – like Ben Bernanke – that somehow this ‘wealth’ will trickle down to the working stiffs.

They’re right. It does seep into the consumer economy, eventually. But not as wealth. As anti-wealth. Prices for toilet paper, parking spaces and cookies increase. The working stiffs end up with lower real purchasing power.

We’re not there yet. Consumer price inflation is still – apparently – very low. In fact, we are in what looks more like a period of disinflation than an inflationary cycle.

In fact, we’re so far away from consumer price inflation that investors can’t see it coming. They think the feds have everything under control. They think the economy is fundamentally sound… and that monetary policies are fundamentally sensible!

They’re betting that Mr. Bernanke can work things out with Mr. Market…

We don’t approve of speculation – not in gold and not in anything else. Most people – including us – don’t have the stomach for it.

Instead, put your money to work the way serious people do. The way the Swiss do. If you haven’t done so already, begin a lifetime program of gold accumulation, not gold speculation.

Set aside some amount. Buy gold every month. And hope the price goes down so you get more for your money.

Regards,

![]()

Bill

About Bill Bonner

Bill Bonner founded Agora Inc. in 1978. It has grown into one of the largest independent newsletter publishing companies in the world. In 1999, along with Addison Wiggin, Bill founded The Daily Reckoning. Today, this daily e-letter reaches over 500,000 readers around the globe.

Bill has also co-written two New York Times bestselling books, Financial Reckoning Day and Empire of Debt. He has written or co-written other widely read books as well, and has penned a daily column at The Daily Reckoning for over 12 years. Recently, Bill decided to “retire” from his role at The Daily Reckoning and begin writing his Diary of a Rogue Economist.

Bill Bonner’s Diary of a Rogue Economist is your gateway to Bill’s decades of accrued knowledge about history, politics, society, finance and economics. Sometimes funny, sometimes frightening – but always entertaining and packed with useful insight, Diary of a Rogue Economist can help you make sense of the complex world we live in today.

Michael Campbell interviews income and dividend investing expert Aaron Dunn of Keystone Financial for the best he has.

{mp3}mtjune29hour1{/mp3}

*Note: Aaron also recently produced a new MoneyTalks DIY portfolio course available online. This insightful, easy to follow, tried and tested approach to building, managing and succeeding with your own self-managed equity portfolio. Great for beginners and experienced investors alike. Find this streaming MoneyTalks DIY portfolio course HERE

*Note: Aaron also recently produced a new MoneyTalks DIY portfolio course available online. This insightful, easy to follow, tried and tested approach to building, managing and succeeding with your own self-managed equity portfolio. Great for beginners and experienced investors alike. Find this streaming MoneyTalks DIY portfolio course HERE

As we have noted, in the credit markets, the term “Disorderly” is a euphemism for “Crash”. And this is the condition afflicting most classes of bonds.

As we have noted, in the credit markets, the term “Disorderly” is a euphemism for “Crash”. And this is the condition afflicting most classes of bonds.

The key event has been the reversal from a speculative surge to a downtrend. This was expected in or around May.

Using the High-Yield Corporate Bond (HYG), the price soared to 95.80 on May 7th, which was followed by a dramatic Outside Reversal day. We reviewed this with Bond Markets – A Profound Change? on May 13th.

The main point was that the hot action was vulnerable to a seasonal reversal centered in May, and that market forces would overwhelm bond-buying programs by the ECB, BoJ and Fed. Mother Nature and Mister Market would preempt the “official” decision by senior central banks to end the program.

The test of the high reached 95.39 on May 22nd, and the breakdown was accomplished on May 23rd. Technically, the trend reversed to down in price and up in yield. The possibility of widening credit spreads has yet to work out. Treasury bond prices have fallen with lower-grade bond prices.

At some point spreads between treasuries and corporates will turn to serious widening.

The other part of the Great Bond Revulsion will be a serious increase in interest rates relative to the rate of CPI inflation. Rising real interest rates is one of the features of the post-bubble condition and will be reviewed in the next week or so.

The last disorderly market brewed up last summer and was mainly focused upon European Sovereign Debt. Using the Spanish Ten-Year as the proxy, the reversal from party-time was accomplished in early April 2012 when the yield rose above 5.50%.

The high in the panic was 7.50% set on July 24th.

The yield plunged to 4.0% on May 3rd, and the breakout at 4.43% was accomplished last week. Now it’s at 5.16% and rising quickly.

However, in looking at the leading disasters such as HYG and Emerging Debt (EMB) the plunge has been severe. Severe enough to drive the Weekly RSI on the HYG to 33, which is the lowest since the 2008 Crash.

On the EMB the RSI is down to 18. While not as low as with the 2008 Crash, it is extremely oversold.

The action in US corporates has been very bad but “Emerging” has been worse. The yield ratio between EMB/HYG soared to 1.36 last November and then HYG began to outperform.

The yield ratio declined to 1.24 in March and rallied to 1.29 in April. From 1.26 last week it has crashed to 1.14 earlier today. With this the Weekly RSI has plunged to 15 – the worst on a chart back to 2008.

Over the past week the calamity drove the DX from 80.5 to 82.8 earlier today.

Wrap

– Lower-grade bond markets are extremely oversold and can enjoy a brief rally. There could be even greater liquidity problems in the fall.

– With this, the US dollar can decline.

– A technical rebound for the precious metals is possible.

– For this to work out, gold stocks would begin to outperform gold and silver would begin to rise relative to gold.

FREE TRIAL SUBSCRIPTION

The term “Rational Fringe” has been used to distinguish our research from the mainstream convictions that financial history was random and could be managed by inspired manipulation of interest rates.

Our models are based upon a thorough review of the highly volatile conclusions of 5 previous new financial eras. This provides forecasts of significant trend changes with enough lead time to formulate strategy. See our notes on the Capitulation Model.

Our original observations were that key financial sectors such as the stock market or the yield curve each recorded similar behaviour patterns through each previous era of great financial booms.

The conclusion was that these patterns would provide a guide through our wild financial party and that the action would override orthodox financial research and policy making.

….read more about the service HERE

Does a Bell Ring at Market Tops? Well with a $25 Million Dollar Condo sale in Vancouver it sure looks like one has just gonged for Vancouver Real Estate.

Does a Bell Ring at Market Tops? Well with a $25 Million Dollar Condo sale in Vancouver it sure looks like one has just gonged for Vancouver Real Estate.

The Condo was a 6400sf 2 level penthouse overlooking Coal Harbour, Stanley Park and the North Shore Mountains. The owner had it up for sale for 2 years, and in the end apparently made a 47% capital gain in just 3 years of ownership.

That said, this sale comes on the heels of an astonishing 10 year 200% plus rise in Vancouver real estate prices. Moreover the chart below clearly shows that this $25,000,000 sale showed up just as a decline in pricing has begun.

Now if market wizard Marc Faber is correct that: “Maybe gold is signaling a deflationary collapse of all asset prices”……. if you have profits in your Vancouver Real Estate, it sure looks like it might be time to bank some just to be safe in uncertain times.

Charts by Canadian Housing Price Charts

We don’t believe real estate is a good hiding place either? Here’s why…….

Recently, a newsletter guru (who shall remain nameless) listed several reasons why he believed real estate would be a great place to put cash. We were surprised because we don’t believe real estate will be a haven after another major washout in global markets if global demand doesn’t materialize soon.

It just so happens a good friend of ours, his name is Clive, agrees. We have printed below Clive’s well- reasoned and articulate responses to said newsletter guru’s consensus rationales for buying real estate. We couldn’t have said it better…thanks Clive.

Guru: We have to be prepared for when it does happen. How? Probably the best way is to buy real estate with long term, ultra-low, fixed-rate mortgages. Non-recourse, if possible. In September 2011, we recommended you increase your family’s allocation to real estate to take advantage of this unique situation. It was a better investment then. Still, now is not a bad time to invest in bricks and mortar.

Clive: This idea of [said guru] is so appealing that I thought I would try it, a few months ago. I couldn’t make it work. I bought my house in New Hampshire, in 2010 because I like the house and it is part of a 100 acre farm which provides good food for six months of the year. It has been a great place to live, but a bad investment. The market price has declined by 40%. I hoped it would decline only 20% because the housing market had already taken a hit. Next year I may be able to get my property tax reduced… maybe. If so, I’ll lose less over time.

Guru: US real estate is an ideal investment for this non-recovery world. Here’s why: It is relatively safe. In the case of a financial Armageddon, real estate is still valuable. It doesn’t go away.

Clive: Land may be safe, but real estate (buildings) burn, with their contents, in revolutions. Both are almost impossible to liquidate when there is the slightest whiff of trouble. Moving them is even more difficult. Over the last century, there were lots of Russians, East Germans, Chinese, Africans, South Americans… who found out the hard way about “real estate”. All they have left is worthless title deeds. The US may be a little more stable… until it is not. It wasn’t so long ago that fine Southern families moved from their land with nothing more than their good manners and empty stomachs. Factories in the North needed cheap labor.

… and the parasites? OMG. Real estate taxes, insurance companies with their “requirements”, lawyers, accountants, contractors, all those regulations… and that is before dealing with the realities of physical maintenance. Houses and property are sitting ducks for extraction purposes.

Guru: Average US home prices have risen about 12% year-over-year. But they are still reasonably cheap – depending on where you buy. If central banks succeed in tapering, real estate and rents will probably both rise.

Clive: It seems to me that real estate is being bought with funny money. The “investors” take their bonuses, short term profits and steal the money in the form of “salaries” and handling fees, but when the Taper sharpens it teeth, surely the buying will stop and prices will drop? An increase in interest rates will also dampen enthusiasm, especially if there is no real growth. Perhaps inflation will eventually increase nominal prices, but I don’t anticipate much demand from a declining population.

Guru:…If they don’t, your mortgage gives you a free “option.” If yields rise after 32 years of trending in the other direction you will get a windfall. If they don’t, you will still have your rental income (or personal use). If you have financed on a non-recourse basis, you are in an even better position. You have made a one-way bet. You can only win.

Clive: Unless the property price declines! I could not find a bank that would give me more than a five year fixed mortgage. After that, it “floated”. No thanks. I paid cash for my house rather than have to deal with all the parasites that climb aboard as soon as a bank is involved.

I am stuck in my house unless I want to take a loss now, but property prices could decline more, just like the stock market, gold or anything else that has not yet had its day of reckoning. Only in the fantasy world of T.L. Friedman are house prices destined to increase with more government subsidies and mortgage interest tax breaks.

It’s over. Populations in advanced economy countries are declining with the decline of cheap energy (oil). The Fed doesn’t really care about house prices and they can do nothing about it short of sending everyone a check for $100,000 a year. They could! They have our addresses from our tax returns. Krugman would be thrilled, but even the smug bearded Ben is not likely to do that. The Fed cares only about the Government and keeping interest rates low to reduce the cost of their obligations. That manipulation will work only as long as other nations accept our debt but a bit of trade “re-balancing” could make some people really unhappy. Interest rates will probably rise… slowly, not like the 1970s because baby booming is out of fashion.

Guru:– Can you lose? Of course! If property prices fall and continue to fall… and rental rates fall too… you will lose money. Maybe serious money. (Unless you have a non-recourse mortgage.) This is a possibility. But it suggests a level of deflation I believe would be intolerable to the authorities.

Clive: Of course the authorities don’t want a decline. They have all their economic models based on GROWTH. It worked as long as there was cheap energy. Populations increased and everyone had two houses, cheap food, a car or two, a lawn and it was onward and upward. Things are different now. Energy is becoming more expensive and complicated. There are no more gushers. The intolerable deflation is beyond the control of the authorities. They are going to get it whether they like it or not, probably in a place they won’t like.

Guru:— That is when Bernanke or his successor would be likely to resort to Overt Monetary Financing, aka “helicopter money.” This has already been widely discussed in the press. Central bankers are already considering it. In an emergency, it wouldn’t be long before they would use it. Then, like my parents in the 1970s, your mortgage will seem like a gift from heaven.

Clive: I think it will be very difficult to “induce” inflation with helicopter money. Food stamps, welfare (social and corporate) and “defense” spending cannot last forever at China’s expense. Middle class people are sick of credit. During the last fifty years, credit allowed leveraged investments to grow very nicely. The bigger the credit, the safer the loan. Ask Donald Trump. Now people think they may have to pay back their loans and that makes them upset. Nobody wants more credit. They want less. The mentality has changed. Having “free time” (to talk on a cell phone for example) is much more valuable than having a pile of stuff bought on credit because it will be “more valuable” in the future.

This is a devil of a problem for us long term investors. I don’t see real estate being a good investment other than as a place to live. Owning gives some liberties that renters to not have, but it does not give the important liberty of “leaving” at a moment’s notice.

A big pile of cash appeals to me more than a pile of bricks and mortar… at least until the market has sorted itself out. That may still take a few more years. Then I will buy a pile of gold and who knows what… maybe real estate, or more [xxx] stock. If I have cash, I’ll be king! I hope my house does not make me a poor king.

…………………………

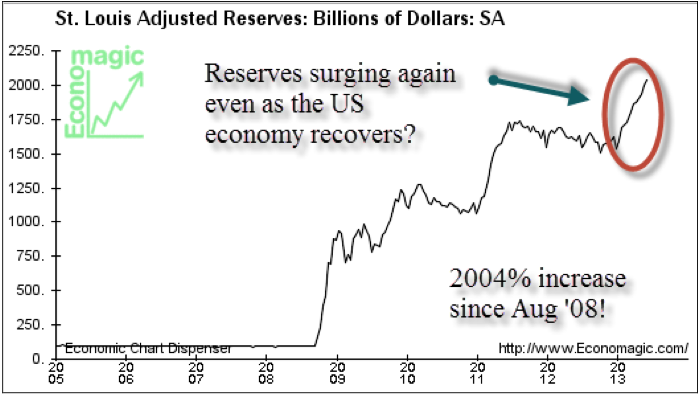

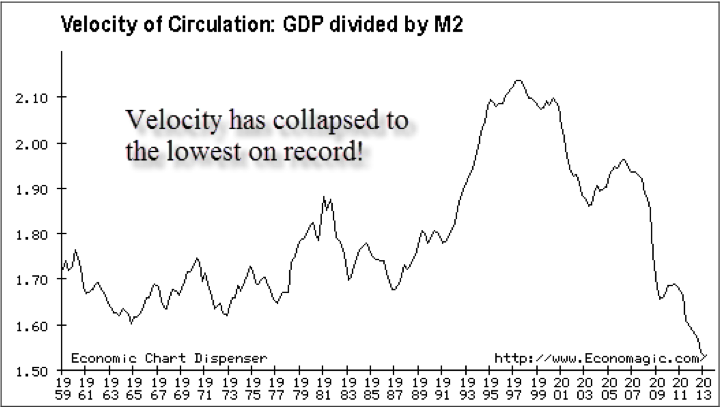

I provide two charts and some comments from our recent Global Investor macro view to support Clive’s arguments and make it quite clear the Fed is losing the battle no matter how much “helicopter” money it spends (rising bank reserves and a tumbling monetary velocity tell us Fed stimulus isn’t getting where it was supposed to go).

…If the primary rationale for holding stocks is based on faith in central bankers, then what follows is an implicitly belief stocks as an investment class are primarily liquidity-driven speculative vehicles. A more nuanced view accounts for the power of liquidity and the discounting value of futures earnings in a zero interest rate environment. But implicit in this view is a belief said future earnings, presently supporting these discounted cash values, are tethered to the underlying growth opportunities where these businesses operate.

Secondarily, those who have placed their full faith in central banks see little chance of a negative feed-back loop stemming from the wholesale manipulation of money and credit. A couple of possibilities for negative feedback include: 1) a huge jump in price levels (inflation) should the weight of banking reserves circulate back into the real economy. Banking reserves have increased stunning 2004% since they began ramping up in August of 2008 as a result of the credit crunch; if real economy lending opportunities were abundant and consistent with US growth optimism, we wouldn’t be seeing a surge in banking reserves:

We believe deflation is the problem facing the global economy; not inflation. How else could one explain the relative calm in global headline inflaiton indicators (with mandated and regulatory costs as exceptions) given the massive amount of money and credit created globally? So, although there is logic to the inflaiton argument, we believe the real economcy is signaling global inflaiton is a problem for another day, that day could be years away.

2) A deflationary spiral, or long period of extremely low growth (the Japanese quagmire for Europe and the US) is the more likely scenario given what the Austrians refer to as malinvestment. We could witness a complete loss of credibility in the Fed as key players abandon their belief in Keynesian-style stimulus.

Monetary and fiscal policy failure in attempt to avoid the so-called “Keynesian liquidity trap” (a false premise) is already evident by the performance of the real economy. The excerpt below, taken form “Liquidty Trap or Malinvested Resources” provides a clear and logical rationale why monetary and fiscal policy is now likely doing more harm than good to the structure of the economy:

Economists of the Austrian school give another explanation, which resorts to neither Keynesian policy prescription and in which there is no such thing as a “liquidity trap.” Last week I wrote of malinvestments, which are investments made during a boom that cannot be sustained because consumer spending patterns, which ultimately determine production structures within the economy, will not permit investments at their previous levels. (The collapse of the housing boom created the present situation.)

Austrians note that government actually retards economic recovery by holding down interest rates. First, government tends to target new money created by the banking system toward those industries that have become depressed, ignoring the malinvestments that originally put them into that situation. Thus malinvestment persists, pulling capital and resources from economic sectors that originally were not as badly damaged during the boom and subsequent recession.

Second, economist Robert Higgs notes that government activism to end the downturn creates what he calls “regime uncertainty.” In its efforts to “do something,” Higgs notes that governments often are hostile to private property rights and discourage long-term investments by healthy firms. Furthermore government is even more hostile to profitable firms and successful individuals, claiming they are not “paying their fair share” of taxes, making future investment less certain.

The U.S. economy recovered nicely from a severe recession in the 1980s, even with double-digit interest rates and low rates of inflation, which Keynesians would claim to be impossible. True, government spending rose during that time, but not nearly at the rate it has risen the past few years.

There was no “Keynesian situation” then, and there is none today. There only are malinvestments.

If monetary and fiscal policy were at best neutral, why have we seen a complete collapse in monetary velocity? The monetary velocity ratio has collapsed to its lower levels in recorded history going back to 1959.

Though there are many valid criticisms of the velocity of money concept, we do think it does point to one important reality—there is a strong and growing demand to hold greater levels of cash which in itself it a reflection of both fear and uncertainty in the economy. It is also helps explain why monetary stimulation has not sparked the real economy, but has been funneled increasingl into financial assets via bank reserve leakage.

Unless we see a rebound in US demand, coupled with a rise in real income, it seems unlikely to me that real estate will sustain recent gains given what Clive calls “funny money” going into real estate. A break in financial assets means a fall in collateral as many leveraged funds have to sell collateral to cover stock margin. There is big “fund” money now invested in real estate, and much of that investment has been subsidized by our government—you and me, in other words.

Stay tuned.

Jack Crooks

William Shakespear, King Lear

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair