Personal Finance

At one point in my life you might have heard me say something like, “I’ve probably made more money in real estate by accident than I have in the market on purpose.” For many years, you could buy good-quality property, as much as you could afford, and you were almost guaranteed to make money. That ended in 2008. Now folks are looking for bargains, hoping to profit from the crash.

So what has changed? I don’t have to tell you that the commercial and residential real-estate markets took a huge hit in 2008 and have yet to fully recover. Many folks saw the value of their homes drop by 40% or more, and their net worth drop right along with it. In the meantime, bank short sales have skyrocketed.

So what has changed? I don’t have to tell you that the commercial and residential real-estate markets took a huge hit in 2008 and have yet to fully recover. Many folks saw the value of their homes drop by 40% or more, and their net worth drop right along with it. In the meantime, bank short sales have skyrocketed.

Opportunities to buy may be returning, but something else has also changed. Folks on either side of the retirement cusp are in a different place in life than when they bought their McMansions. Children have fled the coop, so their needs have changed. Also, retirees and folks approaching retirement cannot afford a do-over. We no longer have time to recover from investment losses… certainly not if we plan on staying retired.

When we conducted a survey of readers last fall to see what was on their minds, investment wise I mean, real estate investing was in the top 3. The other two were annuities and income investing. We’ve covered both several times, most recently here and here.

With real estate investing a hot topic, I’d like to review theMoney Forever Five-Point Balancing Test and see how it applies to real estate. It’s the test we apply to all of our investments, not just stocks.

- Is it a solid company or investment vehicle?

- Does it provide good income?

- Is there good opportunity for appreciation?

- Does it protect against inflation?

- Is it easily reversible?

Some real estate may indeed meet all five criteria, but folks of retirement age must be much more selective.

My wife Jo and I moved to Fort Myers, Florida in 1985 – about the time that the new airport opened, which allowed bigger jets access to the southwest corridor of Florida. I-75 was also extended south from Sarasota down through Naples and over to Miami. Real estate in the southwest part of Florida exploded.

I had a good friend who put together several partnerships to invest in property. Twenty of us would put up 5% each, buy land, get the necessary permits, and then sell the property to a developer. We did well on several parcels.

One parcel we bought, which I thought would provide the greatest return of all, we still own over 20 years later. We’re still paying property taxes and associated costs after all these years.

The situation is almost funny. We have to pay a farmer to “rent” some cattle in order to maintain our agricultural exemption on the property. While it seemed like a good investment when I was 52, I would pass on it today at age 73. Why? Those types of partnerships do not provide income, nor are they liquid. That means they fail no. 2 and no. 5 on our Five-Point Balancing Test.

We have friends who for years bought homes and apartments, fixed them up, and then rented them out. Some resold them and some converted apartments into condominiums, often doing very well for themselves.

Today these same friends want passive investments. They are quick to remind me that being a landlord means running your own small business. Their investments demanded a big time commitment; they were anything but passive.

Ask any active landlord and he will tell you of the amazing time commitment required – of the 3 a.m. phone calls from the fire department, the plumbing leaks and electrical mishaps, and the renters who never seem to pay on time. Retirees want to make money with their capital. They are not looking for a full-time job.

That’s why most folks on either side of the cusp of retirement are likely better off with investments that meet our Five-Point Balancing Test. That does not mean that rental property or buying property for appreciation is out of the question. But we’re looking for real-estate investments that are professionally managed and liquid. We’ve recently added a real-estate investment in our portfolio that meets all five points in our balancing test. Use this link to start a 90-day risk-free trial to Money Forever and get the full report on our real-estate investment.

Making money in real estate is no easier than it is in the stock market. It requires a lot of work, patience, and in some cases a lot of luck. Retirement is not the time for a “get rich quick” scheme.

We need investments that meet our five criteria. One area of real estate that sadly many retirees have been convinced is the next best thing to a “get rich quick” scheme is reverse mortgages. While not real estate investments as most people view them, they are often portrayed as a way to make easy money during retirement. In response to so many questions from readers about reverse mortgages we’ve put together a new publication called “The Reverse Mortgage Guide” to help you better understand what a reverse mortgage can and cannot do for you and whether you might be a good candidate for one. Click here to find out how to get this report for free.

Must-Reads for Thursday, May 30

Must-Reads for Thursday, May 30

1. Wall Street Breakfast: Must-Know News by Wall Street Breakfast

2. U.S. Dollar Breakout: Gold To $1,250, Silver To $19 By Year End by Mike Williams

3. We’re Just At The Tip Of The Iceberg, Triple Net REITs Will Soon Be A Glacier Sector by Brad Thomas

4. Silver Wheaton: A Buy Even With Lower Realized Prices And A Billion Dollar Debt by Jeff Williams

5. How Much Is This Giant Tech Stock Really Worth? by Gillian Mauyen

6. Electric Utility Investors Should Worry More About Pricing Than Comparable Yields by Jon Parepoynt

7. 2 Potentially Explosive Small Cap Stocks For 2013 by Kelly Berman

8. The Frannie Gamble by Felix Salmon

9. Taiwan Semiconductor Tries To Pull A FinFAST One by Ashraf Eassa

10. Avanir Pharmaceuticals’ CEO Presents at 38th Annual dbAccess Health Care Conference (Transcript)

Most Popular

Fannie Mae And Freddie Mac: All Speculation, Little Value by Dividend Monkey

One Word Separates Apple From $500 by Dana Blankenhorn

BlackBerry Q10 Outsells iPhone 5 And Galaxy S4 In France by Jean-Christophe Larsimont

Real-time Market Update

(Canada’s #2) For a good chance at a happy life, head to Australia, which one again topped the Organization for Economic Cooperation and Development‘s Better Life Index, which looks at the quality of life in member countries.

(Canada’s #2) For a good chance at a happy life, head to Australia, which one again topped the Organization for Economic Cooperation and Development‘s Better Life Index, which looks at the quality of life in member countries.

The (OECD) — an international economic organization — analyzed 34 countries in 11 categories, including income, housing, jobs, community, education, environment, civic engagement, health, life satisfaction, safety, and work-life balance. (You can read the full methodology here.)

We looked at the countries with the highest overall scores, and highlighted a few of the criteria on the following slides.

……view all 15 and their summaries HERE

Many folks are afraid they simply won’t be able to retire — or stay retired — when and how they planned. We can talk about retiring later, taking a part-time job and cutting back on expenses, but those are only partial solutions. Of the seniors who are still working, very few are earning as much as they did at their peak. Their life savings still need to make up the difference.

Many folks are afraid they simply won’t be able to retire — or stay retired — when and how they planned. We can talk about retiring later, taking a part-time job and cutting back on expenses, but those are only partial solutions. Of the seniors who are still working, very few are earning as much as they did at their peak. Their life savings still need to make up the difference.

I receive a lot of letters from very concerned baby boomers and retirees who are watching their principal erode every year, but don’t know what to do about it. Unfortunately, some have unrealistic expectations.

I received a note from a woman in her early 70s who had fired her stockbroker (for good reason) and asked if there was a basket of mutual funds she could invest in that would do the trick. I had to tell her that there simply are no “set it and forget it” solutions anymore.

When our parents retired, CDs earned enough interest to keep their portfolios afloat. As long as they had saved diligently for retirement, they could go on trips and maintain the same lifestyle without much worry.

Today, even if you have a sizeable nest egg, you still need to actively manage your portfolio. Otherwise, it will slip through your fingers.

If you are as concerned about inflation as I am, precious metals are the best place to start. Historically, they have held their value even as governments and currencies collapsed.

No, I do not suggest selling everything and buying gold and silver. There is no one investment that can do everything our portfolios need.

However, a moderate, long-term investment in precious metals will help hedge your portfolio against inflation.

What about additional income to help pay the bills?

One of the reasons the stock market is doing so well is because retirees are desperate. There is no other place left to earn a decent yield, so we have to put our money at more risk than we would like.

The lessons of 2008 are still in the back of our minds — for good reason.

But the Federal Reserve has made it clear that interest rates are going to stay low, so we have to learn to manage the risk to our portfolios as we invest in the market.

In How to Profit from Risk, I recommend allocating a small portion of our portfolio in speculative investments. Retirees have a lot to lose, so high-risk, high-reward investments should represent no more than 10% of our portfolios. And of course, never invest a penny without thoroughly researching an investment. They won’t all be winners, but when one does well, it can take a lot of pressure off the rest of your portfolio.

So if we own precious metals to hedge against inflation and a small number of speculative stocks to relieve the pressure, what should we do with the rest of our portfolio? Again, there is no one answer.

However, every investment in a retiree’s portfolio should be weighed against our Five-Point Balancing Test:

- Is it a solid company or investment vehicle?

- Does it provide good income?

- Is there good opportunity for appreciation?

- Does it protect against inflation?

- Is it easily reversible?

If our portfolio is going to keep up with inflation and provide income to supplement our Social Security checks, a sizeable portion of it should be in reasonably safe investments that will appreciate and provide dividend yield. Putting no more than 5% of our portfolio into any one investment with a 20% trailing stop will further help limit risk. That way, if the stock tumbles, we can’t lose more than 1% of our overall portfolio.

The first cold, hard fact of retirement is that it takes a lot of money. The second is that it takes lots of work. Most of my friends who are doing well in retirement are spending a lot more time looking after their life savings and a lot less time on the golf course than they originally intended. They are, however, enjoying the peace of mind that comes with knowing they are on top of their finances.

Regards,

Dennis Miller

for The Daily Reckoning

Ed. Note: Daily Reckoning email subscribers have regular opportunities to learn specific ways to make a lot of money for their retirement funds. If you haven’t signed up yet, what are you waiting for? Click here now to start getting The Daily Reckoningdelivered directly to your email inbox, every day.

Dennis Miller is the author of Miller’s Money Forever and the free journal, Miller’s Money Weekly. Working with Casey Research analysts, Dennis advises subscribers on how to prepare a bulletproof retirement portfolio and ensure having their own money forever.

Finally, technical evidence of at least a short term peak in most equity markets and sectors has surfaced. Appropriate action is recommended –

(Ed note: Click HERE for the entire interview with Michael Campbel)

MORE NOTES FROM DON

Earnings focus this week remains on the Canadian banks.

Economic news this week is expected to have a neutral impact on equity markets. Data is not expected to change significantly from previous monthly reports. Investors are waiting for more clues about timing of winddown of Quantitative Easing

Currency wars will continue. Volatility in currencies was exceptional last week and is expected to continue.

Short term technical indicators turned bearish last week and intermediate term technical indicators are showing early signs of peaking from intermediate overbought levels. Bearish key reversal patterns were recorded on Wednesday by broadly based U.S. equity indices and most sectors. Broadly based equity indices around the world quickly followed. Initial targets for broadly based U.S. equity indices is to the top of previous trading ranges on the breakout on May 3rd following the surprising April employment report: S&P 500 Index to 1,597, Dow Jones Industrial Average to 14,887 and the NASDAQ Composite Index to 3,307.

Economically sensitive sectors were notable underperformers last week including Industrials, Materials, Financials and Technology, typical underperformance on a seasonal basis for this time of year.

Large cash positions held by Canadian and U.S. corporations continue to be employed in dividend hikes and share buy backs, a short term bullish scenario with long term negative implications.

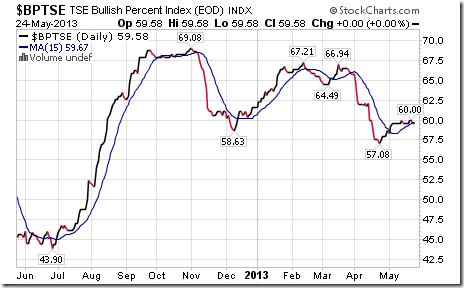

Bullish Percent Index for TSX Composite stocks was unchanged last week at 59.58% and slipped below its 15 day moving average. The Index remains intermediate overbought.

The TSX Composite Index added 54.17 points (0.43%) last week. Trend remains up. The Index found resistance near the 12,900 level. The Index remains above its 20, 50 and 200 day moving averages. Strength relative to the S&P 500 Index changed from negative to neutral. Technical score based on the above technical indicators increased to 2.5 from 2.0. Short term momentum indicators are rolling over from overbought levels.

Percent of TSX stocks trading above their 50 day moving average increased last week to 55.42% from 49.17%. Percent is intermediate overbought.

Percent of TSX stocks trading above their 200 day moving average increased last week to 54.58% from 53.75%. Percent remains intermediate overbought.

For Don’s weekend Charts & Notes of every Market view HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair