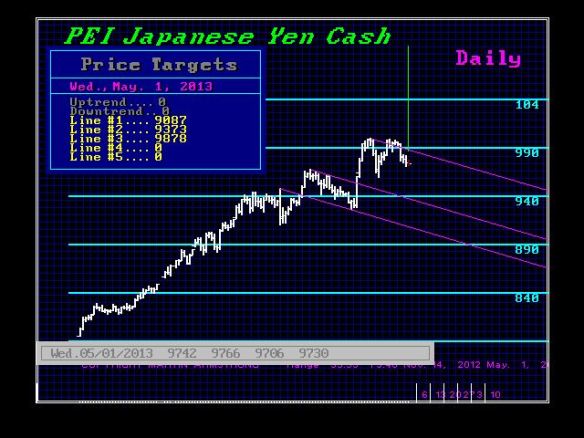

The Japanese yen declined and the dollar made an effective double top at the 99.93 level. This is a big psychological area being par 100. Japanese institutions took profits selling foreign assets since it was the first 20% profit they have seen in 23 years. Nonetheless, only a daily closing BELOW 92.75 would suggest some follow-through. Here we will see most likely a 3rd test of the 100 level, and it may be the 4th time that we plow through it. The highest monthly closing has been 97.40 on the cash. A monthly closing above 97.76 will signal we are starting to breakout, Technical support begins at mid 9300 area with the critical intraday support at the 9000 level. This double top formation is important for it will show the dollar rally that will put the most pressure on the entire global economic system and eventually force the US economy into recession starting 2015.75.

The best trading strategy under these conditions is to sell highs in the Euro according to time against reversals where the risk is the least. In the yen, buy the dollar against support below or on the breakout when that unfolds. Both the euro and the yen are reflecting that we are indeed in a bull market for volatility and when everything turns again with 2015.75 on the ECM, the volatility will be twice as high as what we experienced between 2007-2009. That is where we can see the next phase transition in gold. Don’t forget, gold has yet to test the 1980 high adjusted for inflation which standards at about $2300 level. So forget the hype. Gold has NOT broken out yet nor has it truly made new highs in REAL terms – only nominal.

http://www.mining.com/gold-on-top-no-longer-investors-have-a-new-darling-25556/?utm_source=digest-en-mining-130501&utm_medium=email&utm_campaign=digest

The call for this week: This week will see a large 29 different economic indicators released with the most important being the ADP employment report, initial unemployment claims, the monthly non-farm payrolls report, the Chicago PMI, the ISM Manufacturing report, and the ISM Services report. Such a deluge of economic data within a one-week time period is fairly rare, so buckle up. All such reports can be market moving, but so far the bears, rubbing their collective hands together with glee over the fiscal cliff, sequestration, the continuing resolution, the debt ceiling, etc., have been totally w-r-o-n-g. I feel sorry for the bears waiting for the “crash” they have been expecting for the past four years all to no avail. It looks to me as if the stock market will continue its move irregularly higher until we get indications that something is irrevocably wrong. So far, nothing in the stock market’s internal structure has told us to be anything more than cautious, but NOT bearish.

The call for this week: This week will see a large 29 different economic indicators released with the most important being the ADP employment report, initial unemployment claims, the monthly non-farm payrolls report, the Chicago PMI, the ISM Manufacturing report, and the ISM Services report. Such a deluge of economic data within a one-week time period is fairly rare, so buckle up. All such reports can be market moving, but so far the bears, rubbing their collective hands together with glee over the fiscal cliff, sequestration, the continuing resolution, the debt ceiling, etc., have been totally w-r-o-n-g. I feel sorry for the bears waiting for the “crash” they have been expecting for the past four years all to no avail. It looks to me as if the stock market will continue its move irregularly higher until we get indications that something is irrevocably wrong. So far, nothing in the stock market’s internal structure has told us to be anything more than cautious, but NOT bearish.