Personal Finance

“I think here we’re going to go down 20 percent from the recent top at 1,470. The technical position of the market is poor and the corporate earnings are worsening. And I believe that if the statistics were precise – which they aren’t – (…) I think there’s hardly any growth,” Faber said.

“I think here we’re going to go down 20 percent from the recent top at 1,470. The technical position of the market is poor and the corporate earnings are worsening. And I believe that if the statistics were precise – which they aren’t – (…) I think there’s hardly any growth,” Faber said.

Four months ago, Faber turned his attention to European stock markets, attracted by the low valuations.

“Greece, Italy, Spain, France, Portugal, they were four months ago at the 2009 lows or even lower,” he said.

Faber recommended buying European stocks at the time and for the first time in his life bought them himself.

“I did it simply because the valuations were low. Since then, Greece is up 65 percent,” he said.

He would no longer buy European stocks, he said. “I expect a correction but no new lows,” Faber said.

Now he is focusing on Asia.

“In Asia, Thailand from the 2009 lows is up 250 percent. Other markets like the Philippines, Indonesia, Malaysia, Singapore, are up by a similar amount,” he said. The Chinese benchmark index on the other hand was at 6,000 in 2007, now it is at 2,000.

“I think China and Japan could have a rebound here. If Greece could rebound by 65 percent the greatest garbage could rebound by 65 percent,” Faber said.

Faber: Reduce Government by 50%

The debt burden in the U.S. and other Western countries will continue to increase, Marc Faber, author of the Gloom, Boom and Doom report told CNBC on Monday, leading to a “colossal mess” within the next five to 10 year

“I think the regimes will try to keep the system alive as it is for as long as possible, which means there’s no “fiscal cliff,” there’s a fiscal grand canyon,” Faber told CNBC’s“Squawk Box.”

Faber argued that the political systems in place in the West would allow the debt burden to continue to expand. Under such a scenario of never-ending deficits, the Western world would rack up huge deficits.

One day, the system would break, he said.

“Eventually, you have either huge changes occurring in a peaceful fashion through reforms, or, usually, through revolutions,” he said. The U.S. is getting closer to such a revolution, he said, as is Europe.

“I think the timeframe would be within five to ten years you have a colossal mess … everywhere in the Western world,” Faber said. “I think the deficit here (in the U.S.) — irrespective of who is in the White House — will stay above a trillion dollars per annum for at least as far as the eye can see“.

Bureaucracies in the U.S., as well as Europe, are far too big, he said, and are a burden on the economy.

“My medicine for the U.S. is: Reduce government by minimum 50 percent,” he said. “The impact would be immediately an improvement in the economy.”

Prices are 3-4 times higher in Vancouver & Toronto than average house prices in the United States and more than double their historical average price ratios.

New Mortgage Rules Apply the Brakes to Rising House Prices

Last July 9th. Finance Canada announced changes to the Canadian mortgage market which included a reduction in the maximum amortization period for insured mortgages to 25 years from 30 years; as well as a reduction in the home mortgage loan to value ratio to 65% from 80%. Not only, did it represent the fourth intervention in the rules governing the Canadian mortgage market in as many years, but also, these were the changes which had the biggest market impact. Potential first-time home buyers, who in a typical housing market

It’s not just the US central bank that’s printing money…

European Central Bank (ECB) President Mario Draghi has declared that it will buy unlimited quantities of European sovereign debt.

Japan’s central bank is expanding its current purchase program by around 10 trillion yen ($126 billion) to 80 trillion yen.

The Chinese, British, and Swiss are all adding to their balance sheets.

The largest economies of the world are all grossly devaluing their currencies. This will not be consequence- free. Gold and silver will be direct beneficiaries – as will mining companies – starting with rising prices.

There are other consequences, both good and bad, of gold hitting $2,000 and not stopping there. We think investors should be prepared for the following:

Tight supply. As the price climbs and attracts more investors, getting your hands on bullion may become increasingly difficult. Delivery delays may become commonplace. Those who haven’t purchased a sufficient amount will have to wait in line, either figuratively or literally.

Rising premiums. A natural consequence of tight supply is higher commissions. They won’t stay at current levels indefinitely. Premiums doubled and more in early 2009, and mark-ups for silver Eagles and Maple Leafs neared a whopping 100%.

Swelling profits for the producers. If margins on gold production average $1,000 per ounce now, what will earnings be like when they average $1,500? At $2,000? Gold can rise much faster than operating costs, so this could happen. Imagine what this could do to dividend payouts, especially those tied to the gold price and/or earnings.

Tipping point for a mania. There will be an inflection point where the masses enter this market. The average investor won’t want to be left behind. Will that happen when gold hits $2,000? $2,500?

The message from these likely outcomes is to continue accumulating gold – or to start without delay. Waiting will have consequences of its own.

This is an excerpt from Mark Leibovit’s 19 Page VRGoldLetter published Oct 19th/2012

Do you subscribe to the Leibovit VR Gold Letter? Here is the link: www.vrgoldletter.com. The October 12 edition was sent to subscribers Friday morning. New subscribers receive a 50% discount during the first month.

The Provincial Government released guidelines for the return to the old GST/PST system. Now the change is going to employ more tax collectors and administrators as we fill two Tax Bureaucracies instead of one. At an additional cost of 30 Million more Dollars each year just for Tax Collection, not for Healthcare, Homelessness or Education.

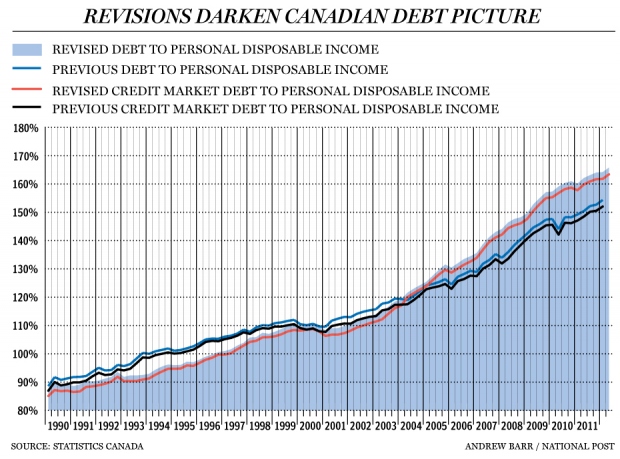

Shortly after the peak in the US housing bubble, Americans’ household debt-to-income ratio reached 170 per cent.

For comparison purposes, Canadian household debt-to-income is now at 163 per cent, according to Statistics Canada.

Canadians’ debt-to-income ratio has soared to 163 per cent, much higher than previously believed, according to revised Statistics Canada figures.

I

nane Housing Comments From Wright

Those comments from Wright are quite amazing. The more leverage one has in housing, the more susceptible personal finances and the economy will be to a sustained downturn in that area.

What really takes the cake however, is Wright’s “hope (the debt) ratio will stabilize” in spite of falling home prices.

Good grief.

In a recession (and one is on the way if not started), layoffs will increase and income will drop. Housing prices and the stock market will both take a hit as well. Thus, debt-to-income ratios will rise and net worth will plunge. Canadians should expect a double whammy.

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair