Personal Finance

Strange. Most investors I talk to think the world is doing just fine. They say the U.S. economy is growing and the gains in employment have been nothing short of spectacular.

They say Europe is not collapsing as so many experts have feared. And that Mario Draghi’s pedal-to-the-metal euro printing is working.

They even claim Britain is doing fine, France will escape its troubles and inflation is coming back.

About the only part of the world they’re negative on is China, claiming that if there’s one single threat to global growth, it’s the Middle Kingdom and nothing else.

Well, I’ve got news for them. This is precisely what the markets want you to believe. They have an uncanny way of first separating you from your money, then washing it all down the drain.

When the markets are acting like this, making almost everyone feel everything is just dandy, or will turn out dandy — risk levels are actually at their highest. Investors are lulled to sleep. They’re complacent. They’ve dropped their guard.

And the next thing that happens? Those investors lose their money, big time.

Look. Markets do not change their major trends all that often. At most, a market may change its major trend once every three years. More commonly, they change trends every five years. And even that is rare. Most major trends persist for at least seven years.

Instead, what happens is this. You get a major trend unfolding on cue, with its cycles. Then you get a pause, a sideways consolidation period, often wrought with pullbacks.

The money that is made during the trending part of the move is often given back during the non-trending, sideways portion. Especially by trigger-happy, impatient investors and traders.

It seems they just can’t stand the fact that all markets need to occasionally take a breather. That all markets need to shake out the earlier investors — so new investors can come in. Or so short-sellers can take profits and cover their positions (in bull markets).

Markets are, yes, living, breathing beasts whose main function is to outwit you. And one of the ways markets do that is to stage what seem like long, sideways periods of tight trading ranges and pullbacks — or rallies in bear markets — that frustrate the heck out of you and force you into making mistakes at the worst possible times — just before the major trends come back to the forefront.

As they are right now. For instance …

A. There is no evidence whatsoever that gold is going to blast off now to $1,400 and higher, as so many pundits would have you believe.

Simply look at my latest neural net forecast model for gold and you’ll see what I mean.

Yes, gold is rallying in the very short term. But the rally is merely short-term noise in the market, designed to throw you off course.

The major intermediate-term trend is lower, into late May. And then the major long-term trend will re-emerge, which is a bull market, and the next leg higher.

So what should you be doing now in gold? You should be looking to buy the decline into May, or if you’re a speculator, you should be shorting gold, looking to make some money as gold slides into a late May cycle low.

Could this model be wrong? Sure it could. But everything I monitor, not just my neural net models, also tells me that gold must pullback — probably to below $1,200 — before the next bull leg higher unfolds.

Ditto for silver, platinum, palladium and for mining shares.

So if you want to be part of the majority that will get eaten up by gold trying to trap you on the wrong side of the market with its meager, very short-term rallies like we’re seeing right now, be my guest: I’ll sell you all the gold you want.

B. Then there’s the dollar right now, another perfect example of a fake-out move that’s going to hurt a lot of analysts, traders and investors. Its recent decline has many of them convinced the dollar is dying again and that other currencies, especially the Japanese yen, are rising to be king of the mountain.

All because the dollar has staged a minor pullback!

You can see it here on this chart I have for you. Actually, it’s a bit of a test, for you to see how much perspective has to do with things.

Most pundits are looking at the decline in the dollar on the extreme right side of this chart.

They see the decline and they shout from the rooftops “The dollar is dead. The dollar is going over an abyss. Death to the dollar!”

And then they come up with all kinds of conspiracy arguments and ridiculous fundamental explanations why the dollar must collapse (and along with it, the USA).

But now, you tell me. Look at the dollar since August 2011 and what do you see? A rather strong, steady uptrend that broke through the top of an uptrend channel in October 2015 …

Then consolidated near the highs with some swings back and forth … and is now merely pulling back to re-test the upper support line of a rising trend channel.

Sorry all you dollar bashers: My 5-year-old son can interpret this chart better than you can.

Now let’s take the analysis a few giant steps forward and run my AI neural net on the dollar, calculating billions of price data points to discern hidden cycles and make a high probability forecast into the future.

Here is the chart. And what does it tell you?

That the dollar is on the cusp of a new, and powerful leg higher, one that could start any day.

That’s just two markets that serve my point: Markets are never what they seem they are, not on the surface. And if you let those surface impressions fool you, not only will you most likely lose treasure troves of money …

You’ll miss out on the really big moves when they do come.

Best wishes,

Larry

P.S. To help you get ready to take full advantage of the bull market of a lifetime, I want to send you a complete Dow 31,000 Preparedness Kit — five distinct free reports! The first free report spells out step-by-step what you must do now to position yourself for amazing profits (and protection) over the next two years. Click here to download now!

Larry Edelson, one of the world’s foremost experts on gold and precious metals, is the editor of Real Wealth Report and Supercycle Trader.

Larry has called the ups and downs in the gold market time and again. As a result, he is often called upon by the media for his investing views. Larry has been featured on Bloomberg, Reuters and CNBC as well as The New York Times and New York Sun.

It’s the same story pretty much everywhere: Cities and states promised ridiculously generous (by today’s standards) pensions to teachers, cops and firefighters, failed to sufficiently fund the plans and invested the money they did have very badly. And now the weight of the resulting unfunded obligations are crushing not just plan recipients but entire communities. Here’s a representative case:

It’s the same story pretty much everywhere: Cities and states promised ridiculously generous (by today’s standards) pensions to teachers, cops and firefighters, failed to sufficiently fund the plans and invested the money they did have very badly. And now the weight of the resulting unfunded obligations are crushing not just plan recipients but entire communities. Here’s a representative case:

Oregon PERS unfunded liability swells to $21 billion

(KTVZ) – This week, Oregon’s Public Employee Retirement System Board received an earnings report on the status of the PERS fund investment. The report said Oregon’s PERS fund fell by 4 percent in 2015, a loss of nearly $3 billion — and a Central Oregon lawmaker said that means major reforms are more urgent than ever.

“The blow to PERS from the Moro court case left Oregon with an additional $5 billion in unfunded liability,” Sen. Tim Knopp, R-Bend, said Tuesday. “Now PERS is an additional $8 billion short of its target.”

In that ruling nearly a year ago, the state Supreme Court overturned the vast majority of the PERS reform cost-saving provisions enacted by the 2013 Legislature.

The current unfunded PERS liability now exceeds $21 billion, up from $18 billion last year, he noted.

PERS Communications Director David Crossley said while the PERS fund earned just over 2 percent last year, it did not achieve the “assumed savings rate” of 7.75 percent, so the liability increased by about $3 billion.

He noted that PERS had positive earnings, but lost value because it pays out about $3.5 billion in benefits a year.

PERS rates for school districts and local governments will rise in July 2017, Knopp said, forcing school districts to lay off teachers, reduce school days, increase class sizes, and cut programs like art and PE. Local governments will also have to make cuts to public safety and other critical services.

This combination of worse-than-expected investment returns and legal barriers to cost savings is playing out across the country. See Fitch downgrades Chicago after “worst possible outcome” in state supreme court pension reform bid.

What follows — “…forcing school districts to lay off teachers, reduce school days, increase class sizes, and cut programs like art and PE. Local governments will also have to make cuts to public safety and other critical services” — is also playing out in most states and cities.

And this, remember, is at the tail end of an epic bull market in financial assets. If pension plans aren’t fully funded now, they’ll fall into an abyss in the coming correction.

The result: everyone gets poorer. Or more accurately, everyone discovers that they were never as rich as they thought they were, and that the down escalator they’re on has a long way to go.

At the risk of belaboring the point, imploding pensions, like most other modern problems, can be traced back to easy money. Put a monetary printing press in the hands of government and the resulting corruption flows from Washington outward to every state capital and mayor’s office. With interest rates artificially low and inflation artificially high, generating 8% returns as far as the eye can see looks not just possible, but easy. So promising benefits based on high rates of return seems reasonable to elected officials anxious to buy labor peace. And once the Ponzi scheme is in place, there’s no way to turn it off without creating chaos.

The only solution (again at the risk of repetition) is to take the easy money program to its logical extreme and devalue the dollar by an amount large enough to make nominal pension benefits affordable. That’s functionally the same as honestly cutting benefits and will impoverish everyone who doesn’t own lots of real assets, but it will be easier to hide.

I just got back from a week in El Salvador with my wife and daughter, and while the trip got off to a rough start — full of delayed flights and lost luggage — we ended up having a GREAT time.

You might think it’s a little crazy to spend spring break in a Central American country that boasts one of the highest murder rates in the world. But as I recently explained in my latest issue of Income Superstars, it is precisely those kind of headline worries that create opportunities for savvy travelers.

To wit …

We stayed in a luxurious oceanfront room, with its own private plunge pool on the balcony, for less than I’ve paid at a budget hotel in Florida.

When I got out of the surf, a guy stood ready to grab my board, throw a towel over my head, and hand me a bottle of cold water — services I would never request but that were just customary in a place that aims to please.

We never spent more than $25 on dinner — for a family of three, including drinks. The typical entrée of local fish, veggies, and corn tortillas was going for about $6 at one of the “fancier” places in town.

On one excursion, my guide pointed out some houses in a new beachfront community and noted they were selling for about $100,000. Speaking of which, El Salvador is officially on the U.S. dollar and has been since the early 2000s.

And healthcare? It’s universal, though I definitely had no desire to visit the nearest hospital about 45 minutes away in San Salvador.

Obviously, visiting a place like El Salvador isn’t for everyone. And choosing to stay there for a longer period of time is probably out of the question for many more.

But I’m telling you all of this because it highlights some of the opportunities that are available outside of the United States … opportunities that can be reached in less than six hours from most major U.S. cities.

So Let Me Ask: Would You Ever Consider Retiring to a Foreign Country?

In just the last year, I’ve been to France, Germany, Italy, Mexico, and El Salvador. And quite frankly, I could have stayed in any one of those places for months on end. The same is true of other countries I’ve visited whether you’re talking about South Africa or Peru.

More importantly, just about everywhere I’ve been I’ve met fellow Americans who are doing just that — living out their dreams in picturesque towns that most people only see on postcards.

Indeed, more and more U.S. citizens are choosing to live abroad — even if it’s just through VERY extended vacations — so they can stretch their retirement dollars further, gain access to affordable medical care, have new adventures, even hire personal assistants for less than a daily meal at McDonald’s.

Consider Panama, a country I visited back in 2001 …

There are spectacular and affordable beachfront condos that you can rent for a few hundred bucks a month.

And on the kind of budget that wouldn’t even cover rent here in the U.S., an expat can retire in impressive comfort in Panama, thanks in part to the country’s special Pensionado program.

You’ve probably heard of it — a special program that allows income-earning foreign retirees to obtain indefinite residence in the country plus get a whole host of other benefits including big discounts on movies, concerts, bus fares, medical services, and a whole array of other things.

Or what about Thailand, which I traveled to eight years ago …

I personally know a number of U.S. citizens who now live there at a fraction of what they spent here. I’m talking about personal chefs, nightly massages, high-speed Internet connections, and beachfront accommodations for less than renting an apartment in Philadelphia or Kansas City.

And although it’s still on my “to visit” list, Ecuador also provides an attractive package for American retirees — including discounts on many services plus the ability to participate in the country’s national retirement system for about $60 a month.

I could keep going all day … Nicaragua, Costa Rica, Malaysia, and countless other places that provide bountiful benefits worth exploring.

Heck, I have one friend near retirement who plans on buying a sailboat and spending the first part of his golden years going wherever he wants!

At the end of the day, the point I’m trying to drive home is that increasing income is certainly one way to better your situation no matter what your age. But changing your perspective, cutting costs, and considering less-traveled paths is certainly another — and complementary — way to get the things you want out of life.

So get out there and do some research. You’ll be amazed at what you find. And if you’re already living your dream, don’t hesitate to write in and tell me about it!

Best wishes,

Nilu

With the markets bouncing around and headlines in the financial media designed to cause concerns, I thought it might be worthwhile to provide a broader context to the current environment and how that environment impacts your portfolios. As always, I will refrain from trying to outsmart the market by predicting its short term direction because the market will always conspire to make such prognosticators look foolish. That said, I do wish to provide a framework of understanding.

The most important consideration to keep in mind is that your portfolio is mathematically designed to dampen exactly the kind of volatility that the market is exhibiting now. This is done by our group constructing your portfolio with negative correlation. In other words, we use positions which move up or down based upon different economic inputs, such as interest rates and commodity prices. Each and every position in your portfolio is carefully selected because we feel it will be profitable, but each position (or groups of positions) will react slightly differently to one another over any shorter term economic environment. For instance, despite the correction in equity prices generally, the world’s largest gold miner, Barrick Gold, has risen over 130% since last September.

The key take-away is that your portfolio is not the market.

It has been constructed to deliver the greatest possible rate of return for your given level of risk based upon the proven and Nobel Prize winning mathematical concept of Modern Portfolio Theory. So strong is this process, and our proprietary interpretation of it, that each client model portfolio was profitable in 2015, ranging from +3.25% to +7.85% (net-to-client) despite the fact that virtually every indices in North America and globally was negative over the year.

But what of the market as a whole and the prospects for the current year? It is important to understand that despite the fact that your portfolios hardly were impacted, from the fall of 2014 until the recent bottom of the market on January 20th, the TSX fell an astounding -27%. This collapse more or less imitated the 70% collapse in oil prices over much of the same timeframe.

It is a difficult number to get your head around; just imagine if we had a 27% correction in real estate prices here in Vancouver or in Toronto. But that couldn’t happen could it, because real estate prices in Vancouver never go down, do they? I suggest you watch The Big Short, or at least watch this BNN interview:

http://www.bnn.ca/Video/player.aspx?vid=818699

But I digress. In fact the TSX is now more than 12% below where it was back in 2007 before the financial crisis, some 9 years ago.

Similarly, the Dow Jones in the U.S. has fallen some 15% from its peak in 2015. Global markets have corrected more than 23% from their peak in 2015.

What this suggests is that the equity markets contain much less risk than they did previously and clearly have more potential upside. The question of course, is ‘when will they achieve that upside potential’?

Those that are fearful and therefore are selling equities in this environment point toward a shaky U.S. economy and China growing at a lower rate than it has in previous years. Let’s review the current economic topography.

While we always need to be careful because market corrections and talk of recession can sometimes become a self-fulling prophesy, the reality is that the U.S. is in a real, although anemic, recovery. It is extremely unusual to have a sustained major market correction without a recession proceeding it. This would suggest that the current U.S. equity market has perhaps already seen its lows. As an example, the giant JP Morgan Chase is trading at just 9.4 times its earnings and throwing off a dividend of over 3%.

China’s rate of growth is slowing and its demand for commodities is falling, but this has been happening for almost 5 years and should not come as a surprise. Keep in mind that while the Chinese economy is the second largest economy by size in the world, it is not the second most important. The reason is because they are not yet global consumers. They are not buying goods manufactured in North America or Europe, at least not in large enough quantities to be impactful. A lower growth rate in China should have little effect outside of a slowing demand for commodities, which as mentioned, is something fully baked into future financial expectations. While their volatile stock market is down –50% since last year, again this should have little direct impact on the global economy for the same reasons. Eventually the domestic economy in China will indeed have more of a global impact, but this will not happen until China converts from an export dominated economy to one sustained internally by its consumers.

The TSX here in Canada has tracked the collapse in oil prices over the last 18 months. However, energy prices have stabilized to a degree and technical charting suggests that they may indeed have already bottomed. This bodes well for the TSX, where many of the companies listed on our market fell based solely upon their association to Canada and the TSX. Many companies we own such as Bank of Montreal and Manulife Financial are now trading at 10 times or less next year’s earnings yet have dividend yields over 4%. This would suggest that these companies are attractive at the current prices. Evidently international markets agree as the TSX has been the top performing major index in the world since January 1st of this year.

Nothing, of course, is certain and volatility over the next few months no doubt will continue (please see Ethan Dang’s column), but the fact remains that the current market is much less expensive than it was 18 months ago and by most metrics, inexpensive in general. The best part of this scenario is that despite the correction in equity prices over the past 18 months, your portfolio was hardly impacted (please see the most recent performance numbers in the performance tab on this email), and each model portfolio is well positioned for the eventual recovery.

Have a great week!

Neil

Indecisive Market Direction

by Ethan Dang, CFA, MBA

This year continues to display uncertainty and indecisiveness for global equity markets as investors grapple with slowing global growth against the conviction of global central banks to support equity markets through expanded monetary stimulus. The latest example is the Bank of Japan’s move to implement negative interest rates on January 29th in order to encourage its citizens to spend and its banks to increase lending. Equity markets remained volatile in February. Volatility may be ideal for day traders, but can be emotionally draining for long-term investors. In this type of environment, it is very important to stick to the plan and focus on risk management and diversification.

Consistently Working In Our Clients’ Best Interest

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable

for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them, having regard to their own particular circumstances. Richardson GMP Limited is a member of Canadian Investor Protection Fund. Richardson is a trade-mark of James Richardson & Sons Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

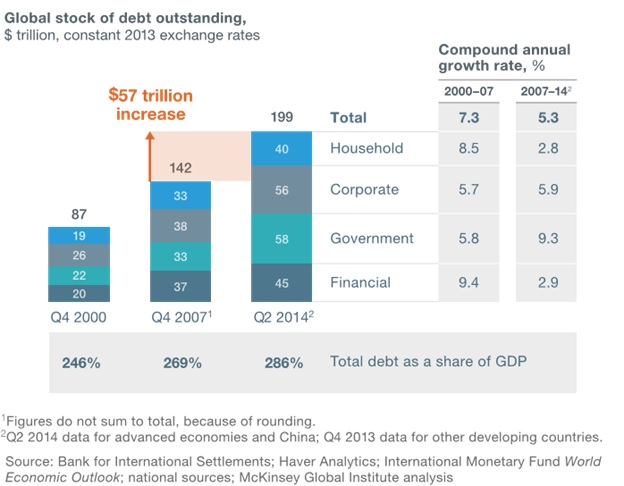

The major global economies have had a staggering debt of $199 trillion as of Q2 of 2014. The most recent figures will be closer to $230 trillion because, after 2014, the ECB, Japan and China have all resorted to ‘massive monetary easing’ programs while the US debt continues to escalate, with every passing second. The total debt, as a percentage of GDP, stood at 286%; the latest numbers will prove to be much worse.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair