Personal Finance

One of the groups of investors that’s the most mistreated by Government is the millions who have responsibly saved for their retirement. This analysis is based on American figures but is relevent to Canadian investors just as well – Money Talks Editor

Income Inequality is a Problem – When Caused by Government Meddling

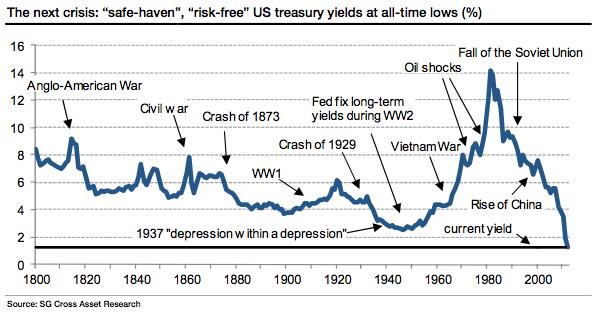

When I entered the investment business as a stock broker at Merrill Lynch in the 1980s, savers could routinely get 7-9% on their money with riskless CDs and short-term Treasury bonds.

In fact, I sold multimillions of dollars’ worth of 16-year zero-coupon Treasury bonds at the time. Zero-coupon bonds are debt instruments that don’t pay interest (a coupon) but is instead traded at a deep discount, rendering profit at maturity when the bond is redeemed for its full face value.

At the time, long-term interest rates were at 8%, so the zero-coupon Treasury bonds that I sold cost $250 each but matured at $1,000 in 16 years. A government-guaranteedquadruple!

Ah, those were the good old days for savers, largely thanks to the inflation-fighting tenacity of Paul Volcker, chairman of the Federal Reserve under Presidents Jimmy Carter and Ronald Reagan from August 1979 to August 1987.

Monetary policies couldn’t be more different under Alan “Mr. Magoo” Greenspan, “Helicopter” Ben Bernanke, and Janet Yellen. This trio of hear-see-speak-no-evilbureaucrats have never met an interest-rate cut that they didn’t like and have pushed interest rates to zero.

The yield on the 30-year Treasury bond hit an all-time record low last week at 2.45%. Yup, an all-time low that our country hasn’t seen in more than 300 years!

These low yields have made it increasingly difficult to earn a decent level of income from traditional fixed-income vehicles like money markets, CDs, and bonds.

Unless you’re content with near-zero return on your savings, you’ve got to adapt to the new era of ZIRP (zero-interest-rate policy). However, you cannot just dive into the income arena and buy the highest-paying investments you can find. Most are fraught with hidden risks and dangers.

So to fully understand how to truly and dramatically boost your investment income, you absolutely must look at your investments in a new light, fully understanding the new risks as well as the new opportunities.

There are really two challenges that all of us will face as we transition from employment to retirement: longer life expectancies; and lower investment yields.

Risk #1: Improved health care and nutrition have dramatically boosted life expectancies for both men and women. We will all enjoy a longer, healthier life, which means more time to enjoy retirement and spend with friends/family, but it also means that whatever money we’ve accumulated will have to work harder as well as longer.

Today, a 65-year-old man can expect to live until age 82, almost four years longer than 25 years ago; the life expectancy for a 65-year-old woman is also up—from 82 years in the early 1980s to 85 today.

The steady increase in life expectancy is definitely something to celebrate, but it also means we’ll need even bigger nest eggs.

Risk #2: Don’t forget about inflation. Prices for daily necessities are higher than they were just a few years ago and constantly erode the purchasing power of your savings.

The way I see it, your comfort in retirement has never been more threatened than it is today, and it doesn’t matter if you’re 20 or 70.

The rules are different, and you only have two choices:

#1. spend your retirement as a Walmart greeter (if you’re lucky enough to get a job!); or

#2. adapt to the new rules of income investing.

Today, the new rules of successful income investing consist of putting together a collection of income-focused assets, such as dividend-paying stocks, bonds, ETFs, and real estate, that generate the highest possible annual income at the lowest possible risk.

Even in an environment of near-zero interest rates and global uncertainty, there are many ways an investor can generate a healthy income while remaining in control. Income stocks should form the core of your income portfolio.

Income stocks are usually found in solid industries with established companies that generate reliable cash flow. Such companies have little need to reinvest their profits to help grow the business or fund research and development of new products, and are therefore able to pay sizeable dividends back to their investors.

What do I look for when evaluating income stocks?

• Macro picture. While it’s a subjective call, we want to invest in companies that have the big-picture macroeconomic wind at their backs and have long-term sustainable business models that can thrive in the current economic environment.

• Competitive advantage. Does the company have a competitive advantage within its own industry? Investing in industry leaders is generally more productive than investing in the laggards.

• Management. The company’s management should have a track record of returning value to shareholders.

• Growth strategy. What’s the company’s growth strategy? Is it a viable growth strategy given our forward view of the economy and markets?

• A dividend payout ratio of 80% or less, with the rest going back into the company’s business for future growth. If a business pays out too much of its profit, it can hurt the firm’s competitive position.

• A dividend yield of at least 3%. That means if a company has a $10 stock price, it pays annual cash dividends of at least $0.30 a year per share.

• The company should have generated positive cash flow in at least the last year. Income investing is about protecting your money, not hitting the ball out of the park with risky stock picks.

• A high return on equity, or ROE. A company that earns high returns on equity is usually a better than average business, which means that the dividend checks will keep flowing into our mailboxes.

This doesn’t mean that you should rush out and buy a bunch of dividend-paying stocks tomorrow morning. As always, timing is everything, and many—if not most—dividend stocks are vulnerably overpriced.

But make no mistake; interest rates aren’t rising anytime soon, and the solid, all-weather income stocks (like the ones in my Yield Shark service) will help you build and enjoy a prosperous retirement. In fact, you can click here to see the details on one of the strongest income stocks I’ve profiled in Yield Shark in months.

Tony Sagami

![]()

30-year market expert Tony Sagami leads the Yield Shark and Rational Bear advisories at Mauldin Economics. To learn more about Yield Shark and how it helps you maximize dividend income, click here. To learn more about Rational Bear and how you can use it to benefit from falling stocks and sectors, click here.

Over the years, I’ve explained a lot of Wall Street’s “secrets”…

I’ve explained how discounted bonds are sometimes vastly better investments than stocks. I’ve covered how selling naked puts is almost always safer and more profitable than buying stocks outright.

These concepts (and others) are critical to active investors. They all play a role in giving you the tools you need to increase your returns. You ought to know all about them and be able to use them tactically to take advantage of opportunities in the market.

I’ve written about these concepts many times over the years. And I’ve said they’re the “most important” thing I could teach you from time to time. I wasn’t lying. All of these strategies have their “time in the sun.”

Believe me… having this tool bag and knowing when to use these strategies will make you a much better investor. It will allow you to profit from opportunities the market always creates.

But… how can you learn to be patient enough to wait for these opportunities? That’s what I’d like to show you with today’s essay. I hope you’ll print this one out… mark it up… and keep it near your desk.

The real secret is in this one…

So what’s the most important idea I’ve discovered in finance? What’s the one thing I’m going to teach my kids beyond the obvious stuff about saving, compounding and risk management? What do I believe is the real secret to investment success?

And… the biggest question of all… How do I invest my own money in securities?

Over the long sweep of your investing lifetime, strategies that only work extremely well in certain market situations are unlikely to play a dominant role. The big secret, therefore, is something you can use all the time, for your entire life, as an investor. And here it is: Some companies are much better than others at compounding capital. Much better.

If your goal as an investor is to compound your savings over time, wouldn’t it be easier to simply figure out which companies will compound your capital at an acceptable rate, buy those firms (and only those firms) at reasonable prices and then do something else with the rest of your time?

Here’s a simple but powerful example…

Well-run insurance companies can produce what’s called an “underwriting profit.” They are literally paid money in advance to manage your capital. And they get to keep not only the investment profits, but profits from the premiums, too.

That’s like paying the bank to keep and use your money. No other business can compound capital so consistently.

Insurance companies have other fantastic advantages, too. They’re able to legally defer most of their taxes. They’re nearly immune to economic factors. They’re scalable. I could go on…

They’re a focus for us because well-run insurance companies are legendary compounders of capital. Buy them at reasonable prices, and it’s impossible not to do well.

In the March 2012 issue of my Stansberry Investment Advisory, we explained that insurance stocks had rarely been cheaper. We recommended several through the year. Since then, stocks of all stripes have exploded higher… but they haven’t outpaced insurance companies.

Insurance stocks as a whole – as measured by the SPDR S&P Insurance Fund (KIE) – have far outpaced the S&P 500.

It’s not an accident that the greatest investor in history, Warren Buffett, has long focused on insurance stocks and other companies that are highly capital efficient. That is, companies that are natural wealth-compounders.

Starting with his 1972 investment in See’s Candies, Buffett gradually over the years shifted the bulk of his wealth into a simple, long-term compounding strategy…

While Buffett didn’t abandon all other forms of investing, his largest allocations since 1972 have all used this compounding strategy. That famously includes his 1988 purchase of Coca-Cola… when Buffett put roughly 25% of Berkshire’s capital into a single stock!

And it wasn’t a cheap stock, either. At the time, Coke was trading for 16 times its annual earnings. Buffett had figured out the one real secret of finance… the one secret to “rule them all.”

To use a long-term compounding strategy effectively, you really only have to answer three questions:

- First, is the company in question able to produce very high returns on its assets? In other words, is it a great business?

- Second, are these unusually high returns very likely to continue for decades, without requiring large and ongoing capital investments?

- Third, can the management of the company be trusted? Will bankruptcy never be even a remote possibility?

If the answer to these questions is “yes,” then all you have to do is simply not pay too much when you buy the stock. Most of the companies that fit these criteria are branded consumer-products companies – stocks like McDonald’s, Coke, Heinz and Hershey.

Buffett explained in his 1983 shareholder letter how he thinks about these companies. The secret to their long-term earnings power is very simple: It’s their brand and the relatively unchanging nature of their products.

These companies’ products are so well known (and adored) by customers that these firms can constantly raise prices to keep pace with inflation.

Meanwhile, the brands – while requiring some advertising – aren’t like factories, gold mines or drugs…

They don’t require massive investments of new capital. There’s no new gold mine to find and build. There’s no patent that’s going to expire. And there’s not even any new product that must be created: Coke’s fans went crazy with anger when the company tried to change its product in a small way back in 1985.

All these firms have to do is continue to deliver the same thing, year after year. And that means they can afford to return huge amounts of capital to shareholders.

Merely buying and holding any of the stocks I mentioned above would have made you 15% a year if you’d just reinvested the dividends for the last 30 years.

Even if all you did was invest $10,000 and then nothing else – not a penny more – you’d still end up with $575,000 at the end of 30 years. If you invested $10,000 annually, you’d end up with $4.3 million.

And the best part? This approach can be used by anyone.

The math is simple. And is it really that hard to realize that Heinz is the best sauce company… that Coke is the leading soft-drink business… or that McDonald’s makes the best hamburgers for kids?

The No. 1 objection I get from readers when I talk about this strategy is: “That’s great, Porter. Wish I’d known about that when I was 25. But it’s too late for me now. I don’t have 30 years.”

That’s nonsense. Think about it this way… Buffett was born in 1930. He didn’t buy Coke until 1987. He was 57 years old. It has been one of the greatest investments of his life – bar none.

If that doesn’t convince you, just think about it this way. How often do you make more than 15% on your portfolio in a year? Whether you’ve got three decades to invest or only one, you should aim to produce the highest possible annual return without putting your capital at undue risk.

There’s no safer investment approach than this one, as your returns are being manufactured by great businesses. You don’t need a “greater fool” to pay too much for your shares to make a profit. In fact… the biggest risk you face is selling at all because that will trigger taxes (in most accounts).

It’s this seemingly invisible power that allows these companies to return massive amounts of capital to shareholders – a factor that sets them apart and greatly reduces investor reliance on capital gains. This is incredibly important over the long term.

P.S. In Stansberry’s Investment Advisory, Porter and his team have used these simple concepts to help subscribers make big returns on safe, high-quality stocks.

He also has a long track record of calling important economic trends… like the mortgage crisis that bankrupted Fannie Mae and Freddie Mac and the downfall of American icon General Motors.

In his new book, America 2020, Porter describes a new looming crisis in the US economy – one that could be worse than the financial meltdown we faced in 2008. And most importantly, he explains how you can protect yourself from it. It’s yours today for just the cost of shipping – Click Here for America 2020 – The Survival Blueprint.

Dow up big time – 259 points, or 1.5%

Dow up big time – 259 points, or 1.5%

Gold up too – to over $1,300 an ounce.

This year is going to be a hoot. Boom, bust, lies and claptrap – we’re going to have it all!

What accounts for yesterday’s big bullish surge? From Bloomberg:

The MSCI Emerging Markets Index added 0.8% to 983.53. Russia’s dollar-denominated RTS Index rose the most in the world and the ruble strengthened as the ECB’s move encouraged investors to buy riskier assets.

Gauges in Poland, Hungary and the Czech Republic increased at least 0.9%. Oil producer Petroleo Brasileiro led gains in Brazil. Asian stocks jumped as China pumped funds into the financial system.

ECB President Mario Draghi unveiled a quantitative easing plan of 60 billion euro a month until at least the end of September 2016. The move, which is intended to counter slowing growth and the threat of deflation, may spur capital inflows into developing countries. China’s monetary authority used open-market operations to add cash to the financial system for the first time in a year and spurred loans amid a fund shortage.

Awe and Wonder

Will this bold move help the euro-zone economy? Will it make Europeans richer, happier, better lovers or better sportsmen?

Not if it works like the US version.

The funniest part of this story is that Draghi made his announcement with a straight face. What a comic – a real Leslie Nielsen. As we saw yesterday, the average American is poorer than he was before the QE programs began.

But all over the world, speculators are running wild. In a single day, following Draghi’s big news, they made a cool $1 trillion.

Where does this money come from?

Corporations are not worth a penny more than they were on Wednesday. Why would they be? All that has happened is that the European Central Bank has pledged to use money it doesn’t have to buy assets that are already extraordinarily expensive.

Bonds from Italy, Spain and France are already priced at levels never before seen in human history. On the evidence, never have investors had more faith in European governments’ ability to service their debt… or more faith in the currency in which their obligations will be honored.

This alone makes our mouth drop in awe and wonder. Never before in history have these very same governments been so deep in debt with so little prospect of ever paying that debt back. And never before have their central bankers been so openly committed to devaluing the money they are supposed to be protecting.

All of which is mind-boggling… extremely funny… or both.

Europe’s QE program is supposed to “counter slowing growth and the threat of deflation.”

But how does Mario Draghi know how fast an economy should grow? How does he know what prices should be?

Oh, we are being mean-spirited to ask. It’s like asking an aging prizefighter if he really needs another blow to the head; we’re just making fun of him.

Yes, another giant money-printing scam is under way – this time in Europe. This will put two of the world’s biggest economies – Japan and Europe – in full liquidity-pumping mode.

The dollar goes higher. American chests fill with pride – apparently unaware that they are losing the “race to the bottom.”

Their exporters will find their sleds rubbing up against hard stone and soft mud. Especially their oil exporters! For the price of oil has dropped in half in the last six months.

Silver Linings… No Clouds

According to TV’s Larry Kudlow, the US enjoys the equivalent of a “giant tax cut” thanks to low oil prices.

Nine months ago, he said it was enjoying an “economic renaissance” thanks to high oil prices (which brought a boom in the fracking states).

What a great time to be an investor. Silver linings everywhere – with no clouds. And when you are riding your bike, all roads are downhill.

Yesterday, we promised to tell you why America’s middle classes have lost ground.

It barely seems possible. America is the crown of capitalism, isn’t it? And doesn’t the 21st century – which we live and breathe every day – carry in its balmy air the elixir of growth, progress and riches beyond our imagination?

How is it possible… with so many more lawyers… so many more economists… so many more public servants – all striving, sweating, straining to make life better for us all – that we have less real, spendable wealth than we had before the century began?

State of the Union

We are staggered by the question.

And once we recover our footing, we will come up with an answer. It is too big a subject to tack onto this Diary entry, but we will give a hint by asking another question:

Who makes life better? Who actually adds to humans’ wealth, happiness and the quality of their lives?

Politicians?

Government employees?

Economists?

Lawyers?

Is it the people who say they are working to create a better world – like President Obama in his State of the Union address:

… helping working families feel more secure in a world of constant change… That means helping folks afford child care, college, health care, a home, retirement – and my budget will address each of these issues, lowering the taxes of working families and putting thousands of dollars back into their pockets each year.

Or is it another class of people altogether – people who are too busy turning out products and services to feed you a line of B.S.?

You can guess. But you may not know that those people are disappearing.

More about them on Monday…

Regards,

Bill

Further Reading: Enjoying Bill’s insight into the world of history, finance and economics? Why not go right to his sources for more? We are giving away a Kindle loaded with 33 of Bill’s favorite books on history, economics, investing and life. All you have to do to enter to win is answer one simple question.

Market Insight:

“Grexit,” Part II?

From the desk of Chris Hunter, Editor-in-Chief, Bonner & Partners

At least America is not Greece…

As you can see from today’s chart, from Gallup, fewer than 1 in 5 Greeks approve of their country’s leadership.

Which is probably why Greek voters are on track, according to the latest polls, to elect the radical left-wing Syriza party to government.

Syriza wants to tear up the country’s bailout agreement because of what it claims are unfair austerity clauses that come with its emergency loans.

If Syriza wins an outright majority, expect to see the dreaded “Grexit” term fill newspaper headlines once again.

This could become even more pronounced if Syriza fails to win an outright majority and is forced to form a coalition government with an even more radicalized left-wing party (which are in no short supply in Greece these days).

Of course, it’s yet another sign of our Hall of Mirrors economy that a Greek political party can complain about “austerity” when the country has a debt-to-GDP ratio of 177%.

We suspect renewed worries over the political and economic integrity of the euro zone could soon rain on Mario Draghi’s victory parade…

P.S. Have you joined our competition to win Bill’s personal investment library? We’re giving away a Kindle loaded with 33 of Bill’s favorite books. For a chance to win, all you have to do is answer the following question.

Shopping malls across America are going to look a whole lot emptier soon. An exodus of giant retailers is beginning with the announcement of hundreds of store closures and thousands of people newly unemployed.

Shopping malls across America are going to look a whole lot emptier soon. An exodus of giant retailers is beginning with the announcement of hundreds of store closures and thousands of people newly unemployed.

The first of January, I broke with my usual tradition and wrote not about positive resolutions, but about the impending rockslide of the US economy. And “rockslide” is an apt word: as one thing starts rolling down the mountain, it will pick up other things until a veritable avalanche of other businesses and people are affected and rolling pell-mell right alongside.

Last year, we saw announcements of the expected closure of some retail giants. In February of 2013, Michael Snyder wrote on The Economic Collapse Blog that we would see the following:

…..read more HERE

With the gold market soaring and major turmoil in currency markets on the heels of the stunning news out of Switzerland, today one of the great minds in the business sent King World News a timely piece that contains the wisdom of Jim Rogers and Benjamin Graham

With the gold market soaring and major turmoil in currency markets on the heels of the stunning news out of Switzerland, today one of the great minds in the business sent King World News a timely piece that contains the wisdom of Jim Rogers and Benjamin Graham

….continue reading HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair