Personal Finance

Market Analysis plus Simple Strategies to Employ When Buying Stocks – Editor Money Talks

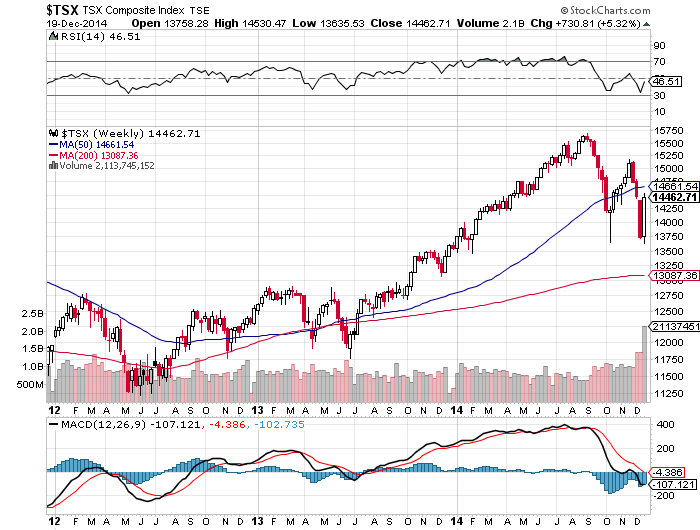

The TSX Composite Index closed the week at 14,468 points, up a solid 5.7% after 4 straight days of gains. This week’s partial recovery was a welcome sigh of relief to investors who nervously watched the market shed almost 10% of its value in the 3 week period ending last Monday.

Click on the image for the more dramtic Daily Chart

But before investors get too complacent let’s remind ourselves that we are not out of the woods yet. The culprits that

brought on this malaise were low energy prices coupled with a weak outlook for global growth. It may be the case that the former will help to bolster the latter as few things are more economically simulative as a big drop in energy prices. But at least in Western Canada the economic wagon is firmly tied to the price of oil which has yet to offer a clear sign it has stabilized.

But consumers at least are benefiting from a quasi-tax break at the pump with the average gasoline price in Canada declining below a dollar to $0.99 per liter for the first time in 4 ½ years. This is a far cry from just a few months ago when the average price was over $1.30 per litre. Over the course of a year, many analysts suggest that this can result in savings of $1,000 to $2,000 per family. Time to max out those TFSA contributions!

One of the issues that we have had with the Canadian stock market and economy in general is that it is too focused on resource related sectors. Energy alone accounts for nearly 25% or ¼ of the entire TSX Composite index. With mining and materials accounting for another 9%, we have nearly 35% of our top stock exchange weighted to the two most cyclical industries in the world. Technology on the other hand (an industry which we should be focused on growing) accounts for a measly 2%. This is compared to a technology weighting of 20% for the S&P 500 in the U.S. Clearly our capital markets and economy needs to diversify and it is times like these when this concept really hits home.

——–

Simple Strategies to Employ When Buying Stocks

1. Build your Portfolio Gradually over Time: There is a general tendency for the investor to want to put all of their capital to work immediately. We strongly advise against rushing in and becoming fully invested right away. Our opinion is that it is usually better to take 6 to 18 months to build a portfolio if you are starting from scratch. Taking this time allows you to keep some capital available to purchase new recommendations that come out over the course of the year. Spreading the portfolio building process also mitigates the risk of short-term market volatility and gives you the opportunity to purchase attractively priced stocks during market bottoms.

2. Buy Businesses with Recession Resistant Qualities: This is a theme that has always been a key ingredient of our investment philosophy. With the threat of economic contraction always looming, it is advisable to build your portfolio around a core of recession-resistant businesses. These can be conventional industries with recession resistant traits such utilities and infrastructure, or it could be a special situation company that occupies a valuable niche position in an attractive market.

3. Buy Strong Balance Sheets: This is another theme that has remained core to our strategy. We continue to favour companies with strong financial positions. An ideal situation would be a company with a significant cash balance and little to no debt. Not only does that cash provide a protective buffer for the company in the event of a downturn but can also be employed to purchase “on sale” assets during periods when competitors are having difficulty accessing capital. Realistically, companies that operate in highly capital-intensive industries will utilize debt in the capital structure (and utilize it well) and may find avenues to invest excess cash as soon as it is generated. The objective as an investor is to ensure that you are not buying a company that is leveraged with debt which makes it more susceptible to economic and market contractions.

4. Diversify by Sector: Try to avoid accumulating too many stocks that operate in the same (or similar industries) sectors or are dependent on the same geographies. Within your 8 to 12 stock portfolio, you will have room to diversify into a multitude of different industries and geographies. Companies that operate in the same industry (and often geography) are exposed to many of the same risks. Diversifying provides significant risk management to your portfolio.

5. Don’t Be Afraid to Layer into Positions: Just as we recommended that you build your total portfolio over time, it is sometimes prudent to build positions in individual stocks over time. For example, if you plan to purchase a total of $10,000 of shares in a single stock, you can break that position up into two or more separate purchases. This can help you to mitigate risk and benefit from volatility that occurs through the year. Individual reports provide specific instructions in this regard when appropriate (such as “BUY HALF” recommendations).

11/28/2014

NATIONAL AND INTERNATIONAL WIRELESS RETAILER GLENTEL RECEIVES 121% TAKEOVER BID FROM BCE INC. – SELL

….to take advantage of the:

Tax Loss Silly Season

Tax Loss Silly Season

by Bob Moriarty 321Gold

I read something a couple of days ago about the Tax Loss season. When investors take a hit, they tend to dump the shares in December to move into something else. They take the loss and write it off. The interesting thing about the Tax Loss season is that for the past 11 years if you bought the gold/silver indexes on Dec 22 and all you did is hold for 90 days you would make a profit. That is if you were smart enough to take profits, many people aren’t.

It seems pretty obvious that we have been in a major bottoming pattern for two months with the resources. They are thoroughly hated and despised by burned out investors still licking their wounds. There will be a lot of selling of stocks this Tax Loss Silly Season. If you are smart enough to duplicate last year, buy the stuff now and hold it for 90 days. I have identified a couple of companies that have been beat and battered in spite of good news.

….read of the opportunites HERE

The markets at end of 2014 are setting up an interesting 2015. Over the last few weeks on Money Talks, you’ve heard warnings from many advisers concerned about where the public markets are heading. Are we setting ourselves up for the fear factor to sell high while the smart money waits to buy low? Thankfully there is now a clear alternative to the jitters of the public markets.

The markets at end of 2014 are setting up an interesting 2015. Over the last few weeks on Money Talks, you’ve heard warnings from many advisers concerned about where the public markets are heading. Are we setting ourselves up for the fear factor to sell high while the smart money waits to buy low? Thankfully there is now a clear alternative to the jitters of the public markets.

I’m a big believer in not worrying about being the smartest person in the room. What’s more important is to be wise enough to hear the smartest idea in the room, in other words sifting the chatter from leading institutional funds and institutions.. What are the current trends that the average investor needs to know to ensure a preservation or growth of their financial portfolio?

There’s a trend over the last 2 years that many haven’t recognized and that most advisers have failed to see or inform their clients. The growth of the alternative / private equity investments has been substantial over the last two years. In fact, according the Chair of the OSC (Ontario Securities Commission), Howard Wetston, more money was raised last year in Canada in the private markets than the public markets. This trend continues year over year.

Twenty years ago, a typical institutional fund had 2% – 5% weighting in private and alternative investments. That all changed when the Yale Endowment Fund was launched over 20 years ago by the legendary investor, David Swensen. Over the last 20 years, the fund has generated 13.7% annual returns compared to the S&P 500 of 8.8%. As of June 2012, the fund has over 66% of its funds in alternative and private investments. Many funds have been trying to catch up like the Canada Pension Plan (17.3%) and Ontario Teacher’s Pension (23%). In fact, according to a Mercer survey in 2013, 38% of Canadian pension funds are investing in alternatives, compared to 25% of funds in 2010.

What other trends should investors to take note of? According to Byron Wien, Vice Chair of Blackstone Advisory Partners, people need to temper their expectations for 2015 with a best case scenario of single digit returns. The S&P 500 has surged 40% over the last two years with high valuations returning to 18 times earnings, which means expansion based on earnings alone is largely over. Despite strong economic news for the US economy, how strong does it have to continue to keep valuations at this high level?

How about wealthy investors, what are they doing in 2015? According to a survey by Tiger 21, an investor network of high net worth people with a minimum of $10MM in assets, the response was mostly that people were keeping with the status quo. The three assets that most wanted to increase in 2015 was cash, private equity and real estate.

If you want to look at allocating some of your portfolio towards private or alternative investments, look for an experienced adviser that can help you find what plan is best for you. To learn more, visit our website at www.triviewcapital.com.

During the mating season, the male Iberian emerald lizard changes color from the neck up. This transformation from green to turquoise is a double-edged sword for this tiny reptile. On the one hand, the male lizard’s vibrant colored-headdress gives him a leg up when trying to attract female lizards, but on the other hand, his loss of camouflage amidst the green woodlands of Spain and Portugal makes it easier for birds of prey roaming the skies from above to spot him.

Through the evolutionary process of self-selection, nature took care of this potentially dangerous facial makeover. In order to avoid detection, the lizard’s head reflects light differently depending on the angle of observation. From the perspective of a bird’s-eye view, the emerald lizard still maintains its greenish camouflage, providing protection from predators flying above it in search of their next meal. From the vantage point of a female lizard positioned directly in front of it, the male’s bright colored shade of turquoise is still visible. This keeps the female interested in the male as the woodland creatures go about their mating ritual.

Depending on the viewpoint, Benjamin Graham’s value-investing criterion for the enterprising investor faces a similar dichotomy. From a bird’s-eye view, this stock-filtering criterion’s superior performance can at times be concealed from its true potential. One of the selection filters Graham advocated for enterprising investors is to purchase stocks trading below liquidation value. The calculation involves subtracting all liabilities and preferred stock from a company’s current assets. All of these data are readily available on a company’s balance sheet reported to the SEC on a quarterly basis. If the stock price is trading below this conservative measure of liquidation value, it can be purchased at a significant margin of safety. Intuitively, this strategy seems attractive, but there are times when Graham’s deep-value criterion will leave you wanting.

The chart below shows the best one-, five-, and 10-year holding periods of the S&P500 Index over the study period of 1950-2009. In those select time periods when the S&P500 shined oh so brightly, Graham’s criterion for enterprising investors had underperformed the broad market index.

* No more than ten percent was invested in any one stock trading below liquidation value, and all the stocks were held for exactly one year. If few stocks could be found, the balance remained idle in a money market fund.

During those euphoric time periods when the stock market was firing on all cylinders, Graham’s criterion for the enterprising investor not only underperformed the market but worsened as the holding period was extended. During the past 60 years, the best five-year holding period of an index fund had outperformed Graham’s value criterion by more than 5 percent. The best 10-year holding period for a stock index fund had clobbered Graham’s deep-value criterion by close to 8 percent. For individuals who have a bent toward value investing, those long stretches of disappointing results might challenge the patience of investors committed to Graham’s original teachings.

For holding periods where the broad stock market average is on a roll, an investor who pours more cash into a low-cost index fund recommended by his or her robo-advisor might feel invincible. Let’s change the viewing angle of Graham’s enterprising approach to value investing and see if things appear a little different. Sharing the same viewing angle with a female Iberian emerald lizard who is staring directly at her male counterpart sporting a fancy headdress might increase the attraction level for investors committed to value investing.

* No more than ten percent was invested in any one stock trading below liquidation value, and all the stocks were held for exactly one year. If few stocks could be found, the balance remained idle in a money market fund.

By only focusing on the best-performing holding period(s) of the S&P500, the superior long-term performance of purchasing stocks trading below liquidation value is concealed. If one takes into account all holding period(s) and not just ones where an index fund towers above the rest, the picture changes. Including dividend income and transaction fees in all of the calculations, the chart clearly shows that stocks trading below liquidation value had outperformed an index fund over the long haul. This value thesis holds true even if investors had to sit on the sidelines in some years, waiting patiently until more stocks could be found to meet Graham’s stringent stock selection criterion.

Beauty is in the eye of the beholder not only for Iberian emerald lizards but also for value investors. Seeing the merits of value investing requires a longer-term perspective, blocking out temporary distractions when an index fund holds a full dance card of pretty clients and lots of cash.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair