Personal Finance

We talk a lot about Warren Buffett around these parts (for good reason), but today, I’m going to share with you something a bit different:

We talk a lot about Warren Buffett around these parts (for good reason), but today, I’m going to share with you something a bit different:

Wisdom from a now-deceased investor from California you’ve likely never heard of … that was written three decades ago … and that originally appeared in a stunningly boring-sounding publication called The Journal of Portfolio Management.

Stay with me, though. It’s worth it!

Back to the future

At the time Robert G. Kirby published “The Coffee Can Portfolio,” he had already been in the money management industry for 30 years, most prominently in senior roles with the Capital Group, a Los Angeles-based institutional investor of many, many billions of dollars.

Even in 1984, well before computer-driven algorithms and high-frequency trading were the flavours of the day, Kirby, the wily veteran of the markets that he was, had found a flaw with how most money was being managed by institutional investors — aka “the pros.”

In a nutshell: transactions.

More specifically, Kirby found flaw in the number of transactionsmade by institutional money managers. All their transactions had a detrimental impact on their portfolio performance because of — you guessed it — the costs of every transaction.

These costs were (and still are) a significant performance drag, in Kirby’s estimation. He figured there had to be a better way.

Choice #1

One alternative Kirby identified was simply indexing a portfolio. His rationale here was that since it was

widely known that in aggregate most money managers couldn’t beat a broadly based, unmanaged portfolio, why bother?

Kirby pointed to two flaws in this approach: 1. Indexes too are, in reality, actively managed. 2. Does a widely followed index like the S&P/TSX Composite or the S&P 500 truly represent the market?

Though the number of changes an index makes over the course of a year is relatively small in comparison to a typical professionally managed portfolio, over time, they can add up. And as a result, so too can transaction costs and the accompanying drag they bring to your portfolio.

Also, the changes that occur in an index are not necessarily the result of a formula that produces a consistent, predictable kind of alteration. Human judgement is involved, which can open gaps to possible error between what the index represents and what the market actually is.

Though we acknowledge Kirby’s reservations with indexing, for many it truly does offer a perfectly viable investment strategy.

Choice #2

For those of us that believe the “market” is beatable, Kirby’s other alternative is deeply insightful, well thought out, and best of all, timeless. (In my opinion, at least!)

Kirby had for years been intrigued by the idea of the “Coffee Can Portfolio,” a strategy that harkens back to the Old West, when people put their valued possessions in a coffee can under their mattress. The can represented a no-cost way to hold valuables.

Kirby’s core idea: that investors treat their brokerage account like a coffee can. Inside the can would live a collection of the best companies around. Once a company’s stock was purchased, it was not to be touched for 10 years.

Each stock would be left to its own devices to grow and compound over that period of time. Some would, some wouldn’t — but in the end, Kirby theorized, those that succeeded would trounce the ones that flailed and the investor would be very nicely ahead.

The evidence

Kirby never did employ this methodology — the practicalities of the institutional money management industry were too daunting. And besides, the article provided no irrefutable proof that the Coffee Can Portfolio actually works.

But he did tell a story that demonstrated these coffee-can-like principles in action.

The firm at which Kirby once worked utilized a method of portfolio management that involved regular rebalancing. Winning stocks that were deemed “expensive” and had grown into large portfolio positions were sold, the proceeds recycled into less successful investments that had grown “cheaper.”

One day, a client called to indicate her husband had passed away; she was to transfer her deceased husband’s assets over to Kirby’s firm (where her money was already being managed).

When the list of assets was received, Kirby found that the husband had been piggybacking his wife’s account — following the same recommendations that she’d been receiving as a client of Kirby’s firm. But there was one major difference.

The value of his estate was vastly bigger than the value of her account.

Though the husband had been selecting the same stocks, he paid no attention to the advice to sell down the winners and put the money into the less successful companies in the mix.

He simply put $5,000 into every purchase recommendation, and he forgot about it.

A number of his holdings were valued below $2,000 — down significantly. Several were valued in excess of $100,000 … and there was one massive winner that was worth more than $800,000!

This single stock exceeded the value of his wife’s account — where it had likely been shaved continuously over the years and/or had been completely sold out of for much less than what the husband had gained.

Foolishly yours,

Iain Butler, CFA

Chief Investment Adviser | Motley Fool Canada

The BOJ used “shock and awe” on the markets last week…announcing a MASSIVE increase in their QE program…a program they hope will end 2 decades of deflation in Japan. The Japanese Government Pension Investment Fund (GPIF) added to the “shock and awe” by announcing that they would switch ~$250 Billion of their portfolio from bonds to stocks…thereby effectively “green-lighting” all major pension funds in Japan to dump bonds and buy stocks. On the announcements the Yen fell ~3.5% to 7 year lows, the major Japanese stock indices jumped ~8% to 7 year highs, and the major American stock indices soared to New All Time Highs. We think the BOJ/GPIF announcements may have been one of the most important financial events of the year…and may signal another leg higher in the US Dollar and in the major global stock indices. Money “printed” in Japan can and will find its way to markets around the world.

The BOJ’s new stimulus program is bigger, in relative terms, than anything previously done by any major central bank…they are “going all-in!” They will “print” the equivalent of ~$750B each year…given that the Japanese economy is about 1/3 the size of the US economy their level of stimulus is about double what the Fed was doing when they were running “full throttle.” The GPIF will reduce the bond portion of their portfolio (effectively selling their bonds to the BOJ) from ~60% to ~35% while expanding the equity portion of their portfolio from ~25% to ~50%. They are expected to buy ~$90B of Japanese stocks and ~$110B of non-Japanese stocks.

The BOJ’s surprise announcement came only a day after the Fed announced the end of their latest round of “money printing”…thereby adding to the market’s perception of DIVERGENT monetary policies between the USA and “the rest of the world.” This divergence plays out in favor of the US Dollar.

For several years we have believed that EXPECTATIONS of Central Bank policy have been the main “driver” of Market Psychology…at the margin nothing else mattered…buyers would be more aggressive than sellers so long as they believed that the CB’s “had their backs.” We think that last week’s BOJ/GPIF announcements will have a HUGE impact on Market Psychology going forward.

Over the past 2 years we have frequently posted charts of American stock indices with an uptrend line beginning in November 2012…the date the BOJ began their first (Abe inspired) wave of “money printing”…we believed that the BOJ actions since 2012 “underwrote” part of the rally in global stock markets…we can imagine that Phase 2 of the BOJ’s reflationary efforts will have a similar bullish impact on world stock markets…that the uptrend line will extend into the future…likely at a steeper angle.

Regular readers will notice a “change in our tune.” We have been opportunistic short sellers of the American stock market this year…we’ve been expecting a “topping process” that would produce price breaks and rallies…but not new highs. We thought that the September 19 highs might be the highs for 2014…if not longer…BUT… last week we specifically stated that IF the DJIA rallied past the 17006 level then the October break was probably another “Buy the Dip” opportunity and new All Time Highs would be likely. Well the DJIA went through 17006 like a “hot knife through butter” the day BEFORE the BOJ/GPIF announcements and closed the week at New All Time Highs. (We don’t even want to think about who might have known…)

We are traders here…first and foremost. When the markets change…we change. We trade our own money and we manage some money for friends and clients. We are very cautious about using leverage. We’ve had profitable trades and losing trades and we’ve certainly had trades that we didn’t make that we should have…witness our blunder in not re-establishing our short position in crude oil this summer…BUT…we constantly ask ourselves, “Are we trading the market the way we think it SHOULD be…or the way it is?” Right now the path of least resistance for the US stock market looks higher!

Because we can’t say it enough, we think the “Shock and Awe” from the BOJ/GPIF may have been one of the most important financial events of the year…we can imagine “Phase 2” of the BOJ reflationary efforts…this time with the “added punch” of the GPIF (and other Japanese pension funds that will likely follow suit)…will cause the Yen to fall…will cause the Dollar to rally…and will cause the global stock markets to rally.

The “mantra” at this blog throughout 2014 has been that capital is “Coming to America” for safety and opportunity. We can imagine a reprise of the virtuous circle of the late 1990’s when the US Dollar rose ~50% and the S+P rallied from 500 to 1500!

Three final thoughts:

The falling Yen is another aspect of “Currency Wars” and will export deflation from Japan to the rest of the world. The last thing the Eurozone needs at the moment is more deflation…therefore the BOJ action may inspire intensified reflationary efforts from the ECB…which would pressure the Euro lower Vs. the Dollar.

If these actions from the BOJ/GPIF do not end deflation and deflationary expectations in Japan…then what? A couple of years ago we wrote that the “Authorities” were only fighting a rear-guard action against deflation…maybe that’s how it will play out…maybe not…but it feels like we just stepped into a Brave New World and the stakes are way bigger than they were before.

If there is no real “follow-through” in the stock market after this VERY bullish news…well…we will revert to our skeptical attitude about the stock market…taking to heart the old adage that a market that can’t rally on VERY bullish news is in BIG trouble!

Chart section:

The major Japanese Stock Indices rallied ~8% (in a day!) to new 7 year highs on the BOJ/GPIF announcements…

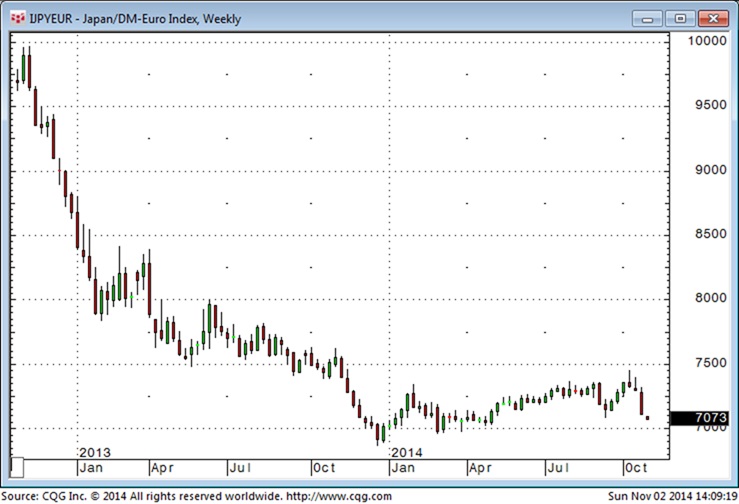

While the Yen fell~3.5% to 7 year lows against the US Dollar…

The Yen may be starting another leg down against the Euro…after falling ~30% since Phase One of the BOJ reflationary efforts started in late 2012.

The US Dollar rallied against nearly all currencies last week to close at new 4 year highs…for the past year and more we have believed that the US Dollar was beginning a multi-year rally as capital “Came To America.”

The S+P 500 benchmark of American stocks soared to New All Time Highs following the BOJ/GPIF announcements…and may be about to resume the uptrend it’s been on since Phase One of the BOJ reflationary efforts started in late 2012.

Gold: You might have expected gold to rally on the Japanese reflationary actions…BUT…it fell to 4 year lows…it seems that the King Dollar trumped any worries about “excessive money printing.” Perhaps the gold price action reflects the concern that inspired the Japanese Authorities to act…namely, that Deflation is gaining ground…despite all the efforts of all the king’s men….we should note that gold did rally in Yen terms on Friday….BUT…

Gold in terms of the S+P 500 fell to new 7 year lows…down ~60% since gold made its All Time High in 2011. For the last 3 years the market has clearly preferred stocks (paper) over gold. Central banks hate deflation and (apparently) will “print money like crazy” to fight deflation…the expectation of all that “printing” has been very bullish for stocks…but not for gold…perhaps someday it will be bullish for gold.

Today the Godfather of newsletter writers, 90-year old Richard Russell, shares what he has learned after 90 years on this earth. The 60-year market veteran also covered gold, silver, deflation, Europe, Germany, the Fed, QE, the U.S. dollar and much more…..continue reading HERE

Today the Godfather of newsletter writers, 90-year old Richard Russell, shares what he has learned after 90 years on this earth. The 60-year market veteran also covered gold, silver, deflation, Europe, Germany, the Fed, QE, the U.S. dollar and much more…..continue reading HERE

“In many ways, my grandfather and his generation enjoyed a much simpler world. First of all, he was raised before radio and TV became a right for all Canadians to have in their house. His generation truly did not know how the other half lived. He grew up in a depression and fought in WWII. Coming back home to raise a family, having a secure job for life, a roof, clothes and food on the table was a pretty good deal in his eyes.”

“In many ways, my grandfather and his generation enjoyed a much simpler world. First of all, he was raised before radio and TV became a right for all Canadians to have in their house. His generation truly did not know how the other half lived. He grew up in a depression and fought in WWII. Coming back home to raise a family, having a secure job for life, a roof, clothes and food on the table was a pretty good deal in his eyes.”

Why I can’t invest like my grandpa

I loved my grandfather. It was a special relationship, in part, because my paternal grandfather passed away before I was born. My mom’s father was part of that extraordinary generation that came through the depression, fought in WWII and built the nation we are lucky to live in. He wasn’t a rocket scientist, a doctor or a lawyer but he was 10 feet tall to me. As he liked to say, he was in the “transportation business”. He was a city bus driver for the TTC (Toronto Transit Commission).

I can remember as a little boy the day this big bus parked outside my house. It was the “Bellamy 9” (which was my grandfather’s old route) and his route ended close to our house. He drove it to our place when it was off service and I can remember my brother and a few neighbours getting to jump on the bus – while we got to sit in the driver’s seat and wear his TTC hat. Imagine, my grandfather was a bus driver and my friends thought he had the coolest job! My grandfather embodied what was so special about his generation. Everyone had a job to do and you did it. Many worked for the same company for their entire working life. On a bus driver’s salary, he raised 4 kids and Nanna took care of the house.

In 1985 I had just completed high school. I remember asking my grandpa why he didn’t go to university and never seemed to care that he spent his whole life working for the TTC. My generation was brought up if you didn’t go to university, somehow you’d be an epic failure in life. I was interested because my grandfather was smart, especially with math. I can remember how he could add, subtract, divide and multiply without paper or a calculator. It was amazing. I’d ask questions like 4 ¾ + 5 1/8 x 17 and boom, he’d have the answer. He did all this with a Grade 8 education.

I asked him – did he regret not going to university and only working as a bus driver? He told me he grew up in the Depression and his father came from a generation that valued “more earning and less learning” so when he finished Grade 8, if was off to work for him to find odd jobs until he joined the army in WWII. In the war he drove trucks, so when the war was over, he went to work as a bus driver to provide for his wife and young family. For him, there was less choice and when you had mouths to feed, that became your priority.

I admit that I’m a workaholic and lot of who I am is what I do. My grandpa was opposite, he believed work was something you did to survive and life was about living, not working. I supposed the day will come when I lie on my deathbed and decide who was right, but there was a big difference from his generation to my generation – and it’s affected how I work and why I work.

In many ways, my grandfather and his generation enjoyed a much simpler world. First of all, he was raised before radio and TV became a right for all Canadians to have in their house. His generation truly did not know how the other half lived. He grew up in a depression and fought in WWII. Coming back home to raise a family, having a secure job for life, a roof, clothes and food on the table was a pretty good deal in his eyes. Having a government job, he didn’t worry about losing his job in bad times because that meant more people would need to take a bus to get around. Maybe in his own way he figured out the importance of job security and the comfort of a steady job instead of worrying about the risk of working in the private sector.

I couldn’t be a bus driver. I have a university education. I grew up watching Lives of the Rich & Famous. But I also grew up in the troubled economic times of the late 70’s / early 80’s, an era that killed my father’s business. I had to watch my parents try to survive with 5 kids in tow. As a teenager I witnessed the social contract between employee and employer break when millions were laid off and job security in the private sector vanished along with pensions. A situation I saw repeated as an adult in 2008. Which is why I can’t be like my grandfather. I’ve been exposed to things he never saw – as I was never exposed to what he saw.

When it came to investing grandpa’s strategy was simple; he’d have a pension for life and he invested in blue chip stock. The stuff you bought and forgot. He bought stocks like GM, Nortel and Bell. Blue chip stocks that paid dividends and went up every year. If he were alive today, what would he think of Bell divided, GM bankrupt and Nortel gone? This was something that was considered impossible in the 70’s. Greater interdependence and emerging economies make North American and European behemoths increasingly vulnerable to market change.

At TriView, we focus primarily on real estate in strong economies like Alberta, Texas and Arizona. We see opportunity in residential, commercial, retail and industrial but investing in specific sectors and specific locations takes experience and local knowledge.

It’s an area where stock brokers and mutual fund reps can’t help you diversify your portfolio. At this time, traditional investment in stock markets can be risky given the market cycle and volatility we’ve seen over the past few weeks. Given the potential of inflation, bonds may be risky as well. In fact, I was at a Family Office conference a couple of weeks ago in Vancouver and noticed many of them are putting large reserves in cash mainly due to their fear of the stock and bond markets. A natural hedge to inflation and volatility is hard assets like real estate or gold.

Over the next few weeks, we’ll be providing information on why we like real estate and what areas we specifically like. We’ll go even further and discuss what particular sector and what region we believe will be a good investment as well as a natural hedge against inflation. If you want to learn more sooner than later, please visit us at www.triviewcapital.com or contact us toll free at 1-855-984-6570.

Craig Burrows

President & CEO

TriView Capital Ltd.

You’re 65—Now What? Unlike Jack Nicholson’s character in A Few Good Men, we trust that you can handle the truth. No matter your age, securing a comfortable retirement is a huge concern. Folks want the whole truth about their financial outlook, but straight answers are hard to come by.

Both sides of the mainstream media habitually present opinion-tainted partial facts. Case in point: the unemployment numbers announced earlier this month. One side is cheering because unemployment dropped to a six-year low, while the other side is calling it pure fraud.

I found author and libertarian-about-town Wayne Root’s remarks in a recent article for The Blazeparticularly telling:

The middle class isn’t getting richer, it’s getting poorer…

The only people being hired are your grandparents. 230,000 of the new jobs went to those in the 55-to-69-year-old age group. In the prime working age group of 24 to 54 years old, 10,000 jobs were lost…

It means grandma and grandpa are desperate and willing to take grandson’s low wage job to survive until Social Security kicks in. The US workforce is now the oldest in history. And if grandpa has to work (out of desperation) until the day he dies, there will never be any decent jobs for the grandkids.

Here’s the part Root gets wrong: Baby boomers are not working until Social Security kicks in. They’re working well past that point, because they feel they must. Smart boomers know they can’t afford to wait until robust interest rates return; they’re taking action to protect themselves now, lest their circumstances become truly dire.

You’re 65—Now What?

The Employee Benefit Research Institute surveys workers each year concerning their retirement confidence. Despite an uptrend, the latest report shows that 82% of workers feel less than “very confident” about having enough money to retire comfortably.

With that statistic in mind, we looked at three different 40-year retirement scenarios. Note that the numbers and charts in this overview are meant to illustrate several scenarios, not provide individual guidance. Every person’s situation differs in terms of taxes, time horizons, and other parameters, and we encourage you to work with a financial planner to manage your savings.

The data exclude other sources of retirement income you may have, such as Social Security or a pension. All of the amounts, including annuity incomes, are pre-tax.

- Scenario 1. At age 65, you decide to retire with $500,000 in personal savings. You anticipate your expenses will rise approximately 3% annually. Thus, with each subsequent year, you will need to withdraw 3% more than the previous year. You estimate that your savings will grow by 5% annually. You are planning for a 40-year retirement, meaning your savings must last until age 105.

How much money can you withdraw each year, using those assumptions?

- Scenario 2. At age 65 you have the same $500,000 in personal savings that you did in Scenario 1; however, you take $100,000 from your account and buy an annuity. Our go-to source for annuity information, Stan The Annuity Man, says that currently, this annuity would pay $527 for the rest of your life. You use the remaining $400,000 as principal for the next 40 years in the same fashion as in the first case: assuming the same 5% rate of return and an annual 3% withdrawal increase.

- Scenario 3. Instead of retiring at age 65, you work for five extra years and buy a 100,000 annuity at age 70. We will assume you did not add to your savings during that time (though it did earn interest). Many boomers use extra working years to eliminate any lingering debt, so they can retire 100% debt-free. (However, note that we encourage a different approach: using extra working years to save as much as possible, including maximizing catch-up contributions to your 401(k) or IRA.)

If your nest egg grew at a 5% compound rate, it will total $638,141 when you are age 70. So, excluding the $100,000 spent on an annuity, you have $538,141 to draw from. As with Scenarios 1 and 2, we’ll assume the withdrawals last for 40 years here, stretching the retirement period until age 110. Buying the annuity at age 70 instead of age 65 raises your monthly annuity payout to $582 per month.

Now, let’s take a closer look at each of these cases.

Scenario 1: He Who Takes It All Is Not the Winner

For your nest egg to last 40 years, in year one, you can withdraw $17,747, or $1,479 per month, from your $500,000 nest egg. Each year you take out 3% more to keep up with rising expenses.

Follow the yellow line representing your nest egg in the chart above. As you can see, after 40 years your $500,000 is gone.

What happens if you stay within your monthly allowance and live past age 105? Here’s hoping you have generous grandchildren. If not, you might be at the mercy of a Social Security system that may or may not be around in its current form.

There’s good reason the Bureau of Labor Statistics projects that workforce participation for people age 75 and over will rise to 10.5% by 2022, up from 7.6% in 2012. For the 65-74 age group, it projects that the rate will jump to 31.9%, up from 26.8% in 2012 and 20.4% in 2002. Better health and a sustained desire to work may be one reason more seniors are working longer, but another is fear.

61% of older Americans fear outliving their money more than they fear death. This is a fear we hope no one encounters as they near the end of the line. Other than the late George Burns, I doubt many centenarians are holding down a job.

Running out of money and having Social Security as your final safety net is a legitimate concern. Every politician, regardless of party, acknowledges the US government cannot make good on all of its promises. No one knows what the future will bring.

With that in mind, let’s move on to Scenario 2.

Scenario 2: Spreading Out Risk

Insurance companies have a range of annuities that will pay you for the rest of your life, which our team covered in detail in Annuities De-Mystified. In essence, holding an annuity as part of your overall retirement plan is one way to reduce the risk of running out of money. Since going back to work at 105 is both unappealing and impractical, let’s look at how Scenario 2—the same $500,000 nest egg with $100,000 used to purchase an annuity at age 65—plays out.

Your annuity will provide monthly payouts of $527. Using the same 40-year time frame, your monthly income from the remaining $400,000 will be approximately $1,183 per month in first year, or a total of $1,710.

You start out with a bit more money; however, the annuity payment will remain constant, with no adjustment for inflation. At the end of 40 years, your nest egg will be gone, but you will still receive the annuity payments.

There is no way to know how long you will live. Today, a man who reaches age 65 can expect, on average, to live to age 84.3; a woman, 86.6. One in ten 65-year-olds, however, can expect to live past age 95. Medical advancements are pushing those numbers up, making life after age 105 seem not too far fetched. An annuity is just one way to hedge against running out of money too soon.

One big disadvantage of an annuity is that it doesn’t offer real inflation protection. Even annuities with inflation riders usually yield marginal results.

If you receive Social Security, you can hope the annual inflation adjustments make up some of the difference, but it’s unlikely to be enough to maintain your current lifestyle. That brings us to Scenario 3.

Scenario 3: Delayed Gratification

Congratulations! You made it to age 70. The $500,000 in savings you had at age 65 has grown to $638,141 (at an annual rate of 5%). You buy an annuity for $100,000 that will pay you $582 every month until death and draw down the remaining $538,141 over the next 40 years—again assuming 5% growth rate and 3% annual withdrawal increase.

The lump sum of $538,141 will provide approximately $1,592 per month during the first year. Add the annuity payouts and your total monthly income comes to $2,174, before taxes.

In the first year, your total income, including withdrawals and annuity income, will be $26,085 compared to $17,747 in Scenario 1 and $20,516 in Scenario 2.

And although your savings will still run out after 40 years, you will be 110. By working an additional 5 years and deferring the start date you get an additional five years before you have to rely on the annuity only.

The Takeaways

This is all a reminder that the best way to enjoy retirement is to build a portfolio that can generate enough capital gains and dividend income to satisfy your spending needs, while leaving the principal intact as long as possible. If you want to end up in the 18% of people who are very confident about having enough money to retire, you may want to keep working after age 65, if possible, and investpart of your savings in an annuity to ensure you have at least some income if you outlive the rest of your nest egg.

To determine if an annuity is right for your retirement portfolio, read your free copy of our special report, Annuities De-Mystified. It includes tips for uncovering hidden fees and a frank look at the risks associated with annuities. Plus, it’s the only such report we know of written by financial educators who do not sell annuities. Access your free copy of Annuities De-Mystified here.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair