Personal Finance

In all my years in the market, I’ve never heard of such an incredible track record.

In all my years in the market, I’ve never heard of such an incredible track record.

The IPO prospectus from high-frequency trading firm Virtu Financial reveals that in the past four years, the company has lost money in exactly one of 1,238 trading sessions.

J.P. Morgan didn’t have a single losing day in 2013. Bank of America notched a perfect performance of its own in the first quarter of 2013.

Clearly, Wall Street trades and invests its own money a lot differently than the “buy and hold” strategy it preaches to its clients.

One of the best-kept secrets they use is selling options.

Does that sound scary? Intimidating?

If it does, there’s a very good reason for that: That’s exactly how Wall Street wants it.

Wall Street works very hard to keep one of its most powerful income strategies out of the hands of regular investors.

Because what most investors don’t realize is that selling puts isn’t just one of the most conservative options strategies… it’s one of the lowest-risk investment strategies in the entire market — more conservative than owning individual stocks and bonds or even mutual funds and ETFs.

The conservative strategy of selling options is driven by a fact you might find shocking: About 80% of options expire worthless. That means whoever sold those options gets to keep the full premium collected as income from their sale 4 out of 5 times.

And these aren’t small premiums. They’re annualized yields of 36%… 47%…. even 87% from well-known, trusted companies like Microsoft (Nasdaq: MSFT) and Verizon (NYSE: VZ).

Despite Wall Street’s best efforts, well-informed investors are embracing selling options as an important source of portfolio income. In fact, this is what we do every week in my premium newsletter service, Income Multiplier.

But deciding to sell options is only half the battle. Learning how insiders increase their returns and win ratios is the other. That’s why I’m sharing these 5 insider tips that provide a basic framework for understanding how Wall Street insiders increase the probability of winning trades.

1. Only sell options on stocks you want to own.

Selling a put offers two potential outcomes.

The first is that the options expire worthless and the put seller keeps the entire premium generated from the sale. This is a powerful income strategy and the most desirable outcome when selling an option because we keep this premium as pure profit.

The second potential outcome is that shares of the underlying stock fall below the strike price on the date the option expires. This obligates the put seller to take ownership of the shares.

Although that’s a low-probability outcome, it’s the reason why it’s so important to sell options only on stocks you actually want to own. In the event that the put seller is put shares, you want to own a great company with plenty of long-term potential that will quickly rebound from a temporary pullback.

2. Avoid long-dated expirations.

All options contracts have an expiration date. Some options expire every week; other options expire after several years. Options that are dated far into the future have a higher premium value because a longer time allows significant price swings or unexpected events to occur. That could be a macroeconomic event (like a recession) or a company-specific event, such as earnings falling short of expectations.

Conversely, options that expire in just a few weeks or a month are much less susceptible to price fluctuations. Think of this like a baseball player hitting a bunch of singles and doubles as opposed to an occasional home run with lots of strikeouts.

3. Sell puts more than 5% out of the money.

Every options contract carries a probability of expiring worthless. Some options contracts have a 90% probability of expiring worthless; others have a 50% probability. It all depends on the variables of each individual contract.

One of the biggest factors impacting the probability of a worthless expiration is an option’s strike price. Options with strike prices that are far away from the underlying stock’s current share price have a lower probability of assignment than those with strike prices that are close to current prices.

Selling puts with strike prices more than 5% away from the current share price greatly increases the chances that the puts you sell will expire worthless.

4. Diversify.

Regular stock investors should always diversify their portfolios. Holding stocks from different sectors and regions of the world is a great way to reduce volatility and short-term price risk. Stocks from different sectors and industries tend to have a lower correlation with each other.

That same concept of diversification holds true for selling options. As an options seller, it’s important to avoid highly concentrated positions in sectors, stocks or themes with a high correlation. This reduces the probability of one single event triggering assignments on multiple open put positions.

5. Don’t increase the size of positions too quickly.

This is the No. 1 mistake made by new options traders. It’s also a familiar theme across any asset class. A novice investor experiences great results early in the game with a new investment strategy. Gaining confidence, the investor begins to quickly ramp up the size of their position, increasing risk significantly. When the size of the investor’s trades has grown out of proportion to the value of the account, one small miscue can have serious implications.

This is a recipe for disaster. The value of any individual put-selling position should be calculated as a percentage of overall account value. That makes actual results and the growth of an account the primary drivers of position size as opposed to a bout of short-term confidence driven by a bull market.

The unprecedented track records that Wall Street trading firms are racking up are due in large part to successful strategies like these.

But I think it’s time that regular investors got in on the wealth-building opportunities that these traders are so set on hiding from the public.

In my premium newsletter Income Multiplier, I’m showing readers my research each and every time I sell a put option, and we’re seeing annual yields on our trades that make regular dividends look meager by comparison. As I mentioned earlier, we’re talking 36%… 47%… even 87%. To learn more about how easy it can be to multiply your income, I’d like to invite you to watch a special presentation I’ve prepared. Simply follow this link to learn more.

Good investing,

Michael Vodicka

Chief Investment Strategist

Income Multiplier

Most investors get what they deserve, too…

In trying to beat the market, they end up underperforming it.

The reality is that most investors don’t have a clue what they’re doing. They’d be better off putting their money in a low-cost index tracking ETF and going to sleep for 20 years.

But that’s not the way human nature works. Everyone wants not just what the market gives them (beta), but also some extra helpings of returns (alpha).

The compulsion to seek alpha, and the below par results this often leads to, is writ large in the chart below from The Vanguard Group. It shows the median performance of stock funds versus their style benchmark over 36 months following a Morningstar rating.

The conclusion is clear: By chasing “hot” funds, investors underperform their benchmarks. A better strategy, based on the data set analyzed above, would be to buy the least popular funds.

As top fund manager Howard Marks wrote recently in Barron’s, “The road to above average performance runs through unconventional, uncomfortable investing.”

Our advice: Either take what the market gives you. Or choose the unconventional and uncomfortable path.

Trying to beat the market by following the crowd is a mug’s game.

As part of our research to unveil the best tactics and strategies to protect against the upcoming tsunami in monetary and financial markets, we have reached out to Charles Savoie, author and researcher, with a tremendous knowledge of precious metals history. Our question was how individuals and small investors can best protect during the hard times that are coming, which will most likely be characterized as turmoil and collapses (of all sorts of assets, including currencies, around the world).

As part of our research to unveil the best tactics and strategies to protect against the upcoming tsunami in monetary and financial markets, we have reached out to Charles Savoie, author and researcher, with a tremendous knowledge of precious metals history. Our question was how individuals and small investors can best protect during the hard times that are coming, which will most likely be characterized as turmoil and collapses (of all sorts of assets, including currencies, around the world).

Charles Savoie wrote a very useful document for our readers. It is entitled “The Best Monetary Insurance”, counts 38 pages, and is a mix of practical tips embedded in an historical context. The key message of Mr. Savoie is to hold enough silver in physical form, ideally a mix of formats, but for sure silver dimes.

In this article, we highlight the most actionable tips and tactics. The full document is embedded at the bottom, it can also be downloaded.

Visit Mr. Savoie his two websites: www.nosilvernationalization.org and www.silverstealers.net. He offers all this information as a free service to the public.

Silver has historically played an important role. It has been money, but, more than anything else, a metal of the elites. Consider this:

U.S. Congress knew silver to be more valuable in regard to gold than the present bullion banking fiends. And Congress knew it nine generations ago! For details, see Senate document number 67 of the first session of the 73rd Congress, “Elementary Facts Bearing On The Silver Question” by Joel F. Vaile” (50 page document, 1896). Today the reality ratio of silver to gold may have fallen to 9, due to depletion of minable silver (The U.S. Geological Survey concurs) and even more so, the evanescence of above surface inventories. Ratios of silver to gold such as the approximate 64 to 1 of late March 2014 are illusory. But the real impact is that silver is a better buy than gold.

The best monetary insurance you can have is 90% silver dimes 1964 and earlier. Many gold bugs readily admit silver to be more depressed than gold. Ted Butler stated long ago that not even gold has a users association. The fact of the existence of this group is another of many proofs that synthetic money creators hate and fear silver even more than their loathing for gold. The Silver Users Association started out as the Silver Users Emergency Committee in World War II and in 1947 was renamed the Silver Users Association. Directors of SUA companies, especially the biggest silver users, are also since that time, directors of megabanks. 90% U.S. coins, historic money, facilitated many billions of transactions during their long history spanning many generations. Inasmuch as silver is so depressed relative to gold, personally, I advocate owning little or no gold; unless the investor cannot acquire silver. This is not disdain for gold, but more so, advocacy for acquiring the interest with higher potential. Silver can be swapped for gold at a later time if the ratio tilts to overvalue silver versus gold. Why buy 1 ounce of gold today versus 60+ silver ounces, when you may be able later on to swap those 60 + silver ounces for over 5 gold ounces?

A silver dime at the mints started out with a content of .0723 oz silver (4 digits is enough!) Due to average circulated wear, the business typically uses the figure of .0715 ounce contained silver. You will be able to tell the difference from a dime with no wear and a dime with light wear and more so, a heavily worn dime. I feel that very worn dimes are better melted, except for collectors seeking an inexpensive “cull” or “filler” coin for a key date and mint mark. When you buy dimes, you’re unlikely to get any with 89.24% silver, which were minted from 1796 to 1837. The clear advantage of Mercury dimes over Roosevelt is guaranteed identification of purity with no check of the date nor glance at the rim to look for telltale copper insides. Silver coins have a surprisingly large variation in surface tone, and you can’t always rely on telling the surface tone of a cupronickel (sandwich dime, 1965 and later) from a silver dime. Of course, proof silver dimes (1992-2009) can be found in dates beyond the fabled 1964 date. These are good buys generally only if you chance to come by some in a batch of mixed date dimes, in which case, they won’t be proof anymore, but will very likely stand way out due to newness and absence of wear.

I am not saying buy silver dimes, and no other silver. I have all types except the 1,000 ounce ingots, which you can anticipate having to have assayed if you have these and decide to sell. Unless you’re a larger investor and have intentions of using metal to buy land, stick with smaller units. Having smaller units wouldn’t preclude their use in buying land; smaller units are more “maneuverable” as to utility in purchases.

If dimes aren’t available, try for quarters. It mostly comes down to two considerations. One, the 90% coins haven’t been minted now for an entire half century—they get scarcer by the day, as some of these are always being smelted into bullion with silver scrap at refineries, and being melted in jewelers crucibles with some three-niner, in a proportion to yield .925 Sterling jewelry and Two, the silver dime is the most divisible, or the most fractionated, form of silver. You can go buy a 100 ounce silver bar. However, you can instead go for the same amount of silver, approximately, in 90% dimes. This equates to almost exactly 1,400 dimes (28 rolls of 50 coins) at the .0715 figure. In most cases, dealers have allowed me to cherry pick the dimes I wanted and the methodology I used was as follows.

Tip: Avoid damaged coins

Never buy coins with damage such as hole drilled, bent, clipped, etched (vandalized) or shaved rims. There’s the inevitable coin with red nail polish, best avoided. While date and mint mark checking is usually only practical in over the counter situations, and is unlikely to turn up anything of outstanding scarcity, it could help you in terms of being able to assemble some starter sets for sale to numismatic collectors. So while you aren’t paying numismatic prices, you will be getting some numismatic values, as long as people want to collect coin series as a hobby or business. It pays to print out a list of these mint issues and be familiar with them

Tip: Avoid high premiums

You can buy .999 silver as half, quarter, and tenth of an ounce rounds. There is nothing wrong with these items. However, know two things—the collectible value will remain less, and when you buy 90% coin, you aren’t paying for any manufacturing or minting premium. You will pay such premiums with the smaller three-niners. Seven dimes in nearly all cases can be considered a touch more than a half ounce of silver; and 14 dimes a full ounce. In terms of how much silver is out there as separate items each weighing less than one ounce, definitely at this time, there is more 90% coin than these newer bullion items.

If your silver consists entirely of three and four-niner bullion—stop! Buy some dimes, or trade bullion for some dimes. These 90% coins—in all denominations—are increasingly hard to source. More investors have caught on that whereas these coins are a half century and older, and the supply is constantly shrinking; bullion silver will be produced as long as mining and scrap can supply silver. The 90% silver, though not industrially pure as is, is nonetheless the scarcer form of silver. If buying on E-Bay, do avoid dealers with less than very high positive feedback. Be fairly quiet about your holdings—no boasting to anyone. Keep these precious items in several scattered, and unpredictable—locations. If a thief finds one cache, hopefully the others will be missed.

Tip: Where and how to store your bullion

If you don’t have a vault or safe, and plan to obtain one, you may consider paying cash, for clear reasons you can imagine yourself. If it needs to be delivered and installed, arrange to have someone photograph the delivery personnel and the vehicle, from several views. When my vaults were delivered to an off-site location I have, I remarked as they were finishing, “Now if I only had something worthwhile to store in them;” I then indicated I expected to inherit an antique gun collection in several years. It never hurts to be careful. Read “The Art Of War” by Sun-Tzu. Many major military blunders, costing so many lives. As always, check ratings first, and buy from the source with the best ratings.

There’s always the steel vault and loaded gun approach—which are quite reasonable. I advise going on EBay and buying some cheap synthetic rubies. Then, you make up a phony gemological appraisal showing a stone is worth lots of money. Next, you place these in a jewelry box (unlocked) on top of a dresser. A thief would think he’s got a real haul, and maybe decide to stop searching. I suggest printing out articles making fun of silver as investment, and leaving these where you think it might mislead someone. If you use a keypad operated vault, consider acquiring a battery recharger and the http://www.ebay.com/bhp/solar in case the power grid fails and the stores close. If you find your battery operated keypad fails due to battery exhaustion, this device will solve the problem of accessing your money metal. Be sure you’re using compatible batteries in the first place; they must be a size that matches the recharger, and must be rechargeable batteries. Keep backup batteries in a climate controlled environment where they’ll last longer. Cover any vault/safe with a tarp or other use of drapery, such as a decorative item—even a Mexican style multicolored serape http://www.ebay.com/bhp/mex or even plain canvas. Whenever possible, place any type of objects of low value on top, around and in front of the safe.

Tip: Check what you are buying

Never buy a bag, half bag, quarter bag or tenth of an ounce bag in a shop without first having it opened up and spread out, unless you have a long trust relationship with the dealer. Paper rolls, more than plastic tube rolls, should be checked. You aren’t accusing the dealer of dishonesty, you are verifying contents, because errors can happen on anyone’s part. Eventually, due to real variations in silver weight in bags, these will have to be sold by actual weight rather than by face value times a factor! Check ratings of Internet sellers before buying. Many unfortunates out there are stressed out due to the Tulving fiasco. I consider the 40% Kennedy halves (1965-1970) a poor choice as long as 90% is available. The war nickel series, 1942-1945, contains even less silver, at 35% but is a better buy, weight for weight, if similar rates for contained silver are offered. Those nickels are more historic.

In closing, Charles Savoie says: “The suppression of the silver price is the most nagging and pestilential problem in world monetary history.”

To read the entire 38 page report from Charles Savoie go HERE (scroll down)

Also from GoldSilverWorlds

10 Questions About Gold Investing In 2014

Stay Hedged with Precious Metals against Geopolitical Tensions and Monetary Policies

Is It Imaginable That Governments Would Confiscate Your Bank Account?

Dow down 159 on Friday. Gold up $18 an ounce.

Remember, it’s just a matter of time until US stocks begin to fall. How much time? Darned if we know!

We spent Friday cosechando (harvesting). We were on our knees going through the vineyard at the family ranch, harvesting grapes. The going rate for such work is 5.70 Argentine pesos (or about $0.70) per gamela – the plastic bin we dragged along after us.

This was the first time we had ever worked as a grape picker. Experienced, hardy pickers can fill 40 gamelas a day, giving them about 230 pesos (or about $28) for the day’s work. Your editor worked at fast as he could. Still, he was only able to pick at the rate of nine gamelas a day. That gave him an income for the day of 51.30 pesos… or about $6.40.

The sun beat down. The grapes hid behind leaves and clung to vines, making it hard to cut them off. Our knees found every rock in the field. Still, we were proud to be doing honest work… and happy to earn some extra money.

Now, let us turn back to last week’s subject.

You’ll recall that the credit bubble must continue to expand. Or else all Hell will break loose. Civilization probably won’t be able to survive a real credit deflation, economist and author Richard Duncan believes. With visions of chaos, depression and war in his head, he advocates policies that give the bubble more air.

We live in a credit-driven economy. The money supply relies on banks creating new credit. Credit must expand… or the economy shrinks. It can’t stand still because the current level of jobs and incomes depends on additional debt.

Last year, for example, through its QE program the Fed created $1 trillion of new bank deposits (offsetting them with $1 trillion in new bank reserves). And the economy grew just 1.9% – or by only about $320 billion. Think what would have happened without this boost!

But for credit to really expand without the help of QE, banks must find willing and able borrowers. And who will those willing and able borrowers be?

Not consumers. They don’t have the disposable incomes to support much additional borrowing.

And not corporations. Their earnings are beginning to turn down, too. The days of borrowing money in order to goose up their own stocks (and, not coincidentally, get management bigger bonuses) must be nearing an end.

Who does that leave? Government. Government is the only large entity with the ability (in theory at least) to borrow an infinite amount of money. Because it doesn’t have to worry about paying it back. It’s the only institution with the legal right to counterfeit its own money… and use this cash to pay its own debts.

What a sweet deal!

Duncan reckons that the US can, will and should follow the example given it by the Japanese.

Although the US has debt equal to about 100% of GDP, Japan’s government debt is about 240% of GDP. By that measure the US could borrow another $17 trillion – enough to keep the credit bubble and the economy expanding for many years.

You see, dear reader, we live in a world of wonders. One of them is that we have an economy that now lives, and apparently thrives, on air.

Each year, households, government and corporations spend their revenues…. and then some. This extra spending would normally come from savings. Instead, it comes out of thin air – conjured up by the Fed and the banking system.

Now, imagine that the air were cut off. You can see what a disaster it would be. Everyone would be gasping for cash… for credit… for a last breath.

What’s the solution? Keep the credit flowing!

That is what the Japanese did following their stock and property market crash in 1990. And it’s what they’ve been doing ever since. They were faced with the same challenge – the household sector could no longer be persuaded to borrow… and the corporate sector could no longer afford to.

So, the government stepped in as the borrower and big spender of last resort… allowing the Japanese government to run up record amounts of debt relative to the size of its economy.

But wait… With the government borrowing and spending so freely, didn’t prices go up? Didn’t inflation discourage people from lending to the government?

Nope. Prices were stable or actually fell. For two reasons. Because everyone else was paying down debt and reluctant to spend at all. And because wage competition from nearby China was substantially lowering the cost of consumer items.

So, with no threat from consumer price inflation, the government just kept borrowing and spending. This has held the Japanese economy together for 24 years. Many economists look at the Japanese example as a success story.

But the final chapter on that story still hasn’t been written. We will take a guess at how it turns out: badly.

Regards,

Bill

Editor’s Note: Our new analyst, Braden Copeland, has put together a special report on what to do when the “thin air” economy finally falls apart. Learn about the three important steps you need to take to protect your wealth before, during and after the coming crisis by following this link.

Market Insight:

A BIG Headwind for

Stocks Right Now

From the desk of Chris Hunter, Editor-in-Chief, Bonner & Partners

Nobody knows for how long US stocks can continue to rally…

But a BIG headwind for the US stock market is overstretched valuations.

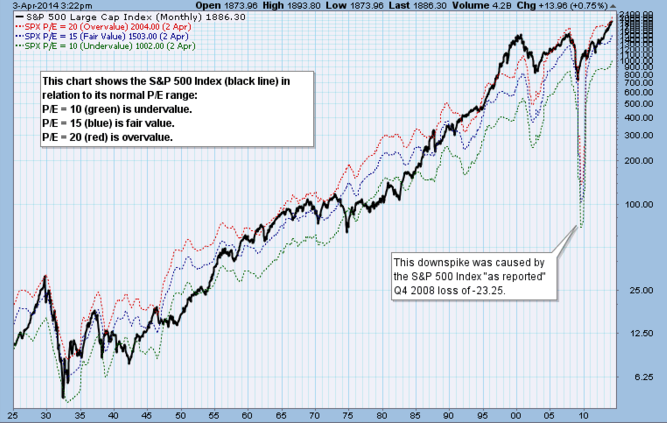

There are different ways to value stocks. But one of the most straightforward is to look at their price relative to their 12-month “as reported” earnings. (What’s also known as a “trailing P/E.”)

As you can see from the chart below from StockCharts.com, the normal range for the trailing P/E for the S&P 500 going back to the 1930s is between 10 (green line) and 20 (red line)… with an average trailing P/E of 15.5.

And as you can see, the index is now at the top of its normal range.

Overstretched valuations like this don’t necessarily cause a crash. But they will make investors think twice about going long the S&P 500… and encourage more investors to take up short positions.

Meanwhile, the Wall Street consensus for earnings growth for Q1 has gone from 4.4% year over year in early January to -0.4% today.

If prices don’t fall, a drop in earnings will push up P/Es even higher… and create an even bigger headwind for US stocks.

P.S. Don’t forget to check out Braden’s new report on what to do to prepare for a crash in the US stocks. It contains a list of six stocks to buy when the next crash comes. Find full details here.

As I pen this column, gold and silver continue to build a base. That base will strengthen dramatically as long as gold holds the $1,278 level on a weekly closing basis, and silver holds its June 2013 low at $18.18, also on a weekly closing basis.

Meanwhile, the euro appears ready to crack, and deflation still has the upper hand in an assortment of commodities — ranging from oil to wheat, and soon to follow, soybeans, which could be about to fall very hard.

Also, keep your eyes on the U.S. equity market: If the Dow can give us a weekly close above 16,650, it could be headed for 18,000-19,000. If not, I still think a sharp market pullback is in order, especially in Europe.

That’s the near term. But now, let’s turn to the Big Picture. I am often asked …

“Larry, what can we do to prevent our country

from continuing to slide down a slippery slope?”

(while concentrated on the US, a lot of this applies to Canadians – Editor Money Talks)

“What can we do to get our country out of debt? What can we do to rebuild America? What are your ideas?”

I have ten proposed ideas, all of them controversial, too. And all of them difficult to execute, to be sure.

But in my opinion, in order to get our country back on track, at a minimum, we MUST get started on the following:

FIRST, and foremost, aim to pay off our foreign creditors. 100 percent on the dollar. Stop the bleeding interest payments and become 100 percent invulnerable to foreign financial threats.

SECOND, aim to ultimately pay off domestic creditors to the U.S. government as well. There isn’t enough money to do so. But, there are assets and equity.

How will that ever be possible? Here’s an idea: Offer domestic creditors a second, alternative choice: A swap of their domestic U.S. debt for equity in a newly established, not-for-profit federal government. Make the equity transparent and liquid and tradable on an established exchange, but only by U.S. citizens.

That would be radical and far off, of course. But a first step in that process is not: Just move step by step to privatize as much of the federal government as possible to free up cash, to stop cronyism, and to get rid of a bloated, wasteful government.

THIRD, aim to abolish the tax code. Replace it with a consumption tax, with the only exempt items being food and clothing. By getting rid of the current tax code, we also get rid of politicians’ non-stop efforts to play God and socially engineer society.

FOURTH, move toward maximum term limits for all members of Congress. For example, they could serve one 3-year term, and that’s it. Also enact term limits for federal, state and local judges.

FIFTH, take steps to privatize Social Security and Medicare. Most fears about privatizing Social Security and Medicare are unfounded. Consider Chile and other countries that have very successfully privatized national retirement and health programs.

SIXTH, abolish Obamacare. Also bust the informal union of malpractice, ambulance-chasing lawyers.

SEVENTH, put all votes on ALL major federal and local bills and laws to the public via referendums. No more coming up with insane laws and burying them in some larger bill so they get passed without the public having any clue what’s going on whatsoever.

Consider the FACTA foreign reporting of American overseas bank accounts and how that was slipped into Obama’s 2010 Hiring Incentives to Restore Employment Act … how that is now causing banks all over the world to stop doing business with Americans.

EIGHTH, stop all spying on domestic U.S. citizens, unless a legitimate search warrant has been issued.

NINTH, scale back the police state that we now have.

NINTH, scale back the police state that we now have.

Just consider how the esteemed Economist describes the American paramilitary force, where SWAT teams are now used around 50,000 times a year, compared to 3,000 times in 1980.

Or consider the small town of Keene, New Hampshire, which spent $286,000 on an armored personnel-carrier known as a BearCat — to patrol Keene’s annual “Pumpkin Festival.”

TENTH, open up the spigots on our new energy independence and become an energy exporter.

And more, including deregulating small business, which is 70 percent of our economy and the home of American entrepreneurship.

Difficult to do? Absolutely. Controversial? You can bet on it. But these kinds of steps will put us on the right track — back to the great Constitution our forefathers drew up that made America a great nation. That gave us liberty and the pursuit of happiness, for all.

It’s time for change. You know it. I know it. So does the rest of the world.

Best wishes,

Larry

More from Swing Trading: A Very Bad Chart Day

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair