Personal Finance

For many, it’s the forgotten variable in accumulating wealth…

For many, it’s the forgotten variable in accumulating wealth…

A good blue-chip stock can bring you thousands of dollars in dividend income every month.

But if you’re blowing money on things you don’t need, you’ll never build substantial wealth… no matter how well your investments are performing.

When it comes to watching your spending, it’s best to focus on big-ticket items like homes, vacations, and furniture. You can also make the mistake of spending unwisely on cars.

Below are two of the costliest mistakes you’ll ever make on your car…

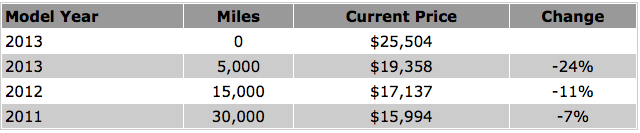

Most people have heard that when you buy a new car, it loses a big chunk of value as soon as you drive it off the lot… But how much?

We ran a quick test using my favorite American car – the Ford Taurus. According to the Kelley Blue Book independent vehicle-valuation service, you can still buy a new 2013 Taurus for $25,504.

The “fair price” for a used 2013 Taurus in excellent condition: $19,358. The car drops in value by 24% that first year. Is it worth an extra $6,000 just to be the first to drive this car? Not to me.

You can see how big your savings are going to be from new to used when you look at a few more years in this table below. The table shows the current prices on the following model years and mileages, according to the Kelley Blue Book.

Don’t ever pay extra for the “new-car premium.” The savings of $8,000 every six or seven years over a few decades of car driving adds up to nearly $100,000 extra money in retirement.

The dividends from investing that money over time could allow you to drive a brand-new car and do other things with the extra money in your retirement. But spend it early, and you’re broke in your later years…

Many rental-car companies will pressure you to accept their insurance when you pick up one of their cars… Don’t fall for the hard sell.

The premium adds $10-$30 extra per day. Instead, just pay with a credit card (which is required in most cases anyway)… Many cards offer collision-damage coverage on domestic (and even foreign) car rentals.

Visa, for example, will reimburse your auto-insurance deductible, towing charges, administrative fees, and loss-of-use charges imposed by the rental company.

You just need to do a few things to make sure you’re covered. Most credit-card companies will require you to use the card that offers the coverage to pay the rental in full.

You also have to decline any coverage the rental company provides. Visa, MasterCard, American Express, and Discover all have slightly different policies. And not every card offered by the company has this coverage.

Just call the company’s customer service to determine if you have this coverage, learn the terms, and save hundreds of dollars a year in fees.

Also, it’s likely that much of the coverage you have under your regular car-insurance policy carries over to your rental car. Just call your insurance company to find out what’s covered before you rent next time.

As I mentioned at the start of this essay, making good money with your investments is just one part of accumulating wealth. Smart spending is another. Keep these ideas in mind when spending on cars… and your wealth will grow much faster.

Here’s to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

While the economy is looking up, Doc says investors are still afraid to buy big banks. “That is exactly why bank stocks are cheap today.” Learn why Doc thinks banks are a great buy… and a simple way to trade them… here.

With continued chaos and uncertainty in global markets, today KWN is publishing another important piece that was written by a 60-year market veteran.

With continued chaos and uncertainty in global markets, today KWN is publishing another important piece that was written by a 60-year market veteran.

The Godfather of newsletter writers, Richard Russell, covers everything from silver and gold, to heroin and another Great Depression.

He also included a key portion of an article that reveals an increase in shared living in the U.S. because Americans continue to struggle in this fragile economy.

The strategy I’m writing about today is one of my favorite, guaranteed moneymakers. These are trades we can all easily make, requiring no capital outlay and guaranteed to make a profit or you don’t make them. What’s the catch? We might occasionally find ourselves lamenting how much more money we might have made.

Experienced investors have likely figured out that I’m talking about a stock option called a “covered call.” Buying options is for speculators, and that’s not what I’m talking about today. I want to show you the one and only option trade that meets my stringent criteria for comfort.

Covered calls:

- Are easily understood;

- Are easy to implement;

- Require no market timing to make your predetermined profit; and

- Require minimal time for investors to manage.

In addition, you can calculate your profit clearly at the time of the trade (if there’s no hefty gain, you pass on it); the risks are financially and emotionally manageable; and the upside potential is excellent with covered calls. Let’s begin with the boilerplate stuff first before we discuss strategy.

There’s an options market that allows people to buy and sell options on stocks. Speculators have made millions of dollars trading options without owning a single share of stock. That’s the wrong place to be with your retirement nest egg. I’m going to show you how an average investor with an online brokerage account can supplement his income in a safe, easy, responsible, and conservative manner.

Let’s start with a basic premise: money is consistently made on the sell side of the transaction. Selling one type of option is the only strategy that will meet our stringent criteria.

Before we proceed, here’s a need-to-know glossary for covered calls:

Stock option. An option is a right that can be bought and sold. There are markets for trading options in an orderly manner. Two transactions may occur between the buyer and seller. The first is the transaction when the right (option) is sold. The second transaction is “optional” and at the discretion of the buyer. If the buyer exercises his right (option), the seller is required to complete an agreed-upon stock transaction. Today we’re focusing on covered call options.

Covered Calls. When you sell a covered call, the buyer purchases the right to buy a certain number of shares of stock which you own, at an agreed upon (strike) price, at any time before the option expires (known as the expiration date). The option buyer is not obligated to buy your stock; he has the right to do so. You’re obligated to sell the stock if the buyer exercises the option. The term for this is your stock gets “called away.” Regardless, you keep the money you were paid when you sold your option.

There are four elements to an option transaction:

- the price of the option in the market (what you can buy or sell it for);

- the number of contracts (each contract is 100 shares);

- the price of the underlying stock (referred to as strike price); and

- the expiration date.

Option price. This is the price the option is bought or sold for. This changes as the price of the underlying stock moves in the market and the time frame moves closer to the expiration date. Readers will see that there are two prices: “bid” and “asked,” just like stocks. When you sell an option, this completes the first part of the transaction. The money changes hands and is yours to keep, regardless of what happens later. Cha-ching!

Strike price. This part of the transaction is agreed upon when the option is bought/sold. Let’s assume the buyer purchased a call (a right to your stock) at a strike price of $55/share. Should the buyer choose to exercise his option, the buyer pays you $55/share, and you (through your broker) deliver the stock, regardless of the current market price of the stock.

Expiration date. Options generally expire on the third Friday of every month. When looking at the options trading platform on any major stock, you’ll find options available for several months in advance. You’ll notice that the longer the remaining time, the higher the price of the option.

At the time the stock option is bought/sold, all of the elements above are agreed upon. The buyer has until the expiration date to exercise his option. The numbers of shares and selling price have already been determined. If your stock is called away, you’ll see the cash come in to your brokerage account, and the shares will automatically be delivered to the buyer.

Never sell a call option without owning the underlying stock; it’s much too risky for your retirement nest egg.

Option contract. An option contract is for 100 shares of the underlying stock. Options are sold in contracts, and the prices are quoted per share. For example, if you see an option price of $1.15, the contract will cost $115 ($1.15 x 100 shares). If a buyer/seller wants to have an option on 500 shares, he buys five contracts.

There are two types of options: puts and calls. We’re going to discuss the only option strategy that meets our stringent, conservative criteria: selling a covered call.

Why would an investor buy a call option? Buyers of call options are generally speculators who believe that a stock will appreciate above the strike price before the option expires. If they guess right, they can make a lot of money.

The vast majority of call options expire worthless. The rules are simple. Don’t sell an option unless you own the underlying stock. (This is referred to as a “naked call”.) Don’t buy options—period!

A Savvy Strategy

We’ll use a fictional company – ABC Products – for an example. Say we bought the stock in October 2012 for $40; the market price one year later (in November 2013) was $55/share. Why would we want to sell a covered call?

In November, ABC was $55/share. We’ll say its current dividend is $0.55/share. The March call option at a strike price of $57 is selling for $1.10/share—twice as much as the current dividend.

Assume that on December 20, you either called your broker or went online and brought up ABC in your trading platform. You would have seen the current bid and asked prices. Assume it sold for $1.10/share.

Now, one of four things could have happened:

- The stock didn’t go over the $57 strike price, so the stock was not called away. In approximately 90 days, you’d have received $0.55/share in dividends, plus $1.10 for the option, for a total of $1.65. You just added more than double the dividend to your yield without spending a penny more of your investment capital. What do we do when the option expires? Look for another juicy opportunity for the June options and do it again!

- Let’s take the worst-case scenario: the market tanked. You had a 20% trailing stop in place. You got stopped out at $44—$11/share lower than the November price. But wait a minute, what about the covered call? The value of the option would also have dropped and sold for mere pennies. If you got stopped out of the stock, you could have bought back the option at the same time. For the sake of illustration, say you bought it back for $0.04. You netted $1.06/share profit. Instead of losing $11/share, your loss became $9.94. If you didn’t buy back your option, you’d have had huge risk exposure should the stock jump back up. It isn’t worth the risk, so you’d spend the few pennies it takes to close out your position.

- You wanted to exit your position before the expiration date. If the stock rises above the strike price of the option, generally the price of the option will move right along with it. If the stock moved to $59/share, you would “buy to close.” The market price should be close to $2/share; however, that would be offset by the fact that you sold your stock for $59.00 share.

If the stock remained stagnant or started to drop and you wanted to exit your position, the market price of the option would decline more rapidly. You’d likely buy back your option at a profit.

- The most difficult situation emotionally is when the stock rises well above the strike price and gets called. Let’s assume that in March, ABC has appreciated to $59/share. Your option is called at $57 (the strike price). You make a profit of $2/share from the time you sold the option, plus the $1.10/share for the option and the $0.55 dividend, for a total of $3.65/share. For the 90-day time frame, you earned 6.3% on your money ($55/share), or 24.9% on an annualized basis, net of brokerage commission. Yet we’ll lament the fact that you could have made more.

In each case, you haven’t invested any more capital. You make 100% profit on the call in two cases. The worst case is you generally break even on the options should you want to exit early. In the vast majority of cases, selling covered calls is straight profit on top of your dividends.

Here are some guidelines:

- Sell covered calls for stocks you own and would gladly keep.

- Sell covered calls to expire after the dividends are paid.

- Sell covered calls at a strike price above the current market price of the stock, referred to as “out of the money.”

- Don’t lament the times your stock gets called. You took a nice profit, and there are plenty more opportunities out there.

- Use stocks that are heavily traded, as they are more liquid.

- To calculate gains for any stock and option price combination, please use ouroption calculator, which you can download here.

Selling selected covered calls is a great way to turbocharge yield without any additional investment. At the same time, it will mitigate a bit of risk. If you have a 20% trailing stop in place and the stock gets stopped out, your 20% will be offset by the profit you made on the option sale. While most investors are starved for yield, you can find yield in the safest and easiest manner possible.

Each month, we look at the Miller’s Money Forever portfolio and recommend and track covered calls on some of our positions. If you’re not a current subscriber, I highly recommend taking advantage of our 90-day, no-risk offer. Sign up at the current promotional rate of $99/year, and download my book and all of our special reports—really take your time and look us over. If within the first 90 days you feel we’re not for you, feel free to cancel and receive a 100% refund, no questions asked. You can still keep the material as our thank-you for taking a look. Click here to subscribe risk-free today.

About the Author

Over the course of his career, Dennis Miller has consulted with many Fortune 500 companies, training hundreds of executives to effectively communicate the value of their company’s products to their customers. Among his many multi-national clients are: GE, Mobil, Shell, Schlumberger, HP, IBM, Corning Glass, Eastman Kodak, AC Nielsen, and Johns-Manville.

An active international lecturer for 40 years, Dennis wrote several books on sales and sales management. He was a contributor to… read more

Legendary investor Jeremy Grantham says the US Federal Reserve is killing the recovery of the world’s biggest economy and the ”next bust will be unlike any other”.

Legendary investor Jeremy Grantham says the US Federal Reserve is killing the recovery of the world’s biggest economy and the ”next bust will be unlike any other”.

Mr Grantham – the cofounder and chief investment strategist at the $US112 billion ($123 billion) Boston-based fund manager GMO –said he wouldn’t invest his clients’ money in US stocks for at least the next seven years because of the Fed’s ”misguided policies”.

Mr Grantham has an impeccable track record, having called both the internet bubble and then the US housing bubble. In November he said he believed the US sharemarket could rise another 30 per cent, although he believed it was overvalued, before crashing again.

”We invest our clients’ money based on our seven-year prediction,” Mr Grantham told Fortune.

….read more HERE

The Dow rose 91 points yesterday. Gold was flat – after getting battered last week.

The Dow rose 91 points yesterday. Gold was flat – after getting battered last week.

Today, we go even farther into the unknown… beyond eventually and past sooner or later… to what happens next.

Specifically, we don’t think central bankers are going to take the end of the world lying down. They’ve got tricks up their sleeves. These are not new tricks. They’ve been used many times in many different forms. But they’ve never been used on the scale we now foresee.

But before we begin guessing, let us tell you a bit about what is really happening here at Finca Gualfin, our ranch here in northwestern Argentina.

Three days ago, Jorge – the farm manager – came to us with a problem:

“Señor Bonner, we found two calves dead. They looked fat and healthy. I’m afraid it is a disease called la mancha. I saw it many years ago. Healthy young cows just all of a sudden fall down and die. It almost wiped out our herd.”

We still don’t know what la mancha is. But it is evidently not something to trifle with. Word went to Salta, a city about six hours away, that we had an emergency. A veterinarian advised us to inoculate the whole herd. Within hours, the medicine was on a bus bound for the hamlet of Molinos, about an hour and a half from the ranch.

The next morning, all the hands were turned out – including your editor. We mounted up and headed out to the campo – an immense valley of some thousands of acres. Our job was to sweep the valley of all the cows…driving them to the main corral, where they would be vaccinated.

The operation took three days. Your editor was probably more of a liability than a help. Driving cattle is not as easy as the local gauchos make it look.

When the Debt Bubble Pops

Meanwhile, away from the ranch…

The end of the world comes when the debt bubble pops. But before we get there, we will see more attempts by central banks to keep the debt bubble expanding. From Richard Duncan, author of The New Depression: The Breakdown of the Paper Money System:

Given that the Fed has been driving the economic recovery by inflating the price of stocks and property, it is unlikely to allow falling asset prices to drag the economy back down any time soon. To prevent that from happening, it looks as though the Fed will have to extend QE into 2015 and perhaps significantly beyond.

So far, so predictable. But there is a “sooner or later” for QE, too. There will come a time when the world can take no more debt… and at that point, the debt bubble will finally blow up.

Then we get the equal and opposite reaction. Asset prices that have been inflated by debt will be deflated by debt de-leveraging. A depression will most likely follow.

This is not a bad thing… not at all. Contrary to popular opinion, crashes and depressions do not destroy wealth. They merely tell you that the wealth you thought you had really didn’t exist.

As long as the EZ money flows freely, mistakes remain invisible. Rotten companies are kept alive. Bad speculations seem to pay off. Debts that can never be paid are still serviced. Stocks with little or no earnings shoot up.

Then when the bubble explodes the mistakes become painfully obvious. Phony gains return from whence they came. Investors reprice assets at more realistic levels. (After first going to unrealistically low levels and presenting opportunities for patient investors with plenty of cash onboard).

Only then, when the economy has been thoroughly thrashed can it get up, dust itself off and get back to work.

But central bankers are not likely to let it happen. They’ve made their careers by pretending to improve the economy. When the bust comes they will swing into action with more quack cures.

That is when we arrive at the second stage of the coming debt deflation. It is when we will wish we had bought more gold… more real estate… more old cars and new potatoes.

Most likely (but this is not guaranteed) central banks will find new and bolder ways to get money into consumers’ hands. (Remember Ben Bernanke’s “helicopter” speech?) This will be followed by a crisis of a different sort: high levels of consumer price inflation.

Put on your seat belt. It’s gonna be one helluva ride.

Regards,

Bill

Wall Street’s Dirty Secret

From the desk of Chris Hunter, Editor-in-Chief, Bonner & Partners

Wall Street has a dirty secret…

On average, over a five-year period, about 25% of actively managed funds outperform their indexes.

That’s just one in four funds that do a better job, on average, than an index-tracking ETF or passive mutual fund.

Another roughly 25% will underperform by a small amount. Another roughly 25% will underperform by a large amount. And another roughly 25% will shut up shop before five years is over.

In other words, by investing in actively managed funds you are giving yourself 3-to-1 odds of underperforming a passive index.

Here are the results from the S&P Indices Versus Active Funds (SPIVA) US Scorecard for 2013. It shows the percentage of active funds outperformed by the index over five years ending 2013.

As you can see, for the five years ending in 2013, small-cap funds did slightly better than usual. The small-cap index outperformed just 66.8% of them for the period. Large-cap funds did a couple of percentage points better than the average. And mid-cap funds did slightly worse than average.

This is strong evidence that you’re far better off holding plenty of diversified passive index funds in your portfolio, than chasing after elusive… and expensive… actively managed funds.

Of course, you can seek out some outperformance with a small portion of your portfolio… by stock picking or getting someone else to stock pick for you.

Just be aware that the odds are heavily stacked against your beating a passive-investing strategy over the long run.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair