Stocks & Equities

“Trump’s inaugural overseas trip could well result in a positive effect on world trade, job creation and economic growth. Coupled with the prospect of greatly increased defense expenditure, equities should benefit.”

“Trump’s inaugural overseas trip could well result in a positive effect on world trade, job creation and economic growth. Coupled with the prospect of greatly increased defense expenditure, equities should benefit.”

Given the media’s obsession with some of the President Trump’s communication challenges, it was utterly predictable that the President’s declaration that his trip to Europe and the Middle East should be considered a “home run” was met almost universally with ridicule. In truth, the President actually did accomplish a series of victories overseas, or at least laid important groundwork that should help advance American interests in ways that prior Administrations have failed to do. It’s a shame that these developments have been ignored among the din of partisanship.

From my perspective President Trump reasserted American leadership in the primary security challenge of our day, namely the defeat of radical Islamic terrorism. He also struck deals that could prove financial windfalls to U.S. industry. The President ran on security and prosperity and that was precisely the thrust of the trip.

Trump’s first stop was Saudi Arabia, the keeper of the most holy places in Islam, the most influential of the Sunni Arab states and the one with whom America has long enjoyed close relations. Over the previous eight years Sunni Arabs had been increasingly dismayed by the Obama Administration’s tilt towards friendship with Shiite Iran and her allies. (This change resulted in the Iran Nuclear Treaty which is widely despised among Sunnis.) Given that some had concluded that Trump had won the presidency on in part through anti-Islam rhetoric, his meetings in Saudi Arabia should do much to quell anxiety in America’s most important Islamic allies.

Possibly even of more significance was King Saud’s invitation to Trump to address the leaders of 50 Sunni Arab states, something never done before by a U.S. President. In his speech the President offered traditional American leadership, but in return demanded cooperation in the ideological battle with radical Islam. He exhorted Arab leaders to “Drive them out. Drive them out of your places of worship … your communities … your holy land … out of this earth.”

To achieve this he announced the opening of the new Global Center for Combatting Extremist Ideology to be located symbolically in Saudi Arabia. He assured his audience that while “America seeks peace-not war. … Our friends will never question our support and our enemies will never doubt out determination.” If any doubted Trump’s conviction, his ordering of a 59 Tomahawk Cruise missile strike into Syria on April 6th and the dropping of the CBU 43/B ‘Mother Of all Bombs’ in Afghanistan on April 14th, proved the determination of his words. All 50 national leaders signed an agreement designed to starve ISIS of international funds. This is an achievement that the mainstream press has bent over backwards to ignore.

But the biggest take away from Saudi Arabia may be financial. The Saudis agreed to a $100 billion arms purchase from the U.S. and a $400 billion joint investment in oil, gas, and high technology. Many have concluded that these deals could lead to the creation of hundreds of thousands of jobs in the U.S.

With positive accolades from the Saudis, Trump went to Israel for meetings with Prime Minister Netanyahu. While the President did not make any mention of a ‘two-state’ solution, the message was clear that Trump felt very positive that a long sought peace deal was possible between the Israelis and the Palestinians. Furthermore, in what appeared to be very friendly and positive meetings, he assured Israelis that America would “…never, ever allow Iran to possess a nuclear weapon.”

The most significant portion of the trip came when the President landed in Brussels for meetings with NATO leaders, who collectively represent America’s most vital allies. After a campaign in which candidate Trump famously asserted the obsolescence of the Post-war NATO alliance, the majority of the leaders in attendance were convinced that as President he would move past campaign rhetoric to adopt the pragmatism typical of American presidents. As such, it was expected that Trump would re-affirm the United States’ commitment to Article 5 of the NATO Treaty (that assures mutual defense if any single NATO member nation is subjected to outside attack).

To their dismay, Trump conspicuously failed to do so. This omission elicited palpitations on both sides of the Atlantic and caused many to conclude that the Western alliance had been permanently fractured and that the Russians had achieved their long awaited strategic triumph. This conclusion is laughably premature.

As an accomplished business negotiator, Trump knows that it is unwise to fold one’s cards while the hand is still in play. His real goal here is not to abandon Western Europe to the perils of Russian expansion but to compel wealthy European countries to finally pay for a commensurate portion of their own defense. For years many of these countries have spent far less than the 2% of GDP on defense as NATO membership requires. The neglect has been easy to make when these governments could be assured that a muscular Uncle Sam would always ride to the rescue regardless. As the old saying goes, “Why buy the cow when you get the milk for free?”

Undoubtedly Trump sought to create the ‘leverage of fear’ to force the cooperation of reluctant NATO leaders in meeting their defense spending targets. Following the initial shock, Trump’s attack appeared to have positive results. By the close of the NATO and subsequent G-7 meetings, many national leaders, including France’s new President Macron, who dined privately with Trump, appeared to agree that NATO must meet its defense spending commitments.

Trump also appears to have been successful in pushing the NATO allies in committing more resources in the fight against international Islamic terrorism. While ISIS has not yet been able to deploy weapons of mass destruction, it has instead been able to utilize a substitute: the weapon of mass immigration. It is likely that hundreds of ISIS cells live within NATO countries, where Muslims already have been given preferential treatment under local laws. The disgustingly barbaric ISIS attack in Manchester was mentioned repeatedly by Trump as a contemporary event in order to drive home the ever increasing, ever broadening global threat of ISIS. The Manchester attack may help stiffen the backs of NATO leaders in taking resolute anti-terrorist measures, including not merely watching but deporting known radical suspects. Again, it supported Trump’s long held stance on illegal immigration.

In the aftermath of the trip many have cited Chancellor Merkel’s remark that Europe must be more self-reliant as evidence of Trump’s failure as a world leader. But for those who have long believed the Translantic status-quo as both inequitable and inefficient, her admission may very well be a sign of his success.

The President’s trip can be viewed as the initial step of first isolating and then possibly forming a massive military U.S. led coalition of Sunni Arabs, Israel and NATO to defeat ISIS, while leaving Shite Iran and its nuclear treaty to be dealt with later. Trump’s inaugural overseas trip could well result in a positive effect on world trade, job creation and economic growth. Coupled with the prospect of greatly increased defense expenditure, equities should benefit.

Recently, lots of news items have been discussing the run in the US equity markets and “how long can it go on like this?”. Our analysis of the markets shows us that many of these industry analysts are failing to consider one very important factor in much of their results. We wanted to share this with you through our own analysis so you have a clear picture in your head regarding the potential for US equities.

In our opinion, most of the industry leading analysts are developing conclusions based on Keynesian models that fail to adjust to recent disruptions in the global markets. Keynesian theory is focused on aggregate demand and the variations of this demand factor through normal and recession/depression economic events. In simple terms, as economies falter, Keynes suggested demand would suffer as a result of constrictions within the overall economy as a natural factor. His theories were radically opposed to those of the times (early 1900s) and proposed that government intervention to support demand would provide a more substantial economic recovery as savers would be converted into consumers and economic activity would inherently increase.

These theories have become entrenched in global economics and have been put to the test recently with the 2001 and 2009 market meltdowns. Yet, we believe something unprecedented has taken place recently and most of the industry analysis still fail to understand the affects and results of these clear indicators. First, Central Banks have backed this recovery with over $18T (globally) over the past 7+ years – a massive amount of capital investment. Second, M2 Money Velocity has decreased dramatically over the past 7+ years (to levels not seen in 50 years).

Interestingly, M2 attempted a slight recovery between 2003~2005 at levels much higher than statistically normal levels over the prior 40+ years. This move is very telling in the sense that capital supply post 9/11 was resulting in healthy M2 velocity acceleration – a sign of a healthy and organically growing economy. As M2 Velocity begins to increase, the economic engine is revving up on its own. After the 2009 market crisis, though, M2 Velocity has fallen dramatically and this tell-tale indicator is indicating that we have yet to see the economy begin to REV-UP. When it does, it could be a dramatic and explosive move.

In our opinion, the recent warnings from industry analysis of a potential “end to this run” or “end of the Trump Bump” are failing to understand the fundamental capital process that is taking place right now. In simple terms, the global Central Banks have injected nearly $18+T of capital into the markets that is searching for healthy returns. Much of this capital has been used to pay down corporate debt and to provide a recovery in the ailing housing markets. Additionally, much of this capital has been deployed into restoring financial order and capabilities within foreign governments and banking institutions. Therefore, we can assume that a portion of this capital has already been deployed into suitable fundamental support systems. Yet, a large portion of that capital is still searching for capital opportunity and will transition as the marketplace identifies healthy opportunities.

It is our opinion that we are about to enter a phase of a super-bull run that may last for an unknown period of time in certain markets. We believe the US, Canadian and UK markets are uniquely positioned to take advantage of this opportunity because they inherently support mature and structurally functional economic systems. We believe other, shorter-term, opportunities will present themselves in other foreign markets as dynamics shift that represent uniquely healthy economic investment. Just as quickly as these dynamics shift from one opportunity to another, the capital deployed into these opportunities will shift equally as fast.

We do expect market pullbacks and minor corrections to occur throughout this phase of the super-bull run. It would be foolish to think that this transitional shift in capital deployment would not be without some risk. We believe any positive rotation in the M2 Money Velocity indicator will be a strong sign that “capitulation of capital process” is beginning to take hold and become the turbo-charger of the mature markets (US, CAN, UK). Until this happens, our analysis is structurally sound and functional, yet it is missing the component that will create the “super-bull event”.

See for yourself how the market is reacting within these channels and try to understand that capital will always seek to find healthy economic environments that support adequate ROI. Given the amount and scope of capital that has recently been injected into the global markets, we believe the only locations this capital will find for adequate ROI will be the mature economic systems with the capabilities to innovate, lead and adapt to global market inconsistencies.

While I feel the equities market will run out of steam later this summer July/August, there is a case for the super bull-run, the ultimate wall or worry fueled by renewed M2 velocity and a recovery at some point. Take a look at the chart below because a bull market like this could be happening again and catch everyone off guard:

Do you want to learn how to profit from our detailed analysis of the markets? Visit ATP and learn how we can help you understand market dynamics, opportunities and develop clear objectives for success.

By Chris Vermeulen

The U.S. and other nations with “free market” economies got credit for defeating the communists in Russia. That is ironic, because it is now more clear than ever that western leadership actually shares the Soviet inclination for central planning, and they have been increasingly intervening in our markets since the collapse of the USSR.

Our officials make economic policy as if healthy markets must be planned and coerced, much like the politburo. Some of this policy is created and run in the open; the government bailouts, Quantitative Easing, and zero interest rate policy, for example.

Other programs are more secretive. Investors know the “Plunge Protection Team” exists to be the buyer in markets when all genuine buyers have left. But we can only guess as to what that crew actually does day to day.

What these self-appointed market masters do in complete darkness is likely even more controversial and intrusive. They remain violently opposed to audits and other attempts to impose accountability.

But, recently, some leaked documents have given a sense of what western officials do behind closed doors.

They have actually been micromanaging markets since the 1970s.

Ronan Manly with Bullionstar wrote a terrific piece outlining the coordination among western central bankers pertaining specifically to the gold market after Nixon shut the “gold window” and launched the era of purely fiat currencies.

Wikileaks published a secret memo sent from London to the U.S. Treasury Department regarding the purpose behind the formation of the futures markets for gold.

Officials wanted to create a paper market which dwarfed the physical market and encouraged volatility; all with the aim of discouraging investors from holding bullion. To wit:

TO THE DEALERS’ EXPECTATIONS, WILL BE THE FORMATION OF A SIZABLE GOLD FUTURES MARKET. EACH OF THE DEALERS EXPRESSED THE BELIEF THAT THE FUTURES MARKET WOULD BE OF SIGNIFICANT PROPORTION AND PHYSICAL TRADING WOULD BE MINISCULE BY COMPARISON. ALSO EXPRESSED WAS THE EXPECTATION THAT LARGE VOLUME FUTURES DEALING WOULD CREATE A HIGHLY VOLATILE MARKET. IN TURN, THE VOLATILE PRICE MOVEMENTS WOULD DIMINISH THE INITIAL DEMAND FOR PHYSICAL HOLDING AND MOST LIKELY NEGATE LONG-TERM HOARDING BY U.S. CITIZENS.

The futures markets have served their nefarious purpose very well. Americans today view gold as volatile and risky, and almost no one owns any of the physical metal.

So it is with good reason that many investors look at today’s markets and sense the disconnect from reality. We now know what artificial forces produce record high stock prices relative to earnings.

We understand why precious metals investors have been driven to distraction wondering why prices never seem to reflect fundamentals. We can see why government regulators might intentionally turn a blind eye to clear evidence of bank traders rigging prices and cheating customers.

What are the consequences of all this central planning? It would be impossible to list the full effects. But is easy to identify some of the winners and losers that have been hand-picked by the bankers and bureaucrats who run this show.

The banking and finance industry has more than doubled as a percent of GDP over the past 40 years. The government sector is also just about double the size it was in the 1950s in proportion to the economy. Meanwhile, the gold and silver markets spend years with prices held at, or below, the cost of production – a playground for crooked bullion bankers.

Western central planners aren’t going to be immune from the consequences of their actions.

People are waking up to just how fake today’s markets are. After all the public interventions never end, the leaked documents are generating new awareness, and many fundamental investors now sense the markets are little more than Potemkin villages – even if they don’t fully understand why.

These factors are eroding confidence, which means the ultimate consequence of all this central planning may not be so different from that which befell the USSR. The facade can be maintained no longer and therefore crumbles.

We may be one big shock in the financial markets away from a collapse of confidence. The jig will be up. And, we can hope, responsibility will be pinned where it belongs. The central planners here in the West should be remembered for being just as inept and destructive as those who once set Soviet quotas for the production of ball bearings.

Clint Siegner is a Director at Money Metals Exchange, the national precious metals company named 2015 “Dealer of the Year” in the United States by an independent global ratings group. A graduate of Linfield College in Oregon, Siegner puts his experience in business management along with his passion for personal liberty, limited government, and honest money into the development of Money Metals’ brand and reach. This includes writing extensively on the bullion markets and their intersection with policy and world affairs.

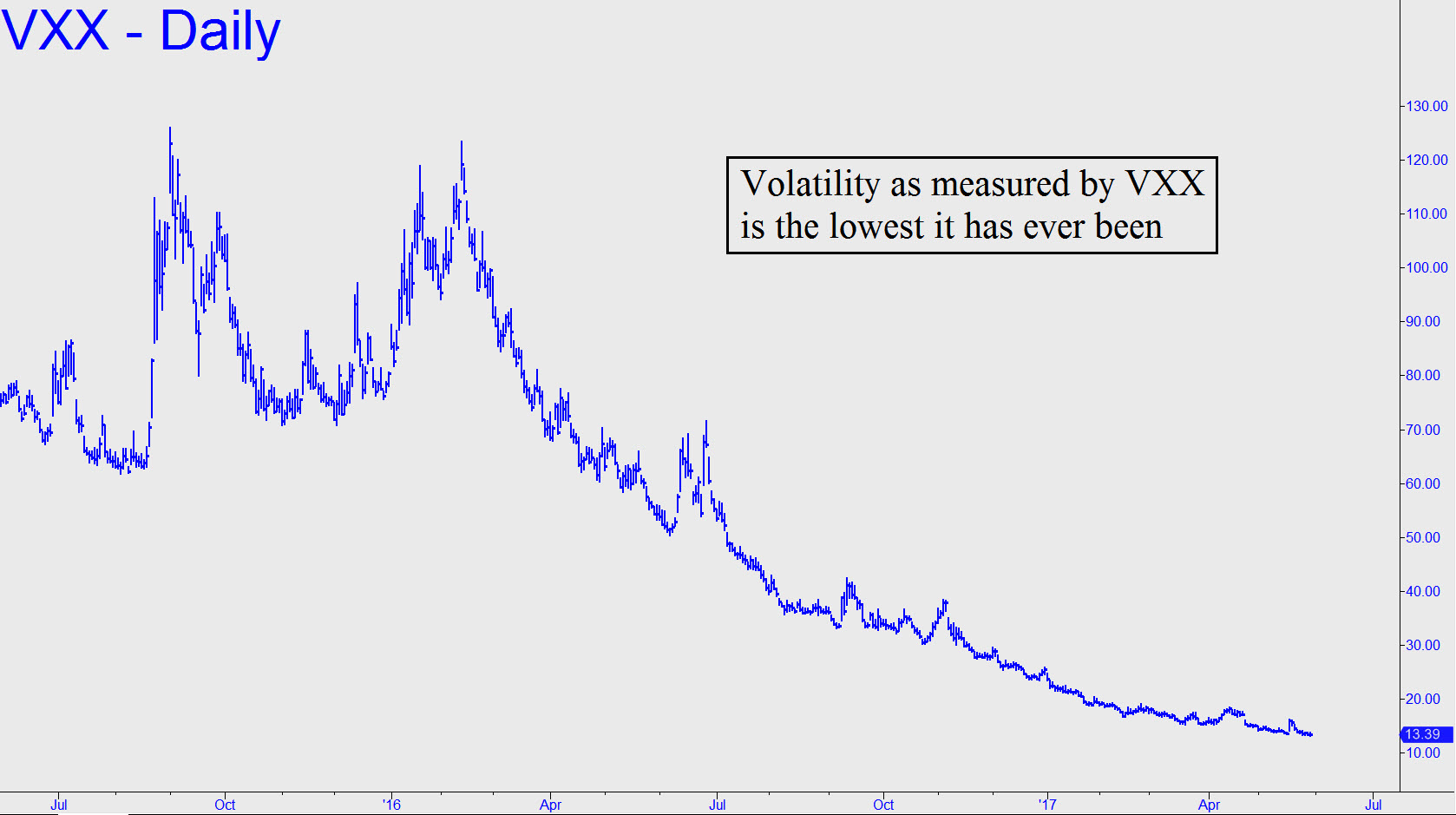

Volatility has gone brain-dead, as today’s chart makes clear. What this implies is that ‘everyone’ has bet the opposite or is hedged up the wazoo with puts, calls or straddles against a stock market melt-up or -down. Such an event is inevitable, but not on any time schedule that traders have been able to predict with any particular success. We’ve got a small bet down ourselves, having hit .666 in our last three at-bats. Two of the trades precisely caught trampoline lows in VXX within hours, allowing subscribers who followed my explicit guidance to easily quadruple their money. Some who held onto a portion of their initial position reported doing far better than quadrupling their stake. Past performance is of course no guarantee of future success, but the current bet, notwithstanding VXX’s relentless sinking spell, is one I can surely live with. See my tout below for explicit details.

If you don’t subscribe, click here for a free two-week trial that will allow you not only to view the tout, but to enter the Rick’s Picks chat room, where great traders from around the world gather 24/7.

“Technically Speaking” is a regular Tuesday commentary updating current market trends and highlighting shorter-term investment strategies, risks, and potential opportunities:

With the markets closed on Monday, there really isn’t much to update you on “technically” from this past weekend’s missive. The important point, if you haven’t read it, was:

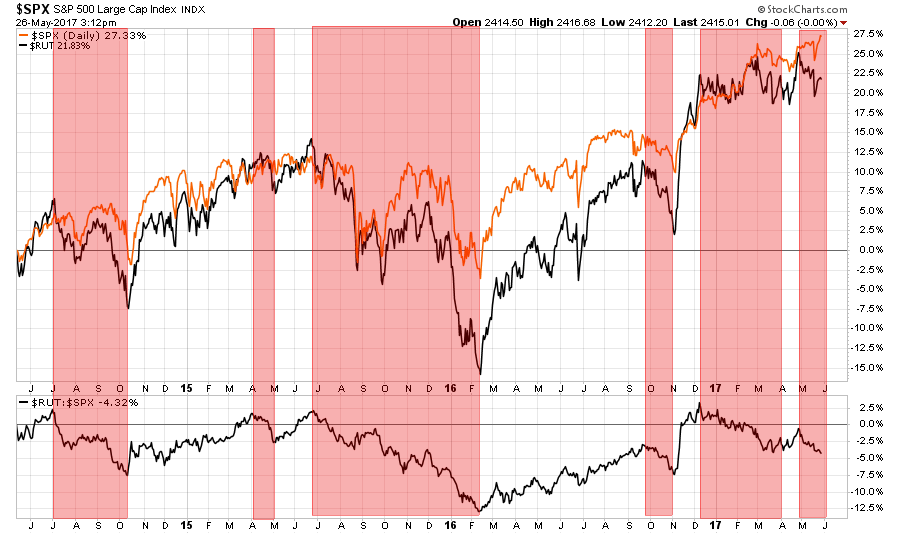

“The failure of the market to rotate to the “risk on” trade should not be lightly dismissed. A healthy breakout of the market should have been accompanied by both an increase in trading volume and leadership from the “smaller and riskier” stocks in the market.

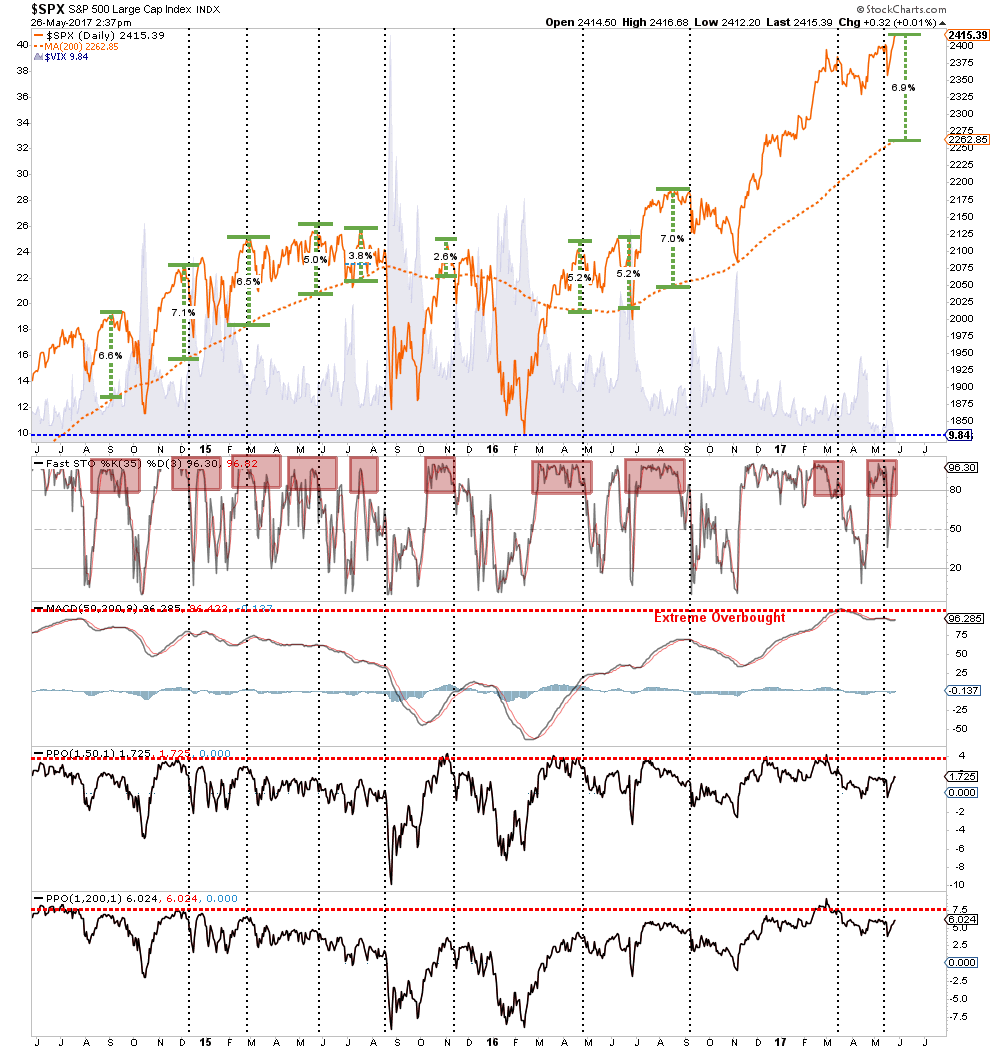

You can see this exuberance in the deviation of the S&P 500 from its long-term moving averages as compared to the collapse in the volatility index. There is simply “NO FEAR” of a correction in the markets currently which has always been a precedent for a correction in the past.

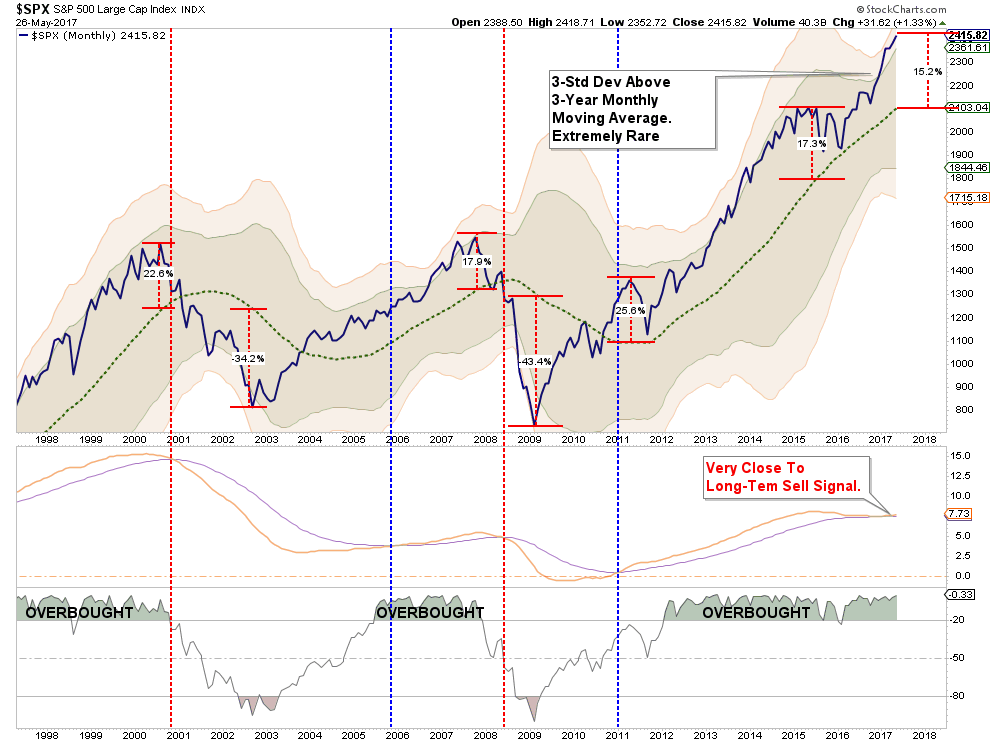

The chart below is a MONTHLY chart of the S&P 500 which removes the daily price volatility to reveal some longer-term market dynamics. With the markets currently trading 3-standard deviations above their intermediate-term moving average, and with longer-term sell signals still weighing on the market, some caution is advisable.

While this analysis does NOT suggest an imminent “crash,” it DOES SUGGEST a corrective action is more likely than not. The only question, as always, is timing.

However, this brings me to something I have addressed in the past but thought would be a good reminder as we head into the summer months:

“The most dangerous element to our success as investors…is ourselves.”

The Formula To Buy High / Sell Low

This past week, Mark Yusko and I had the following exchange on Twitter.

The point here is quite simple. Individuals, especially in very late-stage cyclical bull markets, tend to get “sucked” into the markets primarily due to the Wall Street and media driven hype which feeds the “fear of missing out (FOMO).” As I noted previously:

“The longer a bull market exists, the more it is believed that it will last indefinitely.”

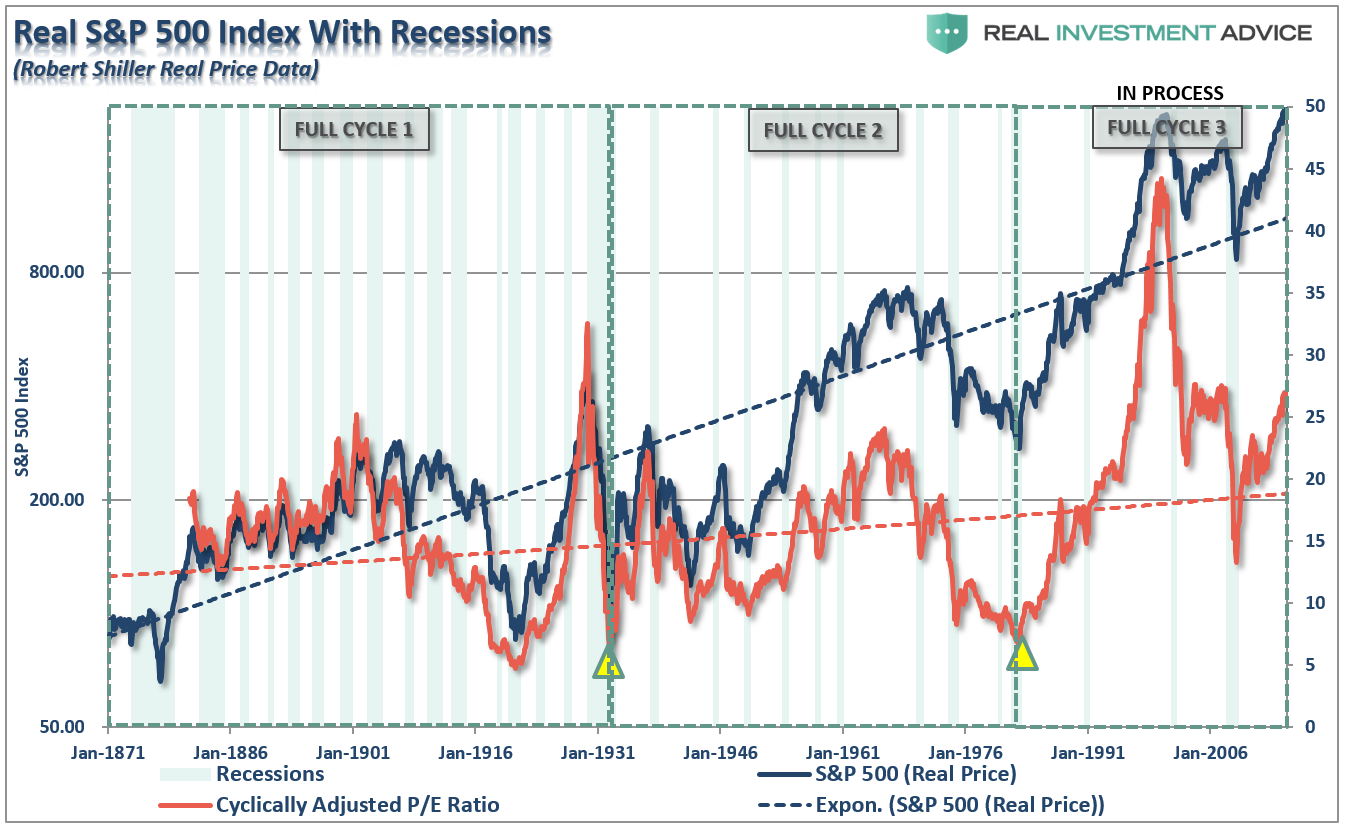

The chart below shows the long-term view of the market with its inherent full-market (combined secular bull and bear)cycles exposed.

The idea of full market cycles is important to understand as this is precisely how the formula functions. In the latter stages of the bull market cycle, as “exuberance” eventually sucks the last of the holdouts back in, the “buy high” side of the equation is fulfilled. The second half of the full-market cycle will complete the process.

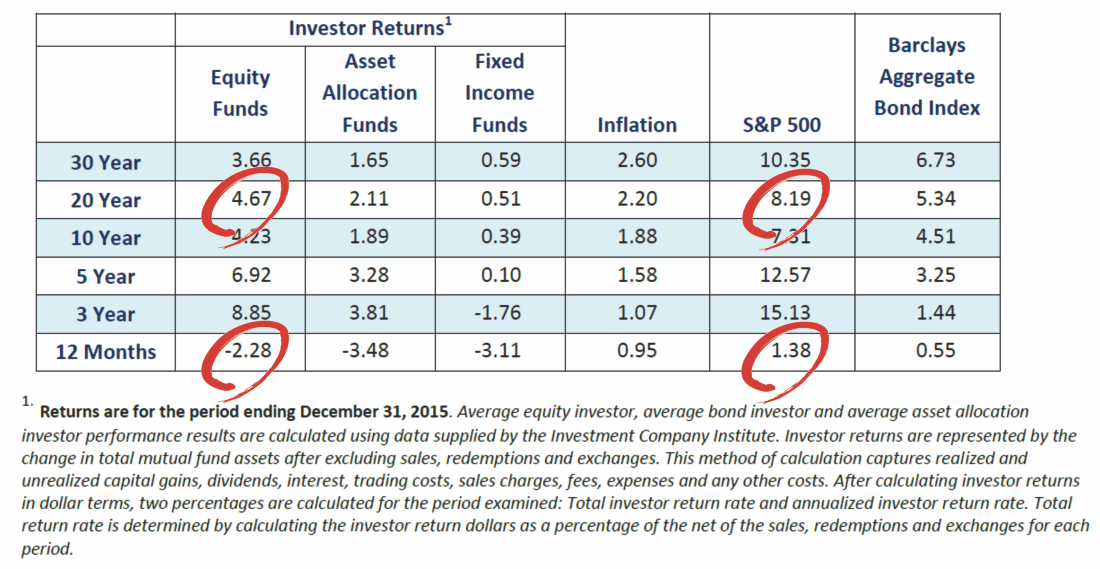

Every year Dalbar releases their annual “Quantitative Analysis of Investor Behavior” study which continues to show just how poorly investors perform relative to market benchmarks over time. More importantly, they discuss many of the reasons for that underperformance which are all directly attributable to your brain.

George Dvorsky once wrote that:

“The human brain is capable of 1016 processes per second, which makes it far more powerful than any computer currently in existence. But that doesn’t mean our brains don’t have major limitations. The lowly calculator can do math thousands of times better than we can, and our memories are often less than useless — plus, we’re subject to cognitive biases, those annoying glitches in our thinking that cause us to make questionable decisions and reach erroneous conclusions.“

Cognitive biases are an anathema to portfolio management as it impairs our ability to remain emotionally disconnected from our money. As history all too clearly shows, investors always do the “opposite”of what they should when it comes to investing their own money. They “buy high” as the emotion of “greed”overtakes logic and “sell low” as “fear” impairs the decision-making process.

Here are the top-5 of the most insidious biases which keep you from achieving your long-term investment goals.

1) Confirmation Bias

As individuals, we tend to seek out information that conforms to our current beliefs. If one believes that the stock market is going to rise, they tend to only seek out news and information that supports that position. This confirmation bias is a primary driver of the psychological investing cycle of individuals as shown below. I discussed this just recently in why “5-Laws Of Human Stupidity” and in “Media Headlines Will Lead You To Ruin.”

As individuals, we want “affirmation” our current thought processes are correct. As human beings, we hate being told we are wrong, so we tend to seek out sources that tell us we are “right.”

This is why it is always important to consider both sides of every debate equally and analyze the data accordingly. Being right and making money are not mutually exclusive.

The issue of “confirmation bias” also creates a problem for the media. Since the media requires “paid advertisers” to create revenue, viewer or readership is paramount to obtaining those clients. As financial markets are rising, presenting non-confirming views of the financial markets lowers views and reads as investors seek sources to “confirm” their current beliefs.

As individuals, we want “affirmation” our current thought processes are correct. As human beings, we hate being told we are wrong, so we tend to seek out sources that tell us we are “right.”

This is why it is always important to consider both sides of every debate equally and analyze the data accordingly. Being right and making money are not mutually exclusive.

2) Gambler’s Fallacy

The “Gambler’s Fallacy” is one of the biggest issues faced by individuals when investing. As emotionally driven human beings, we tend to put a tremendous amount of weight on previous events believing that future outcomes will somehow be the same.

The bias is clearly addressed at the bottom of every piece of financial literature.

“Past performance is no guarantee of future results.”

However, despite that statement being plastered everywhere in the financial universe, individuals consistently dismiss the warning and focus on past returns expecting similar results in the future.

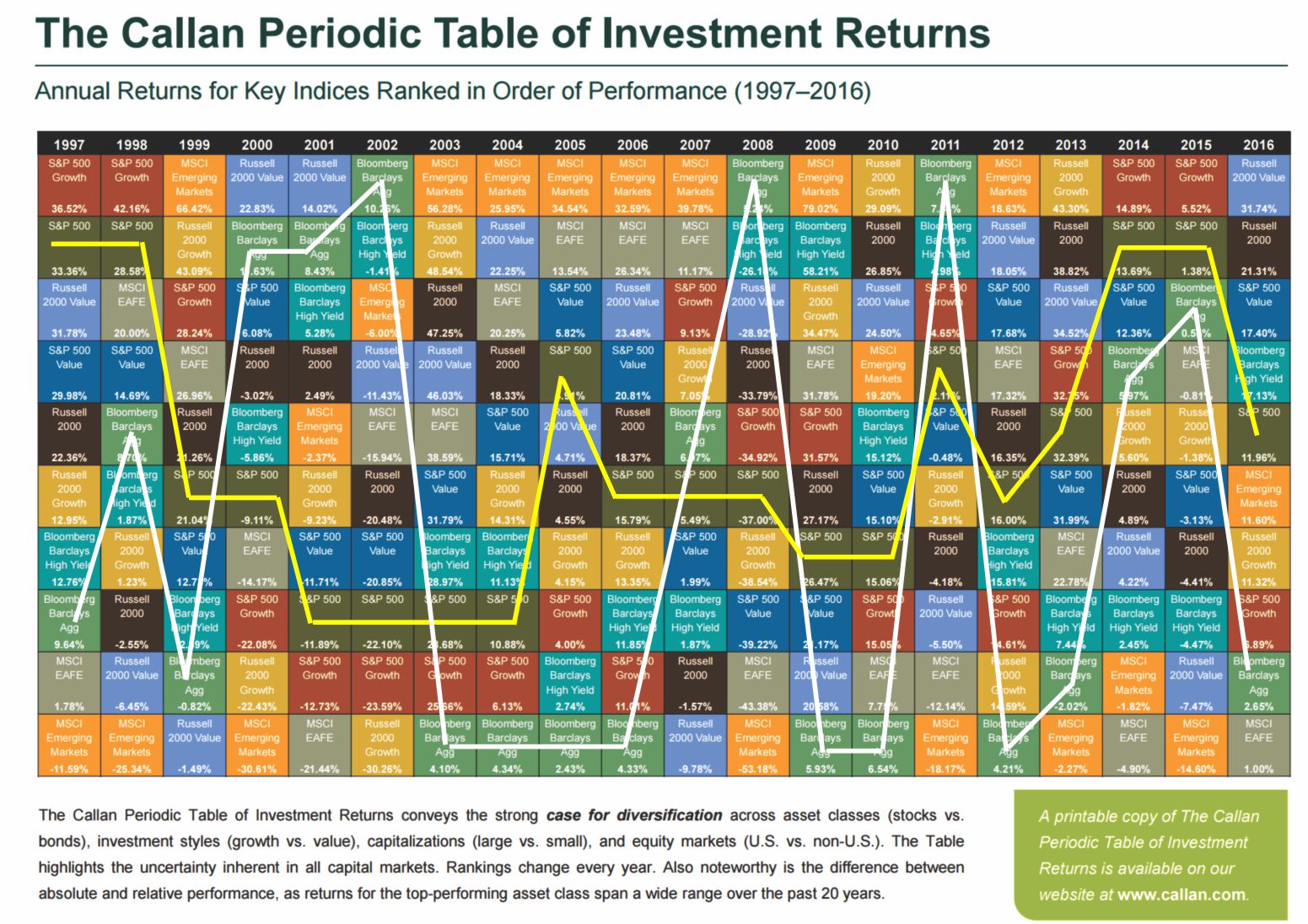

This is one of the key issues that affect investor’s long-term returns. Performance chasing has a high propensity to fail continually causing investors to jump from one late cycle strategy to the next. This is shown in the periodic table of returns below. “Hot hands” only tend to last on average 2-3 years before going “cold.”

I traced out the returns of the S&P 500 and the Barclay’s Aggregate Bond Index for illustrative purposes. Importantly, you should notice that whatever is at the top of the list in some years tends to fall to the bottom of the list in subsequent years. “Performance chasing” is a major detraction from investor’s long-term investment returns.

Of course, it also suggests that analyzing last year’s losers, which would make you a contrarian, has often yielded higher returns in the near future. Just something to think about with “bonds” as one of the most hated asset classes currently.

3) Probability Neglect

When it comes to “risk taking” there are two ways to assess the potential outcome. There are “possibilities” and “probabilities.” As individuals, we tend to lean toward what is possible such as playing the “lottery.” The statistical probabilities of winning the lottery are astronomical, in fact, you are more likely to die on the way to purchase the ticket than actually winning the lottery. It is the “possibility” of being fabulously wealthy that makes the lottery so successful as a “tax on poor people.”

As investors, we tend to neglect the “probabilities” of any given action which is specifically the statistical measure of “risk” undertaken with any given investment. As individuals, our bias is to “chase”stocks that have already shown the biggest increase in price as it is “possible” they could move even higher. However, the “probability” is that most of the gains are likely already built into the current move and that a corrective action will occur first.

Robert Rubin, former Secretary of the Treasury, once stated;

“As I think back over the years, I have been guided by four principles for decision making. First, the only certainty is that there is no certainty. Second, every decision, as a consequence, is a matter of weighing probabilities. Third, despite uncertainty we must decide and we must act. And lastly, we need to judge decisions not only on the results, but on how they were made.

Most people are in denial about uncertainty. They assume they’re lucky, and that the unpredictable can be reliably forecast. This keeps business brisk for palm readers, psychics, and stockbrokers, but it’s a terrible way to deal with uncertainty. If there are no absolutes, then all decisions become matters of judging the probability of different outcomes, and the costs and benefits of each. Then, on that basis, you can make a good decision.”

Probability neglect is another major component to why investors consistently “buy high and sell low.”

4) Herd Bias

Though we are often unconscious of the action, humans tend to “go with the crowd.” Much of this behavior relates back to “confirmation” of our decisions but also the need for acceptance. The thought process is rooted in the belief that if “everyone else” is doing something, they if I want to be accepted I need to do it too.

In life, “conforming” to the norm is socially accepted and in many ways expected. However, in the financial markets, the “herding” behavior is what drives market excesses during advances and declines.

As Howard Marks once stated:

“Resisting – and thereby achieving success as a contrarian – isn’t easy. Things combine to make it difficult; including natural herd tendencies and the pain imposed by being out of step, since momentum invariably makes pro-cyclical actions look correct for a while. (That’s why it’s essential to remember that ‘being too far ahead of your time is indistinguishable from being wrong.’

Given the uncertain nature of the future, and thus the difficulty of being confident your position is the right one – especially as price moves against you – it’s challenging to be a lonely contrarian.”

Moving against the “herd” is where the most profits are generated by investors in the long term. The difficulty for most individuals, unfortunately, is knowing when to “bet” against the stampede.

5) Anchoring Effect

This is also known as a “relativity trap” which is the tendency for us to compare our current situation within the scope of our own limited experiences. For example, I would be willing to bet that you could tell me exactly what you paid for your first home and what you eventually sold it for. However, can you tell me what exactly what you paid for your first bar of soap, your first hamburger or your first pair of shoes? Probably not.

The reason is that the purchase of the home was a major “life” event. Therefore, we attach particular significance to that event and remember it vividly. If there was a gain between the purchase and sale price of the home, it was a positive event and, therefore, we assume that the next home purchase will have a similar result. We are mentally “anchored” to that event and base our future decisions around a very limited data.

When it comes to investing we do very much the same thing. If we buy a stock and it goes up, we remember that event. Therefore, we become anchored to that stock as opposed to one that lost value. Individuals tend to “shun”stocks that lost value even if they were simply bought and sold at the wrong times due to investor error. After all, it is not “our” fault that the investment lost money; it was just a bad stock. Right?

This “anchoring” effect also contributes to performance chasing over time. If you made money with ABC stock but lost money on DEF, then you “anchor” on ABC and keep buying it as it rises. When the stock begins its inevitable “reversion,” investors remain “anchored” on past performance until the “pain of ownership”exceeds their emotional threshold. It is then that they panic “sell” and are now “anchored” to a negative experience and never buy shares of ABC again.

This is ultimately the “end-game” of the current rise of the “passive indexing” mantra. When the selling begins, there will be a point where the pain of “holding” becomes to great as losses mount. It is at that point where “passive indexing” becomes “active selling” as our inherent emotional biases overtake the seemingly simplistic logic of “buy and hold.”

Conclusion

In the end, we are just human. Despite the best of our intentions, it is nearly impossible for an individual to be devoid of the emotional biases that inevitably lead to poor investment decision making over time. This is why all great investors have strict investment disciplines that they follow to reduce the impact of human emotions.

Take a step back from the media, and Wall Street commentary, for a moment and make an honest assessment of the financial markets today. Does the current extension of the financial markets appear to be rational? Are individuals current assessing the “possibilities” or the “probabilities” in the markets?

As individuals, we are investing our hard earned “savings” into the Wall Street casino. Our job is to “bet” when the “odds” of winning are in our favor. Secondly, and arguably the most important, is to know when to “push away”from the table to keep our “winnings.”

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair