Stocks & Equities

A little and a little, collected together, becomes a great deal; the heap in the barn consists of single grains, and drop and drop make the inundation.Saadi

Trump’s win proves that mainstream Media is in trouble; it is going to be all downhill from here except for the ones that parted ways and tried to provide accurate coverage of what was going on. The crowd will turn increasingly to social media and outlets that focus on facts as opposed to fiction. Mainstream media is in for a painful ride as the crowd is not going to forgive them so easily for their transgressions; the only exceptions being the ones that portrayed an accurate image of what was taking place. Many pollsters might have to look for new jobs, and as we just stated, we feel that social media is going to be the biggest winner. Perhaps this is why Google has its eye on Twitter and has decided to donate its search engine business and in doing so take a $1 trillion business write off.

Trump’s win proves that mainstream Media is in trouble; it is going to be all downhill from here except for the ones that parted ways and tried to provide accurate coverage of what was going on. The crowd will turn increasingly to social media and outlets that focus on facts as opposed to fiction. Mainstream media is in for a painful ride as the crowd is not going to forgive them so easily for their transgressions; the only exceptions being the ones that portrayed an accurate image of what was taking place. Many pollsters might have to look for new jobs, and as we just stated, we feel that social media is going to be the biggest winner. Perhaps this is why Google has its eye on Twitter and has decided to donate its search engine business and in doing so take a $1 trillion business write off.

Google is working with a financial adviser to consider a potential bid for Twitter Inc., as the social-media company continues to explore a sale, according to a person familiar with the arrangement.In tapping Lazard Ltd., Google hasn’t indicated it will definitely make an offer for Twitter. However, the move suggests that Google is evaluating the option, pitting the search giant against other potential bidders including Walt Disney Co. and Salesforce.com Inc. Full Story

No matter how mainstream media tries to spin it, they blew it; it was Brexit on steroids. Trumps win highlights the power of social media and how terribly controlled traditional media outlets are. They misfired on Brexit and grossly over exaggerated Clinton’s lead. It was a stunning defeat and the fact that mainstream media was so far off the mark will now serve as the bedrock to propel social media to levels never seen before. Expect a whole new range of social media apps and sites to emerge that are going to put many newspapers out of business. As the masses grow increasingly suspicious of mainstream media, we believe that social media will be able to provide valuable insights into the mass mindset.

Being politically correct is now a dead concept

All over the world, the politician that speaks his mind is the one that will resonate well with the public. Those that focus on their P’s, and Q’s will be toast. The crowd seems to agree:

Most Americans (59%) say “too many people are easily offended these days over the language that others use.” Fewer (39%) think “people need to be more careful about the language they use to avoid offending people with different backgrounds.” About eight-in-ten (78%) Republicans say too many people are easily offended, while just 21% say people should be more careful to avoid offending others. Among Democrats, 61% think people should be more careful not to offend others, compared with 37% who say people these days are too easily offended Full Story

Regulations in the US are going to be torn apart

The Hill, for example, compiled a solid list of “14 Obama Regs Trump Could Undo” that are surely being reviewed by transition operatives.For present purposes, there are a couplecategories of rules potentially subject to elimination by the Trump administration. The first consists of already finalised (and often legally challenged) rules, like the Environmental Protection Agency’s Clean Power Plan and the Waters of the United States rule; the Department of Labor’s “overtime rule” and its “fiduciary rule.” Then there is the big one, Obamacare. These are long-discussed items like those in the Hill article noted earlier. Full Story

Obama care will be gutted as in general it is a disaster; “You can keep your doctor” slogan and the steep rise in premiums clearly demonstrate the detrimental nature of this program. Many small businesses were forced to fire workers as they could not afford to pay these premiums. It remains to be seen what will replace it, but for now, the news is being greeted with enthusiasm. Trump’s decision to knock off two rules on the book for every rule created should contribute to creating a more friendly business environment.

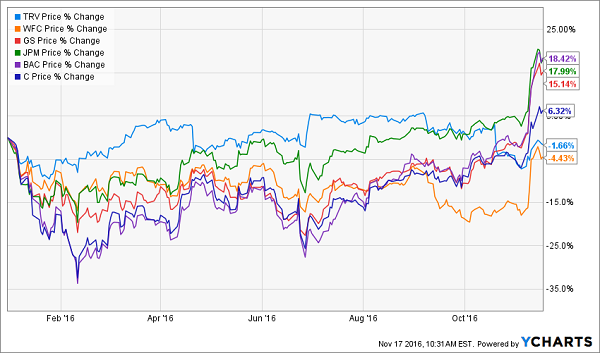

The energy, transportations and Banks are just a few of the sectors that will do well. Banks have rallied strongly as there is a wide held belief that Trump’s administration will gut the Dodd-Frank Act. This will pave the way for banks to speculate and that should provide more fuel for one of the most hated bull markets in history.

The trucking sector has rallied sharply, possibly on the expectation that tougher trade deals will be negotiated and the hope is that this will lead to a rise in manufacturing activity. Whether this belief is true or not hardly matter; the rally has gathered momentum after Trump was declared the winner. Markets are forward looking beasts and the long term trend for the transportation sector and banking sectors have turned positive. BAC and SAIA are two random stocks we picked from the banking and transportation industry to illustrate the strength behind the current rally.

SAIA Inc is just one of the many stocks in the trucking sector, but you can see how strongly it has rallied over the past few weeks. It has tacked on more than 30% in less than eight weeks and is now clearly trending upwards. There is a strong wall of resistance in the 42.50-44.00 ranges, but once it overcomes this zone, it should soar in to put in a series of new highs.

The pattern in the banking sector is pretty similar to that of the Transportation sector; Bank of America has rallied very sharply over the past few weeks, surging from the 15.00 ranges to almost 21.00 for a gain of over 30%. The stock has broken out and is now trading at new three-year highs; as the trend is up, it is likely to continue trading higher for several years to come. A Strong pullback should be viewed through a bullish lens.

Conclusion

Many sectors are breaking out, but the transportation and the financial sectors are two important segments that have the potential to drive the markets significantly higher. The financial sector has been a laggard for a long time, and as the trend change is relatively new, this trend should remain in force for a significant period. The markets have responded well to a Trump win and what we stated in an article that was penned before the election results came in has come to pass; once again proving that as long as the trend is up, every substantial pullback should be viewed through a bullish lens.

From a contrarian angle (and not a political point of view) a Trump win could be construed as a positive development; non-contrarians will demand to know why? Mass Psychology clearly states that the masses are always on the wrong side of the equation. A Trump win will create uncertainty, and the lemmings will flee for the exits; markets will pull back sharply and viola the same old cycle will come into play. The cycle of selling based on fear which equates to opportunity for those who refuse to allow their emotions to do the talking. Full Story

In general, we have stated for the past few years that as long as the trend is up, all substantial pullbacks should be viewed as buying opportunities. Some of our readers (claiming to be expert floor traders, etc.) have erroneously assumed that we are advocating a buy on the dip strategy. The keyword they forget to pay attention to is the trend. Individuals like this are famous for flip-flopping, saying one thing today and changing their stance tomorrow. Be wary of such people and take their ramblings with a barrel of salt. If this was our strategy we should have taken the same position with Gold, but since we bailed out in 2011, we have not viewed pullbacks through a bullish lens because the trend is not positive. However, we have seen the dollar through a bullish lens since 2011 as the trend is positive. Our strategy is based on the trend and market sentiment and as long as the trend is up, the greater the deviation; the bigger the buying opportunity.

If the only tool you have is a hammer, you tend to see every problem as a nail.

Abraham H. Maslow

![]()

In This Week’s Issue ending November 28, 2016:

- Weekly Commentary

- Strategy of the Week

- Stocks That Meet The Featured Strategy

- Stockscores’ Market Minutes Video – Fear Can Keep You Out of the Game

- Stockscores Trader Training – Checking the Charts

- Stock Features of the Week – Abnormal Breaks

Stockscores Market Minutes – Fear Can Keep You Out of the Game

Investors constantly hear of fear based analysis the predicts dramatic corrections. Rarely are these predictions right so there needs to be a better way. This week, I discuss this plus my regular weekly market analysis and the trade of the week on $OPXA. Click Here to Watch

To get instant updates when I upload a new video, subscribe to the Stockscores YouTube Channel

Trader Training – Checking the Charts

Stock chart analysis is becoming more and more popular every day; investors are realizing that the chart is a graphical representation of what thousands of investors believe about a stock and is often more reliable than the opinion of just one person’s fundamental analysis.

The problem is that there is a lot of incorrect chart analysis happening and one of the most common mistakes I see is the use of the wrong chart for making a decision.

Do you look at monthly, weekly, daily, hourly or even minute by minute charts when doing chart analysis? The answer should be motivated by the type of investor you are.

A long term trader, someone trying to maximize the return of their long term retirement portfolio should not get too caught up in the day to day gyrations of the market. It is the big picture trend of the market that should matter the most, making the gain or loss for the stock or the overall market on a single day quite irrelevant to the trading decision.

On the other end of the time frame spectrum are the day traders who should really be concerned with what is happening on the 2 minute, 5 minute or 15 minute charts. For the short term trader, these time frames are the most relevant and yet the decisions of many short term active traders are swayed by the headlines they read about big macro-economic issues that could affect the long term direction of the market. The level of debt that the US Government has does not have a lot of relevance to what a hot bio tech stock is going to do over the next day.

On Stockscores.com, it is possible to set the default time from of the charts you look at to suit your trading time horizon. If you are a long term trader, set the default to a three year weekly chart. Medium term? Focus on the daily chart. A swing trader can set his or her default time frame to the 15-minute time frame.

Doing this is relatively simple:

- Pull up the chart for any stock by entering the symbol in the upper right corner of the site. Remember that Canadian symbols need a prefix, T. for the TSX and V. for the Venture.

- Go to the charting tab, this is either beside the small chart view or below the large chart view.

- Make sure that the chart type is set to Quick.

- Set the interval to the time frame that suits you.

- Set the lookback period. I like to look back as far as possible without having the resolution of the chart degraded.

- Click on Create Chart

This has now established a new chart default which will remain as your default each time you log in using that computer. If you use a different device, you will have to reset the chart settings on that machine as well.

While it is important to focus on the time frame that suits your style the best, it is also wise to look at other time frames for confirmation. A person focused on the daily chart should check the weekly and the hourly for confirmation. A day trader may be focused on the two minute but a quick check of the 15 minute and daily will be helpful as well.

You can do that using the fast time frame links that you will see at the top of the chart.

Click on one of these to change the time frame quickly without changing your default chart.

Stock Features of the Week – Abnormal Breaks

This week, I ran the Stockscores Abnormal Breaks for the US and Canada. With the major markets up a lot in the last two weeks, I wanted to focus on smaller cap stocks trading abnormally as they should be able to do ok even if the market pulls back in the short term. Here are two low priced stocks that I found:

1. CTIC

CTIC had some late day buying today which pushed the stock higher and out of a bottom fishing chart pattern. Support at $0.38.

References

- Get the Stockscore on any of over 20,000 North American stocks.

- Background on the theories used by Stockscores.

- Strategies that can help you find new opportunities.

- Scan the market using extensive filter criteria.

- Build a portfolio of stocks and view a slide show of their charts.

- See which sectors are leading the market, and their components.

….related: 3 Dividend Stocks to Buy Now and Hold for 20 Years

Disclaimer

This is not an investment advisory, and should not be used to make investment decisions. Information in Stockscores Perspectives is often opinionated and should be considered for information purposes only. No stock exchange anywhere has approved or disapproved of the information contained herein. There is no express or implied solicitation to buy or sell securities. The writers and editors of Perspectives may have positions in the stocks discussed above and may trade in the stocks mentioned. Don’t consider buying or selling any stock without conducting your own due diligence.

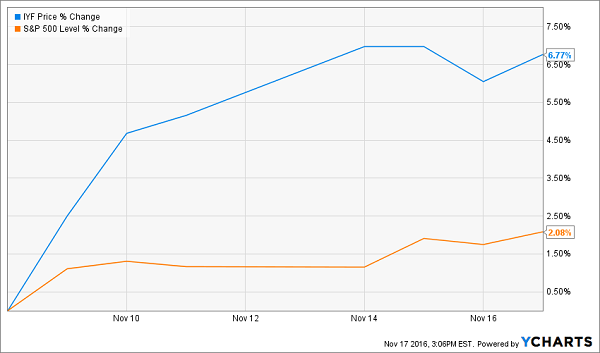

Forget the pundits—they totally blew the call on this election. And I sure hope you didn’t take their stock advice, either.

Ahead of the vote, one economics professor said the market would drop 7% if Trump won. Another analyst said you should go to cash “if you’re not already there.”

I could go on.

If you followed that advice, you’ve missed a 2.1% rise in the S&P 500 since Election Day. It’s worse if you were overweight financials, as the sector has been on an absolute tear, with the iShares US Financials ETF (IYF) surging 7.0%.

Sad!

But not surprising, as banks will benefit most from higher interest rates—and a selloff in the bond market has pushed the yield on the 10-year Treasury to around 2.25% from 1.87% on November 8.

Which begs the question: what the heck do you do with your portfolio now?

Let me give you an answer: buy more stocks, particularly companies that pay—and better yet grow—their dividends, including the three I’ll name in a moment.

But instead doing it in one fell swoop, consider using one of my favorite strategies: a “boring” go-slow approach called dollar-cost averaging.

It’s perfect for volatile markets like today’s because it’s the exact opposite of trying to time the market based on the headlines. You simply commit to buying a fixed dollar amount of a particular investment on a set schedule.

That’s it.

That simple commitment comes with an unbeatable payoff: you’ll naturally buy more shares when they’re cheap and fewer when they’re pricey.

Here’s a real-world example: let’s say you decided to invest in insurer Travelers Companies (TRV), one of the three stocks I recommend buying now and holding for the next two decades, back in 2006. And let’s say you bought $5,000 worth of TRV on the last trading day of the year over the following 10 years.

Your first purchase, on December 29, 2006, would have rung in at $54.03 (good for 92 full shares), and the latest would have been $114.12 (or 43 full shares) on December 31, 2015.

But thanks to the periodic nature of your purchases, your average price would have been just $70.05. That’s a big discount to the stock’s average price of $84.08 during that time and far below today’s price of $111.40.

And don’t forget TRV’s dividend. Shares yield 2.4% today—just above the S&P 500 average—but the quarterly payout has soared 157% in the past decade, so you’d be yielding a tidy 5.0% on your first $5,000 buy now.

Sounds easy, right? You can make it even easier by signing up for a company’s dividend reinvestment plan (DRIP), which you can do through your discount broker.

DRIPs are a powerful (yet underused) tool that lets you convert your dividend income into additional shares—and fractions of shares—commission-free.

This leads to a pleasant cycle: as you buy more shares, you generate higher dividend payments … which you use to buy more shares. And you still get the main benefit of dollar-cost averaging, because you’ll automatically buy more shares when they’re cheap and fewer when they’re pricey.

TRV: A Terrific Play on Rising Rates

Which brings me back to Travelers, a provider of car, home and business insurance that’s been around since 1853.

Insurance stocks also jumped following Trump’s win, but unlike the big banks—with the exception of scandal-plagued Wells Fargo (WFC)—TRV is still down year-to-date.

What’s more, the stock’s forward price-to-earnings ratio clocks in at 11.6, a discount to peers like Allstate (ALL), at 16.9 and Progressive (PGR), at 21.8.

That adds up to an excellent entry point on a top-quality company that stands to gain from rising rates because it invests its clients’ premiums in interest-bearing securities.

Higher income (and the fact that Travelers pays out just 26% of its earnings as dividends) means stronger dividend growth and share buybacks, both of which help drive the stock higher in a rising market and throw a floor under it in a downturn.

Follow Buffett on DAL

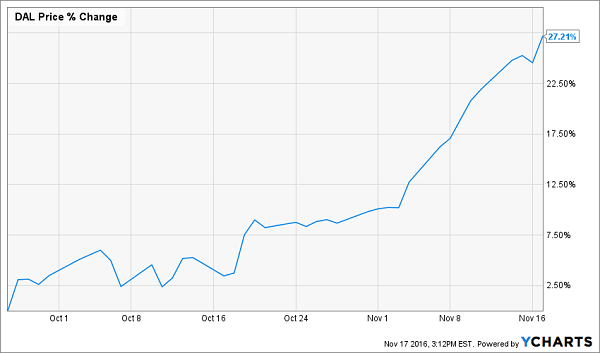

I hope you snapped up Delta Air Lines (DAL) when I recommended it on September 26. If so, you’re sitting on a 27% gain in less than two months!

If not, don’t worry. You’re not too late. Because despite DAL’s climb, it’s still down 4.5% year-to-date and sports a ridiculously low forward P/E ratio of 8.7.

That was enough to grab Warren Buffett’s attention. Last week, Berkshire Hathaway (BRK.A) revealed that it had bought stakes in Delta, American Airlines Group (AAL), United Continental Holdings (UAL) and Southwest Airlines (LUV).

The move caught the market by surprise, especially since Buffett has called airlines a “death trap” for investors in the past.

It shouldn’t have. In the past dozen years, the airline business has been whittled down to just four domestic carriers from 12. That’s put an end to cutthroat price wars and thrown up a high barrier to entry, something Buffett’s always looking out for.

Still leery? Consider this: even though many people avoid airline stocks because they see them as too volatile, that’s not the case with DAL: the stock’s beta rating is 0.89, meaning it’s historically been 11% less volatile than the overall market.

I expect DAL to catch even more lift as it flies onto income investors’ radar. The stock yields just 1.7% today, but the company has boosted its quarterly payout by 237% since it started paying dividends in 2013.

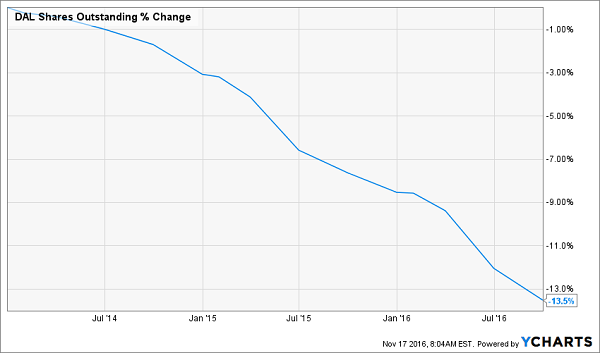

Today, DAL pays out a miniscule 10% of its earnings as dividends, so there’s lots of room for more growth and buybacks: in the past three years, it’s slashed the number of shares outstanding by 13.5%.

BPY: Set It and Forget It

The final buy-and-hold pick I have for you today is Brookfield Property Partners (BPY), which boasts a 5.4% dividend yield and trades at a ridiculously low 72% of book value (or what it would be worth if it were broken up and sold off today).

Brookfield owns malls, office towers, industrial properties, shopping centers and apartments the world over, with about 250 million square feet of leasable space.

The company (technically a partnership, not a real estate investment trust) also gives you a nice mix of high yield and strong dividend growth: since it was spun off from Brookfield Asset Management (BAM) in 2014, BPY has hiked its quarterly payout twice, for a total increase of 12.0%. That’s in keeping with management’s stated goal of hiking by 5% to 8% annually.

Those increases should be well supported by the 8% to 11% increase in funds from operations (FFO; a better measure of the partnership’s performance than earnings) per year management is targeting, thanks to rising rents, low occupancy rates and the 9 million square feet BPY has in development.

In the third quarter, Brookfield paid out $0.28 in dividends, or 85% of its $0.33 in FFO. That’s a reasonable payout ratio for the partnership, and it’s down slightly from a year earlier.

Brookfield will likely announce its next hike in early February. With the stock down year-to-date and since Election Day on overhyped interest rate fears, we’re nicely set up to buy in.

Brett @ https://contrarianoutlook.com

The Walt Disney Company is one of the largest media conglomerates in the world. To understand the company’s scale, we can look at the Media division, which alone represents approximately 40% of revenues.

The Walt Disney Company is one of the largest media conglomerates in the world. To understand the company’s scale, we can look at the Media division, which alone represents approximately 40% of revenues.

The Media division includes one of the four major television networks in the United States (ABC) and various other networks known as “Disney Channels”. The crown jewel of this division is the ESPN sports network and its affiliates (ESPN2, etc.).

Another division, the Disney brand products, has a huge library of movies among other assets. The latter continues to expand through the regular introduction of new products from various divisions, such as Pixar (Toy Story), Marvel Comics and its multiple superheroes and, more recently, the acquisition of Lucasfilm (Star Wars).

Obviously, these stories and characters are also marketed as amusement park attractions and other derivative products… CLICK HERE for Steve’s complete analysis

Last year, Richard Russell made one of his last and most shocking predictions ever. Below is what the Godfather of newsletter writers had to say. (Richard was 91 when he wrote his last article) A must Read in full M/T Ed:

Last year, Richard Russell made one of his last and most shocking predictions ever. Below is what the Godfather of newsletter writers had to say. (Richard was 91 when he wrote his last article) A must Read in full M/T Ed:

The Calls That Made Him A Legend

Russell gained wide recognition via a series of over 30 Dow Theory and technical articles that he wrote for Barron’s during the late 1950s through the 1990s. Through Barron’s and via word of mouth, he gained a wide following. Russell was the first (in 1960) to recommend gold stocks. He called the top of the 1949-’66 bull market. And almost to the day he called the bottom of the great 1972-’74 bear market, and the beginning of the great bull market which started in December 1974.

Frightened, People Wouldn’t Pay $10,000 For A Building In New York City

I remember well during 1932, that real estate parcels in New York City were often for sale for $10,000 cash. Yet they didn’t sell because people were afraid to put down $10,000 cash on a New York City building. Anybody who had cash refused to part with it regardless of the huge possible return on their money. If you had cash, you thanked God that you had it and no investment was juicy enough to entice you to put down your money. Thus, New York real estate was selling at giveaway prices and it stayed that way until the Great Depression ended..

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair