Stocks & Equities

Coming into this corporate earnings season, everyone seemed to expect disappointment. But they thought it would come from the energy sector and the banks that had lent that sector way too much money (see Goldman Sachs is a flattened slug).

Technology was, as always, thought to be immune to the vagaries of the Old Economy. But apparently what’s bad for Exxon and Caterpillar is also bad for Google and Microsoft. Here’s what Big Tech is doing this morning:

Why the sudden carnage? Various reasons, including a strong dollar (Microsoft) which makes US software more expensive for foreign buyers, the decision by several big players to ramp up growth in hot divisions at the cost of lower profits (Google and as usual Amazon), and rising competition in niches like video-on-demand (Netflix’s share price is down 30% in the past year).

But the strong dollar is by far the most common complaint. Take Microsoft’s surprisingly weak Q1 report:

(Ars Technica) – Microsoft posted revenue of $20.5 billion in the third quarter of its 2016 financial year, down 6 percent from the same quarter a year ago. Operating income was $5.3 billion, a 20 percent drop, net income was $3.8 billion, down 25 percent, and earnings per share were $0.47, a 23 percent decline.

Over the past few quarters, Microsoft and other tech companies have reported significant impact from the high value of the US dollar and have offered equivalent financial figures that show what their numbers would have been had the value of foreign earnings not been eroded by this conversion. This currency impact was estimated as reducing revenue by about $0.8 billion. The company also reports that there was a $1.5 billion impact from a combination of revenue deferrals due to Windows 10 upgrades and restructuring charges. Excluding this impact, and assuming constant currency values, the company says that its revenue was $22.1 billion (up 5 percent), operating income was $6.8 billion (up 10 percent), and net income was $5.0 billion (up 6 percent).

Now the question becomes, if Google and Microsoft are underperforming, what’s left to push US equities higher? The chart below illustrates the dilemma facing the S&P 500. Repeated stabs at the 2200 level have failed, with the latest beginning to roll over this week. The implication: The next leg up, if it’s going to happen, needs a catalyst of some sort.

So let’s consider some possibilities.

First, given the inverse relationship between interest rates and the value of corporate stock dividends, you’d expect falling interest rates to result in higher stock prices. But a consensus seems to be forming that monetary policy in general and zero-to-negative interest rates in particular have stopped working. Here’s an excerpt from Mervyn King Joins Central Banks Seeing Limits of Monetary Policy.

(Bloomberg)- Former Bank of England Governor Mervyn King added to calls by central bankers to recognize that monetary policy is close to its limit, saying the world faces a “major disequilibrium.”

Central banks need to “argue much more forcefully than they are doing that the answer is not monetary policy,” King said in an interview Wednesday on Bloomberg Television’s “The Pulse” with Francine Lacqua.

While policy makers have bought time, they can do little more, he said, noting that the introduction of negative interest rates by some central banks demonstrates they are facing “diminishing returns.”

King’s comments come amid increased questioning of monetary policy’s effectiveness even within the central banking world. Reserve Bank of Australia Governor Glenn Stevens said on Tuesday that “maybe we need to be clearer about what we can’t do,” and Stephen Poloz, who heads the Bank of Canada, said policy might be “close to its maximum ability.”

Mark Carney, King’s successor at the BOE, told lawmakers in London Tuesday that officials have room to cut the U.K.’s benchmark rate still further. Policy makers last reduced it, to a record-low 0.5 percent, under King’s tenure in 2009.

Let’s assume that this is true, and that falling interest rates aren’t going to ride to stocks’ rescue anytime soon. To push the S&P 500 beyond its current record level, then, a major buyer or group of buyers will have to analyze US equities, accept that interest rates aren’t going to fall further, and decide nevertheless to go long the market. Two logical candidates are foreign investors and US corporations. The first, according to recent reports, is not looking good, while the second is a maybe.

Chinese investors dump U.S. stocks, but corporate buybacks offset losses

(MarketWatch) – Last year, Chinese investors dumped nearly all the stocks that they had acquired over a span of seven years and are likely to remain cautious this year amid ongoing financial market volatility at home. But aggressive stock buybacks by U.S. companies flush with cash will likely offset the sting of waning Chinese appetite, according to Goldman Sachs.

China accounted for $96 billion in sales of U.S. stocks in 2015, wiping out almost all of the $97 billion purchased between 2008 and 2014, said David Kostin, chief U.S. strategist at Goldman Sachs, in a recent report. That is more than half of the $171 billion in U.S. equities sold by foreigners last year with much of the Chinese exodus occurring in the fourth quarter.

“Investors in China also sold $130 billion of U.S. debt securities in 2015, suggesting an overall reduction in U.S. investment from China rather than a rotation from U.S. equities to bonds,” he said.

The steady decline in oil prices accelerated U.S. stock sales with outflows from Canada and the Middle East hitting their highest levels since 2004.

Canadians sold $80 billion in U.S. stocks, contrasting with $3 billion in purchases in 2014. Investors from the Middle East sold $39 billion worth last year, nearly doubling the $20 billion in sales in 2014.

“Despite a low positive correlation between oil prices and flows from the Middle East, the drop in oil prices appears to have magnified U.S. equity outflows from both the Middle East and Canada,” said Kostin.

Goldman estimates that international investors will divest a total of $50 billion worth of equities this year, the second year in a row that foreigners are net sellers.

Still, corporate buybacks are expected to more than make up for dwindling foreign interest with U.S. companies projected to repurchase $450 billion in shares this year. That is below 2015’s $561 billion but above the average of $360 billion buybacks between 2011 to 2015.

“With the U.S. economy expected to grow at a modest 2% pace and cash balances at high levels, firms are likely to continue to pursue buybacks as a means of generating shareholder value,” said the strategist.

J.P. Morgan Chase, Rockwell Automation, and Bank of America have all announced sizable stock repurchase plans in the past couple of months with more companies likely to follow suit. Among the most scrutinized will be Apple, which could release its capital allocation plan as early as Monday when it reports fiscal second-quarter earnings amid expectations that the company may boost its buyback program by $40 billion to $50 billion.

Goldman Sachs expects the S&P 500’s earnings per share to rise 9% to $110 in 2016 from $100 in 2015.

We can of course dismiss Goldman’s EPS projection out of hand. Corporate operating earnings are more likely to fall by 9% than rise by any amount in 2016, based on Q1 results (see below). So for earnings per share to rise by 9% would require financial engineering on a supernatural scale.

And what about all the cash corporations are supposedly sitting on? It turns out that most of it came from borrowing, which means it’s not really cash at all, but simply the asset side of an asset/liability entry that nets to zero. Assuming there’s a limit to how much companies can borrow before new debt spooks investors and becomes a net negative, then that point is, if not near, at least closer than ever before.

Add it all up — a strong dollar that hampers exports, already-high US equity valuations, foreign investors souring on US financial assets, corporate debt at five times the 1990 level — and catalysts for another up-leg are scarce. But catalysts for the next crash are many.

Disnat GPS Commentary

Disnat GPS Commentary

Apple’s financial health is one of the best ever.

While official figures show a debt of over $50 billion and a debt/equity ratio greater than 0.40, Apple’s situation is actually much better than it seems. The company currently holds about $200 billion in cash.

That said, much of this cash is abroad, and if Apple decides to bring those profits back the United States, the amount would be taxed as profits made in the US (at a rate between 20% and 35%).

Although there are too many unknowns to make a precise calculation, even if taxed at 50%, Apple would benefit from funds that would be much greater than its debt.

We can therefore say that Apple has no net debt and clearly has a favorable cash position.

Although Apple is one of the most innovative companies in the technology sector and its range of products, which inspire new technologies, is very impressive (suggesting very promising potential sales), we must recognize that the iPhone, which represents 66% of sales, continues to have a crucial impact on the financial results of the company.

Geographically, sales are highly concentrated: 40% of sales come from the US, while China, which is experiencing the fastest growth in the world, already accounts for 25% of total sales.

With over 60% of sales made outside of the United States, a strong US dollar hurts the company’s sales and profits. We do not expect any major rise in the American dollar in the short term. If we are wrong, however, it is reassuring to know that Apple has managed to adapt to a strong dollar in recent years.

Financial Health

Growth

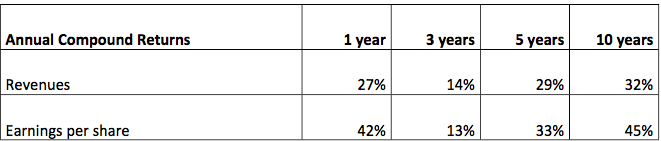

Apple’s revenue growth and earnings per share in the past five or 10 years shows that it has experienced a tremendous growth period for a large cap company.

This growth primarily comes from sales of its iPhone; in addition to representing 66% of total sales of the company, this device showed a solid growth of 52% in 2015.

In comparison, sales of PCs rank second; Mac accounts for 11% of total sales and has grown by only 6%.

Meanwhile, sales of the iPad tablet were down 23% and accounted for approximately 10% of total sales.

Geographically, sales in the US, which constitute almost 40% of total sales, experienced a strong growth of 17%, while China, which now accounts for a quarter of Apple’s sales, experienced an increase of 84% in 2015.

Although GDP growth in China is less than what was observed in previous years, we believe that the transformation of the Chinese economy to one based on consumers will continue to benefit companies like Apple.

Evaluation

Apple’s evaluation, and specifically its undervaluation, is one of the main reasons for our interest in the company.

In terms of price/earnings, price/future earnings and price/cash flow, Apple stock currently trades at a significant discount compared to its average over the past five years. In fact, with a P/E of 11.3, the stock would only be in line with its own average if it instantly rose by 25%.

In addition to trading at a discount to its own average, this stock also trades at a very deep discount to the S&P 500. In this regard, an instant increase of 50% in the stock would produce a price/earnings ratio equal to that of the S&P 500.

In other words, the market currently pays a lot less for $1 of Apple earnings than $1 earnings of an average S&P 500 company. We disagree with the idea that more than 250 companies in the S&P 500 have stronger prospects than Apple.

At Disnat GPS, we believe that the market is not evaluating Apple at its fair value, and we are very pleased to hold the stock at its current price in our portfolio of US equities.

Return on Investment

Dividend:

In 2012, Apple introduced a dividend which has increased every year since, and we are confident that this situation will last for many years. At the current stock price, the dividend represents a yield of approximately 2%.

Shares repurchase:

The company regularly repurchases its shares. In fact, over the past five years, Apple has bought over 15% of its outstanding shares. Apple still has a share repurchase program that it continues to use when the situation allows.

Investment:

Historically, Apple is not a company that has made large acquisitions, and we believe that this philosophy will continue to apply. As for internal investments, it must be understood that few new products or services can have a fast and strong impact on a company the size of Apple. However, as many consumers want to stay within the Apple ecosystem, we can be relatively optimistic and believe that some products (watches, televisions, etc.) could one day exhibit an attractive performance.

Company Description

Apple produces and markets numerous computer products, including smart phones, tablets, computers and MP3 players, as well as software and related services. The company is constantly developing new products and services like the Apple Watch, Apple TV and Apple Pay, whose sales could grow over the coming years.

Disclaimer

This Disnat GPS report is presented to you for general information only. Desjardins Group, Desjardins Online Brokerage (Disnat) and Disnat GPS assume no responsibility for any errors or omissions and reserve the right to modify or revise the content of this report at any time, without notice.

Financial and economic data, including stock quotes, analyses and interpretations thereof, is provided for informational purposes only and should in no way be regarded as a recommendation or advice to buy or sell any security or derivative.

It is possible that Desjardins or Desjardins Securities has published differing or even contrary opinions to what is expressed herein. These reflect the different views, assumptions and portfolio analysis methods used to produce them.

Desjardins Online Brokerage, its directors, officers, employees and agents will not be held liable for damages, losses or expenses incurred as a result of the use of information contained in this report.

All data comes from Morningstar (© Morningstar)

Watch as profits and dividends skyrocket this summer for these three seasonal businesses that perform best in the second and third quarter of the year. Now is the time to start accumulating a position in these stocks that could return high double-digits by late fall of this year.

Watch as profits and dividends skyrocket this summer for these three seasonal businesses that perform best in the second and third quarter of the year. Now is the time to start accumulating a position in these stocks that could return high double-digits by late fall of this year.

You have probably noticed that gasoline prices are starting to rise and have increased quite a bit in just the last few weeks. In my area, gas is up about 60 cents per gallon and seems to be climbing every day. The stocks that see immediate profit increases from higher fuel prices are usually the refining companies. The cyclical nature of the refining business has set these stocks up for some very nice gains between now and next fall, and dividend focused investors can count on some nice quarterly payouts.

Refining is an interesting industry to analyze because the prices of both the raw material, crude oil, and end product, gasoline, diesel, heating and jet fuel, are set in the commodity markets. This means that gross refining margins, usually measured on a per barrel basis, are mostly out of control of the refining companies. The factors these businesses do control are their refining efficiencies, which drive down the expenses to refine a barrel, and their sourcing practices, where they buy and how they transport crude oil.

related:

5 Big Dividends To Sell Now (& Avoid Until 2017)

Over the last couple of weeks, in both the daily blog and weekly newsletter, I have been laying out the technical case for a breakout above the downtrend. Such a breakout would demand a subsequent increase in equity risk in portfolios. To wit:

“As I stated last week, the markets have currently registered a very short-term buy signal which dictates that we must consider increasing equity risk in portfolios. I would be remiss in not paying attention that signal, but such signals can be a “false flag” during a larger market topping process.

The markets must break above the current downtrend line in order to increase allocations in portfolios. I have already positioned model portfolios to increase exposure back to 50% should such an event occur.”

I have updated the chart below through today’s open.

In This Week’s Issue:

– Stockscores’ Market Minutes Video – The Power of Trades That Feel Wrong

– Stockscores Trader Training – Understanding Confirmation Bias

– Stock Features of the Week – Penny Stock Revival Part 2

Stockscores Market Minutes Video – The Power of Trades That Feel Wrong

Trades that frighten you, those that don’t seem to make any sense, often work the best. This week, I explain why and then provide my weekly market analysis.Click Here to Watch To get instant updates when I upload a new video, subscribe to the Stockscores YouTube Channel.

Trader Training – Understanding Confirmation Bias

Investors usually do some research on the stocks that they are considering purchasing. This might involve checking the company’s financial position, reading their recent news releases or consulting research done by experts. The aim is to make a well informed decision.

If the research satisfies their criteria, a trade will be made. For most investors, that trade brings with it a dangerous commitment. Since no one likes the pain of suffering a financial loss in the market, the investor now has a vested interest in finding any information that they can to confirm that they have done the right thing.

Behavioral finance researchers call this confirmation bias. This is the tendency to seek out information to confirm their trading position and ignore or underweight anything that runs contrary to their financial interest. It is dangerous practice and one of the reasons why I think the small investor should not seek out any information at all when buying stocks. Instead, just learn how to interpret the market’s message.

Let’s say you buy a mining stock that has some gold projects that have good potential. Before you buy the stock, you read the company’s news and some analysis done by a mining expert who publishes a newsletter. All indications from your analysis is that this stock is likely to go higher.

After you buy it, the stock does go higher, adding further credibility to the research work you have done. Then, one day, the stock makes a very abnormal move lower without any corresponding bad news. You go on to a stock market message board and find a few comments about initial results from the project rumored to be poor but most comments confirm what you know; the company has some great projects.

You ignore the naysayers and seek out other information that confirms that your stock is a good one to hold. You find enough good information to convince yourself that the market’s recent downward move is an overreaction and wrong.

In doing so, you have behaved like a normal human being eager to avoid pain and pursue pleasure. Unfortunately, we humans are myopic and, in this case, you are likely avoiding short term pain but increasing the chance for long term pain. The market moved down for a reason and, if you wait to find out why, it is usually too late.

I believe that fundamental analysis is essential for the market to function and has to be done. However, it does not have to be done by you because you do not have the resources to do it well. Those who do it right will tell you what they know by their actions in the market. Just listen to them.

If you know too much about a company, you are likely to fall in love and commit the sin of confirmation bias. If you must seek out information, make sure you are balanced in how you do it.

Last week I highlighted the improved market action in the Canadian Penny stocks. This sector of the market has been the doggiest of dogs for many years but in the past couple of months, it has done very well. Take a look at the chart of the TSX Venture index ($JX on Stockscores) to see how the market has done. The leaders have been in mining with Lithium, Silver and Gold the groups that have had the action. Some Biotech names have been doing well too. My two picks from last week’s newsletter were V.SCZ which is now up 57% and V.AVL which has gained 39% at the time I am writing this. These are gains in just one week.

The easiest way to do well in the market is to trade the hot market. The TSX Venture is hot again so this week I scanned for Canadian stocks under $2, making a 3% gain today and trading at least 100 times. Here are a couple of standout charts:

1. V.GPH

V.GPH is a story that I know too well, I bought a lot of it a couple of years ago when it struggled against a weak market. Now that Lithium stocks have been strong on the Tesla battery story, people are starting to notice this one as graphite is also needed for electric cars. Most importantly for me is that the stock is breaking up from a flag pattern after showing life in early March, taking the Stockscores above 60. Support at $0.095.

2. T.CS

T.CS is a copper miner with a good turnaround chart. Broke the downward trend at the start of March and now breaking up from a rising bottom today. Stockscore now above 60. Support at $0.095.

For Tyler’s Penny Stock Revival Part 1 go HERE

References

- Get the Stockscore on any of over 20,000 North American stocks.

- Background on the theories used by Stockscores.

- Strategies that can help you find new opportunities.

- Scan the market using extensive filter criteria.

- Build a portfolio of stocks and view a slide show of their charts.

- See which sectors are leading the market, and their components.

Tyler Bolhorn: Last week I highlighted the improved market action in the Canadian Penny stocks. This sector of the market has been the doggiest of dogs for many years but in the past couple of months, it has done very well. Take a look at the chart of the TSX Venture index ($JX on Stockscores) to see how the market has done. The leaders have been in mining with Lithium, Silver and Gold the groups that have had the action. Some Biotech names have been doing well too. My two picks from last week’s newsletter were V.SCZ which is now up 57% and V.AVL which has gained 39% at the time I am writing this. These are gains in just one week.

The easiest way to do well in the market is to trade the hot market. The TSX Venture is hot again so this week I scanned for Canadian stocks under $2, making a 3% gain today and trading at least 100 times. Here are a couple of standout charts:

For the Full ![]() go HERE

go HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair