Stocks & Equities

Last March, I told you to sell biotech stocks.

The sector was coming off one of its biggest bull runs in history. From March 2012 to March 2015, the biotech sector outperformed the S&P 500 by 128%.

Following this surge, the IBB biotech ETF traded at 50 times earnings. It was also trading near 10 times book value. These valuations were close to 10-year highs.

Plus, our politicians were targeting the industry because prices for most biotech drugs surged over the past few years. I knew this would lead to tons of negative headlines as we pushed into the election year.

If you followed my lead and cashed out of your biotech stocks, you likely saved a lot of money. The IBB biotech ETF plunged 22% since my call. To compare, the S&P 500 index is only down 5% in the same time frame.

Some industry professionals suggest buying biotech stocks on this dip. But my advice is to stay away. There are still plenty of headwinds that will likely push biotech stocks much lower through 2016.

Let me explain …

The run in biotech stocks was nothing short of impressive. Some say the surge in the sector from 2012 to 2015 was based on momentum. Yet, there were also fundamental catalysts that drove most stocks in the industry to all-time highs.

For example, the U.S. Food and Drug Administration was approving new drugs at its fastest pace in nearly two decades. Once a drug receives FDA approval, the company is allowed to sell its product to consumers. That means the company will begin to generate revenue and, eventually, profits.

Plus, we saw technological breakthroughs in areas like immunotherapy, life sciences and orphan drugs (used to treat rare diseases). This led to huge investments into early stage biotech companies.

Cash was also pouring into the industry from large-cap healthcare giants.

Big Pharma companies like Pfizer (PFE), Merck (MRK) and GlaxoSmithKline (GSK)were losing hundreds of billions of dollars in revenue over the past few years as the patents expired on some of their blockbuster drugs.

To stem the bleeding, they invested (through partnerships and directly) into biotechs with promising technologies. These catalysts helped push biotech stocks to all-time highs early last year.

Today, the industry is under attack.

Democratic presidential candidate Hillary Clinton recently spoke about the recent price hikes on specialty drugs. She promised to lay out a plan to help lower drug costs if elected president.

Janet Yellen also chimed in. The Fed Chair said valuations on small biotech stocks are “substantially stretched.” This followed similar comments from N.Y. Fed President William Dudley, who warned about a possible correction in the sector.

These negative comments from political figures are not expected to go away. After all, we are in an election year. And it’s much easier for our potential presidential candidates to trash the biotech industry (in an effort to gain more votes) than go on record for supporting higher drug prices for elders.

Plus, the catalysts that helped push the industry higher over the past few years are starting to wane.

For example, sales from Big Pharma companies are projected to decline sharply from past years. That could result in fewer investments into biotech companies. And the number of new biotech IPOs (initial public offerings) declined by 30% from 2014 to 2015.

Most biotech stocks, despite the recent sell-off, are also still expensive.

Sure, you could buy the best-of-breed names like Biogen (BIIB) and Amgen (AMGN)while they are trading under 20 times earnings.

But many small- and mid-cap names are trading at risky levels. This explains the massive sell-offs we’ve seen this year in names like Sarepta Therapeutics (SRPT), Alkermes (ALKS) and Celldex Therapeutics (CLDX). These companies got crushed after clinical trials fell short of expectations.

Biotech stocks are a risky sector to invest in right now. Despite the recent sell-off, most names are still not cheap. Plus, a lot of the catalysts that fueled the sector’s bull run are waning. And the negative headlines from politicians are likely to get much worse throughout the election year.

This will likely put even more pressure on biotech stocks at least over the next six months.

Good investing,

Frank Curzio

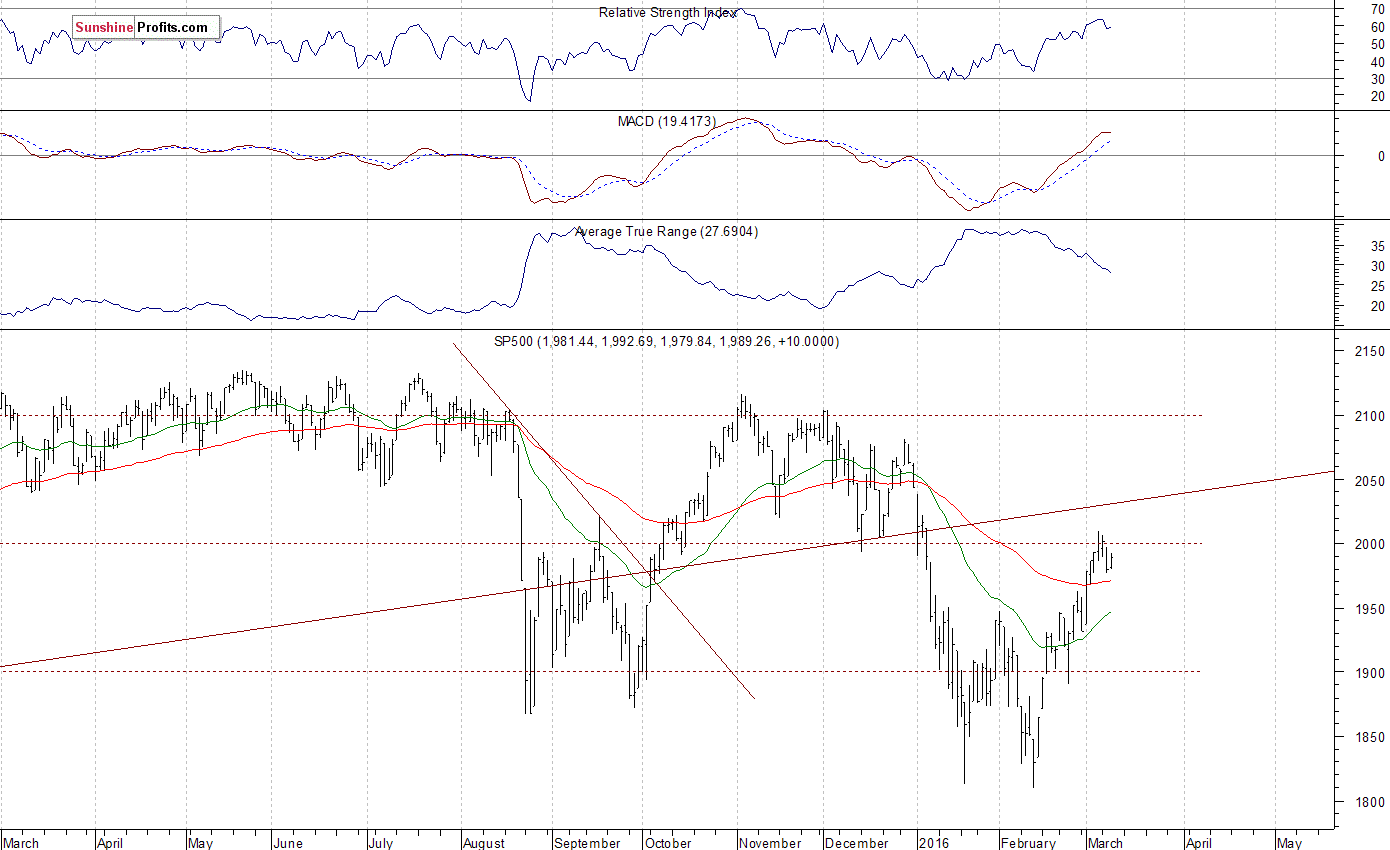

Briefly: In our opinion, speculative short positions are favored (with stop-loss at 2,050, and profit target at 1,900, S&P 500 index).

Our intraday outlook is bearish, and our short-term outlook is bearish, as we expect a downward correction or short-term uptrend’s reversal at some point. Our medium-term outlook remains bearish, as the S&P 500 index extends its lower highs, lower lows sequence. We decided to change our long-term outlook to neutral recently, following a move down below medium-term lows:

Intraday outlook (next 24 hours): bearish

Short-term outlook (next 1-2 weeks): bearish

Medium-term outlook (next 1-3 months): bearish

Long-term outlook (next year): neutral

The broad equities market has gotten a respite from the selling pressure which plagued it for the last few months. Some of this can be attributed to the Kress cycle “echoes” which we reviewed earlier this year. The echoes, which are based on the 6-year, 10-year, and 30-year cycles, suggested that stocks could experience a rally in the March-April time frame based on past rhythms. To date that expectation has materialized as traders cover short positions that were built up to excessive proportions in prior months.

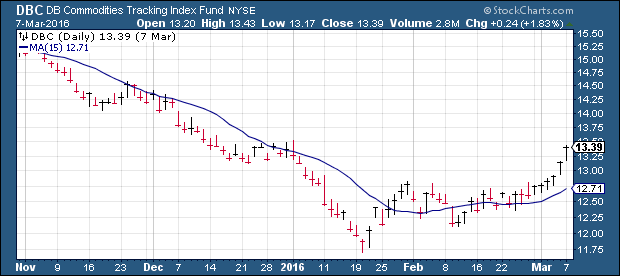

Adding to the upside in equities lately has been a long overdue relief rally in commodities and natural resource stocks. Much of the selling pressure plaguing stocks in recent months was a spillover of commodity market weakness. With commodities now on the upswing, stocks are getting a major reprieve.

The following chart shows the PowerShares DB Commodity Index Tracking Fund (DBC), which largely corresponds to the CRB commodity price index. The greater the distance DBC puts between its January low, the better it will bode for the near-term stock market outlook. A continued rally in commodities would also signal to investors that the global market crisis is in a condition of stasis. This in turn should serve to increase risk appetite among investors.

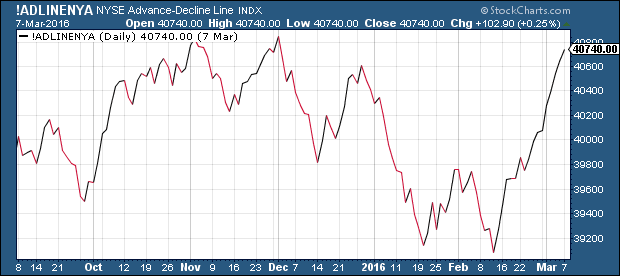

To date, all the classic signs of an interim bottom are in place. The NYSE advance-decline (A-D) line is outperforming the NYSE Composite Index. NYSE advance-decline volume is also confirming the rallies. Most importantly, the number of stocks making daily new 52-week lows on the NYSE has drastically fallen under 40 since last month. This tells us that the market’s internal health is improving and that internal selling pressure is no longer a major problem.

Moreover, the short-term and intermediate-term rate of change (momentum) of that new highs-new lows have dramatically improved in recent weeks. Because the number of stocks making new lows has dropped significantly while the overall hi-lo differential has been positive, the momentum of the new highs-new lows has finally turned up after being down for months. This indicator has been an invaluable aid to confirming that the near-term path of least resistance for stocks since last month is up.

Arguably the biggest boost to equities in the near term has been the upward turn in the crude oil price. Oil is widely regarded as the most important indicator for the overall health of the global economy. Plunging prices in the energy market in past months created a deflationary scare among investors and stoked fears of a global economic recession. Those fears aren’t completely without foundation, but for now another proverbial bullet has been dodged as the oil price enjoys a much-needed relief rally.

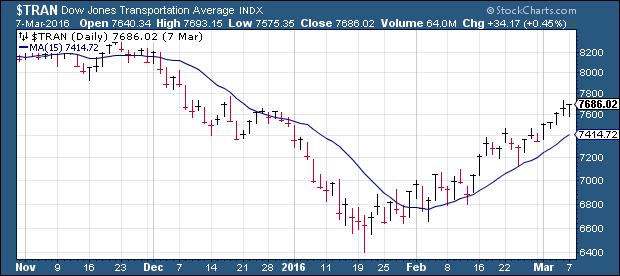

Finally, I would point out the bullish nature of the Dow Jones Transportation Average (DJTA) which has also been a strong leading indicator for the broad market – particularly the Industrials. The leadership of the DJTA has been bullish from a Dow Theory perspective, especially since the Transports led the way lower for the Industrials last year.

As the following graph shows, DJTA is about to test an important chart resistance at the 7,800 area. A breakout above this level would pave the way for another leg higher in the major indices from a Dow Theory standpoint.

In the previous commentary I noted that the bulls would likely do everything in their power to protect the 9,000 level in the NYSE Composite Index (NYA) from being violated. The NYA found support above 9,000 and has benefited from a vigorous short-covering rally since as the implications of a breakdown below this key technical level are simply too severe to happen at this time.

One reason for the premature nature of a break under 9,000 is the spillover impact such a breakdown would have on the global financial economy. The upcoming presidential election is another factor. Surpassing worries over the global economy lately has been the hysteria over the U.S. presidential race. Investors have been polarized over the leading candidates in both parties, particularly over the primary victories of a certain billionaire candidate. My policy of not commenting on politics forbids me from injecting an opinion, but I’d like to share at least one insight.

The current Republican frontrunner has undeniably garnered a rather sizable protest vote among disenchanted voters. In many ways Mr. Trump’s candidacy recalls the populist uprisings of past elections which saw the short-term success of candidates William Jennings Bryan, George Wallace and Ross Perot. In each of these cases an uncertain economic outlook led to the rise of dark horse populist frontrunners.

In the final analysis, however, America’s inveterate tendency to vote for the most electable candidate (based on the conventions of the day) won out and the extremism that characterized the earlier stages of the elections was ultimately discarded. Observers should keep that in mind as the country’s collective passions rise with temperatures this spring.

It also would appear that Mr. Trump’s ascension has been tied, to an extent, to the economic and equity market sluggishness of the last year. Indeed, his biggest victories to date have occurred when stock and commodity prices have been on the downswing and the market has been internally weak. But what happens if the market rebound gains traction and continues beyond March-April seasonal strength? Could this not fuel a resurgence in the prospects of his closest rival for the nomination? If nothing else it would erode deflation fears among investors, which in turn would defuse the urgency of the protest vote. While some may scoff at this unorthodox association, pundits would do well to monitor the correlation in the weeks and months ahead.

Mastering Moving Averages

The moving average is one of the most versatile of all trading tools and should be a part of every investor’s arsenal. Far more than a simple trend line, it’s also a dynamic momentum indicator as well as a means of identifying support and resistance across variable time frames. It can also be used in place of an overbought/oversold oscillator when used in relationship to the price of the stock or ETF you’re trading in.

In my latest book, Mastering Moving Averages, I remove the mystique behind stock and ETF trading and reveal a simple and reliable system that allows retail traders to profit from both up and down moves in the market. The trading techniques discussed in the book have been carefully calibrated to match today’s fast-moving and sometimes volatile market environment. If you’re interested in moving average trading techniques, you’ll want to read this book.

Order today and receive an autographed copy along with a copy of the book, The Best Strategies for Momentum Traders. Your order also includes a FREE 1-month trial subscription to the Momentum Strategies Report newsletter: http://www.clifdroke.com/books/masteringma.html

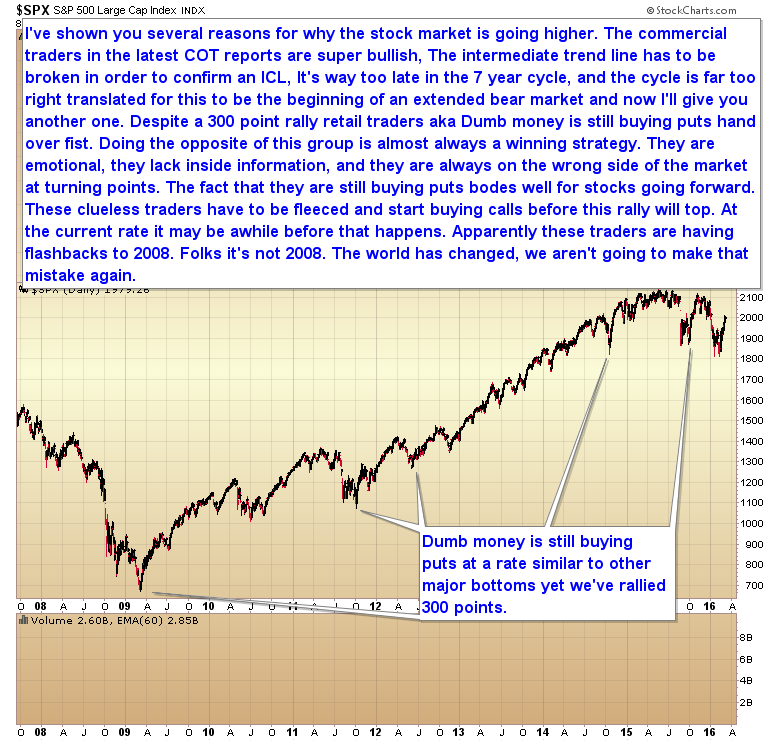

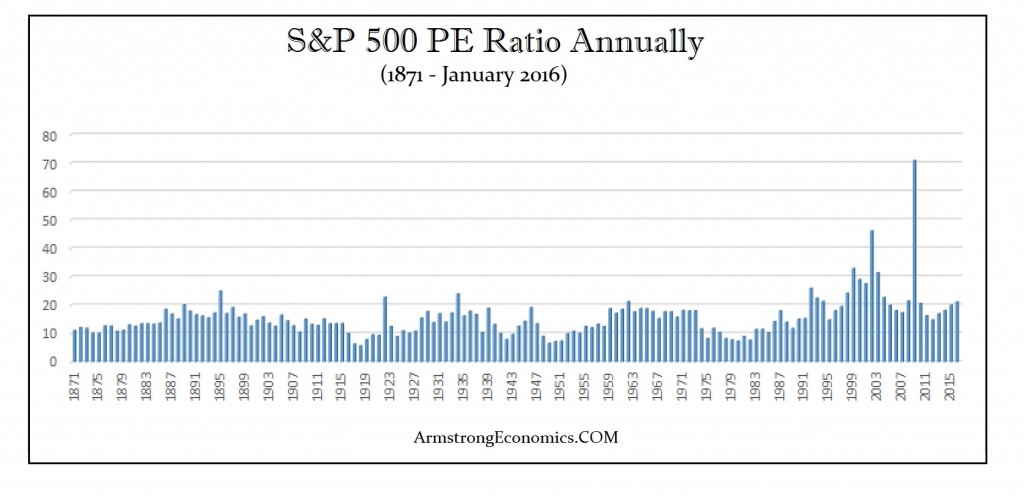

With all due respect, you have to look at this, not as a mania of speculative fever, but as a panic in government with a collapse in confidence. That is when money just seeks safety; not profit. A mania is a speculative boom where profit is the motive. What we face is the opposite. When capital is just trying to break even, the P/E Ratio rises to historical highs. Above is the P/E Ratio on the S&P 500 since the 2007 high. It rose to over 120 during the crash. This is why we warned that the market would make new highs and while Barrons reported that forecast, they were probably doing so tongue-in-cheek.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair