Stocks & Equities

Many were talking about the market crashing last week and the mainstream financial press were waxing hysterical, but as we will now see the crash hasn’t even started yet. If the press got like that last week, imagine what they will be like when it really does crash – last week was just a “warmup”, the 2nd and final warning, the 1st warning was the plunge last August.

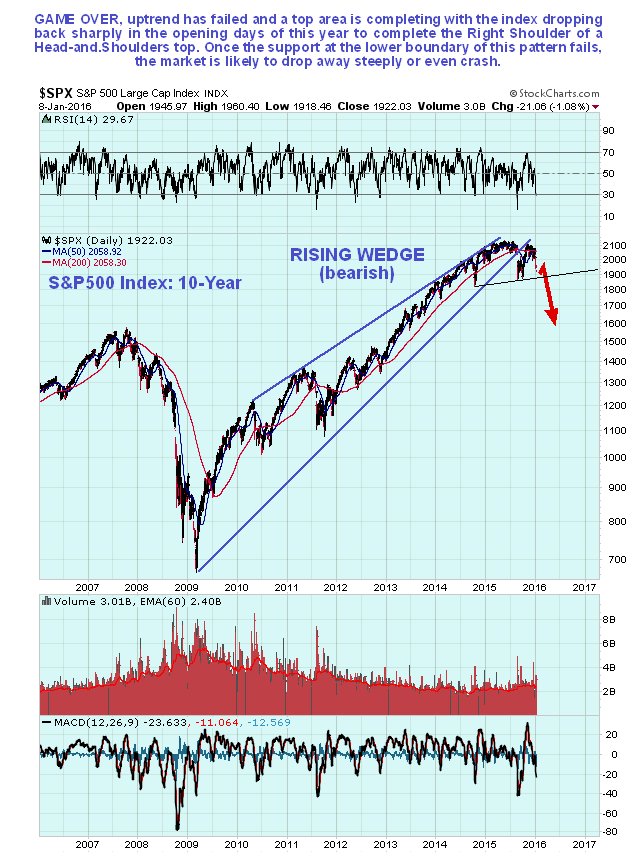

On the 10-year chart for the S&P500 index, we can see that while the market did indeed drop hard last week, it still has not broken down from its Head-and-Shoulders top, the lower boundary of which is shown by the thin black line. When it does break down from the top area, there is an awful lot of air below it – it has a long, long way to drop, and the decline is likely to be precipitous.

What a week. It’s a new year for the world’s financial markets, but it sure didn’t take long for investors to realize that the themes of 2015 are still very much prevalent. The week and the year began with Chinese regulators attempting to maintain control of their currency as the offshore market continues to discount the official rate has seen investors sell Chinese stock markets and prompt fear of further weakness in the world’s second biggest economy. The immediate and pertinent questions as fear of contagion spreads around the globe is, are the events over the previous week indicating some sort of paradigm shift in the global economy like a crisis or is this simply volatility that is to be expected in 2016?

What a week. It’s a new year for the world’s financial markets, but it sure didn’t take long for investors to realize that the themes of 2015 are still very much prevalent. The week and the year began with Chinese regulators attempting to maintain control of their currency as the offshore market continues to discount the official rate has seen investors sell Chinese stock markets and prompt fear of further weakness in the world’s second biggest economy. The immediate and pertinent questions as fear of contagion spreads around the globe is, are the events over the previous week indicating some sort of paradigm shift in the global economy like a crisis or is this simply volatility that is to be expected in 2016?

At this point, it seems the latter scenario of increased volatility is more likely. Furthermore, ending the week Friday with strong US job numbers only added credence to this point. As the US labour market created 292 thousand net jobs in December, the year of 2015 topped out as the second best year for job creation since 1999. The US economy continues to moderately advance as the least dirty shirt in an obstacle-ridden world.

The US Federal Reserve remains in their challenged position as the world’s central bank. As the IMF points out, global growth in 2016 will be muted and uneven, but domestically US businesses continue to have a positive outlook and hire. Hence, there is an environment to continue to support a strong dollar. Shifting overseas, part of the fear of the rapid currency depreciation in China, and other emerging markets is linked to local firms holding US dollar debt that inflates with currency weakness. This currency weakness is being prompted by diverging central bank policy between the US and the rest of the world. This has certainly been the dark cloud that has reappeared over financial markets, not unlike August and September of last year.

Chinese equities perhaps tell part of this story as they represent investors fleeing their domestic market, but don’t share a link to their economy that financial markets in more advanced economies may have. This is why they only an incomplete story. Proof of this is in the issues over the past week where circuit breakers and trading halts that failed to restore investor confidence and minimize what was an incomplete emotion-filled rush for the exits. As their equity markets require reform, it will be important for investors to keep this in mind in the year ahead and anticipate further violent moves. Chinese equities, while making headlines surrounding trading halts and selling bans, are only a small part of the story for global markets.

In retrospect, the outlook for the markets circles back to the US Fed and their interest rate policy. Despite the fact that we are now past the point of quantitative easing and emergency level interest rates, it is still the pace at which the US Fed continues to raise rates that will be the focus of investors. The unconventional measures of the past allowed the fed to maintain a liquidity backstop for global markets. This game is now changing as their ultra-accommodative measures are tapered back. Less liquidity prompts more volatility, and that is why in 2016 it is most important investors are tempered and have a plan for when the market sells off, instead of being caught in shock.

Over the last couple of months, I have repeatedly discussed the deterioration of market breadth, momentum and the fundamental backdrop of the markets.

Over the last couple of months, I have repeatedly discussed the deterioration of market breadth, momentum and the fundamental backdrop of the markets.

I have continually suggested a health regimen of portfolio rebalancing, profit taking and risk controls in this weekly missive: To wit:

“As always, your portfolio, much like a garden, must be tended too in much the same way. By doing so, it will ensure that it prospers and grows over time and yields a fruitful bounty.

- HARVEST: Reduce “winners” back to original portfolio weights. This does NOT mean sell the whole position. You pluck the tomatoes off the vine, not yank the whole vine out of the ground.

- WEED: Sell losers and laggards and remove them garden. If you do not sell losers and laggards, they reduce the performance of the portfolio over time by absorbing “nutrients” that could be used for more productive plants. The first rule of thumb in investing “sell losers short.” So, why are you still hanging onto the weeds?

- FERTILIZE AND WATER: Add savings on a regular basis. A garden cannot grow if the soil is depleted of nutrients or lost to erosion. Likewise, a portfolio cannot grow if capital is not contributed regularly to replace capital lost due to erosion and loss. If you think you will NOT EVER LOSE money investing in the markets…then STOP investing immediately.

- WATCH THE WEATHER: Pay attention to markets. A garden can quickly be destroyed by a winter freeze or a drought. Not paying attention to the major market trends can have devastating effects on your portfolio if you fail to see the turn for the worse. As with a garden, it has never been harmful to put protections in place for expected bad weather that didn’t occur. Likewise, a portfolio protected against “risk” in the short-term, never harmed investors in the long-term.”

As I have discussed many times in the past, the trend of the market is still positive and there is no reason to become extremely defensive as of yet. However, this does not mean to become complacent in your portfolio management practices either.”

It is that last paragraph that I want to focus on with you today…..continue reading HERE

…related:

We have a Colossal Credit Bubble in China

The Chinese economy may be headed for a “hard landing” as borrowers are taking on record amounts of debt to repay interest on their existing obligations, said Marc Faber. “We had a hard landing in the stock market already and we had a hard landing in commodities and we might have a hard landing in the economy,” Mr Faber, the publisher of the Gloom, Boom & Doom Report, said in an interview with Bloomberg Television

“We have a colossal credit bubble in China.”

The Markets

Stocks traded sharply lower on Wednesday following another weak set of economic data out of China, as well as concerns that North Korea successfully tested a hydrogen bomb. The panic sent shockwaves around the globe, fuelling another selloff in what has been a dismal start to the new year. The S&P 500 broke below the lower limit of the multi-month declining trend channel, as well as horizontal support at 1990, although the benchmark did manage to end at this level of support at the closing bell. This is the first significant crack to emerge in the market since the start of November peak in equity benchmarks, possibly suggesting the conclusion to the two month old period of consolidation. While trying to avoid becoming too anxious to conclude a longer-term topping pattern, shorter term, the market is oversold around present levels. At the lows of the session, buyers did appear, potentially covering short positions given the employment report on Friday and the start of earnings season next week. Investors will be hesitant about holding negative bets into these pivotal events. Short-term resistance on the S&P 500 Index is apparent around 2020 and then around 2040.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair