First, let us check in with the markets. Little change since yesterday. Gold is holding above $1,200 an ounce. Stocks still near record highs, as US corporate earnings fall. Bloomberg:

First, let us check in with the markets. Little change since yesterday. Gold is holding above $1,200 an ounce. Stocks still near record highs, as US corporate earnings fall. Bloomberg:

[T]he current estimates show [earnings] will drop 4.5% this quarter. And don’t forget, that’s compared with a 2014 period that included the famous polar vortex… The second quarter’s not expected to be much better, with a 2.8% drop projected.

“The stock market’s march into record territory in the face of deteriorating profit trends makes many professional investors, including ourselves, instinctively uneasy,” Carmine J. Grigoli, chief investment strategist at Mizuho Securities USA Inc., wrote to clients today.

Our advice: Stay in cash, gold and stocks you won’t want to sell even if their market prices get cut in half. This is no time for the amateur speculator to be in the US stock market.

Now, back to Part II of our series, “Money Isn’t Everything.”

High and Dry

We spent all day yesterday getting here.

Where is here?

It’s in Salta Province, Argentina. It’s high. It’s dry. It’s at the end of a long mountain valley, with the snow-capped Nevado de Cachi at the north end and the giant Cerro Remate at the other.

It’s almost impossible to get here unless you know where you are going. In places, the road is a dirt track, with no signs to guide you.

In others, you might get stuck in sand… or in a river… depending on the weather.

When we reach the hamlet of Molinos, we leave the main “highway” (a gravel road) for a rougher dirt road. We cross the river (which was dry) and head southwest toward Cerro Remate. As long as we can see its peaks, we know we’re going in the right direction. Our farmhouse sits at its base, with the ranch stretching out around it.

It is beautiful this time of year. The “rainy season” is largely wishful thinking here. Still, this year we got an average rainfall, totaling about 6 inches.

But it all fell in the last few weeks. So the hills are covered with flowers – sage, cactus, yellow flowers, red flowers, fragrant flowers and bushes.

What isn’t yellow, red or blue is green. And the cattle are eating it as fast as they can – trying to load on as many calories as possible before it all dries up.

A Changing Valley

Yesterday’s Buenos Aires Herald carried the news that there are some 200 million people in Latin America who live on between $4 and $10 per day.

These people are “vulnerable,” says United Nations Assistant Secretary-General Jessica Faieta. She might have been describing about half the people in this valley.

That is to say she might be describing them if she had even the faintest idea of what she was talking about.

Until the government began its latest welfare program, people here had almost no money.

They lived on what they produced with hoes – corn, onions, potatoes, quinoa and beans – and on the animals they raised: beef, lamb, llama and goat. They weaved the llama hair into blankets and ponchos. They traded calves and goats for shoes and hats.

As near as we can tell, they lived decently… even with a rustic elegance. And many survived into their 90s without ever seeing a doctor or a psychiatrist.

But now, with money coming from the Argentine feds, life in the valley is changing fast. The young locals watch TV (using solar panels supplied by the government) and go into town rather than weaving their blankets or planting their ancient varieties of corn.

Now, they depend on the government as they once depended on the rain.

“We need to invest in the skills and assets of the poor,” suggests the UN official.

Meanwhile, she admits, “well-being means more than income.”

Further on in the Herald, actress Patricia Arquette is featured. Accepting her Oscar last week, she confessed her concern about equality between men and women.

Unlike the world improver from the UN, Arquette seems to think that income is all that matters. The paper notes that having children seems to slow down women’s earning power. “Women with children are far worse off than single ones,” it proclaims.

Therein, of course, hangs a long tale.

Single women – without children – make about as much as men. But women cursed with offspring make much less. Apparently, there is no joy in motherhood sufficient to offset a decline in wages, at least none that occurred to Ms. Arquette.

Emile’s Story

We once spent a year in a small village in the French Alps. Among the residents was an old man named Emile. He lived in a rustic chalet on the side of a mountain and tended a garden and a small orchard.

From the garden, he took generous harvests of beets, salads, carrots, leeks and other vegetables. He used cold frames to extend his growing season. And he packed away his carrots and potatoes in dry sand so they lasted all year.

His small orchard gave him apples and pears – from which he made cider and jam. It was too cold for peaches. He overproduced, intentionally, and traded much of his produce with a dairy farmer, from whom he got milk and cheese.

Emile never left the village. When he wasn’t tending his garden or his orchard, he sat out in front of his house carving wooden bears, reading, drinking coffee or just enjoying the warm sun.

In the cold weather, he stayed in his kitchen, which was heated by a big wood-burning stove. He bought bread from a local bakery. He must have bought flour and sugar too. But we never saw him do it.

Emile was far happier than most of our millionaire friends. And far healthier than most people – even those half his age – with luxury spa memberships. Whenever we passed, he invited us into his cozy kitchen for a drink of cider.

Yet, Emile must have lived on less than $4 a day, which would have put him below the poverty level, even for South America.

“Vulnerable”?

Not at all. He was probably the least vulnerable person we have ever met. If the stock market got cut in half, he wouldn’t have noticed. If the country fell into a recession or depression, it wouldn’t have changed a thing about his life or his living standard.

Emile needed no job. He paid no mortgage. He awaited the arrival of no check, neither from the government nor from anywhere else.

It’s not lack of income that makes you vulnerable. Nor is it lack of income equality that makes you a schmuck.

More to come…

Regards,

Bill

Market Insight:

Risk of a Bear Market “Higher Than It’s Been in Years”

by Chris Hunter, Editor-in-Chief, Bonner & Partners

Bill might miss the fireworks on Wall Street while he’s up in the mountains of Argentina…

According to his old friend Mark Hulbert of Hulbert Financial Digest – which tracks the advice of more than 160 financial newsletters – the risk of a major bear market in stocks is “now higher than it’s been in years.”

That’s because the top-performing advisers of 2014 are now recommending portfolios more than three times riskier than the US stock market.

As Hulbert writes:

What makes this trend so alarming is that the stock market has been near a major top whenever the top performers’ risk levels were at or close to current levels. In 2006, for example, the last calendar year prior to the 2007-09 bear market, it rose to slightly higher than current levels: 3.85 times riskier than the market versus last year’s 3.32 times.

In 1999, the last calendar year prior to the bursting of the dot-com bubble.

The thinking behind Hulbert’s indicator is that, as a bull market matures, newsletter editors recommend their readers take on increasing levels of risk… until the next bear market strikes.

Or as Hulbert puts it: “Almost by definition, this bull market will end when the fewest amount of people are acting out of fear of another bear market.”

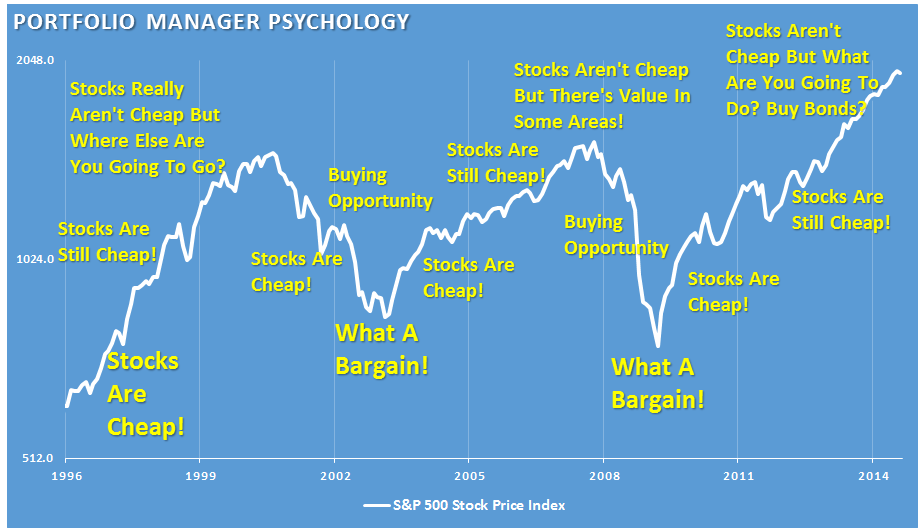

The bottom line: US stocks are in record territory. The bubble continues to build. When it bursts – and it will – you need to know how to protect your wealth.

{kind=link}

{kind=link}