Stocks & Equities

A common theme in most of last year’s missives was the extreme level of complacency in the markets due to extremely low volatility. That has now changed as over the last couple of months market movements have expanded rather dramatically. The previous complacency that markets will only go up is now being questioned and the very issues that I repeatedly warned about last year, are now coming home to roost.

A common theme in most of last year’s missives was the extreme level of complacency in the markets due to extremely low volatility. That has now changed as over the last couple of months market movements have expanded rather dramatically. The previous complacency that markets will only go up is now being questioned and the very issues that I repeatedly warned about last year, are now coming home to roost.

Over the last several weeks I have been discussing the need to increase equity allocations in the portfolio model as we enter into the seasonally strong period of the year. However, I very specifically qualified that statement by stating:

“As I have repeated many times over the last couple of weeks, I am not highly convinced of the markets at the current time. Therefore, if you choose to wait for a stronger confirmation before increasing exposure that is completely acceptable.”

While up almost 2% on the day, Toronto’s main index has gotten off to a rocky start in 2015, down 2.2% year-to-date.

While up almost 2% on the day, Toronto’s main index has gotten off to a rocky start in 2015, down 2.2% year-to-date.

Bucking the trend – we are happy to report that the recommendations from KeyStone’s Annual Cash Rich, Profitable Small-Cap Report are off to a great start. In fact, one of our 3 Top BUYs jumped over 40% this week alone!

Starting with over 3,500 Canadian stocks, our Cash Rich, Small-Cap research uncovered over 60 Small to-Micro Cap stocks – all profitable, cash rich (no debt) companies, many with between 10-100% of their market caps in cash. The report drills down on each providing fundamental statistics and research notes from our management interviews and provides a select number of NEW BUY Reports. Flash Updates with current BUYS|SELL|HOLD ratings on all Cash Rich Stocks currently in coverage.

New buy recommendations included 2 high growth software Small-Caps, one low-priced Micro-Cap and bonus notes on our recent Specialty Pharmaceutical selection which trades at a significant discount to its peers. The report has become an annual must read for growth and value investors and with 16 stocks receiving premium takeover bids it serves as an excellent source of potential takeover targets. We believe this year’s edition will once again include several takeovers.

The report offers unique research you cannot find anywhere else. Last year’s Top Cash Rich recommendation, a Specialty Pharmaceutical Small-Cap, has gained over 145% – do not miss out on this year’s recommendations. If you are not a client to our Small-Cap research you can purchase the report individually today for $599: click here to purchase.

Today’s gain on the Toronto stock market’s benchmark TSX index came after declines in each of the previous five sessions. It still recorded a drop on the week, a period in which market volatility surged due to choppy oil prices and Switzerland’s move to abandon its more than three-year-old ceiling on the Franc’s value against the Euro.

Oil prices, under pressure since June due to concerns about oversupply (and many other factors), strengthened after the International Energy Agency said that it expects “the tide will turn.” Additionally, survey showing that U.S. consumer sentiment rose in January to its highest in more than a decade provided further support for oil.

Whether oils move was a dead-cat bounce or the potential of a bottom forming, we do not see the necessity of jumping on oil related names near term. We hold a couple select names in this segment at present with excellent balance sheets and strong current and future business prospect and we will stick to them, clipping their dividends while we wait.

We continue to focus more on Knowledge Based Businesses in technology as well as healthcare for growth near and long term. Additionally, we selectively continue to like basic meat and potatoes businesses that survive and thrive in most any market conditions – our long-term clients are very aware of these select Canadian Small-Caps.

I don’t want to make too much of today’s news and market action, but on the other hand, I want to make sure to acknowledge what importance it does have and the fact that I think today will be looked back on as a red letter day for “administered rates” on the part of the central planners who call themselves central bankers.

I don’t want to make too much of today’s news and market action, but on the other hand, I want to make sure to acknowledge what importance it does have and the fact that I think today will be looked back on as a red letter day for “administered rates” on the part of the central planners who call themselves central bankers.

By now I’m sure everyone knows that the Swiss National Bank last night abandoned its promise to defend the floor of the euro-Swiss franc exchange rate at 1.20CHF. It also announced it was going to expand its negative deposit rate by 50 basis points, which will now range between -1.25% and 0.25%. (I have no idea how the SNB can administer that rate or how much money printing will be involved, but in all likelihood it will be less than it would have been forced to do to defend the peg further.

From Neutral to Neutron

That unleashed incomprehensible volatility, as the Swiss franc quickly exploded 40% versus the euro before trimming the loss to “only” 15%. I seriously doubt there has ever been a major currency move that far, that fast. (There was similar motion versus the dollar as well.)

Before discussing the various market responses (and I’m going to miss a lot because it’s not possible to capture them all), I’d like to focus on what the big takeaways are from the SNB’s action. First of all, the most important lesson to be learned from this is: no one (not even a central bank) is bigger than the market. I know a lot of people have trouble understanding this because the only history that they have seen firsthand has been the central banks getting their way with virtually every market they command to do their bidding, but that won’t always be the case, and today is a perfect example.

[Read: Global Growth Scare Could Sink Stocks in 2015]

The Swiss had said they would defend the peg no matter what, and all they had to do was print money to accomplish that. However, the consequences of that money printing in terms of speculation inside Switzerland obviously became a cost that was too high for them to continue the process. Therefore, the markets have won. If we have reached the zenith for belief in the ability of central bankers to control any and all markets, there will be big ramifications as a consequence.

Peggy, Bar the Door!

The second most important takeaway is that we are going to continue to see intense volatility virtually everywhere. When central banks print money to suppress (or redirect) the action of the economy because they don’t like the direction it is going, markets are going to become volatile. Just like if they try to peg a currency or some other financial instrument, and monetary policy swings wildly to achieve that, so would the economy.

Thus, oil has collapsed 50% in a few months. Copper has been hammered 15% in six weeks. We’ve seen the ruble obliterated, and now the craziness in the Swiss franc and other currencies (the Swiss stock market also lost 10%). Immense volatility is liable to be the order of the day in the future, not the completely suppressed volatility we saw in 2014. (As I said at the end of last year and repeated at the beginning of this one, 2015 is not going to look anything like 2014. The year is barely a few weeks old and that already looks like a drastic understatement.)

The next conclusion I believe is going to be that folks are no longer going to be able to “trust” the central banks, since bankers can change their minds. We are going to see that in America when it turns out the Fed is unable to raise rates, except instead of breaking a promise like the Swiss did it will be more like, “Gee, we changed our mind.” That, too, will add to volatility and eventually lead to lower multiples in financial assets I would think.

Currencies Take Up Tai Chi

Though this is a bit of speculation on my part, I also believe it is going to become clearer to many people that, as far as paper currencies go, nobody wants to have a strong one. They are all battles of wits between unarmed opponents. Gold, on the other hand, is viewed by many as a currency, even though a lot of so-called enlightened people view it as a “barbarous relic.” I expect gold will come to be looked at as the one currency that doesn’t mind if it trades higher versus others and doesn’t really have a central bank to manage it. Therefore, it is no one else’s liability.

Colored pieces of paper can wage war against each other as they all do laps around the drain versus real assets, and gold will be the store of value that people use to preserve the purchasing power of their colored paper over time. This also probably means that the ECB is getting ready to do something hefty in the QE department, and the Swiss knew that would be untenable for them, so more liquidity is probably on its way, though the response may not be the same in all markets as it has been based on the fact that some confidence (and money) has surely been lost.

Volatility a Double-Hedged Sword

Lastly, I think it is a virtual certainty that there are going to be a lot of “dead bodies” in the leveraged hedge fund community, as the size of the moves we’ve seen have undoubtedly hurt some people, especially anyone who was playing along and assuming the SNB would be true to its word.

So that’s my quick summation of the important ramifications of today’s action on the part of the SNB. Obviously, there are more conclusions to be drawn and actions to take, but that is at least some initial food for thought.

[Hear: Rick Santelli on Volatility: You Ain’t Seen Nothing Yet]

With all of that blather out of the way, turning to the action, overnight our stock market had been strong, but (post the SNB news) it didn’t take long for the buying to turn to selling and through midday the indices were modestly lower. Over the course of the day, the market just sort of wandered around the early lows (in a sort of stunned fashion) before it limped into the close with a loss of around 1% (the Dow was a bit stronger).

Away from stocks was where the real action was. The euro was hit for 1.5% versus the dollar. The Swiss franc was extraordinarily volatile but spent most of the day 15% higher — note: this is a major currency, not a $2 stock — versus the dollar. As for the bond market, it was higher, and of course we are going to see even more negative rates in Switzerland’s and Germany’s bond markets, so the lunacy there continues and will, I expect, until it too teaches everyone the lesson that no central planning is bigger than the market when Mr. Market decides it is time to change his mind about where he wants prices to trade.

Is Gold Finally Ready to Floor It?

Oil lost 1%, while gold spiked almost 3% and from a technical standpoint has broken a serious downtrend line and managed to trade back to and slightly over its 200-day moving average. Exactly what technical factors are really going to matter to gold in the short run, given its explosive move in every currency, I can’t say, but I think the world has changed and we are not going to visit the sub-$1,200 price level. I guess the big question is when the Goldman Sachs of the world throw in the towel on the idea that whatever the Fed is going to do it will categorically be bad for gold.

For the last couple of years the gold market has been hostage to whatever folks’ whims were about the U.S. economy, the Fed, or the dollar. However, it is a much bigger world than that, and I believe the important variables have shifted, though I don’t know exactly what the keys will be. The most important thing to understand, in my opinion, is that the bull market in gold has resumed. That means it is going higher, and that is all anyone really needs to know.

In summary, folks are going to need to prepare for the chaos and volatility that are going to be with us prospectively.

Positions in stocks mentioned: none.

Talk of deflation was overheard on the Street as a few analysts quoted by the news wires mentioned the D-word. One reason for the recent equity market weakness is the uncertainty among investors as to whether lower oil prices are ultimately beneficial or detrimental for the economy. In one camp are those who maintain that lower oil prices will boost consumption; on the other side are those who claim that plummeting energy prices can only lead to outright deflation. Because neither side has a decisive majority right now, equities are caught in the imbalance of opinion which explains much of the recent volatility.

Adding to the uncertainty this week was the latest research note from Goldman Sachs. Goldman’s chief commodities analyst Jeffrey Currie wrote: “To keep all capital sidelined and curtail investment in shale until the market has re-balanced, we believe prices need to stay lower for longer.” Goldman made a high-profile call for $40/barrel oil before the bottom has been seen in the crude market.

Both sides of the argument have merit, but history shows that there comes a point at which falling oil prices eventually exert a negative on equities. The two examples that come to mind are the 2008 oil collapse, which increased downside volatility for the credit crisis. Before that, the 1998 plunge, which took crude prices below $10/barrel, aggravated the Russian Ruble crisis and LTCM hedge fund collapse of that year and had a decidedly negative spillover impact on stock prices for a while.

I would also point out that in the Kress cycle forecast for 2015 the 6-year “echo” suggests that the first few weeks of the New Year could be negative for stocks. The Kress cycle echoes tend to be fairly accurate in warning of broad periods of above-average volatility and of the years which most closely align with 2015 in terms of the key Kress cycles, January was shown to be a particularly vulnerable month for selling pressure.

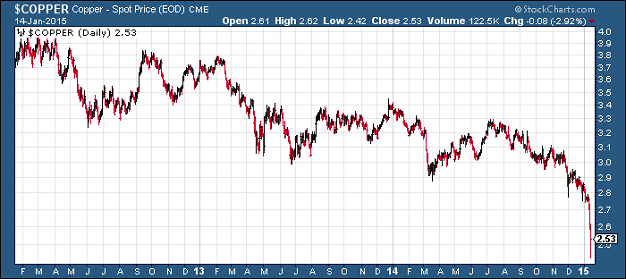

Meanwhile commodities continue to take center stage as concerns mount that the weakness in the energy market may spill over into other areas of the financial system and the economy at large. On Wednesday, Citigroup cut its iron ore and coal forecasts due to supply costs and signaled that the oil price crash is feeding into other commodity markets. An even bigger sign that that weakness is having an impact on global demand can be seen in the chart for copper futures. Copper is a widely watched gauge of global economic strength and the following graph suggests diminishing demand.

One of the major culprits for the weakness in oil and other commodities is the austerity policies in Greece and other euro zone countries, which is coming home to roost right now. While the U.S. Federal Reserve responded to the unmitigated demand for money during the critical years 2009-2012, other countries chose to ignore the need for increased reserves and liquidity and instead initiated an ill-timed tight money policy. Fast-forward to 2015 and while the U.S. finds itself the envy of the world in terms of its domestic economy, other nations are showing major signs of weakness with some verging on recession.

The risk is that the commodities bear market continues exerting a negative influence on economies in Europe and Asia with weakness eventually being exported to the U.S. This is what happened, on a temporary scale at least, in 1998. While we’re a long way from the danger zone, there are preliminary signs that some of that weakness is already showing up. The latest U.S. retail sales numbers, for instance, showed a 0.9 percent drop for December in what should by all accounts have been a positive month. Electronic and clothing retailers were among the nine of the 13 leading categories that showed a decline in sales as Americans chose not to spend the extra money from gasoline price savings.

A better reflection of what the average consumer is doing with his money is visible in the New Economy Index (NEI). NEI is a basket average of several stocks within the consumer retail and business sectors. For years it has provided an accurate real-time picture of the overall state of the U.S. retail economy. Here’s what the NEI looks like right now.

NEI reached an all-time high last January and has spent the past year consolidating its gains since 2009 by tracing out a lateral range. The NEI chart looks decent but could certainly use some improvement. My interpretation of the NEI pattern is that while consumers have been spending at moderate levels, they haven’t completely “let loose” with those frenetic spending binges that have always characterized strong economies of the past.

Although joblessness isn’t a major problem like it was in years past – the latest jobs report showed a surge of 321,000 new jobs in November – consumers are apparently concerned enough about keeping their jobs that they haven’t accelerated their spending. It will be interesting to see how they respond to the continued weakness in the commodities market.

About Clif Droke

Clif Droke is a recognized authority on moving averages and internal momentum. He is the editor of the Momentum Strategies Report and Gold & Silver Stock Report newsletters, published since 1997. He has also authored numerous books covering the fields of economics and financial market analysis. His latest book is “Mastering Moving Averages.” For more information visit www.clifdroke.com

(1) Crescent Point Energy Corp (TSE:CPG.CA) — 10.2% YIELD

Crescent Point Energy is an oil and gas exploration, development and production company with assets focused in properties comprised of crude oil and natural gas reserves located in Canada and the United States. Co. is engaged in acquiring, developing and holding interests in petroleum and natural gas properties and assets related thereto through a general partnership and wholly owned subsidiaries.

![]()

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair