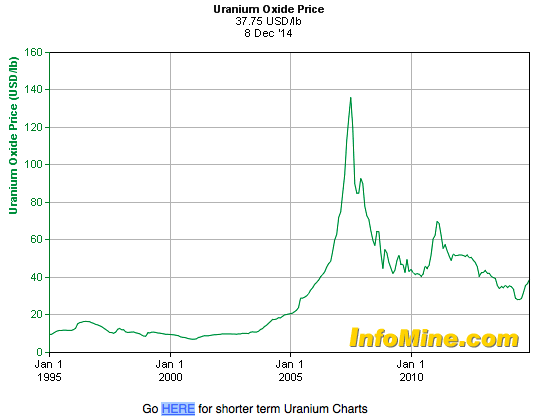

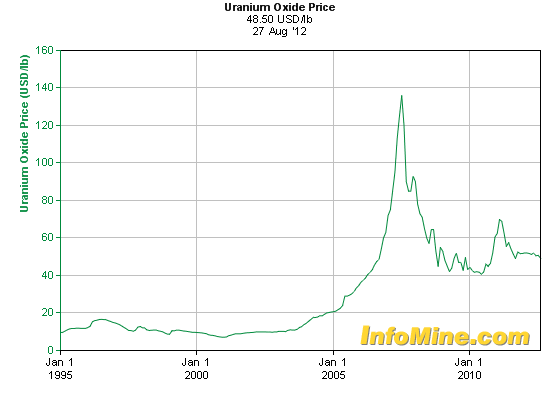

The Mining Report: After the governor of Japan’s Kagoshima Prefecture approved the restart of two reactors at the Sendai Nuclear Power Plant, the daily spot price of uranium jumped $1.40/pound ($1.40/lb) to $39.25/lb. How do you assess this change going forward?

Rob Chang: The restart news is very positive, although it is happening at a slower pace than we had originally expected. The Japanese utilities are well organized. They are asking to restart the two reactors that are most likely to gain approval. That said, the jump in the spot price reflects the news out of Japan. However, we think that the price change is more a matter of what is going on behind the scenes. Two sellers have stopped selling. A number of utilities have increased their buying. One large utility recently purchased 10 million pounds (10 Mlb).

TMR: Who stopped selling and who’s buying?

RC: Uranium spot prices are not traded on the public market. These types of transactions are contracted between producers and utilities with the occasional investor or trading house in between. The uranium spot price is not actively speculated upon like gold or copper, nor can the general public get in on the action. The movement in uranium spot pricing is generally based on transactions by entities that are well versed in the intricacies of that market. They probably would not be trading based on just the Japanese news, especially because most of us were already expecting the reactors to restart.

TMR: Do you think the uranium equities will echo the spot price move?

RC: Absolutely. Uranium prices have been going up since June, even as uranium equities recently hit a 52-week low. As the uranium spot price moves higher, the dichotomy between the two will increase and we believe uranium equities will need to play catch up.

TMR: Are the utilities buying long-term uranium contracts?

RC: I have not heard about many long-term transactions. But the long-term price made a notable upward move of $4/lb to $49/lb. With the uranium spot price nudging the long-term price along, we expect term prices to be pushed higher as the spot price increases.

TMR: What juniors do you like in the uranium space now?

RC: That depends on what you count as a junior. How about anything smaller than Cameco Corp. (CCO:TSX; CCJ:NYSE)?

On the exploration side, Cantor Fitzgerald likes Fission Uranium Corp. (FCU:TSX)and Denison Mines Corp. (DML:TSX; DNN:NYSE.MKT). Fission’s Patterson Lake South is emerging as a world-class asset. We believe Fission will eventually control more than 100 Mlb of high-grade U3O8. It is expected to put out its first resource estimate by the end of the year. Some of the best uranium drill holes ever reported are on Fission’s property, and that is pretty impressive.

On the exploration side, Cantor Fitzgerald likes Fission Uranium Corp. (FCU:TSX)and Denison Mines Corp. (DML:TSX; DNN:NYSE.MKT). Fission’s Patterson Lake South is emerging as a world-class asset. We believe Fission will eventually control more than 100 Mlb of high-grade U3O8. It is expected to put out its first resource estimate by the end of the year. Some of the best uranium drill holes ever reported are on Fission’s property, and that is pretty impressive.

We are very positive on Denison Mines. Denison effectively owns everything of significance in the Athabasca Basin that is not already controlled by Cameco or Fission. Anyone looking to gain a foothold in the Athabasca Basin, be it a Rio Tinto Plc (RIO:NYSE; RIO:ASX; RIO:LSE; RTPPF:OTCPK) or a Vale S.A. (VALE:NYSE), is going to have to deal with Denison, Fission and Cameco. And if Cameco moves to expand its existing holdings, it will have to deal with Denison and Fission. On top of that, Denison has an interest in the McClean Lake mill, which is very important because it has cash flow from processing Cameco’s Cigar Lake feed. Importantly, the mill gives Denison a piece of a strategic asset, processing material from one of the most important mines in the world.

In the U.S.-based space, Ur-Energy Inc. (URE:TSX; URG:NYSE.MKT) is reporting good news on completing contract sales. This company is near the top of our list because it is producing at the low end of the cost curve—in the low $20s/lb. It is enjoying incredible success mining its Lost Creek project, producing uranium at a much higher rate than expected. Plus, Ur-Energy can scale up as prices rise. We recommend Ur-Energy for its low-cost and excellent production profile to date.

TMR: Ur-Energy uses the in situ recovery (ISR) method at Lost Creek. How does that reduce the cost of production?

RC: If the ore is amenable, ISR is the lowest cost recovery format. It does not involve as much earth moving as the conventional open-pit and underground mining methods. The engineers dig an injection well and, farther away, an extraction well. They pump a chemical solution into the injection well. In Kazakhstan, the solution is acid-based; in Wyoming, it is a sodium bicarbonate mix—basically water mixed with baking soda. The solutions dissolve the uranium underground. The liquid filled with dissolved metal is pumped up from the extraction well. This uranium mining method is less intrusive and more environmentally friendly than conventional mining. And it is much less expensive on the front-end capital expenditure (capex) side.

RC: If the ore is amenable, ISR is the lowest cost recovery format. It does not involve as much earth moving as the conventional open-pit and underground mining methods. The engineers dig an injection well and, farther away, an extraction well. They pump a chemical solution into the injection well. In Kazakhstan, the solution is acid-based; in Wyoming, it is a sodium bicarbonate mix—basically water mixed with baking soda. The solutions dissolve the uranium underground. The liquid filled with dissolved metal is pumped up from the extraction well. This uranium mining method is less intrusive and more environmentally friendly than conventional mining. And it is much less expensive on the front-end capital expenditure (capex) side.

TMR: Other juniors?

RC: Uranerz Energy Corp. (URZ:TSX; URZ:NYSE.MKT) just started production and sales. We look forward to seeing its cost performance. But as we have been pointing out for quite a long time, there is an unavoidable supply deficit approaching. Uranium producers stand to benefit most. Uranerz is well positioned for earning long-term profits.

TMR: Uranerz’s shares were steady at $1.50 during 2013 and spiked to over $2 last March. They then fell to almost $1, and shot up to $1.50 in the last couple of weeks. What was the cause of that spike about a year ago up above $2? Are we looking to pass the newest upsurge?

RC: Last March, there was a lot of positive sentiment behind uranium. The prevailing analysis was that uranium was set to move this year because of Japanese restarts. Unfortunately, that did not come to pass. There were a lot of delays with the Japanese restarts, and the uranium sentiment turned sour. At that time, Uranerz was receiving final approval and moving to go into production. Passing through that gateway, plus the positive sentiment toward uranium, contributed to the big rise in March. And in early November Uranerz jumped again, due to the re-emergence of positive sentiment on uranium and the fact that Uranerz is now selling yellowcake. Basically, the same thing is happening with the other producers I mentioned.

We also really like Energy Fuels Inc. (EFR:TSX; EFRFF:OTCQX; UUUU:NYSE.MKT). Energy Fuels is holding several mines on standby. It can start two or three of the mines within six months to a year, and within two or three years of a production decision, it can launch an additional half dozen mines. Production scalability is very high. Energy Fuels owns the only conventional mill for processing uranium in the U.S., and that gives the firm a great strategic advantage. Right now, the mill is on standby because of the previous low-price environment. But as the uranium spot price blasts through $44/lb, a nicely leveraged Energy Fuels will soon be able to pump out profits.

Ed Note: go HERE for more Uranium price charts

TMR: How important is it for a company to control a mill?

RC: Ore extracted by open-pit or underground mining needs to be processed by a mill. A mill is a strategic asset—it is very important because any miner that does not have a mill will have to pay Energy Fuels to use its mill. At current uranium prices, conventional mining is not very economic. But at higher prices, there will be a large demand for milling. There are “mom-and-pop” uranium operations throughout the U.S. that will have to pay Energy Fuels to process their yellowcake.

TRM: What other companies do you like in the U.S. for uranium?

RC: Uranium Energy Corp. (UEC:NYSE.MKT) is similar to Energy Fuels because it’s 100% unhedged and fully exposed to the spot market. Once its sales are up and running again, its share prices will sweeten. We are big on the U.S. producers primarily because the U.S. is the No. 1 consumer of uranium at around 55 Mlb/year. But the country only produces around 3–5 Mlb annually. All of these producers stand to benefit from premiums.

TMR: How did the stocks of the companies that you have mentioned weather the downturn in uranium?

RC: For most of the past year, they were beaten up. Relative to the recent movement in the price of uranium, many stocks have traveled in a different direction, which does not make sense, but it does make them cheap. That said, the firms I am interested in are starting to recover; some are showing notable strength.

TMR: Is now a good time to buy uranium stocks at bargain basement prices?

RC: The bargain basement pricing may have passed. When the uranium spot price was $28/lb and leading the uranium equities downward, we saw a lot of 52-week lows. I doubt that we will see uranium down to $28/lb again. I doubt that it will fall below $35/lb as demand increases.

TMR: What companies are you watching in other metal sectors?

RC: We follow a range of precious metal names. We are particularly excited about Pershing Gold Corp. (PGLC:OTCBB). It is currently listed on the OTC Bulletin Board, but it does have designs to uplist onto a larger exchange. We’re very excited about Pershing because it has a property, Relief Canyon, located in Nevada near Coeur Mining Inc.’s (CDM:TSX; CDE:NYSE) Rochester mine. Relief Canyon is a past-producing mine with an open pit. Most important, it has a mill that was barely used on site. It was shut down because the previous management team ran out of money. The upshot is that Pershing has a relatively new mill on the site of a past-producing pit in a well-known precious metals, primarily gold, jurisdiction with some silver.

We assess that Pershing can get up and running at a very low cost. Money managers often ask us to suggest cheap investments that can produce in the short term. Pershing Gold fits the bill because it will only cost, say, $20 or 30 million of capex to ramp up into production. The asset is fully permitted. In addition, Pershing has had excellent exploration success that is encountering grades that are three to five times greater than what is listed on the official NI 43-101 resource for the project.

TMR: Is there a cost of production below which it doesn’t make sense for Pershing? How low can the price of gold go before Pershing’s Nevada project would not be viable?

RC: We estimate the all-in cost at $850–900/ounce, which is very low. The reason is this is run-of-mine material. You basically take it out of the ground, stick it right on the leach pad and start leaching. It does not cost much to take it out of the ground because much of the overburden is already stripped. Plus, it does not need to be crushed, because it is run-of-mine material.

Another selling point for Pershing Gold is its excellent management. Executive Chairman and CEO Stephen Alfers is the gentleman responsible for discovering Long Canyon, which was sold to Fronteer Gold and later on to Newmont Mining Corp. (NEM:NYSE). He later became the head of U.S. operations at Franco-Nevada Corp. (FNV:TSX; FNV:NYSE). He saw the opportunity at Pershing and decided to leave Franco-Nevada to become Pershing’s CEO. That is a very strong vote of confidence in the solid project.

TMR: Pershing’s stock was at $0.40 in April, and now it is down to $0.28. Is there a reason for that decline?

RC: Pershing Gold has outperformed gold over the past month. Over the past three months, it’s been in line with the gold price movement. As an under-the-radar, near-term gold producer, we think Pershing Gold is quite valuable.

TMR: Are there any other precious metal companies on your radar scope?

RC: Paramount Gold and Silver Corp. (PZG:NYSE.MKT; PZG:TSX) has a 100-million tonne gold and silver resource that is located right beside Coeur Mining’s Palmarejo operation in Mexico. The Palmarejo operation is a significant part of Coeur Mining’s total value. Palmarejo is on its last legs production-wise. Coeur owns a gigantic mill on site, and it has announced a deal with Franco-Nevada to develop a nearby mine called Guadalupe and mill high-grade material from it. Franco-Nevada has a royalty on all of the ore coming out of Guadalupe.

Now, here is the kicker: Paramount’s deposits are located within a few kilometers of the Palmarejo operation. Based on the size of the mill at Palmarejo, Coeur Mining likely needs more material than it is expected to get from Guadalupe. The acquisition of Paramount would give Coeur access to mill feed that is free of the Franco-Nevada royalty encumbering the gold and silver produced from Guadalupe. It makes a lot of sense for Coeur Mining to buy Paramount Gold and run its ore through the mill. That way, it can take more of the revenue. This is an obvious takeout story.

TMR: Thanks for the conversation, Rob.

RC: A pleasure talking to you, Peter.

Cantor Fitzgerald Canada’s Senior Analyst and Head of Metals and Mining Rob Chang has covered the metals and mining space for over eight years for the sellside and the buyside. Prior to Cantor, Chang served on the equity research teams at Versant Partners, Octagon Capital and BMO Capital Markets. His buyside experience includes managing $3 billion in assets as a director of research/portfolio manager at Middlefield Capital, where his primary resource portfolio outperformed its direct peer and benchmark by over 28% and 18%, respectively. He was also on a five-person multistrategy hedge fund team, where he specialized in equity and derivative investments. He completed his Master of Business Administration from the University of Toronto’s Rotman School of Management.

Read what other experts are saying about:

Want to read more Mining Report articles like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see recent interviews with industry analysts and commentators, visit The Mining Report home page.

Related Articles

- Fracking, Uranium and Solar, Oh My!: Growth and Innovation in 2013

- Robert Baylis: A Taste for Tungsten—Finding the Sweet Spot for Investors

- Doug Loud and Jeff Mosseri Say Gold Will Regain Its Shine in 2015

DISCLOSURE:

1) Peter Byrne conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report, The Life Sciences Report and The Mining Report, and provides services to Streetwise Reports as an independent contractor. He owns, or his family owns, shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: Fission Uranium Corp., Ur-Energy Inc., Uranerz Energy Corp., Energy Fuels Inc. and Pershing Gold Corp. Franco-Nevada Corp. is not affiliated with Streetwise Reports. The companies mentioned in this interview were not involved in any aspect of the interview preparation or post-interview editing so the expert could speak independently about the sector. Streetwise Reports does not accept stock in exchange for its services.

3) Rob Chang: I own, or my family owns, shares of the following companies mentioned in this interview: Fission Uranium Corp. and Denison Mines Corp. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: Fission Uranium Corp., Ur-Energy Inc., Paramount Gold and Silver Corp., Pershing Cold Corp., Uranium Energy Corp., Energy Fuels Inc. and Uranerz Energy Corp. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I determined and had final say over which companies would be included in the interview based on my research, understanding of the sector and interview theme. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.

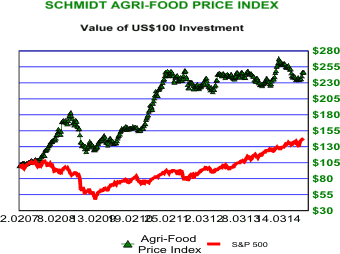

Many investors have not been aware of the exceptional long-term returns in Agri-Equities because of a general misunderstanding of Agri-Commodities, and of commodities in general. As the Agri-Food Price Index, which measures the price trend of 17 Agri-Commodities, portrays in chart to right, the price of a portfolio of Agri-Commodities has not collapsed as many forecast this time last year. Rather, this index hit an last all time high end of March. Reason for that is as the Chinese economy has grown larger than that of the U.S. the incomes of consumers in China have risen. Those richer individuals like to eat better, every day. The propensity of China to buy soybeans, corn, sorghum, etc. far exceeds that for over priced electronic toys masquerading as cell phones.

Many investors have not been aware of the exceptional long-term returns in Agri-Equities because of a general misunderstanding of Agri-Commodities, and of commodities in general. As the Agri-Food Price Index, which measures the price trend of 17 Agri-Commodities, portrays in chart to right, the price of a portfolio of Agri-Commodities has not collapsed as many forecast this time last year. Rather, this index hit an last all time high end of March. Reason for that is as the Chinese economy has grown larger than that of the U.S. the incomes of consumers in China have risen. Those richer individuals like to eat better, every day. The propensity of China to buy soybeans, corn, sorghum, etc. far exceeds that for over priced electronic toys masquerading as cell phones.

You see, back in 1932, three years after the Crash of ’29, 17 countries in Europe started to default on their sovereign debt. Investors yanked their money out of Europe and sent it, guess where?

You see, back in 1932, three years after the Crash of ’29, 17 countries in Europe started to default on their sovereign debt. Investors yanked their money out of Europe and sent it, guess where?