Stocks & Equities

For the fifth week in a row, equity market investor sentiment remains neutral. Over the past 3 weeks, the market erased the losses suffered over the prior 4 weeks and just like that we are at new highs!! Funny thing, the indicators never really unwound. Seven week’s ago The Sentimeter was extremely optimistic and just like that with everyone all in, the market struggles. We should have gotten more selling, but buyers are so conditioned to buy the dip knowing that Ben Bernanke has their backs, and as if on cue, Ben answered the bell this week. However, strong markets usually don’t bounce too high or go too far when the indicators are neutral. So we are still expecting a range bound, choppy market. The way to make money in such markets is to buy the dips and sell the rips. The SP500 has moved about 7.5% in 13 trading days. That’s .57% gain per trading day or 11.5% per trading month or 138% gain trading year. Nothing abnormal here (sic).

See the Equity Market Investor Sentimeter below, which is our most comprehensive sentiment indicator. This indicator is constructed from 10 different data series including opinion data (i.e., how do you feel about the market?) as well as money flow data (i.e., where is the money going?). This is the current state of equity market investor sentiment.

Over the past year, sell offs have been met with Federal Reserve intervention — namely QE3 and QE4. These interventions short circuited the sell offs. I believe this is not healthy bull market action, and at some point, these distortions will be corrected. At this point, it is difficult to know if the Fed has something else in its bag of tricks and what will it take to use it, but rest assured they will do whatever they can to prop up the markets. Last week, all it took was jawboning by Ben Bernanke. A neutral reading in the indicator implies that there is little predictive edge to the market action.

Is it a revolt?” Louis XVI asked the Duke de La Rochefoucauld.

“No, sire, it is a revolution.”

We are already at the Ides of July. More than half of the year is already behind us.

Friday, markets were flat. Neither gold nor stocks did anything worth reporting.

July 21 is statistically the hottest day of the year in the Northern Hemisphere. And it’s already smokin’ hot in Baltimore. The forecast calls for 98 degrees Fahrenheit today. More than 100 later in the week. We’re glad we’re not there. We lived through 48 summers in Baltimore, more than enough for any man.

Sometimes, in the summer months, the TV meteorologists might as well go on vacation. Day after day, the same forecast: hazy, hot, humid… with a chance of afternoon thundershowers. It can go on like that for weeks. Or even months.

It’s hot here in Normandy too. But every hell hath its own heat. It’s Normandy’s version of hot, not Maryland’s version. Yesterday, the temperature must have gotten up into the low 80s here.

When the weather is nice in Normandy, it’s very nice. But sometimes, a whole year can go by with only a few weeks of really nice weather. The good weather here began only very recently. A couple of weeks ago, we were wearing sweaters and jackets and lighting fires in fireplaces. Now the days are sunny and warm. The nights are cool and clear.

It’s finally summer in France… the way it oughta be.

France’s Minsky Moment

Yesterday was Bastille Day.

The French celebrated with fireworks, as usual. On more than one occasion over the years, we asked what they were celebrating. Never did we get a good answer.

“It was the beginning of the revolution,” one said. “But I don’t know why we would celebrate that.”

“It marks the beginning of the French Republic and the establishment of the Rights of Man,” said another, grandly.

And yes, the Republic and the proclamation of the Rights of Man did happen after the Bastille was stormed. But neither depended on it. The Bastille was irrelevant. It held only seven prisoners. Two counterfeiters. Two mental cases. One pervert. It would have held another famous pervert, the Marquis de Sade, but he had been transferred 10 days before.

But in the summertime, things can get hot…

Temperatures had begun to rise in France long before the Bastille was taken.

France had enjoyed a fair period of growth and stability under the Louis. Modern France was put together under them.

By the 18th century, the king was supposed to have a divine right to rule. He was supposed to be an “absolute” monarch. But each Louis found that – to hold onto power – he had to give up a little bit more of it… a little privilege here and there… a right to do this or that… a sinecure… a pension.

Over time, as Professor Mancur Olson explained, groups get together to push programs that benefit them – at the expense of the general welfare. They hire lobbyists. They solicit favors. They get monopolies and set up trade barriers. He did not say so, but they become what we call “zombies.”

“Stability causes instability,” was how Hyman Minsky described it. The accumulation of special favors weakened the authority of the king.

The Power of Talk

And God didn’t seem to help him much.

The clergy had its own lands… and its own government.

The aristocrats insisted on making their own rules too and, importantly, on having the right to approve the taxes Louis laid upon them.

And then, even the Third Estate – the common people – wanted its privileges too.

By the time the 16th Louis came along, the tinder was dry. And a warm wind of revolutionary ideas blew through Paris. In the Palais-Royal, for example, a public meeting continued almost around the clock. All of sudden, talk seemed to matter.

You could talk to each other about how to improve the world. You could talk about giving more food to the poor, for example. You could even set up an assembly of the people’s representatives at which they could talk too.

You could talk about liberty… about justice… And why not about redistributing the lands of the church? And why not a zombie uprising… so everybody got what he wanted?

If you could say something… you could do it, too.

In the summer of 1789, sparks flew. Soon, the dry tinder was lit. Crowds began looting stores and attacking the king’s military bases. Muskets were seized. Revolutionary groups were formed. The proletariat was hot now… and it saw no limit to its power or its prospects. Surely, it could pass laws too… and make itself rich.

Even many of Louis’ soldiers were talking about it… and taking the proles’ side.

Then, on July 14, a mob of about 1,000 people attacked the Bastille. Nearby troops did nothing to aid the small garrison of the fortress. The mob routed the defenders and murdered the Bastille’s governor, Bernard-René de Launay. De Launay’s head was sawed off and put upon a pike that was paraded around Paris.

Louis XVI was executed, by guillotine, on January 21, 1793.

Regards,

Bill

Market Insight:

If This Is a New Bull Market,

Why Are Stocks So Expensive?

by Chris Hunter

Cliff Asness, a former Goldman Sachs “quant” and co-founder of hedge fund AQR Capital Management, has calculated that the prospective returns from a typical stock and bond portfolio (with 60% in stocks and 40% in bonds) is 2.4% per year – the worst predicted return in 112 years.

The problem is stocks and bonds are expensive. And money is made in the markets “in the buying.” In other words, buying low and selling high… not the other way around.

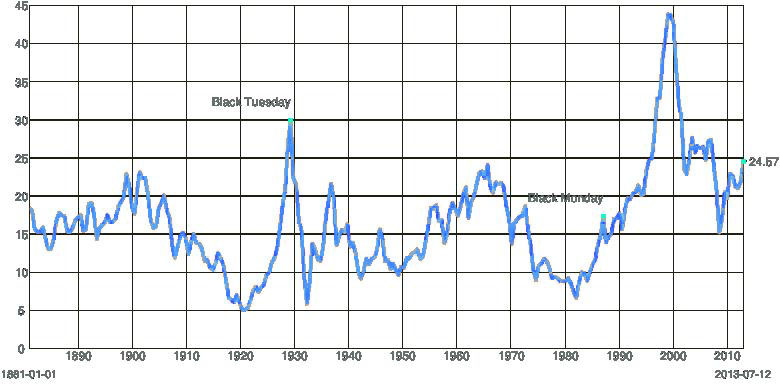

One way to measure how expensive stocks are is by using the cyclically adjusted price to earnings ratio, or CAPE. Unlike the normal P/E ratio, which looks at just 12 months’ worth of earnings or forecast earnings, the CAPE compares share prices to average inflation-adjusted earnings over the previous 10 years.

This smoothes out any anomalies created by unusually high or unusually low earnings over a 12-month period. And it has been a good guide to long-run returns.

At today’s CAPE of 24.6, history suggests returns of less than 1% over the next decade for buying and holding the S&P 500.

This is a problem for the bull case for US stocks. Because it suggests stocks have not yet reached their final secular bear market bottom – where valuation levels are low enough to give above-average returns.

This usually happens with the CAPE in single digits… not far above the historic average, where it sits today.

History suggests we’ll see one last big fall in stocks before the next secular bull begins.

Chris Hunter

Investment Director

Bonner & Partners Family Office

Bernanke Reverses Course

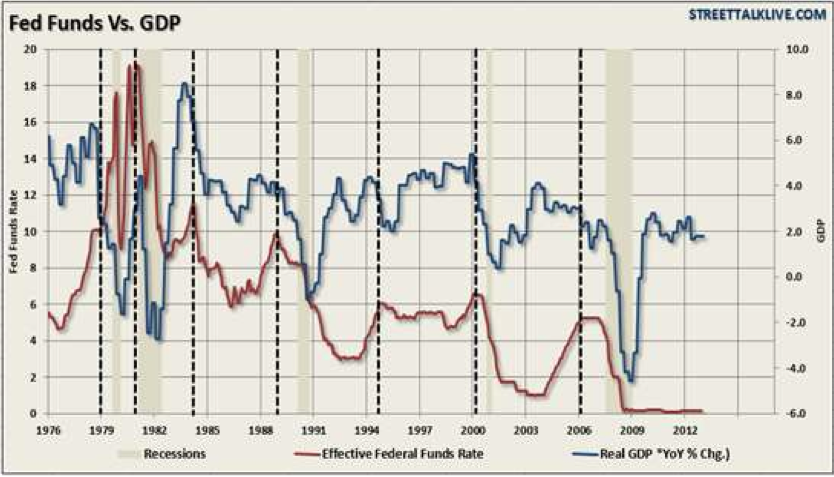

At the beginning of June we began discussing the approach of an initial “sell” signal. I stated at that time that the onset of such a signal would be a “warning” that you should begin paying much closer attention to what is happening inside of your portfolio. The selloff that began in late May coincided with mounting expectations that the Federal Reserve would begin reducing their monetary interventions later this summer and cease the program entirely by 2014.

As I discussed in “The Diminishing Effects Of QE Programs” the economy remains far too weak for the Federal Reserve to begin reducing support for the financial markets anytime soon. I stated:

“…the real issue is that IF the recent negative trends in consumption, employment and inflationary pressures do not start to reverse it is highly likely that the Fed will not be able to extract the monetary supports anytime soon. The recent increases in interest rates, combined with still very weak wage growth, higher costs of living and still elevated unemployment is likely to keep the Fed engaged for the foreseeable future as any attempt to remove its ‘invisible hand’ is likely to result in unexpected instability in the financial markets and economy.”

Consequently, the “trial ‘tapering’ balloon” lofted by the Federal Reserve after the last FOMC fell quickly to earth as stock prices sagged, which began to erode consumer confidence, and interest rates spiked sharply higher putting economic growth in danger. Those realties pushed the Federal Reserve to back pedal on their “tapering” stance as Ben Bernanke clearly stated that:

“I think you can only conclude that highly accommodative monetary policy for the foreseeable future is what’s needed in the U.S. economy. And I guess the final thing I would say in terms of risks of course is that we have seen some tightening of financial conditions, and that if, as I’ve said and as I said in my press conference and other places that if financial conditions were to tighten to the extent that they jeopardize the achievement of our inflation and employment objectives then we would have to push back against that.”

There was a clear confirmation by the Fed to market participants that the Federal Reserve will not take away accommodation because they cannot afford to let the markets “tighten.” Rising interest rates and falling asset markets are one thing and put the economy at risk. However, the lack of inflation is also a real concern.

As the chart below shows, every time the Fed has embarked on such a program to increase borrowing costs it has let do an economic recession or worse.

……read the 10 page report HERE

- Markets in Asia were higher in overnight trading. The Hong Kong Hang Seng rose 0.1% and the Shanghai Composite advanced 1.0%. European markets are higher this morning with the exception of Spain, currently down 0.5%. In the United States, futures point to a positive open.

- China’s annual GDP growth rate slowed to 7.5% in the second quarter from 7.7% in Q1, matching consensus estimates. That puts the average 2013 growth rate so far at 7.6%, just above the government’s official growth target of 7.5%.

- Chinese industrial production rose at an 8.9% annual rate in June, below consensus estimates for a 9.1% advance. Year-to-date fixed asset investment growth stood at 20.1% in June, just below predictions for 20.2% growth. Retail sales rose 13.3% annualized last month, above expectations for 12.9% growth.

- Spanish opposition leaders turned up the pressure on Prime Minister Mariano Rajoy to resign Sunday after Spanish newspaper El Mundo published text messages linking Rajoy to a slush fund used to pay off politicians. Luis Barcenas, the former Popular Party treasurer on the other end of the text messages, told the paper last week that the party has long been financed illegally.

- The main focus for markets this week will be Federal Reserve Chairman Ben Bernanke’s semi-annual Humphrey Hawkins testimony before Congress Wednesday on the U.S. economy and monetary policy. Market participants will be paying close attention to any words from Bernanke that build on his comments last week regarding the recent rise in bond yields and attendant tightening of financial conditions.

- At 8 AM ET, Federal Reserve Governor Daniel Tarullo will give a speech on banking regulation in Washington. Although the speech is unlikely to address current monetary policy, market participants have been giving increased attention to Fed appearances in recent weeks as bond markets have been roiled by the prospect that the central bank will begin to taper bond purchases later this year.

- The advance retail sales report for June is due out in the United States at 8:30 AM. Economists predict sales rose 0.7% in June after advancing 0.6% in May. Excluding autos, sales are expected to post gains of 0.4% after rising 0.3% in May.

- The results of the New York Fed’s July Empire State Manufacturing Survey are also out at 8:30 AM. Economists predict the headline index slipped to 5 in July from 7.84 in June, suggesting a continued but slowing expansion in regional manufacturing over the past month.

- Rounding out the U.S. data is the May business inventories release, due out at 10 AM. Economists predict inventories rose 0.2% in May after posting a 0.3% gain in April. Follow all of the data releases LIVE on Business Insider >

- George Zimmerman was found not guilty of manslaughter in the Trayvon Martin case over the weekend. President Barack Obama released a statement calling the death of Martin a tragedy, and the Department of Justice also made its own statement leaving the door open to a civil-rights case against Zimmerman.

Dow Jones surges to a new all time closing high of 15,460.92 as many market commentators literally never learn! And there is a reason for this.

Bull markets do one thing, and one thing only, they resolve to NEW bull market highs, as that is what ultimately defines what a bull market is, and so the market that I have traded for near 30 years, the DJIA stock index has once more resolved to a new bull market ALL Time High.

My expectations at the time of the May rally were to reduce stock market exposure ahead of a correction to once more accumulate into – 22 May 2013 – Dow, FTSE, Stock Market Panic, Euphoria, Irrational Rally Continues, What I am Doing

Ed Note: More analysis and charts like this interesting one below HERE

……read more HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair