In the middle of crisis are the seeds of both danger and opportunity; think precious metals.

In the middle of crisis are the seeds of both danger and opportunity; think precious metals.

Creating Value in the Stock Market

Let’s address one of the most fundamental inputs in this situation: stock prices. Company valuations and their stock prices are a function of several inputs; the most important of which are earnings growth expectations and dividends.

One way to look at the price of a stock is to look at the present value of the expected future stream of dividends the company is supposed to pay out. In other words, when you get income from this company in the future, what’s that worth to you now?

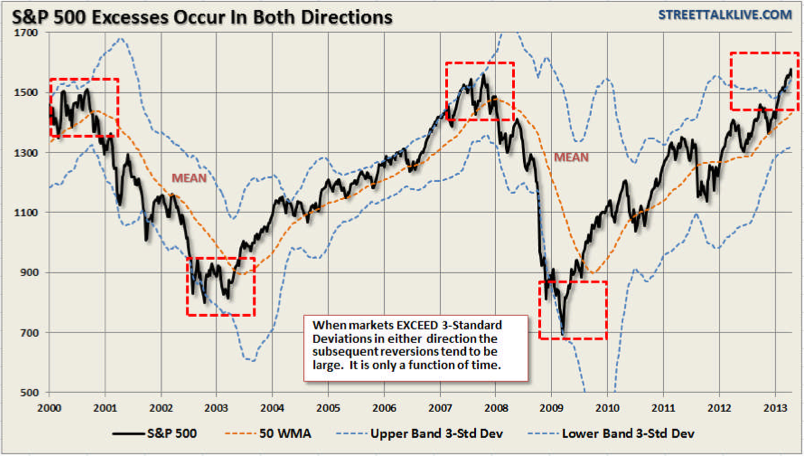

You don’t have to apply any modeling to get to your valuation; the market basically does that for you by arriving at a consensus price that incorporates the discount model math.

Most companies that pay solid, steady dividends don’t see their stock price fluctuate too much because they are yield-based investments more than go-go growth investments.

Prices of high-yielding stocks have risen and been strong because investors starved for yield in the fixed income markets have turned to these equities for the income they deliver. And growth investors that were burned in the 2008 meltdown have sought out yields for safety and steady growth.

That’s making income investments very popular across all investor classes.

Dividends come out of earnings, so earnings are important. But for stocks that don’t pay a dividend, earnings (or in the case of crazy Internet-type stocks, would-be earnings) are everything.

Earnings: Good News vs. Bad News

Steady-state earnings don’t do much for stock prices. Earnings growth is the Holy Grail. The good news is that stock prices have been rising, justifiably, on better and better earnings.

The bad news is, those earnings, upon a deeper look, aren’t sustainable if economic growth doesn’t pick up.

Since 2009, earnings on stocks in the S&P 500 have risen collectively some 200%.

Most of those higher net earnings have resulted from cost-cutting, layoffs, productivity increases, favorable tax carry-forwards, refinancing old debt with cheaper low-interest loans, a weak dollar, and accounting gymnastics.

The bad news is over the same period top-line revenues have grown only about 10%.

In other words, in spite of deathly slow domestic growth in the U.S. and slow global growth, American corporations have benefited by leaning themselves out, globalizing their sales to where the growth is, and enjoying a positive currency translation when they account for overseas earnings in terms of cheap dollars.

Central Bank Steroids

Besides inherent valuation measures, stocks are subject to supply and demand equations. If there are more buyers than sellers on any given day, stock prices will rise.

The Federal Reserve and central banks around the world have been providing an extraordinary amount of buying power to short-term investors by flooding banking systems with trillions of dollars, as well as keeping interest rates at rock bottom levels, which adds to investor buying power.

All the stimulus money floating around the world means there’s plenty of money to buy stocks, especially for financial institutions. And when there are more buyers than sellers, stock prices, and this has been happening worldwide, will rise.

So far that’s all been well and good. GDP growth hasn’t had to be the prime mover of stocks. Inherent factors and superficial stimulus have provided the market’s fuel.

But, without strong economic growth, sooner or later, demand alone will prove inadequate in supplying top-line revenue and net earnings growth and stocks could fall.

The Reckoning

The market, which can still be saved hopefully long enough for GDP growth to kick in, and if sidelined investors keep pumping money into new positions, is nonetheless facing another headwind.

Share ownership and investor participation is dwindling in the U.S. as a stagnant economy is reducing the middle-class and their ability to invest in stocks.

According to Federal Reserve data from 2010, while 47.8% of the top 10% of income earning households in America owned stocks directly and 90.1% had retirement accounts averaging $277,000, in middle-income (the 40-60 percentile) households only 11.7% owned stocks directly and 52% had retirement accounts worth an average of only $22,800.

That’s worrisome for the middle-class, the stock market and America.

Entering the 12th Round

The Great Discrepancy has been bridged so far. But, if U.S. domestic growth continues to be lackluster and global growth, which is already slowing, doesn’t pick up robustly it’s unlikely that soaring stocks can keep fighting against what looks like a rope-a-dope opponent.

Is the fight over? By no means. GDP growth can pick up if housing continues to recover, if energy prices keep falling, if manufacturing jobs get repatriated back here, if the Fed stays its easy money course long enough for growth to get to its knees, stand up and start swinging.

Then again, I watched the famous Muhammad Ali-George Foreman fight where Ali took a beating on the ropes from a wildly punching Foreman, until Foreman ran out of gas and Ali outlasted the opponent he called a dope.

That means, don’t be a dope. Ride the rising market but use protective stops to take profits on the way up so you have a sack full of money to buy from the dopes who’ve forgotten that what goes up, must come down, when the big market hits the canvas.

I’ve been keeping an eye on this battle for some time and that’s why I’ve crafted a successful strategy in my DealBook service where I help investors start to read the clues the market offers and find the opportunities those clues reveal.

Because in this kind of market, even when you’re covered on the ropes, you’re not going to win if you can’t see your opportunities for knock-out punches.

Related Articles and News:

- Money Morning:

Are “Wall Street Buyers” Like Blackstone Group Creating Another Housing Bubble? - Money Morning:

What You Absolutely Need to Know About Money (Part Three) - Money Morning:

What You Absolutely Need to Know About “Their Paper Money” - Money Morning:

What Everyone Absolutely Needs to Know About Money

About The Eliott Wave

About The Eliott Wave