Stocks & Equities

After three weeks of waiting, the S&P 500 Index finally joined the Dow in the record books.

Last Thursday, the most widely tracked Index in the United States closed at 1,569.19 – taking out its previous all-time high of 1,565.15, which was hit on October 9, 2007.

The market hitting new records presents an opportunity for reflection. Or as Erik Davidson, Deputy Chief Investment Strategist at Wells Fargo Private Bank, says, “It is a milestone; it does cause you to stop and evaluate where you are and where you come from.”

For example, this chart certainly gives some perspective:

A Gentleman from Wall Street Daily found that chart and presented it in two articles titled:

10 Startling Statistics About the S&P’s Record High (Part 1)

and….

10 Startling Statistics About the S&P’s Record High (Part 2)

Article one begins with:

Stock Stat #1: Talk of a Tired Bull… is Total Bull

So far we’re four-plus years into a bull market. And the S&P 500 has risen more than 130%.

Even though I told you not to before, it’s only natural to assume that such a sustained and significant rally is close to the longest on record. But it’s not.

In fact, this is only the sixth longest bull market since 1929 (the year the market crashed), according to an analysis by Bank of America (BAC).

….for Statistic 2- 10 go to:

10 Startling Statistics About the S&P’s Record High (Part 1)

10 Startling Statistics About the S&P’s Record High (Part 2)

This Week’s Trading Lesson

I have often said that making money trading stocks is simple, but not easy. Once you learn basic technical analysis techniques, have good tools to identify opportunities and gain some experience at identifying good trading opportunities, the actual job of picking stocks is relatively straightforward. Where most traders fail is in the application of a methodology. The simple and undeniable fact is that we are all human, and therefore, we are all blessed with emotion. When money is on the line, our emotional attachment to it can take over our decision making process. (continued below)

…………………………………………………………………………………………………………………………………………………………

Stockscores Market Minutes Video

Before you take any trade, make sure you analyze the stock’s chart on multiple time frames. Watch this week’s Market Minutes video to see how. Plus, Tyler’s regular weekly market analysis. Watch it byclicking here.

…………………………………………………………………………………………………………………………………………………………With that said, I thought it would be helpful to examine the common problem areas that are a result of mental breakdowns. By examining the emotional conduits to decision making, hopefully I can provide some solutions to correct common trading mistakes.

Trading Problem #1 – No Patience on Entry

Anticipating a signal that never comes is common for traders monitoring the market closely and eager to get some money working. For example, a good buying opportunity arises when a stock breaks from an ascending triangle. Jumping in ahead of the breakout is not an ideal situation because the probability of success buying an ascending triangle is not as good as buying a breakout from one.

What causes this mistake? I think a fear of missing out on the maximum amount of profit or the fear of too much risk in buying a stock are the two most common mistakes. Essentially, the two guiding forces of the stock market are at work here; fear and greed.

By buying early, we can realize a greater profit when the stock does breakout since we will have a lower average cost. Or, by buying early we can reduce risk since a breakout followed by a pull back through our stop will result in a smaller loss as we have a lower average cost.

What tends to happen, however, is that the stock does not break out when expected and instead pulls back. This either leads to an unnecessary loss or an opportunity cost of the capital being tied up while other opportunities arise.

The Solution

The simple and obvious solution is to wait for the entry signal, but there are also some things you can do to help yourself stay disciplined. Rather than watch potentially good stocks tick by tick, use an alarm feature to alert you to when they actually make the break. Watching stocks constantly is somewhat hypnotic, and I think the charts can talk you in to making a trade. However, letting the computer watch the stock may help you avoid the stock’s evil trance.

Another good solution is to focus on different thoughts when considering a stock. Don’t think about potential profits, don’t think about minimizing losses. Instead, focus in on the desire to execute high probability trades. It takes time to reprogram yourself, so persevere.

Trading Problem #2 – Selling Too Soon

We have all felt the disappointment of not selling a stock at the high. When a stock is marching higher, we set a point where we intend to sell so that we can lock in the gain before it goes down. The problem is that after we sell the stock, it continues to go higher leaving us with an opportunity missed.

Selling too soon is a problem that I continue to wrestle with after 23 years of trading stocks. I want to lock in that good feeling of taking a profit off the table. I want to avoid the negative feeling of watching a good profit get cut in half by a rapid sell off. And so, I break my selling rules and sell the stock in anticipation of weakness, rather than when the market tells me I should.

The result is that profitability over the long term is not maximized. Once in a while, I may get out of a trade at a better price than I would if I followed my rules, but over 10 or more trades, my net profitability is not as good as if I had maintained my selling rules. Keeping in mind that trading stocks is a probability game, it is important to maximize gains on the winners so that the inevitable losers can be overcome.

The Solution

There are few things that can help you avoid falling in to this trap. First, go through a number of past trades and apply your selling rules to see what your net profitability would have been if you have been disciplined, and compare those with what you actually achieved. I did this and it gave me powerful proof that maintaining discipline pays off, and is worth striving for. In fact, when I did this over one particular one week period, the difference amounted to a pretty nice new car! That gave me the leverage on my emotions I need to overcome them.

Second, turn off the profit and loss indicator that most brokerages and trading platforms give you. How much you are up or down is irrelevant to the decision making process. Since we have an emotional attachment to the money, knowing that we are up a certain amount and then seeing that shrink on a normal pull back in a stock leads us to make an emotional decision.

Finally, remember to sell at floors, not ceilings. Do not limit the upside movement of a stock by setting a price target, but instead, limit the downside movement by setting a price floor. Sell a stock when it pulls back to a floor, rather than selling it in anticipation of it reaching a ceiling price.

Trading Problem #3 – Letting Small Losses Turn in to Big Losses

As I just mentioned, trading stocks is a probability game. You will not be right all the time, which means that one of the most important aspects of trading stocks is to never let small losses grow in to big, portfolio debilitating losses. You have to limit losses at a risk level if you are going to be successful over the long run.

Solution

The simplest and I think most effective solution for most people is to set a stop loss point before purchasing a stock, and apply it immediately after purchasing a stock. Use basic chart analysis to determine where the market will have proven your decision to enter a trade wrong, and set your stop just below that. Automated stop losses are best because they do not require you to have the discipline to pull the exit button. Do not change your stop once you are in the trade. Making the stop loss judgment before you enter the trade is best since you will not have an emotional attachment to the stock at that point since you have not put your money on the line yet.

Trading Problem #4 – Trading Low Probability Opportunities

My dad is one of those do it yourself guys who would rather work hard than have someone else do the job for him. As a kid growing up, that meant that I helped build fences, garages, basement developments, pour concrete driveways, do yardwork and generally learn that same ethic to work hard. I am thankful that I have that spirit, but in the early stages of being a trader, it was something that hurt me.

The stock market cannot be made to go your way by hard work. There are times when the market giveth, and there are times when the market taketh away. The legendary Vancouver stock promoter Murray Pezim once said that all abnormal profits in the stock market are just short term loans. His point is that people do not know when to leave the market alone, and when it is time to work hard.

Traders will tend to take low probability trading opportunities at the worst time, because it is during weak market conditions that the market only shows marginal opportunities. By working really hard, traders can find opportunities that are pretty good, but not great. By taking these lower probability trades, the trader sets him or herself up for failure, since their rate of success will not be as good.

The Solution

I have said it many times, when the going gets tough, tough traders get lazy. You must always be picky about the kind of trades you make, particularly when the market is weak. Working hard to find opportunities will not make you more money, working hard at being disciplined will.

Teach yourself to look forward to the slow times. Make a list of things that you are going to do when the market slows down. Plant a tree, play golf, kill the ants that are crawling around your house. Just make the list.

Perhaps most importantly, if you depend on the market for a paycheck, make sure that you bank money when the market is good so that you don’t have to trade when the market slows down. Making a trade because you need to pay some bills is not a good way to trade.

Trading Problem #5 – Overtrading

There are stock traders who make 150 or more trades in a single day. I am not sure they make a lot of money. I firmly believe that you can make more money by making fewer trades because it will make you focus on only the best of opportunities, and play them with a larger amount of capital so the pay off is better. By being patient and disciplined with the really high probability trades, you can maximize profitability.

The Solution

If you are currently making 50 trades a week, tell yourself that next week you will only be allowed to make 10. If you are making 20 a week, promise yourself that you can only make 5. Don’t just tell yourself that you are going to stick to your new rule, write it down!

By setting this limit, you will hopefully change your outlook and try harder to only consider very high probability trades. We want to focus on great trading opportunities, not just those that are good.

Trading Problem #6 – Hesitation

You are watching a stock that has all the signals you look for in an opportunity. The proper point to enter comes, but you wait. You second guess the opportunity and don’t buy the stock. Or, you bid for the stock at a price that is not likely to get filled if the opportunity does pan out the way you anticipate it will. As a result, you get left behind while the market pushes the stock higher.

A short while after the initial entry signal, when the stock has made a decent gain, you decide to finally enter the trade. After all, the market has proven your analysis correct, so you must be smart, and right! Not long after you enter, the stock turns south and you end up with a losing trade. If only you had bought when you first thought about it.

The Solution

This is really just a confidence issue. You are either not confident in your ability to analyze stocks, or you are not confident in the methodology that you are using to pick trades. Therefore, you have to research your method so that you have the confidence that it works. Then, you have to start small, making trades that have a potential loss that you are comfortable with. As you gain confidence in your method and your ability, increase the trade size. With your new found confidence, stand in a crowded room and scream, “I am great!” Well, maybe don’t carry it that far.

Trading Problem #7 – Letting Winners Turn in to Losers

The final trading problem that I want to focus on is allowing winning trades to turn in to losers. Many of us have probably had a time when a trade was making big loot, and we started to count the profits like they were ours before we exited the trade. When the stock started to lose the ground it had gained, we avoided selling because we had built up an emotional attachment to the paper profits we had seen. Instead of selling the stock to lock in some gain, we opted to hold out for the stock to go back to where it used to be, promising to sell when it came back to the point where we felt good about the trade. The stock drifts lower, and eventually the gain turns in to a loss. We ultimately sell it at the bottom, swearing never to do it again. But without some reprogramming, we probably will.

The Solution

Like Kenny Rogers used to sing, “Don’t count your money, when you are sitting at the table, there will be time enough for counting, when the dealing’s done.” Do not calculate your profits before you lock them in. Avoiding the profit watch will help you avoid an emotional attachment to the paper profits, giving you greater clarity to take the exit door when the market tells you it is time to do so.

I hope this outline of mental problems and some solutions helps you become a better trader. The difference between those who succeed in trading and those who fail is not the system they play, but how well they play it. Your mind is a powerful thing, don’t let it beat you in the market.

STRATEGY OF THE WEEK

The staple of my position trading strategies is the Stockscores Simple. It seeks stocks with Sentiment Stockscores of 60 or better and Signal Stockscores of 80 or higher. There is an element of skill to this strategy as you have to know what to look for in the charts of stocks that the Market Scan identifies. We want stocks that are breaking through resistance from an optimistic chart pattern with some evidence of market excitement in the recent trading activity.

Here are two stocks that showed some good trading action on a quiet day of trading Monday:

STOCKS THAT MEET THE FEATURED STRATEGY

1. BTH

BTH is breaking out through resistance after breaking its downward trend in January. The break today is an abnormal price move from a rising bottom, a sign of investor optimism. Support at $16.75.

2. GA

GA is already well in to an upward trend but it has paused for about three months, setting up resistance at $6.50. Today the stock broke through that resistance level with good volume, setting the stock up for the next leg of the upward trend. Support at $6.45.

- References

- Get the Stockscore on any of over 20,000 North American stocks.

- Background on the theories used by Stockscores.

- Strategies that can help you find new opportunities.

- Scan the market using extensive filter criteria.

- Build a portfolio of stocks and view a slide show of their charts.

- See which sectors are leading the market, and their components.

Disclaimer

This is not an investment advisory, and should not be used to make investment decisions. Information in Stockscores Perspectives is often opinionated and should be considered for information purposes only. No stock exchange anywhere has approved or disapproved of the information contained herein. There is no express or implied solicitation to buy or sell securities. The writers and editors of Perspectives may have positions in the stocks discussed above and may trade in the stocks mentioned. Don’t consider buying or selling any stock without conducting your own due diligence.

The market pushed to a new high this past week, as I expected, as the continued push of liquidity from the Fed, and the ECB and BOJ, offset such silly concerns as another country going belly up and wiping out depositors. For some background (click on the link or the Chart below) read my post: “Get Ready For A Run To All Time Highs.”

I have spent much of last week doing interviews on what the push to all-time highs means. In reality, for most individuals, it means very little. That is the crux of this week’s missive which is the disconnect that exists between portfolio performance and index performance.

The sad commentary is that investors continually do the wrong things emotionally by watching benchmark indexes. However, what they fail to understand is that there are many factors that affect a “market capitalization weighted index” far differently than a “dollar invested portfolio.”

These misunderstandings lead to emotional decisions to buy and sell at the wrong times; jump from one investment strategy to another as well one advisor to the next. While these actions are great forWall Street, as money in motion creates fees and commissions, it does little to solve the bulk of the problem with investor’s portfolios which is simply emotional mistakes based on unrealistic expectations.

The single biggest mistake that investors make is the fallacy of chasing a benchmark index (i.e. the S&P 500) thinking that it is something\ they must beat. But why wouldn’t they? This is what they are told day in and out by the media. It is the mantra that has been drilled into all of us by Wall Street over the last 30 years. However, what we fail to understand is that this is for Wall Street’s benefit and not our own.

I will cover several of the major reasons why you will NEVER be able to beat the S&P 500 index over long periods of time. It is simply a function of the math.

An Update on the Silver Stocks

by Jordan Roy-Byrne The Daily Gold

When we discuss gold stocks we often refer to gold and silver stocks. Today we take a look at the silver stocks specifically.

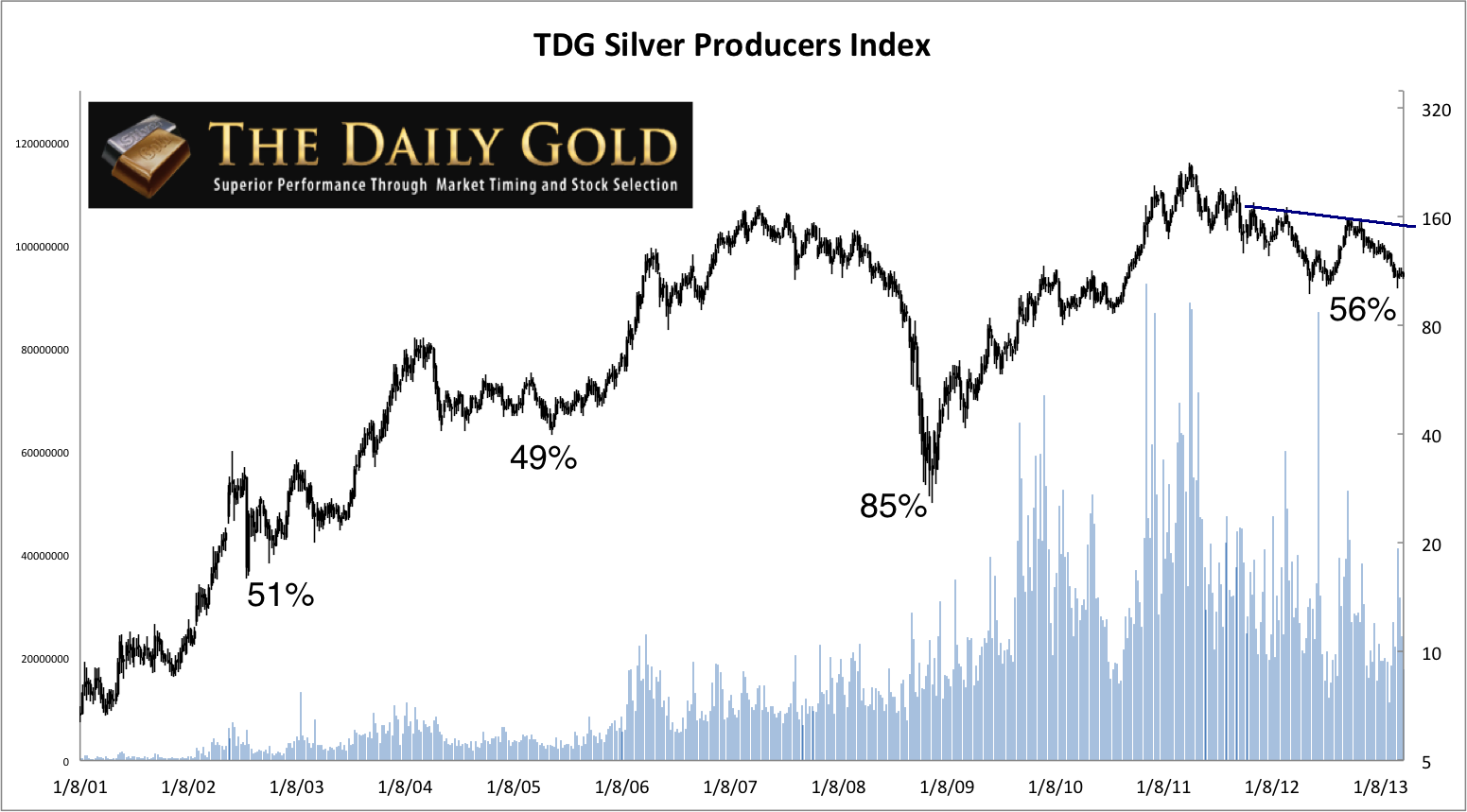

Below is a chart of our partially weighted producers index which contains 14 of the largest silver producers. We didn’t cherry pick the 14. We went down the list and that includes a handful of companies which have really struggled in recent years. Anyway, the 56% in the current cyclical bear is well in line with history. Previous downturns have been 51% and 49% and then 85% from 2007-2008.

Only time will tell but there is a chance that this evolving spring bottom could be the right side of a major long-term double bottom. Keep an eye on the trendline above. A break above that and the multi-year outlook becomes all the more bullish given the lack of overhead resistance.

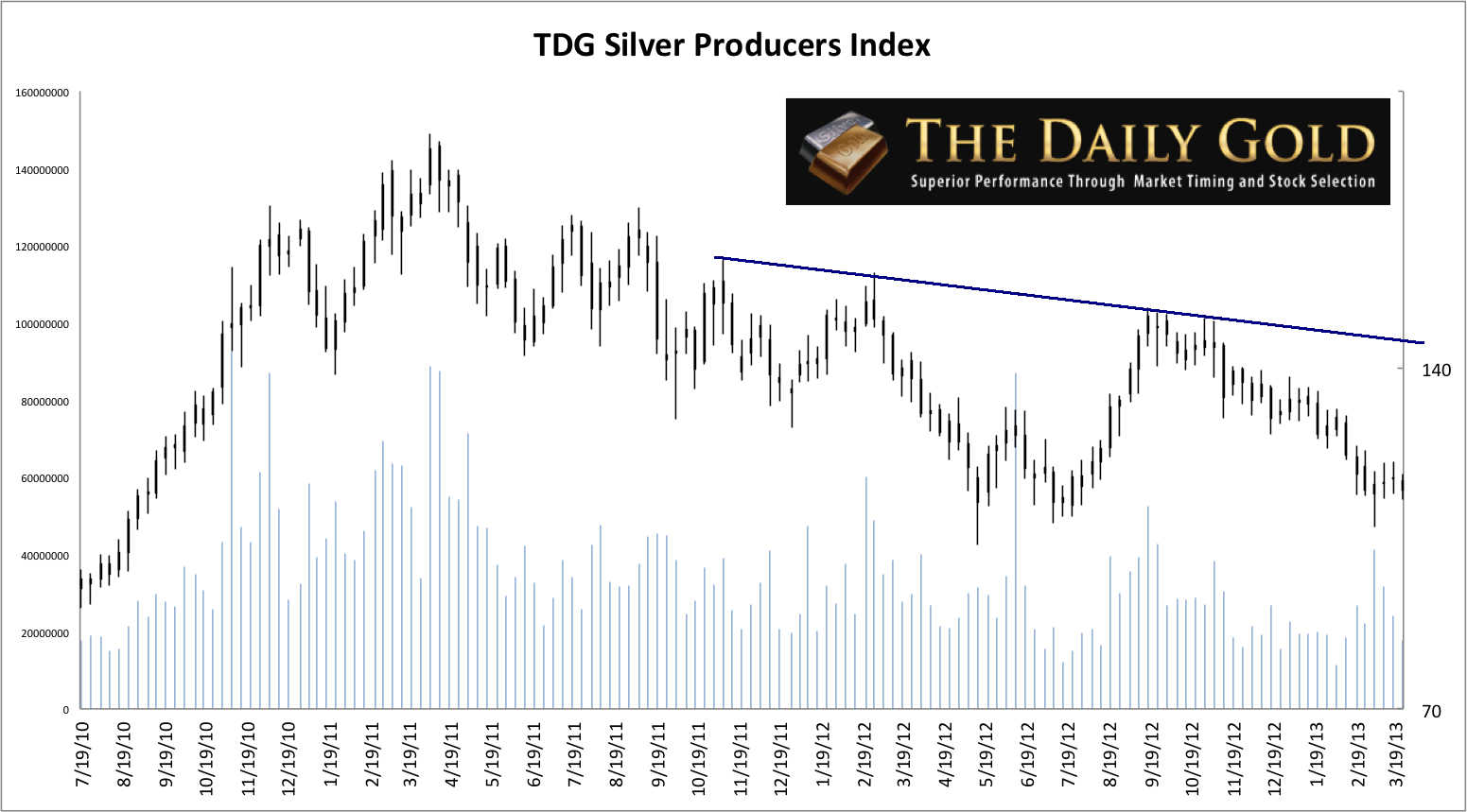

Zooming in (see below) we find that the market is holding slightly above its 2012 double bottom. The silver stocks put in a strong bullish reversal with volume four weeks ago. The market has yet to confirm the bottom but it could if it closes next week or the following week at five or six week high. Once that happens, the downtrend line becomes the next important resistance.

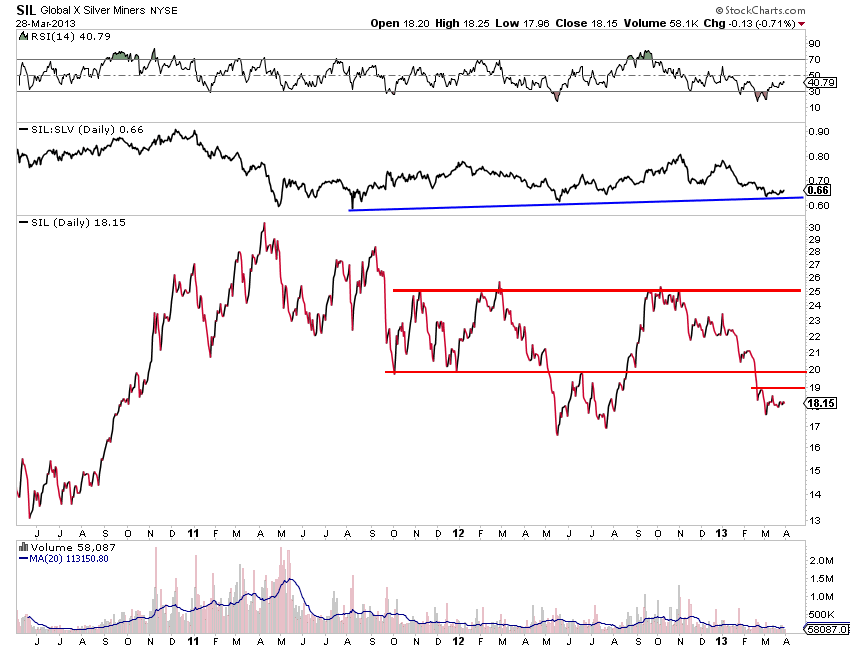

The silver stock ETF, SIL has also failed to close below the 2012 double bottom. It closed at $18.15 and faces key resistance at both $19 and $20.

There are a few other observations to note. First, note that SIL is showing relative strength against Silver. For whatever reason, the silver stocks in comparison to the gold stocks have fared better. The gold stocks (GDX, HUI) have broken below their 2012 lows while the silver stocks have not. Also, note the average volume in SIL. The 20-day average volume is roughly 100K shares. At its peak two years ago it was about 1.5 Million shares. That is 15 times higher!

Relative to gold stocks we were super bullish on silver stocks in 2010 but less so in 2011 and 2012. Gold leads Silver but once Gold finds its stride Silver heats up. If the precious metals bull market has another leg higher in it then we’ll move to an overweight position in the silver stocks at somepoint. The silver stocks as a group haven’t experienced a sustained breakout to new highs since 2007. If Silver is to advance to $40, $50 and beyond then that has incredibly bullish implications for the chart of our Silver Producers Index. The silver producers could be poised for leadership and incredible performance in 2014 and 2015. If you’d be interested in professional guidance in uncovering the producers and explorers poised for big gains in the next few years then we invite you to learn more about our service.

Good Luck!

Jordan Roy-Byrne, CMT

There were a lot of long faces at the PDAC this year. Many of the companies there were pulled off the waiting list when long standing attendee companies decided there was no point having a booth. Others have expressed surprise that few companies seemed to be trying to market financings. This was taken as complacency but it felt more like resignation to me. For the record, resignation is better if you’re a contrarian.

The editorial this month deals with the sea change that seems to have taken place among major companies. They are looking for a different type of project and that creates difficulties for Juniors that focused on things majors are not buying right now. It’s a long topic and I will cover the remainder of it in the next issue.

It was a very quiet month as you’ll see from the update section. A lot of companies aren’t active enough to even come up with the traditional “PDAC Look at Me” news release. That reinforced the point I’ve made before that it will be a slow turnaround and there will be only a small number of companies participating in the early stages of a rally. I’m pleased at how gold has held up against a very strong $US. The type of strong economic stats I feared would knock gold down farther hasn’t done that. I hope that means this bottom doesn’t drag on too much longer.

This year’s trip to the Prospectors and Developers of Canada convention in Toronto was less enlightening than usual but was a good gauge of sentiment.

Just about everyone goes to PDAC and it’s a good chance to talk to mining executives, explorers and analysts from across the globe. The conference is also famous for its hospitality suites. Good places to collect intelligence from a large number of people who actually buy resource stocks (sometimes), not to mention hangovers.

Not surprisingly, almost everyone was downbeat. Estimates of when the market would turn around ranged from “at least a year” to “never”. A lot of comparisons were made to the post-Bre-X meltdown. That bear market lasted for 5-6 years.

David and I lived through it and it wasn’t pretty. The sector was decimated at both the financial level and at the personnel level. Many suppliers disappeared and even more geologists went off to teach high school science, most never to return.

I understand the pessimism after two years of down markets but I have trouble drawing a parallel between now and 1997. After the Asian currency crisis and Bre-X— the former was at least as large a problem as the latter—commodity prices declined across the board for several years. Precious and base metals couldn’t catch a bid for four years and it took a couple more before anyone but the diehards noticed a bottom was in.This time around there is concern about commodity prices but we are dealing with completely different levels of “concern”. If high demand regions (China, the US) don’t have good years there will be metals that move into or remain in oversupply. That isn’t news and no one expects a commodity apocalypse.

Precious metals and most base metals are up anywhere from 300% to 600% in the past 10 years. Even commodity bears are not expecting pullbacks larger than 10-20% from current levels; the jury is still out on whether even that comes to pass. There is a big difference between that scenario and the late 1990’s.

Back then there were widespread mine closures and almost all mines were left operating on razor thin profits or limping along generating losses, eating up equity and praying for a turn in prices. Most producers had mountains of debt back then. Now most have fairly clean balance sheets and large cash balances.

Recently, a lot of top of the mountain, high capex projects have been called off. Not good news but hardly the same as mines going under left, right and center. It doesn’t represent the same level of industry decimation, but it does beg the question of where the sector goes from here.

In the past few years the level of project cost inflation has been incredible. Some of that is energy costs. Hard rock operations require a lot of energy .In many parts of the world that means generator sets, usually diesel fired, rather than just plugging into a grid. Oil has been a big winner this commodity cycle and higher fuel costs go right to the bottom line in a mining operation.

That is only one aspect of costs though. The truth is that virtually every cost associated with mine development from steel to concrete to heavy equipment to engineers and designers have gone through the roof. Some of that is super cycle impact on other commodities but some is the cost escalation that comes when any sector has a good run. Everyone associated wants their piece of the action. Everyone raises their prices or level of professional fees.

I think the fun’s over for now for these suppliers. Senior miners’ shareholders are demanding more accountability and cost control. I was raised in the mining business. I know how hard things were for a long time so I’m the last person to begrudge people in the sector getting a good payday. That said, shareholders have put the mining sector on notice that they only inflation they want to hear about is inflation of the bottom line.

I think you will see suppliers up and down the supply chain getting squeezed hard for the next couple of years. What large company executives can’t enforce the markets will take care of. Margin compression that has been the bane of the mining sector is now being passed onto the suppliers of the mining sector and that’s not a bad thing.

Cost over runs affect operating costs just as they do capital costs. A big factor in operating cost increases is decline in grade. Most precious and base metal operations have seen the average grade of producing deposits decline for decades. More rock has to be moved to produce the same amount of metal. In large part that is a reflection of the fact big high grade deposits are getting harder to find. That statistic is an argument for higher commodity prices, not lower ones.

While I think difficulty in finding new ore is the main culprit for the drop in grade it’s not the only one. I think there has been some “selection bias” in the past decade especially.

Mining companies faced unprecedented increases in demand in the past decade. Commodity prices were rising fast and the market was signaling it was able to absorb larger quantities of new ore than miners dared dream a few years earlier.

Miners had to generate very large increases in production growth. Since mines, be they large or small, need similar levels of executive staffing miners saw efficiency gains in opening a smaller number of large operations. Size mattered.

Large producers wanted deposits that offered the biggest annual metals production and maximum scalability. That meant large, bulk tonnage open pit deposits. Gold miners found themselves drawn to large lower grade deposits where production rates in the 100,000 tonne per day plus were achievable.

Copper miners focused on similar deposits because they were favoring sulphides—large milling operations that allowed for scalability and overall output scale that would be difficult to achieve with an oxide heap leach deposit—assuming you could find a copper oxide deposit that large.

For the junior mining space the preferred end game is take over by a major. Seeing the preferences of the large companies juniors dutifully went out and acquired large low grade bulk tonnage targets. Quite a few of them had some success drilling off large low margin deposits. They were all the rage for a few years and some did indeed get taken out at high prices.

Many more deposits were found than were bought. Quite a few of these are simply not that good for logistical reasons, poor metallurgy, uncertain politics or some combination of all three. They were available because they were uneconomic at circa 2001 metal prices but many of them are marginal even at todays.

When gold and silver were less favored many juniors chased rare earths, or graphite or lithium. Nothing wrong with any of this except that some of these market sectors are not large, at least right now. In the case of most specialty or industrial metals only a handful of new deposits are required short and medium term. Best in class projects can make a go of it but the rest may not find buyers.

Things started shifting in the past 18 months. Metal prices plateaued and the combination of capital cost inflation, permitting and development holdups and increased operating costs shelved scores of projects and made those that did get built less profitable than expected.

Major mining companies didn’t deliver promised profit growth and shareholders have been revolting in the boardroom and voting with their feet. Many CEOs have been fired and their replacements and peers are terrified of repeating mistakes that cost others their jobs.

I’ve had discussions with senior execs at several major companies recently that reinforce the comments above. These companies have shifted from looking for scale to looking for margin. That is a sensible move—it’s what they always should have been looking for. It does create a large problem for the Juniors though.

All these small companies worked diligently for years to find resources they thought would be salable. They are now being told they are not. Where is the endgame for these deals now? I can envision several endgame scenarios, which will only work for some of these companies.

The first scenario is companies with resources getting so cheap they become irresistible. I’m not sure what defines “irresistible” in this new paradigm but I’m afraid it may be cheaper than shareholders want to consider.

At some point, majors and mid-size producers will buy up a bunch of these deposits. If they are merely putting them in inventory don’t expect miracles when it comes to pricing. I don’t think “buyout as endgame” has gone away for these companies but, for the time being, deals will be done at prices that are not accretive to either shareholder value or happiness.

Where does that leave these companies? They could go it alone, but only in theory in most cases. Many companies have generated a PEA (Preliminary Economic Assessment) for projects in the hopes this would smoke out a buyer. I did a quick search for the past six months and found well over 100 PEA announcements. In most cases these have capital cost estimates in the hundreds of millions if not billions of dollars.

Once PEA numbers are released the die is cast as far as shareholders are concerned. They wait for a major to show up and offer to buy them out. If it doesn’t arrive quickly the company’s value starts to deteriorate.

Post-PEA news flow is often the boring technical variety, and full Bankable Feasibility Studies cost millions. Right now, the market is littered with companies that have $20-30 million market values sitting on resources that will require a billion plus to put in production. You can’t make those numbers work. If you’re not offered a buyout you need a Plan B.

One alternative is to focus on higher grade sections of the deposit (if they exist) that might be amenable to a smaller, tighter production plan. If there is leachable gold, or high grade near surface that can be pitted or ramped down to the company could come back with a small production scenario that has a sub $100 million cost. It won’t be massive but it might be doable and may, on a per unit basis, be much more profitable.

If the cash cost was low enough it could be of immediate interest to a producer. It might even be something the junior could tackle on its own. I’m expecting to see a lot of rejigged studies and some will even make sense.

If management has the skills to get the project through development this could breathe new life into the company. The skills required to get a mine into production are a lot different from the skills needed to find one. SilverCrest Mines (SVL-V), a long time HRA favorite is a great example of a company that has management with both skill sets. Not many do.

Another scenario involves picking up new ground to try and restart the discovery process. This will provide the company with news flow and, hopefully, some excitement to draw in new shareholders and cheer up present ones. This scenario may not please institutional shareholders but I don’t think there are institutional shareholders in the space right now. There is no point trying to please shareholders that have already sold.

Perhaps the best recent example of this game plan is Exeter Resources (XRC-T) optioning two projects from HRA list company San Marco (SMN-V; see update). Some XRC shareholders may have wondered why a company with several million ounces in resources would option early stage projects. I didn’t. I thought it made total sense.

Returning to exploration gives a company news flow and a shot at new discoveries that they may be able to develop in house. There are some particular attributes I think would work best in this new paradigm. I’ll go into that next issue.

Ω

What Do Our Subscribers Say?

“I have subscribed to several newsletters and Hard Rock stands far above all others I am familiar with. You are helping me big time in building my retirement and in this area, you are a life-saver for me. I will continue to be a loyal subscriber as long as you’re doing this.” J.T., CA, USA

“The Hard Rock Analyst… To us, with the boom in the junior mining sector right now, its mandatory reading and if you aren’t receiving it yet… you should.” D.P., AB, CAN

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair