Stocks & Equities

As of yesterday, Cyprus was on its way to becoming a distant concern, pushed off the front page by news about New Jersey’s $338 million Powerball winner and the Supreme Court’s likely endorsement of same-sex marriages. And yet, with euroland’s latest banking crisis out of the way for now, investors acted surprisingly subdued yesterday, pushing the Dow to a modest gain of 113 points. Our guess is that Wall Street is quietly gearing up for a rip-roaring short squeeze to finish out the week. The broad averages have been hovering near record highs to begin with, but by the time Friday rolls around, we’re betting that stocks will be trading well above these levels, demonstrating yet again that investors haven’t a care in the world. The flip side, unfortunately, is that gold prices are about to head lower, having failed to register much of a pulse even during the most worrisome phase of negotiations to “rescue” the Bank of Cyprus.

{kind=link}

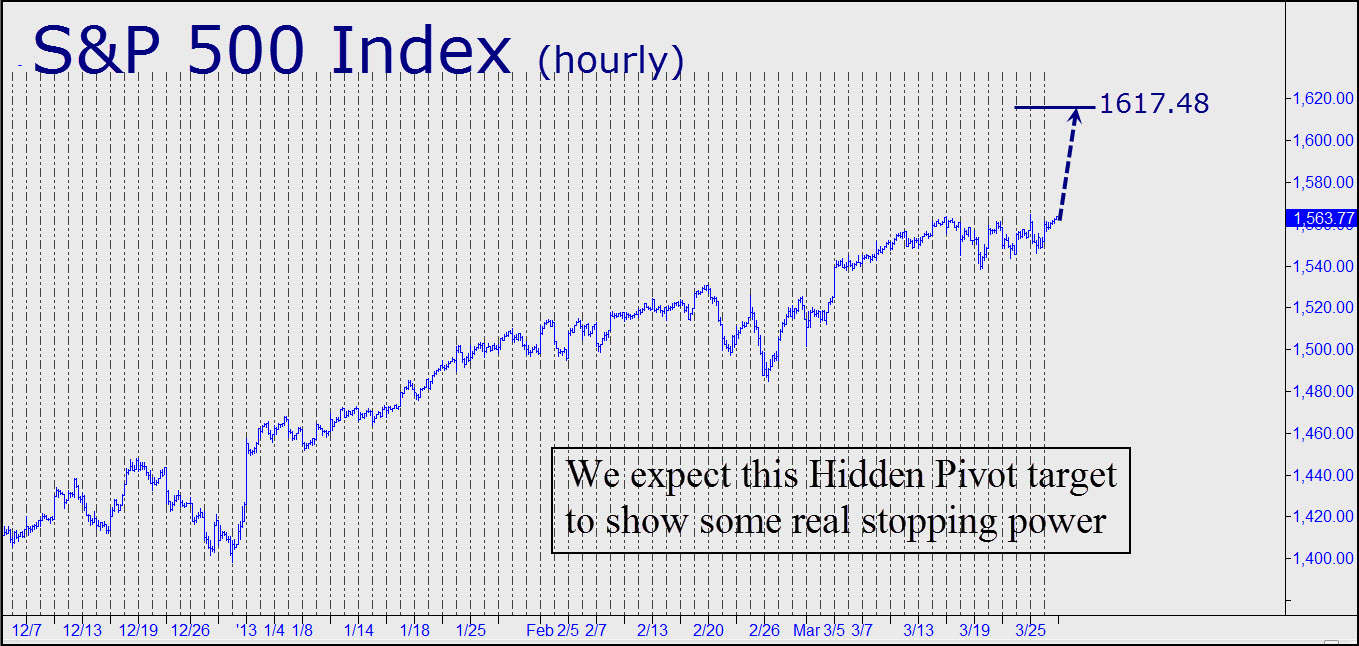

Not to rain on speculators’ parade, but here’s a number to watch if you’re crazy enough, after all these years, to still be looking for a top: 1617.48, basis the S&P 500 Index. Thats a proprietary Hidden Pivot target of ours (see chart above), and although we must concede that no such target that we’ve proffered over the last four years has shown fatal stopping power, this one seems likely to produce at least a short-able high. The purpose of these Hidden Pivot numbers is not only to provide precise swing points to get short or long, but to gauge the strength of the underlying trend. In this case, and generally speaking, if a clear “hidden” resistance such as this one gives way easily, it is a sign that considerable buying power remains to be spent. Thus, we would regard an easy move through 1617.48 as strongly implying that no end is in sight for the bullish rampage. One more thing: the target is also our minimum upside projection for the near term. Under the circumstances, any trades we recommend to subscribers will be from the long side. Click here to join the fun with a week’s free subscription to Rick’s Picks.

Good morning. Here’s what you need to know.

Good morning. Here’s what you need to know.

- Markets in Asia were higher in overnight trading, with both the Japanese Nikkei and Shanghai Composite both up 0.2 percent. European markets are in the red, with Spain leading the way lower, currently down 1.5 percent. Italy is also quite weak due to political chaos and the difficulty the country has in forming a government. In the United States, futures point to a negative open.

…..2 through 10 HERE

“In 40 years of watching markets closely, I have never seen more dangerous conditions than exist in the stock market today…”

What Bob has published is so exceptional that it’s best for me to show instead of tell — and I’d like to provide you with one more example of what that means.

Please take a moment to consider the six decades of data this chart presents, via the S&P 500 (above) and the mutual funds cash-to-asset ratio (below). The vertical dotted lines help show a clear correlation.

Thank you for reading,

![]()

Robert Folsom

Elliott Wave International

The above is one of more than a dozen recent sentiment charts presented in Prechter’s latest Theorists.

Follow this link to see them now — on your screen in moments — all risk-free for 30 days >>

The Bottom Line

Upside potential by North American equity markets into April remains, but many seasonal trades also expire around mid-April. Retention of existing seasonal trades makes sense. However, new seasonal opportunities coming into April are relatively sparse (An exception is the Technology sector). In most cases with seasonal trades, the question is “When to take profits”?

U.S. economic news this week is expected to be slightly bearish (Consumer confidence, New home sales, Weekly initial claims, Chicago PMI).

First quarter earnings reports come into focus starting this week. Most companies are in their quiet time. Only companies with negative surprises are likely to comment. Consensus is a year-over-year gain by the 30 Dow Industrial companies of only 3.1%. Consensus for the TSX 60 companies is no change.

Short and intermediate technical indicators for North American equity indices and most sectors are overbought. Some already are showing signs of rolling over. Another test by the S&P 500 Index of its all-time high is likely, but is not expected to show significant follow through.

Currencies remain a focus, particular with the crisis in Cyprus and its potential impact on the Euro and the U.S. Dollar.

Political concerns are not a factor this week. Congress is getting ready to go on their Easter holiday.

Trading activity will diminish as the end of the week approaches. Look for quarter end “window dressing” to impact selected securities.

Cash hoards remain high.

Ed Note: To read the comments and view the 50 Monday Morning Charts just click HERE. Otherwise a chart from each category below:

Equity Trends

The TSX Composite Index slipped 72.67 points (0.57%) last week. Intermediate trend remains up. Resistance is forming at 12,904.71. The Index slipped below its 20 day moving average, but remains above its 50 and 200 day moving averages. Strength relative to the S&P 500 Index remains negative. Short term momentum indicators are trending down.

Currencies

The U.S. Dollar added 0.40 (0.49%) last week. Intermediate trend is up. The Dollar remains above its 20, 50 and 200 day moving averages. Short term momentum indicators are overbought and showing signs of rolling over.

Commodities

The CRB Index fell 1.74 points (0.59%) last week. Intermediate trend is down. The Index moved above its 20 day moving average. Strength relative to the S&P 500 Index remains negative, but showing early signs of change.

Interest Rates

The yield on 10 year U.S. Treasuries slipped 8.1 basis points (4.06%) last week. Yield fell below its 20 and 50 day moving averages. Short term momentum indicators have rolled over from overbought levels.

Other Issues

The VIX Index gained 2.27 (20.09%) last week.

Special Free Services available through www.equityclock.com

Equityclock.com is offering free access to a data base showing seasonal studies on individual stocks and sectors. The data base holds seasonality studies on over 1000 big and moderate cap securities and indices. Notice that most of the seasonality charts have been updated recently.

To login, simply go to http://www.equityclock.com/charts/

Following is an example, just click on the link:

Stock Market Outlook for March 25, 2013

“The central banks’ gold is likely gone, and the bullion banks that sold it have no realistic chance of getting it back” Eric Sprott tells us.

He also says that these “bullion bank” intermediaries are probably turning around and selling their gold to China.

China, by the way, is the mostly likely catalyst to set off the “zero hour” scenario we told you about on Friday…

We’ve chronicled China’s ongoing gold grab here at Agora Financial — going all the way back to April 24, 2009, when the People’s Bank of China announced its gold reserves had grown to 1,054 tonnes — up from 600 in 2003. And that’s the last official word.

Then there’s private-sector demand in China. The government is equally opaque on this score. But we do get regular figures on Chinese imports via Hong Kong. Last year, they totaled a staggering 834.5 tonnes. And remember, that’s in a market that produces only 3,700 tonnes a year!

Couple those imports with Chinese mine production — and the total amount of gold known to be inside China has doubled in a mere three years.

Then there are the voluminous statements by Chinese public officials best taken at face value…

- China’s gold reserve is “too small,” says the Department of International Economic Affairs of Ministry

- “No asset is safe now,” says the head of the People’s Bank of China’s research bureau. “The only choice to hedge risks is to hold hard currency — gold”

- And maybe most telling for our purposes: “The U.S. and Europe have always suppressed the rising price of gold,” according to a commentary in the Shijie Xinwenbao newspaper, duly noted by U.S. diplomats in cables exposed by WikiLeaks.

Echoing a theme we first wrote about in The Demise of the Dollar (John Wiley & Sons, 2005), “suppressing the price of gold,” the article went on, “is very beneficial for the U.S. in maintaining the U.S. dollar’s role as the international reserve currency. China’s increased gold reserves will thus act as a model and lead other countries toward reserving more gold. Large gold reserves are also beneficial in promoting the internationalization of the renminbi.”

The plot thickens: “In 2009,” says our own Outstanding Investments editor Byron King, “a high-ranking government adviser let slip that a special government task force recommended increasing China’s gold reserves to a staggering 10,000 tonnes.” What’s more, “word is already starting to leak out in Chinese newspapers that government officials intend to make the renminbi ‘fully convertible’ by 2015” — that is, able to be freely exchanged for other currencies.

Put it all together and the picture becomes clear: China aims to grow its gold stash tenfold to bolster the renminbi’s credibility in only two more years.

We come back to Mr. Sprott’s question: “So where’s the gold coming from?”

Germany Has to Wait 7 Years for Its Gold… Make Sure You Have Yours Now

In January, Germany’s central bank posed the same question. It made plans to repatriate much of its gold stash — heretofore kept in France and America, the better to keep it out of the Soviets’ hands in case the Cold War ever turned hot.

The process of moving 674 tonnes back to Germany is scheduled to take… seven years.

Not the sort of time frame that should make you feel warm and fuzzy about how much of the U.S. and French reserves are actual gold — or “gold receivables.”

Which brings us back to zero hour in the gold market. On any given day, the amount of physical gold that’s traded around the world is dwarfed by “paper gold” — mostly futures. In the estimation of experts like our friend Egon von Greyerz of Gold Switzerland and Hong Kong-based hedge fund manager William Kaye, the ratio is 100-to-1.

Up until now, the ratio has posed no problem. Most people trading gold futures are in it for a short-term gain. But a few people always want to take delivery of actual metal. At zero hour, “what happens is someday some guy or country wants to buy gold, and it’s not going to be available,” says Eric Sprott.

The Comex can’t deliver… and offers up a cash settlement instead.

“When does the last bar disappear and somebody fess up? We trade all this paper gold, but we now know there’s nothing behind it, because you can’t get delivery.” The timing is impossible to pinpoint… but “we’re living sort of hand to mouth already,” Sprott warns. “So it could be quite imminent.”

When the day arrives, you don’t want to be holding paper gold — and that includes exchange-traded funds like GLD. As we’ve pointed out before, the ETFs are subject to “counterparty risk” — the risk that whomever you’re doing business with won’t, or can’t, live up to their promises. Just like futures.

When zero hour comes, GLD’s price will do what it’s always done — track the Comex price of gold. Meanwhile, real physical gold in your possession will break away from that price… and you’ll be glad you have it.

While Mr. Sprott hesitates to put numbers to his forecast, we can perform a little napkin math. If the Comex price is $1,800, experience from 2008-09 shows that a Gold Eagle on eBay might go for a 30% premium — that’s $2,340! If panic takes over the Comex and the price rises to $2,000, real metal in your hand will be worth $2,600.

As the old commercial said, “Accept no substitutes.” Own physical gold.

Regards,

Addison Wiggin

Original article posted on Daily Resource Hunter

About Addison Wiggin

Addison Wiggin is the executive publisher of Agora Financial, LLC, a fiercely independent economic forecasting and financial research firm. He’s the creator and editorial director of Agora Financial’s daily 5 Min. Forecast and editorial director of The Daily Reckoning. Wiggin is the founder of Agora Entertainment, executive producer and co-writer of I.O.U.S.A., which was nominated for the Grand Jury Prize at the 2008 Sundance Film Festival, the 2009 Critics Choice Award for Best Documentary Feature, and was also shortlisted for a 2009 Academy Award. He is the author of the companion book of the film I.O.U.S.A.and his second edition of The Demise of the Dollar… and Why it’s Even Better for Your Investments was just fully revised and updated. Wiggin is a three-time New York Times best-selling author whose work has been recognized by The New York Times Magazine, The Economist, Worth, The New York Times, The Washington Post as well as major network news programs. He also co-authored international bestsellers Financial Reckoning Day and Empire of Debt with Bill Bonner.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair