Timing & trends

The month of March typically marks the beginning of Spring. This weekend will also mark the loss of an hour of sleep as we set our clocks forward an hour in observance of daylight savings time.

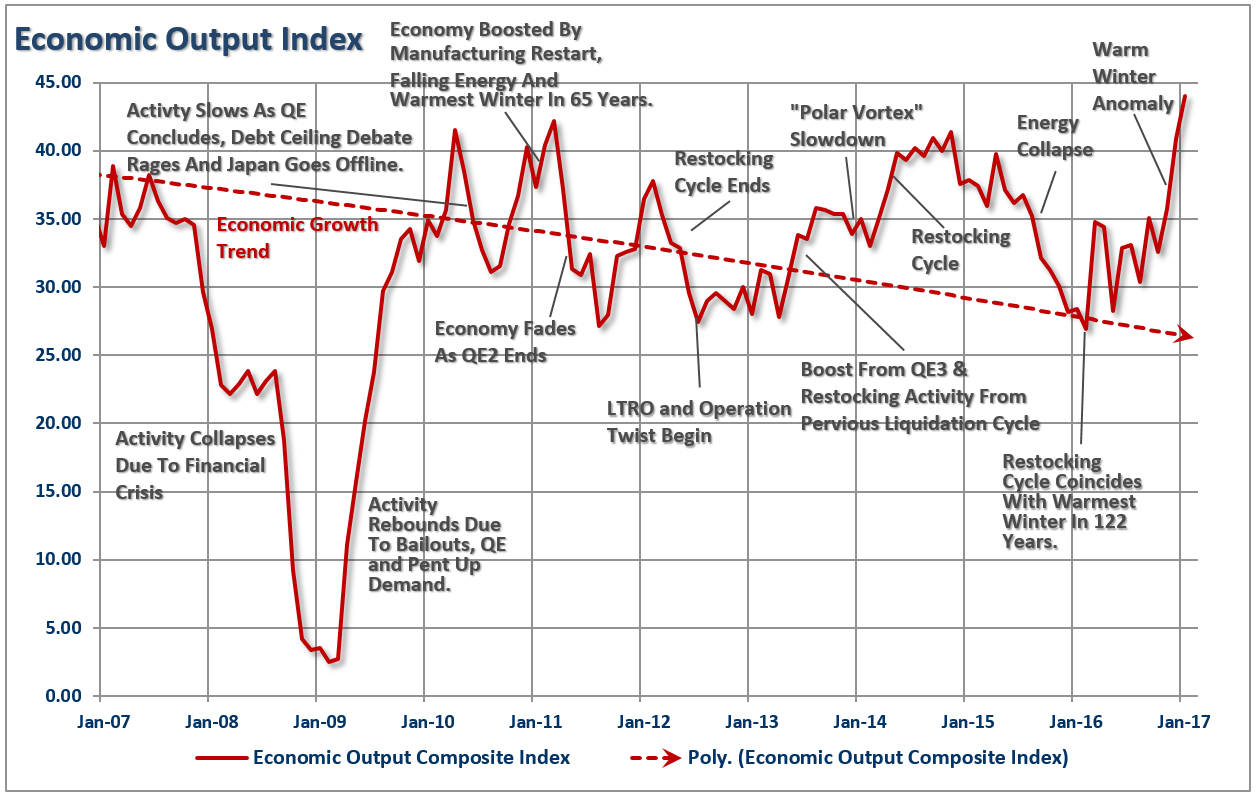

As we will discuss momentarily, the month of March begins following an unseasonably warm winter period that allowed for manufacturing activity to occur during a period where inclement weather normally abounds. This is an interesting point because two years ago, the BEA adjusted the “seasonal adjustment”factors to compensate for the cold winter weather over the previous couple of years which had suppressed first quarter economic growth rates. (The irony here is that they adjusted adjustments for cold weather that generally occurs during winter.) However, the problem with “tinkering” with the numbers comes when you have an exceptionally warm winter. The new adjustment factors, which boosted Q1 economic growth during the last two years now creates a large over-estimation of activity during the first quarter of a year where winter weather is unseasonably warm.

This anomaly has boosted “bullish hope” as the fear of an economic slowdown has been postponed. At least temporarily until the over-estimations are revised away over the course of the coming months. Of course, with the spread between “hope” and “reality” currently at some of the highest levels ever, it is worth paying attention to what happens.

One of the traditional signs of market tops is individual investors finally succumbing to the lure of apparently easy money and pouring their savings into the stock market. In the past this dumb money flowed into equity mutual funds in general. But today it’s favoring exchange traded funds (ETFs) that, rather than trying to pick winners, simply offer exposure to sectors or broad market indexes.

One of the traditional signs of market tops is individual investors finally succumbing to the lure of apparently easy money and pouring their savings into the stock market. In the past this dumb money flowed into equity mutual funds in general. But today it’s favoring exchange traded funds (ETFs) that, rather than trying to pick winners, simply offer exposure to sectors or broad market indexes.

ETFs Race to Fastest Yearly Start Ever Based on Inflows

(Wall Street Journal) – Investors poured $62.9 billion into exchange-traded funds in February, pushing the year-to-date world-wide tally to $124 billion, the fastest start of any year in the history of the ETF industry, according to data from BlackRock Inc.

U.S. ETFs accounted for $44 billion of that, pushing assets in U.S. funds to almost $2.8 trillion.

Most of the money went to cheap, index-tracking ETFs, a sign that the price war in ETFs isn’t over yet. BlackRock’s iShares ETFs were the biggest winner, and its low-cost Core series garnered the bulk of the $38 billion global haul.

“All of the money is going into the cheapest and most boring ETFs. This is the retail investor getting back into the market with a vengeance,” said Dave Nadig, chief executive of ETF.com, an industry website owned by Bats Global Markets, newly a subsidiary of CBOE Holdings Inc.The Rise of the ‘Do-Nothing’ Investor

Passive mutual funds are growing rapidly, pushing aside stock pickers and changing the investment world. Click here to read more about The Wall Street Journal series.The fastest-growing ETF so far this year is the iShares Core Emerging Markets ETF, which took in $4.2 billion in the first two months of the year, 18% of its assets, according to FactSet. Three other Core ETFs that invest in U.S. stocks were also among the top gainers last month.

Why is this a sign of a market top? Because small investors tend to trade on emotion rather than logic or expertise.

It takes them a long time to forget the pain of the last bear market, so they avoid the early stages of recoveries. When they finally conclude that there’s money to be made, it’s usually too late.

And why are individual investors only the second dumbest money? Because governments are even less astute and more emotional than individuals, and their plunge into equities is just beginning. Japan’s central bank is now one of its market’s biggest “investors” while the Swiss National Bank is a huge holder of blue chips like Apple and Microsoft. See We’re All Hedge Funds Now, Part 4: Central Banks Become World’s Biggest Stock Speculators.

In the next downturn — which, based on most valuation measures, seems imminent – the US Fed and European Central Bank will find that interest rates are too low for big further cuts while the supply of bonds is insufficient for big new QE programs. So they’ll join Japan and Switzerland in buying stocks. They’ll do so indiscriminately, creating their own index ETFs and throwing money at a broad range of large cap stocks, possibly pushing prices to levels that history would consider insane. In other words they’ll act like retail investors on steroids.

But that’s a story for the next cycle. This time around the fact that individuals pouring in is all we need to know.

1. Rate Hikes – Trump – Disappearing Pensions

by Michael Campbell

Trump may not be liked by 1/2 the US but after his speech to Congress even the press gave him a credit. Rate hikes on the agenda and so are solutions to the iceberg of unfunded pensions.

2. It’s Crash Awareness Week

2. It’s Crash Awareness Week

by Bill Bonner

A Los Angeles spec house is on the market. It has seven bedrooms and 20,000 square feet of living space. It comes with a gold Lamborghini Aventador and a gold Rolls-Royce Dawn. You also get a wine cellar, a pool, and the usual claptrap amenities to which rich people are easy prey.

The price? A hundred million dollars.

3. Gold Stocks’ Enormous Daily Slide

by Przemyslaw Radomski

Feb 27th was just another period of back-and-forth movement for gold, silver, the USD Index and even the general stock market – but not for precious metals mining stocks. Gold stocks and silver stocks plunged very visibly – there are very important implications of this move and they are not bullish

Rather than immediately wonder how the main stream media became corrupted, it is appropriate to recall when only the tabloids were suspect.

Rather than immediately wonder how the main stream media became corrupted, it is appropriate to recall when only the tabloids were suspect.

Perhaps there was a time when any town that was big enough for two newspapers one would favor the Democrats and the other the Republicans. That would be by editorials going into an election. For most of the time, the goal was accurate reporting. That was back when most small towns were right out of a Norman Rockwell painting. On the outskirts of respectability were the tabloids with sensational headlines about UFOs everywhere and Area 51, specifically. A standing joke was what would happen if a real alien landed at the doors of the National Enquirer?

Much has changed since. In 2010, the “Enquirer” was considered as “legit” by the Pulitzer Prize Board and an almost monolithic Main Stream Media has deteriorated into the fantasy world of tabloids.

Sensationally scary headlines were once limited to tabloids. In the early 1970s, headlines about “global cooling” and “Nuclear Winters” began to be included in the main stream media. Over the past twenty years, today’s form of yellow journalism has heralded the horrors of “global warming” and biblical rises in sea levels, not to overlook the violence of “climate change”.

More hysteria than science, it sells newspapers and gets TV eyeballs, which is business. It also enabled a formidable expansion of state power and wealth, which is control.

How did it happen?

Media and big government found each other.

British Columbia, where this writer lives, provides a colourful political history. Perhaps a micro-model for much of the Western world.

Since the 1950s, it has been a struggle between power-mad socialists and the party that tries to approach sound government. The latter provided some guidance on the US election. Under the name of Social Credit, it was a pro-business and socially-conservative party. It was so non-urban, that no sophisticated person would ever admit voting for the party. But the “Socreds” won majorities for almost 30 years. Currently in the US, the smart set would never admit to supporting the new Republicans. Come to think of it, neither can some old Republicans.

British Columbia’s first socialist government failed dramatically in 1975, defeated by Bill Bennett, a small-town businessman. The winning campaign platform was “Restraint”, which meant cutting excessive government expenditures. This was disquieting to the Left, that had thrived for 4 years at the public trough, while unloading their personal passions on the taxpayers.

Premier Bennett’s first press conference was fascinating. He reviewed “Restraint”, which was refreshing to the taxpayer. This was opposite to the media’s response. Instead of asking for clarification or elaboration, reporters began arguing against the policy points. It was a surprise and in retrospect the start of the unhealthy combination of big government and media. Quite likely this was taking place in many jurisdictions.

In the 1980s and 1990s, articles about journalism schools were published. When asked why students took journalism, the response was “To change the world”. This continues, with The Guardian in 2015 headlining “Would-be journalists still want to change the world”.

Reporting the world’s news seems secondary.

The result has been an unhealthy combination of powerful politicians, government agencies that are working for their own interests, an activist judiciary and FBI all promoted by a highly-politicized media. There is no sophistication about international socialists or national socialists. The Hegelian Dialectic has been corrupted to “You must do this!”. “Why?”. “Because!”.

The governing classes have become, well, ungovernable. Finally, the public is beginning to protest “in-your-face” and “in-your-pocket” bureaucracy. This fits the classic model of a popular uprising. The establishment lives the good life while peddling promises about how good things are to a public that know they are not doing well.

The last successful uprising took down the Berlin Wall and Communism. Beginning in 1989, ordinary citizens overwhelmed the threats of murderous police states. In the West now, all the governing classes have is a propagandizing media.

The popular uprising is the carrying event and is beginning to rank with the great ones in history. Now having an able executive, its success will continue. An uncorrupted media will report it – straight up.

DOW + 301 on 1000 net advances

NASDAQ COMP + 79 on 1350 net advances

SHORT TERM TREND Bullish

INTERMEDIATE TERM Bullish

STOCKS: Sometimes we’re not sure why the stock market does what it does, but this time there is no doubt. President Trump’s tone caught many doubters off guard. He was presidential and positive.

Of course, underneath, things haven’t changed. Investors continue to be encouraged by promises of lower taxes, less regulation and infrastructure spending.

After struggling for a while with Dow 20,000, the blue chip index spent just 24 sessions going the next 1,000 points, tied for the fastest ever/

GOLD: Gold dropped $4. It was down much more intraday. Less political tension dissuaded buyers.

CHART The volume rose sharply on the QQQ which is the ETF for the NASDAQ 100. This frequently marks some sort of a turn, Usually it’s seen at bottoms, but occasionally at tops. We’ll need to keep an eye n this short term indicator. We’re indebted to our friend Tom McClellan of the McClellan Financial Publications for pointing this out.

BOTTOM LINE: (Trading)

Our intermediate term system is on a buy.

System 7 We are in cash. Stay there for now.

System 8 We are long the SSO at 85.05. If there are more declining issues than advancing ones at 3:35 EST on Thursday, sell at the close.

NEWS AND FUNDAMENTALS: Personal income rose 0.4%, better than the anticipated 0.3%. The PMI mfg. index was 54.2, less than the expected 55.0. The ISM mfg. index came in at 57.7, better than the expected 56.4. Construction spending dropped 0.1%, worse than the expected rise of 0.05%. Oil inventories rose 1.5 million barrels. Last month, they rose 600,000.

INTERESTING STUFF: Paul Krugman, Nobel laureate economist with the New York Times said back in November that if Donald Trump won, the stock market would drop and never come back.

TORONTO EXCHANGE: Toronto rose a cool 200.

BONDS: Bonds dropped sharply.

THE REST: The dollar surged. Silver flat to down. Crude oil lost ground.

Bonds –Bullish as of Feb. 6.

U.S. dollar -Bullish as of Feb. 9.

Euro — Bullish as of December 2.

Gold —-Bullish as of Feb. 16.

Silver—- Bullish as of Jan. 31.

Crude oil —- Bearish as of Nov. 29.

Toronto Stock Exchange—- Bullish from January 22, 2016

We are on a long term buy signal for the markets of the U.S., Canada, Britain, Germany and France.

|

|

Wed. |

Thu. |

Fri. |

Mon. |

Tue. |

Wed. |

Evaluation |

|

Monetary conditions |

-1 |

-1 |

-1 |

-1 |

-1 |

-1 |

0 |

|

5 day RSI S&P 500 |

86 |

87 |

89 |

90 |

68 |

88 |

– |

|

5 day RSI NASDAQ |

89 |

67 |

70 |

76 |

50 |

74 |

– |

|

McCl- lAN OSC. |

+12 |

+11 |

-2 |

+13 |

-39 |

+7 |

0

|

|

Composite Gauge |

8 |

10 |

8 |

9 |

14 |

7 |

0 |

|

Comp. Gauge, 5 day m.a. |

8.2 |

8.4 |

8.0 |

8.2 |

9.8 |

9.6 |

0 |

|

CBOE Put Call Ratio |

.89 |

.83 |

.83 |

.83 |

1.18 |

.86 |

0 |

|

VIX |

11.74 |

11.71 |

11.47 |

12.09 |

12.92 |

12.54 |

|

|

VIX % change |

+1 |

0 |

-2 |

+5 |

+7 |

-3 |

0 |

|

VIX % change 5 day m.a. |

+1.8 |

-0.4 |

-0.4 |

+1.0 |

+2.2 |

+1.4 |

0 |

|

Adv – Dec 3 day m.a. |

+191 |

+354 |

-63 |

+240 |

-97 |

+243 |

0 |

|

Supply Demand 5 day m.a. |

.86 |

.78 |

.84 |

.80 |

.73 |

.75 |

0 |

|

Trading Index (TRIN) |

1.38 |

1.52 |

1.64 |

.82 |

1.38 |

.61 |

0

|

|

S&P 500

|

2363 |

2364 |

2367 |

2370 |

2364 |

2396 |

Plurality -2 |

INDICATOR PARAMETERS

Monetary conditions (+2 means the Fed is actively dropping rates; +1 means a bias toward easing. 0 means neutral, -1 means a bias toward tightening, -2 means actively raising rates). RSI (30 or below is oversold, 80 or above is overbought). McClellan Oscillator ( minus 100 is oversold. Plus 100 is overbought). Composite Gauge (5 or below is negative, 13 or above is positive). Composite Gauge five day m.a. (8.0 or below is overbought. 13.0 or above is oversold). CBOE Put Call Ratio ( .80 or below is a negative. 1.00 or above is a positive). Volatility Index, VIX (low teens bearish, high twenties bullish), VIX % single day change. + 5 or greater bullish. -5 or less, bearish. VIX % change 5 day m.a. +3.0 or above bullish, -3.0 or below, bearish. Advances minus declines three day m.a.( +500 is bearish. – 500 is bullish). Supply Demand 5 day m.a. (.45 or below is a positive. .80 or above is a negative). Trading Index (TRIN) 1.40 or above bullish. No level for bearish.

No guarantees are made. Traders can and do lose money. The publisher may take positions in recommended securities.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair