Timing & trends

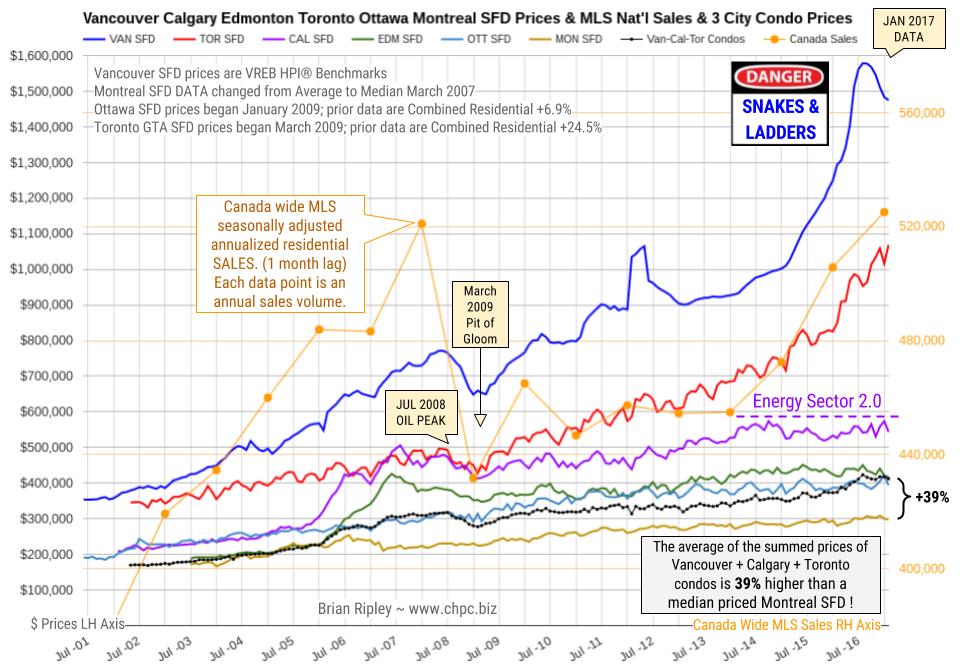

1. Canada 6-City Housing Prices Slide Off Their Highs

1. Canada 6-City Housing Prices Slide Off Their Highs

In January 2017 Canada’s big city metro SFD prices coiled about or slid off their near term highs except in Toronto where detached houses and town houses fetched new peak prices.

2. Why you shouldn’t fear rising interest rates …

“the notions that rising interest rates will kill off equity market gains, particularly in the U.S. … or choke off a real estate recovery … or kill the gold market for good — are myths. Period”

3. Extreme Readings in the Bond Market

Janet Yellen, you’re fired!

For the past 20-30 years, the Federal Reserve has been dominated by academics largely out of MIT. Jim Bianco at Bianco Research says that’s all going to change under Trump, starting with Fed chair Janet Yellen.

Europe could become the site of a new global war in the East as tensions build there against refugees and the economic decline fosters old wounds. The EU is deeply divided over the refugee issue and thus it is fueling its own demise and has failed to be a stabilizing force. After five days of demonstrations, Romania’s month-old government backed down and withdrew a decree that had decriminalized some corruption offenses. They were still acting like typical politicians and looking to line their pockets. After one month, the people have been rising up saying “We can’t trust this new government.”

Europe could become the site of a new global war in the East as tensions build there against refugees and the economic decline fosters old wounds. The EU is deeply divided over the refugee issue and thus it is fueling its own demise and has failed to be a stabilizing force. After five days of demonstrations, Romania’s month-old government backed down and withdrew a decree that had decriminalized some corruption offenses. They were still acting like typical politicians and looking to line their pockets. After one month, the people have been rising up saying “We can’t trust this new government.”

….also from Martin:

That didn’t take long.

After little more than two weeks, President Donald Trump’s honeymoon with Wall Street appears to have been put on hold—for the moment, at least—with major indices making only tepid moves since his January 20 inauguration. That includes the small-cap Russell 2000 Index, which surged in the days following Election Day on hopes that Trump’s pledge to roll back regulations and lower corporate taxes would benefit domestic small businesses the most.

And therein lies part of the problem. Although the president managed to sign an executive order last week requiring the elimination of two federal regulations for every new rule that’s adopted (and ordered a review of Dodd-Frank and former President Obama’s fiduciary rule), other campaign promises that initially excited investors—tax reform and an infrastructure spending deal among them—might have already hit a roadblock.

According to Reuters, a three-day meeting in Philadelphia between President Trump and congressional Republicans ended in a stalemate, with it looking less and less likely that tax reform will happen during Trump’s first 100 days in office—perhaps even the first 200 days. As for infrastructure, several Republicans were reportedly wary of committing to such an enormous spending package before more complete details become available.

|

Meanwhile, Trump’s seven-nation travel ban received a lukewarm—and, in some cases, hostile—reception from many in the business world who have traditionally depended on foreign talent. That’s especially the case in Silicon Valley, where close to 40 percent of all workers are foreign-born, according to the 2016 Silicon Valley Index. (Around the same percentage of Fortune 500 companies were founded by immigrants or children of immigrants, including Steve Jobs, whose biological father was Syrian.) One of the more dramatic responses toward the travel ban was Uber CEO Travis Kalanick’s dropping out of Trump’s business advisory panel, following an outcry from users of the popular ride-sharing app who saw his participation with the president as an endorsement of his immigration policies.

I’ve shared with you before that the media often take Trump literally but not seriously, whereas his supporters take him seriously but not literally. I think it’s evident that the market is finally coming to terms with the fact that Trump, unlike every other politician before him, actually meant everything he said on the campaign trail, including his more protectionist and nationalist ideas.

Although I don’t necessarily agree with Trump’s plans to raise tariffs, withdraw from free-trade agreements and restrict international travel, it might be easy to some to see why he feels American companies need protecting from foreign competition. Last week I attended the Harvard Business School CEO Presidents’ Seminar in Boston, and among the topics we discussed was China’s ascent as an economic and corporate juggernaut. Take a look at the chart below, using data from Fortune Magazine’s annual list of the world’s 500 largest companies by revenue. Whereas the U.S. has lost ground globally over the past 20 years, China’s share of large companies has exploded, from having only three on the list in 1995 to 103 in 2015. The number of Japanese firms, meanwhile, has more than halved in that time.

I will say, while I’m on this topic, that the uncertainty and unpredictablilty surrounding Trump has given active management a strong opportunity to demonstrate its value in the investment world. Assessing the risks and implications of his actions, policies and tweets, which change daily, really requires a human touch that fund managers and analysts can provide.

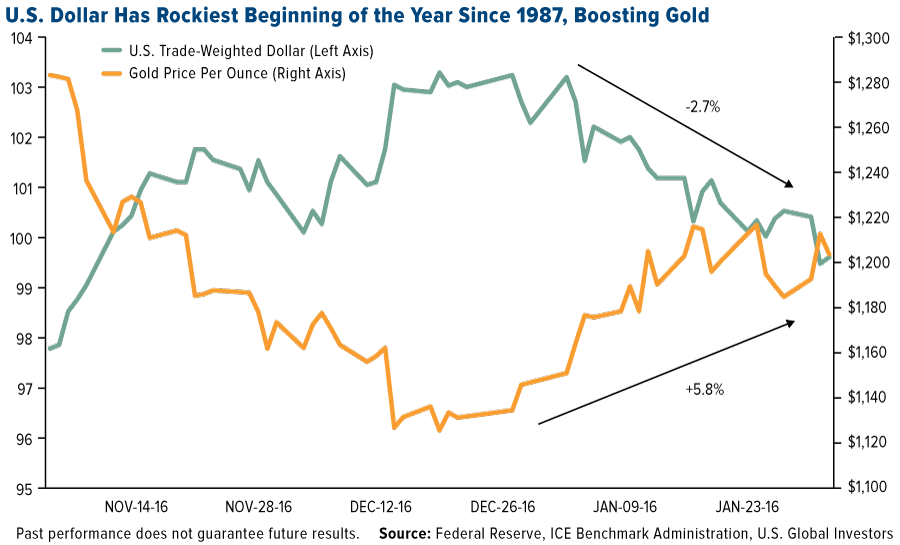

Dollar Down, Gold Up

One of those implications is the U.S. dollar’s decline. Following Trump’s comment that it was “too strong” and hurt American exporters’ competitiveness, currency traders shorted the greenback, causing it to have the worst start to a year since 1987.

This, coupled with a more dovish Federal Reserve, expectations of higher inflation and growing demand for a safe haven, has helped push gold prices back above $1,200 an ounce. January, in fact, was the best month for the yellow metal since June, when Brexit anxiety and negative government bond yields sent it to as high as $1,370.

Demand for gold as an investment was up a whopping 70 percent year-over-year in 2016, according to the World Gold Council. Gold ETFs had their second-best year on record. But immediately following the November election, outflows from gold ETFs and other products accelerated, eventually shedding some 193 metric tons.

But now, just two weeks into Trump’s term as president, the gold bulls are banging the drum, with several large hedge fund managers taking a contrarian bet on the precious metal.

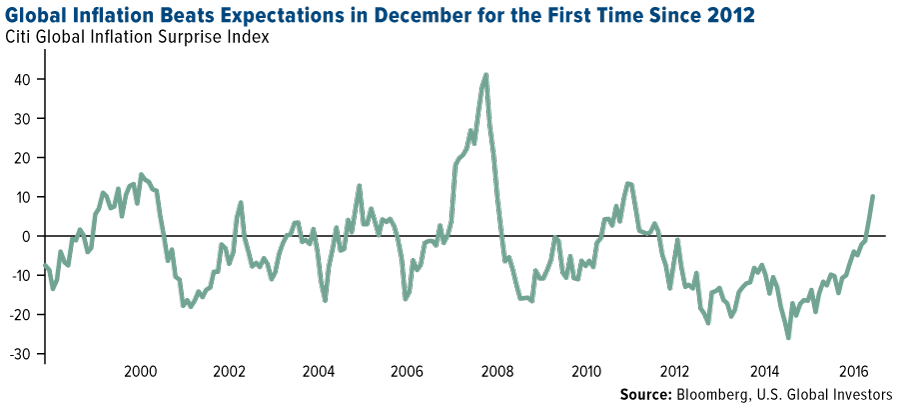

Inflationary pressures are indeed intensifying. U.S. consumer prices rose 2.1 percent in December year-over-year, their fastest pace since 2014, and inflation across the globe is beating market forecasts, with the Citi Global Inflation Surprise Index turning positive for the first time since 2012. Anything above zero indicates that actual inflation is stronger than expectations for the month.

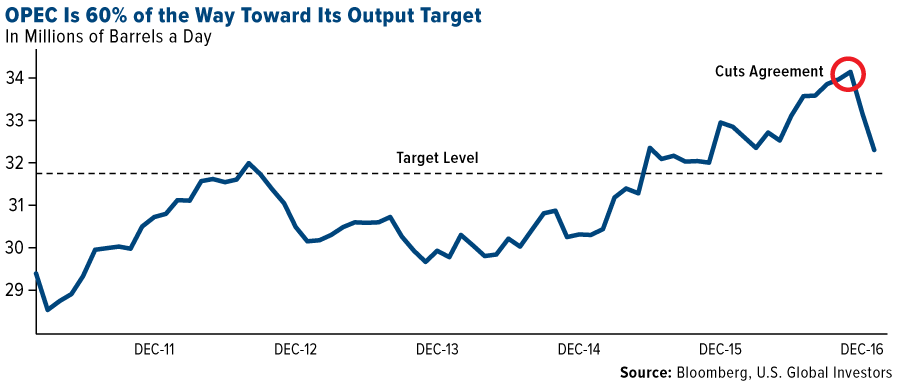

OPEC Making Good on Production Agreement

Among the commodities showing resilience right now is oil, especially on reports that the Organization of Petroleum Exporting Countries (OPEC) is 60 percent of the way to reaching its output target after agreeing to cutting production in early December for the first time since 2008.

Of course, this news is tempered by analysts’ expectations that U.S. producers will export more crude than four OPEC members combined in 2017. According to Bloomberg, the U.S. could sell as much as 800,000 barrels a day overseas, which is more than Libya, Qatar, Ecuador and Gabon produced in December.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every invest. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Russell 2000 Index is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000, a widely recognized small-cap index.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The Citi Global Inflation Surprise Index measure price surprises relative to market expectations. Readings below zero indicate that actual inflation is below market expectations, where readings above zero indicate that inflation is above expectations.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. None of the securities mentioned in the article were held by any accounts managed by U.S. Global Investors as of 12/30/2016.

Victor thinks that you’ve got to get your world view right. The world has changed and the markets are coming around to the view that Trump is going to do what he said he was going to do. Currency markets react. the US dollar down the last 6 weeks in a row after hitting a 14 year high.

…also: Trump Wall Critics Busy Building Walls Themselves

1. Doomsday Clock Dangerously Close to Striking Midnight

1. Doomsday Clock Dangerously Close to Striking Midnight

The Doomsday Clock, started by a group of scientists after the Manhattan Project back in 1947, is updated each January to show how close or how far away we are from the stroke of midnight, which means imminent nuclear holocaust.

Well, according to the latest report from the Bulletin of the Atomic Scientists in January, the clock just moved to two-and-one-half minutes till midnight

2. A Jaw-Dropping 8.6 Million Ounces Of Paper Gold Longs Just Blew Up At The Comex!

With all of the chaos regarding the immigration decrees, I think most observers have lost track of what is really happening with the U.S. economy. Instead they are focusing on the turmoil in the country and the record highs on the Dow.

3. Don’t Count on the Great Rotation

After many false promises and one false start, it is becoming evident that 2017 will be the year the Federal Reserve finally begins down the road towards interest rate normalization. Therefore, it is likely that Ms. Yellen will cause bond yields to rise this year on the short-end of the yield curve. In addition….

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair