Timing & trends

![]()

In This Week’s Issue:

- Three Stocks that meet the Strategy of the Week

- Upcoming Free Webinar – Stockscores Strategy Overview

- Stockscores’ Market Minutes Video -Trading Should Not Be Scary

- Stockscores Trader Training – Trading a Correction

- Stock Features of the Week – These Go Up When the Market Goes Down

Upcoming Free Webinar

Stockscores Strategy Overview

Saturday Nov 5 – 9:00 AM PT, 12:00 PM ET

Click here to register for this free webinar

Description

Stockscores founder Tyler Bollhorn will provide an overview of the Investor and Active Trader strategies. Who they are right for, how much time they take to apply and the basic process behind each.

Stockscores Market Minutes Video – Trading Should Not Be Scary

This week’s Market Minutes video looks at how to avoid fear when trading. That plus the market analysis and my trade of the week. Click Here to Watch

To get instant updates when I upload a new video, subscribe to the Stockscores YouTube Channel

Trader Training – Trading a Correction

There are some signs that the market may enter in to another correction here, not a certainty but certainly a good probability. Here is a list of things to keep in mind when the market is correcting:

1. Stocks Can Go Down To Zero – I often hear investors tell me that they bought a stock because it had fallen so far already, it just had to bounce back. After all, stocks can not go down forever. Yes, that is true, stocks can only go down to zero and then they stop, but a stock that does go to zero is eternally gone. Do not buy something because it appears to be on sale, you should only buy something if it is more likely to go up than down.

2. Never Average Down – averaging down is the practice of buying more of a stock you are losing on as the price falls. Investment advisors sometimes refer to this as dollar cost averaging, but basically, it is all about buying more of a stock that has proven your original decision wrong. If you were betting on a horse that was in last place half way down the back straight of the Kentucky Derby, would you go back to the wager window and add more to your bet if you were able to? Of course not! Buying more when you are wrong is no different, so just wait until the market proves you right and average up.

3. Trade With Who Is In Control – next time you are in an airport, hop on one of those moving sidewalks that speeds you to the gate. When you get off, turn around and hop back on but this time, going against the traffic to understand what it is like trying to trade against the momentum of the market. Yes, it is possible but it sure is a lot harder than going with the flow. The market is no different; you will always have an easier time if you select strategies that are appropriate for the market condition. To understand whether the buyers are in control or the sellers, look at a chart of the stock or market index. If the tops are falling, the sellers are in control. If the bottoms are rising, the buyers are in control. So long as you can draw a line on the chart with a ruler, you can do this analysis and save yourself from a lot of difficulty.

4. Don’t Apply Logic – many investors make the mistake of using logic to make their trading decisions. The market will do a lot of things that do not make any sense because the market has information that you don’t have. A stock that “should” be going higher may not because a large shareholder has learned that there are problems that the general public does not know about. Or perhaps a large shareholder has a liquidity problem and has to sell stock whether they like it or not. You can not argue with what the market does and you will never convince the market that it is wrong. You just have to do what the market tells you to do.

5. Don’t Take More Risk Than You Are Comfortable With – the great enemy of every investor is emotion. It makes us break our rules and lose our discipline. We are emotional because we have an attachment to money that we must learn to minimize if we are going to have a chance of beating the market. The first step toward that goal is to find comfort in the risks that you take. If your exposure to financial loss is too great, you will break the rules and forget your discipline because you don’t want to feel the pain of the loss. If all you are facing is a manageable amount of discomfort, you are more likely to trade well.

6. Markets Predict, Not React – the market is a leading indicator for the economy; it tends to move at least six months early. This means you can not look at the world around you and use what you see to make trading decisions. Since the market looks ahead, so too must you and think about what will happen in the future instead of what has already happened.

7. Diversification Does Not Mitigate Risk – this market is a perfect example of how you can not diversify away risk. An investor with money in bonds, commodities, industrials, technology and banking is feeling losses in all areas. The best way to manage risk is to limit losses. If the market proves you wrong on a decision, get out and take the small loss. Never let small losses grow in to big ones.

8. The Market Never Lies – all markets express the opinions of those who trade it and the wisdom of the crowd is far smarter than you or I can ever be. If you learn how to read the true message of the market, you can make money by doing what it tells you to do. If, instead, you try to outsmart the market, you will likely get your ego delivered to you in the form of debits to your trading account. Do you think you are smarter than thousands of people?

9. Everyone is Smart in a Bull Market – riding a trend is the best way to make money, but many investors confuse their trend timing with investment intelligence. The truly good traders are those that can beat the market in all market conditions. Don’t fall in to a false sense of security if you make money while everything is going up because you are likely to give it all back. For most, profits in the market are just short term loans.

10. Leverage is a Double Edged Sword – all of the problems that we are seeing in the market and the economy right now are because of leverage. Yes, you can improve your return if you borrow money to make money, but always remember that you can also increase the loss potential if the market goes against you. If you use leverage, it is even more important to manage risk and have discipline. If you don’t understand the true risk that the leverage of margin, options and other derivatives provide, don’t trade them.

Here are three vehicles to consider if you think the market is going to go down:

1. T.HVU

A Canadian listed ETF that is based on the Volatility Index. It is leveraged so it will suffer time value decay if the trade is not working so it should only be used as a short term trading vehicle.

2. SDS

Another leveraged ETF, this one goes up twice as fast the S&P500 goes down.

3. QID

Focused on the tech heavy Nasdaq, this is also leveraged and goes up twice as fast the Nasdaq goes down.

Alert: Don’t miss Michael’s great interview with Tyler Oct. 29th/2016 : Tyler Bolhorn on the Markets Today

References

- Get the Stockscore on any of over 20,000 North American stocks.

- Background on the theories used by Stockscores.

- Strategies that can help you find new opportunities.

- Scan the market using extensive filter criteria.

- Build a portfolio of stocks and view a slide show of their charts.

- See which sectors are leading the market, and their components.

Disclaimer

This is not an investment advisory, and should not be used to make investment decisions. Information in Stockscores Perspectives is often opinionated and should be considered for information purposes only. No stock exchange anywhere has approved or disapproved of the information contained herein. There is no express or implied solicitation to buy or sell securities. The writers and editors of Perspectives may have positions in the stocks discussed above and may trade in the stocks mentioned. Don’t consider buying or selling any stock without conducting your own due diligence.

Victor Adair took profits on short Gold positions for gains of ~$90. He’s neutral on gold and remains USD bullish, with yet another reason to be bearish CAD. Our trading accounts have been short US Notes and Bonds for the past several weeks as interest rates have been rising. The stock market looks toppy and much much more.

….related: Tyler Bolhorn on the Markets Today

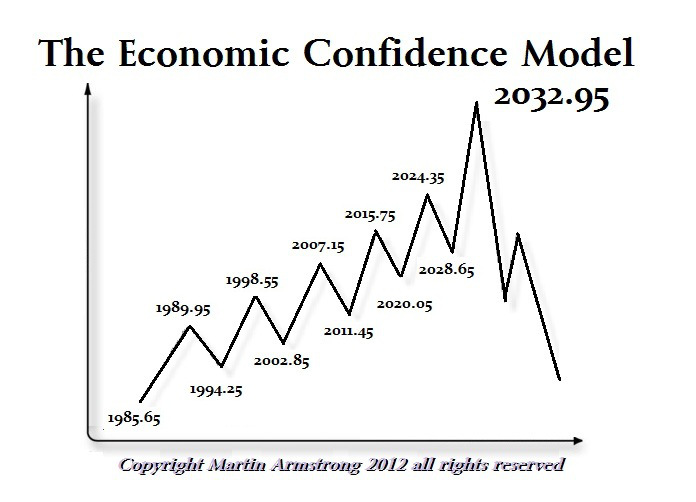

1. The Worlds Top Forecaster, Reputation 2nd to None On The Markets & The US Electlon

1. The Worlds Top Forecaster, Reputation 2nd to None On The Markets & The US Electlon

by Martin Armstrong

Martin Armstrong on the moves he expects in the Stock, Bond, Gold and Currency markets. Martins model’s US election forecast, and when the nearby move up will begin from the current 5000 year interest rate lows.

2. Shelter BEFORE the storm

by Andrew Ruhland

In 2008, many investors were either caught unaware of the systemic risks, or chose to ignore warnings of a major market crash. The financial pain from that (passive or active) decision to do nothing was profound; pain burns deep emotional scars that can be difficult to reverse. The theme of this article is simple: don’t make the same mistake again.

3. Hot Properties: Government Blows Up Canada’s Hottest Industry

by Michael Campbell & Ozzie Jurock

This is what happens when government doesn’t understand markets as sales numbers for Vancouver to October 21st has condo’s down 53% & single family homes down 77%! Thank you foreign buyers tax and Canada’s Mortgage rule changes. Where to from here for Canada’s strongest industry?

Today’s videos and charts (double click to enlarge):

Bonds, Currency, and Stock Markets Video Analysis

Gold & Silver Bullion Video Analysis

Precious Metal ETFs Video Analysis

SF60 Key Charts Video Analysis

SF Trader Time Key Charts Video Analysis

SF Juniors Key Charts Video Analysis

{kind=link}

Morris

website: www.superforcesignals.com

Cyclical turning points tend to feature large numbers of people doing and saying what in retrospect turn out to be amazingly dumb things. Think GM highlighting its line of Hummers just before an oil price spike bankrupts the company. Or half the world betting that tech stocks with infinite P/E ratios would keep rising in 2000. Or pretty much everything that was said and done in the housing market in 2006.

Today’s financial bubble is vastly bigger and more wide-spread than any of its predecessors, so the stupidity is correspondingly global and varied. Some examples:

GM bets big (again!) on gas guzzlers

General Motors third-quarter earnings widely beat expectations

(CNBC) – General Motors reported much higher-than-expected third-quarter earnings on strong North American truck and SUV sales, calming fears that a U.S. auto market slowdown would dent profitability. Overall, GM said third-quarter net income more than doubled to $2.8 billion, or $1.76 a share, from a year earlier.

Rival Ford Motor, due to release third-quarter results Thursday, warned in July that a slowing U.S. auto market would put its full-year profit forecast at risk.

The contrast between the GM and Ford outlooks in part reflects different bets on oil prices in the past. Ford during the past decade spent heavily to boost the efficiency of its top-selling F-series pickup truck by engineering a light, aluminum body, cut back production of large sport utilities and focused on small- and medium-sized cars.

Ford executives have told analysts that with gasoline prices relatively low, it is harder to recover the costs of fuel-saving technology from consumers.

GM stuck with the large SUV market, and now controls more than 70 percent of that market in North America. Models such as the Cadillac Escalade start at more than $70,000.

GM’s results and its outlook depend primarily on strong U.S. and Chinese economies. The company said it lost money in Europe, South America and in Asian markets outside of China.

That’s right, GM is once again on the wrong side of history, and not just because 12-mile-per-gallon SUVs are vulnerable to the next (inevitable) oil shock. Such vehicles’ high sticker prices also make them a luxury purchase for most families, and luxuries will be the first things to go in a downturn.

Meanwhile, relying on the US and China for growth is classic rear-view-mirror thinking. The US is at the tail end of a car loan binge that saw pretty much everyone who walked into a dealership drive out with a 7-year car mortgage. So new buyers will be scarce in coming years. And China, as pretty much everyone (besides apparently GM execs) knows by now, is buying its current growth with a tsunami of new debt that will, as excessive debt tends to do, produce a slowdown if not a crisis in the near future. A safe bet: GM will report losses in 2018 and beyond that more than wipe out the past year’s record profits.

Someone tries to buy Time Warner, again

In 1999 America Online bought Time Warner in a deal that marked the end of the tech bubble. Now AT&T has the same idea. Here’s a great chart from Zero Hedge illustrating the rather terrifying symmetry:

Gigantic mergers are of course a traditional sign of a market top. Before Time Warner there was the RJR Nabisco LBO in 1989 that helped burst the junk bond bubble. See Corporate kleptocracy at RJR Nabisco. And so it has gone back to the dawn of financial capitalism.

Why is this so? Because towards the end of cycles corporate CEOs and their bankers are flush with cash and borrowing power but short on internal growth ideas. New factories are boring and also risky, since so many of them have already been built recently. But buying out a big competitor instantly expands your empire while generating tons of fees that can be milked in various ways. So the deals get bigger and more extravagant — until someone notices that Time Warner is available. Then the system resets.

Bond maturities begin to exceed the human lifespan

Italy’s first 50-year bond sale had huge demand

(Reuters) – Italy sold its first 50-year bond on Tuesday as some investors bet the European Central Bank may soon add ultra-long debt to its asset-purchase stimulus scheme.

About 16.5 billion euros of orders were placed for the bond – 5-1/2 times the expected sale amount, despite concerns over Italy’s banks and an upcoming referendum that could unseat its prime minister.

Many of the fund managers who lend to Italy – and those who have already bought 50-year bonds from France, Belgium and Spain this year – may not live to see it paid back. Those who signed up to Ireland’s 100-year bond in March almost certainly won’t.

Where to begin…well, these are euro-denominated bonds and the eurozone is in crisis, with a growing chorus of former fans now predicting dissolution. What happens to a 100-year bond when the currency in which it’s denominated ceases to exist? Interesting question! And one that will be answered long before these bonds mature.

Keynsians feel free to speak their minds

In normal times, arguing for massive government deficits or exotica like helicopter money and guaranteed incomes is generally done behind closed doors in order to find a way to hide the true nature of the proposal. But in late-stage bubbles so many “innovative” ideas are being put into practice that pretty much everyone’s wish list finds high-profile backers. The following is excerpted from an article by Paul McCulley, a mainstream bond fund manager and, as he is now freely admits, a full-on financial Keynesian. Which of course means he loves government spending of all kinds in every situation:

The deficit is too small, not too big

(The Hill) – First things first: I am (early, via mail) voting for Democratic nominee Hillary Clinton.

My progressive pedigree is robust. I am proudly a liberal Democrat. Not a centrist Democrat, but a liberal Democrat.

And I’m not just a socially liberal Democrat, but a fiscally liberal Democrat.

Thus, while Clinton gets my vote, her insistence at the final debate that her proposed fiscal program will not “add a penny” to the national debt is fouling my wonk serenity this morning.

Every penny of new expenditure, she says, will be “paid for” with a new penny of tax revenue.

Her deficit-neutral fiscal proposal is, I readily acknowledge, better than the status quo, as her proposed new spending would add 100 cents on the dollar to the nation’s aggregate demand, while her proposed tax increases would not subtract 100 cents on the dollar.

Why?

Because she proposes getting the new tax revenue from those with a low marginal propensity to spend, or alternatively, a high marginal propensity to save. To wit, from the not poor, including yes, the rich.

Thus, in simple Keynesian terms, there is some solace in her deficit-neutral fiscal package: It would be net stimulative to the economy, because it would — in technical terms — drive down the private sector’s savings rate.

In less technical terms, it would take money from people who don’t live paycheck to paycheck, who would still spend the same, but just have less left over to save.

And I have no problem with that.

McCulley goes on to explain that the problem with current policy is that the past decade’s trillion-dollar federal deficits were too small because government spending is “investment” while private savings is apparently not. And you can never have too much “investment.”

Again, it’s hard to know where to start. How about with the assertion that private savings doesn’t contribute to growth and progress, when history implies that it’s the only source of productive investment. If government spending produced sustainable growth then the dozens of experiments with massive deficits in pursuit of growth/equity/efficiency would have worked. But they didn’t. Japan’s three decades of record-breaking stimulus produced a flat-lining economy where deflation is now the norm. China’s epic post-2008 infrastructure program quintupled the national debt without making the economy five times as large – thus setting the stage for what looks like an epic and imminent credit crisis. Europe’s experiments with state takeovers of major industries failed across the board.

Anyhow, suffice it to say that in late-stage bubbles lots of ideas that have been previously discredited (or were never seriously considered) seem new again to people who either don’t have a sense of history or do have political agendas dressed up as science. And the result, so far at least, has been the same every time: Debts implode, stocks plunge, economies contract, financial assets fall out of favor and real things start attracting capital. And the people who caused the mess go quiet for a while.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair