Timing & trends

Oct 25, 2016

- The US election is now only about two weeks away. The winner of this election is likely to be… gold. Here’s why:

- Both candidates are eager to increase infrastructure spending, and that’s likely going to open the door to congressional discussion of the issuance of perpetual bonds (aka “perps”).

- That’s inflationary. It is also going to lead to a significant drop in central bank credibility, because central banks will be reluctant to increase the cost of borrowing for governments at a time when governments want to borrow more for their infrastructure spending schemes.

- Please click here now. The longer that central banks wait to increase interest rates more consistently and substantially, the more dangerous the credit bubble becomes.

- Also, bank loan profits have been in a twenty-year bear cycle. That has caused a vicious deflationary bear cycle in money velocity.

- Central banks are prolonging that bear cycle by promoting unprecedented growth of government debt and unfunded social programs.

- The longer that central banks wait before moving interest rates noticeably higher, the more violent the liquidity flows from the government bond markets will be when the rates are finally hiked.

- In my professional opinion, I think most career politicians really believe the world is in a “new era”, where governments can take on unlimited amounts of debt without any real consequences.

- Central bankers are supporting this fantasy world view by pretending that the economic upcycle now in play from 2009 was created by them.

- They created nothing except more danger for pension funds and government bond investors. Central banks effectively engineered a massive flow of bank assets into the stock market, real estate, and government bonds.

- They did it with the biggest attack on Main street citizens in the history of America. Main street workers and pensioners have really been under constant attack since 2009, via QE and low rates.

- The one rate hike that Janet deployed in December of 2015 has been the only real central bank help for Main street in the past seven years.

- That help is just a drop in a bucket. Much more needs to be done in 2017. Main street needs four rate hikes over the next twelve months. I’m predicting they get two, which is better than one or none.

- Western governments need twenty rate hikes from the US central bank. That’s the only way to force them to clean up their disgusting debt-obsessed acts. Sadly, in 2017 I expect most American politicians will cry like babies over just two rate hikes.

- Paul Volker had no problem raising rates to 14% to reign in inflation. Janet Yellen should have even less issue with hiking rates to reign in government lunatics who act more like dictators than politicians. Government size is the disease. Aggressive rate hikes are the cure!

- Gold is very well supported at this point in time. Please click here now. Double-click to enlarge. After bursting upside from a small symmetrical triangle pattern, gold is coiling nicely in a drifting rectangle pattern. My next short term target is $1285.

- Please click here now. Double-click to enlarge this daily bars silver chart. I look for key non-confirmation events between gold and silver, and there’s a great one in play right now.

- On this pullback, gold is trading near the key February highs, and has even traded below them, while silver has held well above its February highs.

- That tells me that inflation is becoming a potential issue, and silver’s relative strength during this pullback is a very positive indication that 2017 will see inflationary pressures strengthen more than they already have in 2016. Two rate hikes in 2017 plus one in December of this year should be enough to reverse the bank loan profits and money velocity bear cycles.

- I’ve predicted a revival in the Chinese gold jewellery market will commence by early 2017, if not sooner. Please click here now. Top Goldman economists are also very excited about the Chinese gold market.

- The bottom line is that gold is well supported by both the Western fear trade and the Eastern love trade.

- Please click here now. Double-click to enlarge. The risk-on dollar is drifting sideways against the safe-haven yen, and is technically overbought. If it starts to decline, I expect gold to race straight to my $1285 short term target zone.

- Please click here now. Double-click to enlarge. The US T-bond has swooned since the Brexit vote occurred, and that’s been a headwind for gold. In 2017, I expect the T-bond to swoon more, but against a background of falling real interest rates and rising nominal rates. That’s good news for gold.

- Gold stocks, like silver, are doing a bit better than gold itself is, compared to the February highs. Please click here now. Double-click to enlarge this daily bars GDX chart. I suggested the $22 area needed to be bought, and the pullback from the $32 area did halt in my target zone. GDX is now trading in a tight range between $22 – $25. I suggested traders could book light profits at $25, and that’s worked out well. Now, I think GDX is getting ready for a rally to $27, and pullbacks to $22 – $23 should be bought again, and sold between $25 – $27 for healthy profits!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Thanks!

Cheers

st

Oct 25, 2016

Stewart Thomson

Graceland Updates

website: www.gracelandupdates.com

email for questions: stewart@gracelandupdates.com

email to request the free reports: freereports@gracelandupdates.com

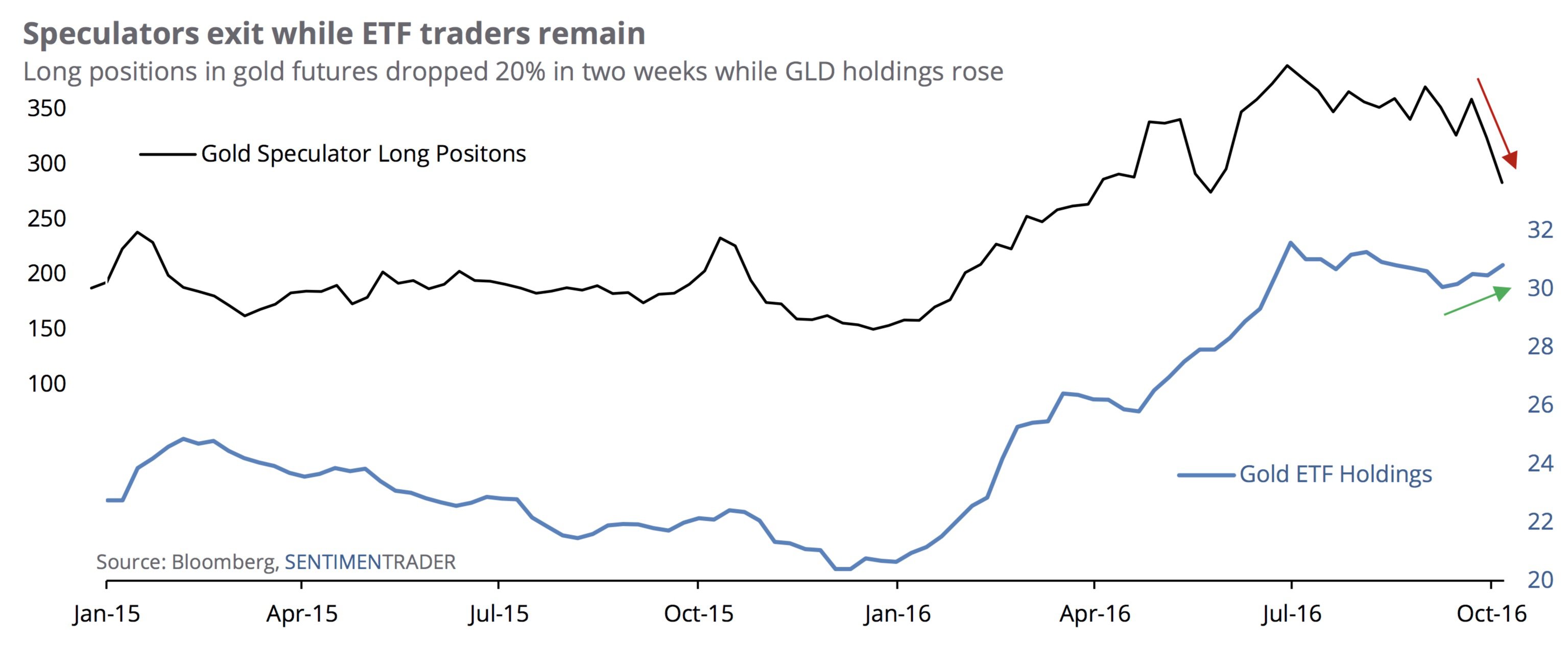

Jason Goepfert of SentimenTrader pointed out that while small speculators have been puking up long gold positions in the paper market, the “smart money” has been buying GLD (see chart below).

…related: in the most recent Committment of Traders – Speculators Close Gold Positions

Here’s a great example of how, no matter what’s happening in the world, there’s always an abundance of compelling, lucrative opportunities.

Here’s a great example of how, no matter what’s happening in the world, there’s always an abundance of compelling, lucrative opportunities.

Lately the British pound has plunged to historic lows.

The pound recently touched a 31-year low against the US dollar, and an all-time low against the euro.

And earlier this month the pound shed nearly 3% of its value in the course of a single day.

That’s simply not supposed to happen to a major currency.

A move of just 1% for a major currency is considered shocking. Currencies are supposed to be stable, not ultra-volatile like a penny stock.

Yet these sharp swings keep happening to the pound, mostly out of Brexit fears.

Emotion has taken over. There’s no rational basis for the pound being this cheap—merely panicked selling on the assumption that everyone else is going to be selling.

This is a broken market. And I imagine it must be nerve-wracking to be living in the UK and watching your currency knocked around like some third-world peso.

Yet anytime markets break down like this and emotions take over, great opportunities almost invariably emerge. We’ve discussed our deep value investment strategy before; financial markets in some parts of the world are so fractured that it’s possible to buy shares of a profitable business for less than the amount of cash it has in its bank account.

That qualifies as a no-brainer– an extremely LOW risk way to generate a built-in profit.

Some colleagues and I are taking this a step further, in fact, and working on a deal to purchase a controlling stake in a listed company that is selling for a fraction of the value of its assets.

(SMPI and Total Access members– watch out for more information on this one.)

These types of opportunities exist almost everywhere that markets have broken down, and the UK is no exception.

I’ll highlight a few simple examples that don’t involve investing tens of millions of dollars.

One asset class that makes sense to consider is collectibles, things like rare coins or wine.

Like gold and silver bullion, collectibles are real assets. And scarce. They’re not making any more 1982 Chateau Petrus.

With collectibles, I prefer to stick to assets with a wide base (i.e. nothing too niche) that are fairly easy to buy and sell.

Art and antiques, for example, can be difficult to value and sell without going to an appraiser and broker.

But certain luxury watch brands, on the other hand, can be sold in minutes, especially the historic high-end Swiss manufactures like Patek Philippe, Rolex, Jaeger-LeCoultre, IWC Schauffhausen, and Vacheron Constantin.

Many of these watches are hand-made and they are NOT mass-produced, so they’re scarce and extremely popular.

Right with the British pound at around $1.22, luxury watches being sold in London and priced in pounds can be had at a steep discount to their US dollar prices across the ocean.

A recent year Patek Phillippe Calatrava model (5119G) is selling for about GBP 12,300 in the UK right now, or right around $15,000.

(And that doesn’t include the benefit of receiving a VAT refund.)

This same watch can easily sell for more than $20,000 in the US.

You could even sell it yourself on Amazon or eBay at a steep discount to that price and still make a very healthy profit.

Technically it should even be possible to sell the watch first in US dollars, and then purchase it in pounds from a UK vendor once you collect the money from your buyer.

That way you can generate a solid profit without actually using any of your own money.

It’s easy to be fearful when markets break down, when terrifying political candidates emerge, and when it seems like World War III is breaking out.

But as a result of all that fear, there are countless opportunities like this to generate low risk, built-in profits.

And thanks to our modern technology, these opportunities are available to anyone in the world who has access to the Internet… and a little bit of hustle.

….related from Victor Adair & Michael Campbell: Live From The Trading Desk: An Astonishing New Low

The British Pound just set a 168 year low, proving what Victor regularily says that currency markets often trend far further than expected. Also Victor short bonds expecting higher interest rates, short crude oil and more…..

Let me cut right to the chase: The global financial markets … entire economies … and even political systems and philosophies — will soon start spiraling out of control.

So don’t kid yourself. The relative calm in the markets of late is a freak occurrence. You’re about to see plenty of action.

We will hit the back wall of the financial hurricane that started in 2008. That part of the financial crisis where the governments of the world stepped in to try and save things, but which are now infected with an even worse disease: Debt-to-GDP ratios that over the next five years will bankrupt first Europe, then Japan and then, the United Sates.

We will hit the back wall of the financial hurricane that started in 2008. That part of the financial crisis where the governments of the world stepped in to try and save things, but which are now infected with an even worse disease: Debt-to-GDP ratios that over the next five years will bankrupt first Europe, then Japan and then, the United Sates.

It won’t be pretty. It will affect everything you do. Everything you own. Every investment you make. Your lifestyle. Your children and grandchildren’s future.

No, I am not being an alarmist or screaming fire in a packed theater. I am merely telling it like it is, for if you understand the forces that are now converging upon the world, you will see the same things coming that I do.

Just take a look around:

![]() Financial markets are starting to swing wildly. Everything from stocks and bonds, to commodities are now on a roller coaster. Whenever that happens — especially after a period of relative calm — it means something big is coming.

Financial markets are starting to swing wildly. Everything from stocks and bonds, to commodities are now on a roller coaster. Whenever that happens — especially after a period of relative calm — it means something big is coming.

Big moves that could destroy your wealth in a heartbeat. Or, big moves that you can capitalize on for big profits. The choice is yours.

![]() Entire economies are quaking. Europe is the worst of them. But there are also problems in China (though they won’t derail China’s long-term growth). There are problems in Australia, Canada, Great Britain. In Brazil, Argentina, Mexico, Venezuela. In Russia.

Entire economies are quaking. Europe is the worst of them. But there are also problems in China (though they won’t derail China’s long-term growth). There are problems in Australia, Canada, Great Britain. In Brazil, Argentina, Mexico, Venezuela. In Russia.

And then there’s the Middle East, where countries are being kicked in the butt by still low oil prices, not to mention rising domestic unrest and terrorism.

![]() Even political systems are under stress. Third parties are rising in strength all over Europe. New Neo-Nazi groups. Separatist groups. Secession parties. Terrorist groups. Cultural clashes. Syrian refugee crisis. And more.

Even political systems are under stress. Third parties are rising in strength all over Europe. New Neo-Nazi groups. Separatist groups. Secession parties. Terrorist groups. Cultural clashes. Syrian refugee crisis. And more.

All part and parcel of the rising war cycles that I’ve been warning you about, conditions that will not abate until at least the year 2020.

So why is all of this happening? Why will it get worse in the years ahead?

It’s actually very simple: You are witnessing the death of communism and Western-style socialism.

It is not the demise of capitalism, as so many think. It’s the opposite:

The death of big government. The death of the state taking care of you. The death of Keynesian economics.

The death of governments that are so indebted from fiscal mismanagement and making promises to you that they could never keep — that they are now waging financial repression against you …

While at the same time finding scapegoats in the form of other countries, other political systems and parties, to blame.

We are entering a crash and burn phase for government. Especially Western governments and their socialist and safety net experiments of the last several decades. Of their currency experiments, their trade wars, their inept policies, bureaucracies, tax systems and more.

It will manifest itself mostly in the sovereign bond markets of Europe and the United States, where interest rates started moving up — and bond prices started falling — even before Janet Yellen started talking about raising rates.

And all the chickens will start coming home to roost, when the citizens of those countries … and investors everywhere … realize that the emperors of western socialized countries — their leaders and governments — really do have no clothes.

And all the chickens will start coming home to roost, when the citizens of those countries … and investors everywhere … realize that the emperors of western socialized countries — their leaders and governments — really do have no clothes.

And then, nearly all markets will swing even more wildly than they are now.

I repeat: This is the first year of five years in total that will be a roller coaster ride through hell. And unless you start preparing now, it will gut your wealth.

My best advice right now:

First, stay out of U.S., Japanese and European government debt. No matter what anyone tells you, sovereign debt markets are soon going to become the biggest disasters of all time.

Second, steer clear of all foreign currencies. Stay mostly in dollars. I know it seems illogical, but it isn’t. As the global economy weakens and geo-political tensions domestically and internationally ramp ever higher, wreaking havoc in almost every corner of the globe …

More and more savvy money will flee to our shores and to the dollar — even as our bond markets tumble.

Third, build your own war chest, to go after the opportunities that are coming.

Some of the opportunities I see coming …

- The next leg up in gold, silver and mining shares.

- A breakout in the Dow above 18,500 on a monthly basis that will kick off a move to at least 31,000.

- Oil shocking everyone, making yet another new low, then turning around next year and rocketing higher.

The profit opportunities for the rest of this year and onward will simply be off the charts. It’d be foolish not to go after them.

Best wishes,

Larry

also from Michael Campbell: Pubilc vs private healthcare solutions: Time To Rock The Boat

The 2016 US presidential election between leading candidates Republican Donald Trump and Democrat Hillary Clinton has been unusual in that allegations of rape have cropped up during the campaign with Bill Clinton accused of rape, Hillary Clinton accused as an accessory, and Donald Trump accused of groping women without their consent. However, the core issue of the campaign — indeed the reason the Trump campaign exists — is citizen anger at a growing sense that their country itself has been abused at the hands of a financial elite. And this core campaign issue is lost as the back and forth sexual recriminations between the campaigns deflects attention from a critical issue.1

Something’s Wrong — And It’s Big

But citizens increasingly know something is wrong – and that realization is despite soaring stock markets and bond markets since the Great Financial Crisis of 2008.

The current US administration promotes an unemployment rate of 5% (down from 10% in 2009) as a sign that the economy has recovered from the Great Financial Crisis.

Flying in the face of this promotion is the fact that the number of adults not in the US labor force is 94 million people in September 2016 up from 80 million not in the labor force in October 2008. Excluding 14 million people from the US labor force so that they are not counted as unemployed helps to statistically reduce the unemployment rate.

And 41 million Americans now remain on food stamps up from 28 million in October 2008.

These statistics, and there are many more, show us that despite soaring financial markets fuelled by the Fed’s 0% interest rates, there is no real recovery underway. Soaring financial markets with moribund labor markets and rising prices for essential goods do not signal a healthy economy. Donald Trump knows it as do US voters.

On September 5, 2016 Trump warned that the Federal Reserve had kept rates artificially low and “It’s an artificial market. It’s a bubble.” warning that the bubble economy that the Federal Reserve has created had resulted in “very scary scenarios”. On September 6 Clinton immediately responded to Trump by saying that “presidents and candidates should not comment on Fed actions”. It was also revealed on September 6 that Goldman Sachs was banning partners from contributing to Trump’s campaign from September 1 forward.

The Rape of America (and Europe and Canada)

By (correctly) identifying the Fed as the source of economic distortions and the coming crash and impoverishment of the American people, Trump was alarming many in the financial industry by lighting fires of inquiry that cannot be put out. And the trail of evidence leads back not only to the Fed but to Goldman Sachs as well.

The rape of America has been a relatively simple process and involves a few key elements:

1) A debt-based currency system run by the central bank.

With a debt-based currency system and the ability of banks to instantly credit money into creation, the age-old formula of blowing bubbles can be effected by continually lowering interest rates and increasing the amount of currency in circulation thus driving speculation continually higher. This creates Trump’s “artificial markets”.

2) Recognize the inverse relationship between real interest rates and gold prices

Gold has historically limited the ability of central banks to blow bubbles by soaring in price. Former Clinton administration Treasury Secretary Larry Summers in his seminal 1985 paper with Barsky identified that the primary factor driving real gold prices was real interest rates (i.e. nominal interest rates minus the inflation rate). As inflation rises from loose central bank monetary policy, the real price of gold measured in constant dollars also rises and is the principal “tell” of those loose monetary policies. The principal driver of consumer goods inflation is monetary policy — as more money is created, goods prices also become more expensive. Indeed, the US dollar now buys 1% of what it could buy in 1913 when the Fed was created. But as was seen in the late 1970s, when inflation rages gold rages more. Central bankers are then forced to choose between abandonment of their paper money and bonds for real assets or to stop their money printing.

Now, Summers and Barsky were so certain of their observation that they wrote “(t)he negative correlation between real interest rates and the real price of gold that forms the basis for our theory is a dominant feature of actual gold price fluctuations.” [“Gibson’s Paradox and the Gold Standard“, Summers and Barsky, 1985 NBER working paper 1680 http://www.nber.org/papers/w1680.pdf]. The principal driver of the gold price was real interest rates — as they collapse due to inflation, the price of gold soars. The implication is that if you would like to sustain loose monetary policy for a protracted period, it is necessary to be able to control the price of gold.

And as we will see, the ability to control the bond market was almost lost in the late 1970s as both inflation and the price of gold soared forcing nominal interest rates up to the high teens before gold’s rise was arrested.

3) Convert the world’s principal gold markets from trading gold to trading paper gold thereby short-circuiting price discovery in the global gold and bond markets

The central characteristics of gold are that it is rare and of universally of value — gold has a 4,000 year history as a monetary asset as it cannot be debased or created without limit as fiat paper money can. With the 1987 creation of the London Bullion Market Association (LBMA) by the Bank of England (https://www.bullionstar.com/blogs/ronan-manly/from-bank-of-england-to-lbma-the-independent-chair-of-the-lbma-board/), gold trading was progressively thereafter converted to paper contract trading through the creation of “unallocated gold contracts” without gold backing and price discovery was thereby thwarted as these contract claims on gold can themselves be created and traded without limit (http://www.safehaven.com/article/42600/transition-of-price-discovery-in-the-global-gold-and-silver-market). By deflecting claims for gold into paper gold contracts, today there are an estimated 400 million to 600 million oz of claims for gold at the LBMA without gold backing and daily gold trading has reached 200+ million oz of gold per day (vs global annual gold mine production of ~ 100 million oz).

Price discovery of gold, and the ability of the price of gold to respond to real interest rates, has thus been greatly arrested — the knock-on and targeted effect was that the bond market was also short-circuited allowing the secular reduction of interest rates (and creation of mountains of debt in our debt-based economies). Central bankers could now defy gravity — for a while.

The following graph using the Bureau of Labor Statistic’s consumer price index (CPI) method of calculating inflation from 1980 held constant shows the 1987 decoupling of the price of gold’s historic inverse relationship with real interest rates with the creation of the LBMA — gold no longer responded by rising in price as real interest rates became negative and central banks were free to blow bubbles. Note also in the graph (where the inverse price of gold is plotted on the right) that in late 1982 the price of gold started to surge driving real interest rates to almost 9% higher than the rate of inflation before money started to return to bonds from gold.

Source: Reginald Howe, GoldenSextant.com. 1980 CPI computations by John Williams at shadowstats.com

Another issue given Goldman Sachs response of banning Goldman partners from donating to the Trump campaign is the key role of Goldman Sachs’ subsidiary J. Aron and Co. gold traders in advising central banks to sell and lease gold in the 1990s. Former gold banker and author Ferdinand Lips wrote at pages 123 to 124 in his book Gold Wars — The Battle Against Sound Money From a Swiss Perspective that he came to recognize in 1996 that Goldman’s J.Aron and Co. were the central advisors to central banks behind their gold policy to aggressively sell and lease gold into the market — thereby further depressing the price of gold (http://www.safehaven.com/article/35086/the-role-of-goldmans-jaron-and-co-metal-division-in-capping-gold-prices). Mr. Trump’s reference to a bubble economy driven by central banks and artificially low interest rates leads inexorably back to Goldman Sachs and the LBMA.

4. Now, continually lower interest rates over the next 30 years creating a succession of financial bubbles — when the bubbles pop, bail-out the banks and not borrowers

With gold no longer properly signalling artificially low interest rates by central banks this enabled the creation of a of a fake bubble economy as identified by Trump. When you rig the global price of gold, you rig the global bond market. Global credit market borrowing now totals $230 billion or 340% of global GDP more than double the historically sustainable level of 150% of GDP.

Central bankers have responded to the succession of bubbles and financial crises of their own creation by bailing-out the banks (lending up to $16 trillion to banks during the Great Financial Crisis) and prescribing lower interest rates and more debt compared to the needed monetary system reform and debt write-down to stabilize our economy. And Alan Greenspan who was appointed to the Fed in 1987 has retired and has been knighted as Sir Alan Greenspan by the UK establishment. A job well done.

The Bubbles are Popping but the Debt Remains

With the creation of the debt bubble and the consequent sequence of financial and economic bubbles, the US economy is now so distorted by Fed policy that even with the zero interest rates the economic output is growing at 1% and is declining. We are at the terminus point of exceptionally loose money started in 1987 by the Bank of England and the Federal Reserve.

With assets stripped from their hands and large numbers of Americans out of work and on food stamps, Mr. Trump’s words have not elicited reasoned discussion. Not only has Trump been told not to talk like that but the recriminations back and forth of sexual impropriety have stopped discussion of this core campaign issue reflecting American voter concern. And the hackneyed accusation of anti-semitism against Trump further muddies the waters (http://wallstreetonparade.com/2016/10/new-york-times-writer-suggests-donald-trump-is-an-anti-semite-for-his-reference-to-banking-conspiracy/) and with hedge fund donations to Trump totalling $19,000 vs 48.5 million for Clinton, we get some sense of the Candidate reflecting the interests of Wall Street. And this mirrors the Obama administration which executive structure was determined by Citibank (http://wallstreetonparade.com/2016/10/wikileaks-bombshell-emails-show-citigroup-had-major-role-in-shaping-and-staffing-obamas-first-term/).

The question now remains whether there will be any further discussion of this key issue broached by Trump and reform forced by the electorate or whether America will proceed with its politicians bickering about sex as the financial, economic and monetary system proceeds over the waterfall.

Notes:

1. The well documented alleged rape of nursing administrator Juanita Broaddrick in 1978 by former President Bill Clinton and Broaddrick’s subsequent intimidation into silence by Democratic candidate Hillary Clinton has revolted many long-time Democratic supporters (for a catalogue of some of Bill Clinton’s alleged crimes against women see: https://www.lewrockwell.com/2016/01/roger-stone/clintons-criminals/). And Hillary Clinton’s successful 1975 legal defence leading to the release of a rapist who raped 12 year old Kathy Shelton and audio tapes of Clinton laughing at the process as well as her using a defence that the child had a “tendency to seek out older men and engage in fantasizing.” leaves observers disgusted. The tape recording of Republican candidate Trump bragging about what women let a star like him do to them as well as the fusillade of accusations by women of unwanted groping and kissing by the Republican further leaves voters shocked — and not thinking. And more allegations are sure to follow in this political season.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair