Timing & trends

Quotable

“If you don’t know where you are going, any road will get you there.” – Lewis Carroll

Commentary & Analysis

After the Bank of Japan (BOJ) did what it did, a boatload of economics Ph.D. descended on the airwaves and internet blogs this morning to share their usual inside baseball stuff in an effort to explain the “bold” move by the Bank of Japan—targeting the yield curve. But outside the minds of economists who actually condone such tinkering will any of this matter?

Japan has blazed the trail to zero rates and beyond. Suckers in Europe have followed because it has worked so well for Japan. This action on the part of the CBs begs the question: To what good have any of your policies done, short of providing liquidity to help stabilize the banking system and credit markets in the midst of the crisis? The BOJ has been at this game of ZIRP off and on (mostly on) for the last 20+ years. Growth in Japan is still morbid. Debt to GDP is off the charts. And deflation is still the order of the day.

Some seers are saying the BOJs decision not rely on increases in the money supply, and just maintain its current level of quantitative easing, is a hint to the Japanese government that monetary policy isn’t getting the job done and structural reforms are needed in order to change the economic trajectory.

To review, Prime Minister Abe was elected in December 2012. Upon taking office he enunciated a three arrow strategy in order to break the grip of deflation in Japan and grow the economy. These three arrows were: 1. the pressuring of Bank of Japan into launching unprecedented aggressive monetary easing and setting a target of 2% inflation to support a target of 2% real GDP growth (4% nominal growth); 2. a blowout deficit-financed supplemental government budget filled with new public works spending; and 3.

a program of reforms to achieve growth through stimulating private investment. The third arrow, the most important if you aren’t a hedge fund manager, is the most important. And so far this arrow hasn’t left the quiver.

Why? Simple answer: Crony capitalism doesn’t want real reform (Brexit a perfect summary of that.) Big business doesn’t want real competition. This is why CEOs of our major corporation are joined hand-in- glove with our political leaders. Big investors love the financial asset bubble; why make changes?

I am not sure if the BOJ is implicitly sending a message to the Japanese political class. But I do know it is past time all central bankers reach back and find their spines, assuming they ever had such a thing to begin with, and explicitly tell their respective governments—we can do no more. Financial repression isn’t working for most of our citizens; save those with access to capital. Is there any wonder why hedge fund manager extraordinaire Ray Dalio, and his cronies, are constantly creating all kinds of arguments why the Fed shouldn’t raise rates—“OMG, they can’t raise rates.” Hell, I think if Ludwig von Mises were pulling down a cool $500+ million a year, as did Dalio in 2015, he’d be all for financial repression too.

Add to this shit-show the fact no one yet understands the potential unintended consequences of negative rates. The prospect of an estimated $12 trillion in paper issued at negative rates is an anathema to a market system that allocates finite resources through proper price signals, and should terrify anyone with a logical brain cell left in their head.

Time for real structural reform, or to put it another way, time for Mr. Market to start clearing away the dead wood so fresh entrepreneurial growth can resume is way past due. That signal for the entrepreneur is sent first and foremost through the rate of interest (the signal now being sent to the market will be responsible, at some point, for the trillions of dollars in capital flowing straight down the rabbit hole). But instead of CBs doing what we know works (does anyone remember a man named Paul Volcker), let’s just keep stumbling along in monetary and fiscal wonderland, keeping those political contributors happy, and expecting everything to work out for the best. It’s such a grand idea it requires a Ph.D. in economics to understand it.

Thank you.

Jack Crooks

President, Black Swan Capital

www.blackswantrading.com

Boston Fed President Eric Rosengren recently rattled markets when he warned that low-interest rates were increasing the temperature of the U.S. economy, which now runs the risk of overheating. That sunny opinion was echoed by several other Federal Reserve officials who are trying to portray an economy that is on a solid footing. And thus, prepare investors and consumers for an imminent rise in rates. But perhaps someone should check the temperatures of those at the Federal Reserve, the idea that this tepid economy is starting to sizzle could not be further from the truth.

In fact, recent data demonstrates that U.S. economic growth for the past three quarters has trickled in at a rate of just 0.9%, 0.8%, and 1.1% respectively. In addition, tax revenue is down year on year, S&P 500 earnings fell 6 quarters in a row and productivity has dropped for the last 3 quarters. And even though growth for the second half of 2016 is anticipated with the typical foolish optimism, recent data displays an economy that isn’t doing anything other than stumbling towards recession.

The Institute for Supply Management Purchasing Manager’s index for the manufacturing sector during August fell into contraction at 49.4, while the service sector fell to 51.4 compared to 55.5 in July, which was the lowest reading since February 2010 and the biggest monthly drop in eight years. And the recent jobs report was also full of disappointment too, with just 151,000 jobs created in August and a decline in the average work week and aggregate hours worked.

But our Federal Reserve is not the only central bank making statements troubling to stock and bond prices. The President of the European Central Bank (ECB), Mario Draghi, threw all the major averages into a tailspin at a recent press conference by failing to indulge markets with a grander scheme to destroy the euro. When asked if the ECB had talked about extending Quantitative Easing (QE) at its meeting, Draghi had the gall to make the egregiously hawkish announcement that they “did not discuss” anything in that regard. This mere absence of a discussion regarding extending or expanding QE caused the Dow to shed nearly 400 points on Friday and spiked the U.S. Ten-year from 1.52% to 1.68%. Indeed, stock and bond prices plunged across the globe.

It appears that nothing is ever enough to satisfy global stock and bond markets that are completely addicted to central bank stimulus. Mr. Draghi has managed to drive rates so low that they are now in effect paying European companies to borrow–yet markets want even more.

That’s correct, it’s no longer just sovereign debt that offers a negative yield. According to Bloomberg, French drug maker Sanofi just became the first nonfinancial private firm to issue debt at yields less than zero. Also, shorter-term notes of some junk-rated companies, including Peugeot and Heidelberg Cement, are yielding about zero percent.

Christopher Whittall of The Wall Street Journal reports that as of September 5th, €706 billion worth of investment-grade European corporate debt was trading at negative yields. This figure represents over 30% of the entire market, according to the trading platform Tradeweb. You can attribute this to the fact that global central bank balance sheets have increased to $21 trillion from $6 trillion in 2007, as central banks continue to flood the markets with $200 billion worth of QE every month.

The bond bubble has now reached epic proportions and its membrane has been stretched so thin that it has finally started to burst. As mentioned, not only did U.S. yields spike on the Draghi disappointment but the Japanese Ten-year leaped close to positive territory from the all-time low of -0.3% in late July. And the German Ten-year actually bounced back into positive territory for the first time since July 22nd.

What did Mario Draghi say that was so unsettling to the Global bond market and caused speculators that have been front-running the central bank’s bid for the last eight years to panic? He didn’t avow to sell assets; he didn’t even promise to reduce the 80 billion euros worth of bond buying each month. All he did was fail to offer a guarantee that the pace of the current bond buying scheme would be increased or extended beyond March 2017. That alone was enough to cause yields around the globe to spike and stock markets to plunge.

This is merely the prelude of what is to come once the ECB and Bank of Japan reverse their monetary stimuli; or when the Fed actually begins its rate normalization campaign. Just for the record, the Fed’s first hike in ten years, which occurred last December, does not count as a tightening cycle.

The bond bubble has grown so immense that if, or when, central banks ever begin to reverse monetary policy it will cause yields to spike across the globe. But as recent trading volatility has proved, it won’t just be bond prices that collapse; it will be every asset that is priced off that so called “risk free rate of return” offered by sovereign debt. The painful lesson will then be learned that negative yielding sovereign debt wasn’t at all risk free. All of the asset prices negative interest rates have so massively distorted including; corporate debt, municipal bonds, REITs, CLOs, equities, commodities, luxury cars, art, all fixed income assets and their proxies, and everything in between will fall concurrently along with the global economy.

Perhaps after this next economic collapse central banks will deploy even more creative ways to increase their hegemony and destroy wealth; such as banning physical currency and spreading electronic helicopter money around the world. In the interim, having a portfolio that hedges against extreme cycles of both inflation and deflation is essential for preserving your wealth.

related:

OUZILLY, France – “In the short run,” says billionaire investor Warren Buffett, “the stock market is a voting machine. In the long run, it’s a weighing machine.”

OUZILLY, France – “In the short run,” says billionaire investor Warren Buffett, “the stock market is a voting machine. In the long run, it’s a weighing machine.”

Put another way, in the short run, the stock market responds to myths and fads. In the long run, these give way to facts.

Outsized Delusions

Remember, myths are not necessarily untrue.

But whatever truth they have seeps from human imagination, not from facts imposed by the outside world.

Gravity, for example, is a fact. You jump out of a second story window; it doesn’t matter how hard you flap your arms or what you think, gravity will pull you down toward the sidewalk.

Corporate profits, too – though they can be manipulated and massaged – are facts. Mythical profits don’t pay real bills.

But there are other “facts,” too… those that owe their existence entirely to our mythmaking ability.

They may begin life as plausible observations. But then they have a way of growing… expanding… mutating into outsized delusions – ones that may cost a nation its money and its soul.

Were the pharaohs divine?

Apparently, the ancient Egyptians thought so. For 3,000 years, they were so devoted to this myth that they applied almost the entire economic surplus of the Nile Delta to building monuments in their honor.

We know of no physical tests for divinity. You might say, “Someone who is divine can’t be killed.”

On occasion, they put a Thutmose or a Neferkare to the blade; they died like everyone else.

“Gods don’t die,” said the doubters. But Jesus did. And Christian scholars spent centuries arguing about how and why that was possible.

In the end, a divinity can do what he wants. He can appear dead… or seem to be mortal in other ways. There is just no way of knowing.

For all we know, the pharaohs were divine. Certainly, it was convenient to believe it – at least for them and the elite surrounding them.

Master-Race Myth

Adolf Hitler (among others) promulgated the myth of a master race.

At first, people took him for a crank. The intelligentsia made fun of him. The “Austrian corporal,” they called him. Or the “little housepainter.”

Even when Hitler became chancellor in 1933, the thinking in polite society was that he could be “tamed” by dutiful functionaries and the weighty responsibilities of his office.

Instead, the myth of the Übermensch (an idea Hitler borrowed, completely out of context, from Nietzsche) took hold of large numbers of Germans.

Again, there was no way to prove it wasn’t so.

And as time went by, more and more people found it agreeable; it gave them a way to feel superior… and perhaps buy a house down the street that used to be owned by Jews, at a bargain price.

Besides, the Austrian corporal was making German industry the envy of the world… with factories booming and full employment. (This, too, was a myth: Hitler had created a bubble economy based on dead-end military spending.)

But as more and more people found it convenient to believe the myth, the more self-evident it became. Soon, they were marching to Stalingrad.

Myths stretch or shrink depending on what you think of them.

According to a new report from Brown University, next year the total sum committed to the War on Terror will rise to $4.7 trillion.

That’s an amount equal to nearly one-quarter of annual U.S. GDP, transferred from the public to the terror-fighting industry.

The War on Terror is the longest war in U.S. history. And for the security industry, it’s the most profitable war ever. Of course it is real!

(When President George W. Bush first announced the War on Terror, we guessed it would do no good… and that it would cost “more than a trillion dollars.” We were off by $4 trillion!)

Bomb, Drone, Kill

There is a word for this phenomenon. We can’t remember what it is. “Self-fulfilling” will have to do.

The more you focus on it… the more real it becomes. Give out the word that terrorists are lurking around every corner. Bomb them, drone them, kill them. (Some estimates put the number of dead at more than 1 million.)

See something, say something! The more enemies you make… the more enemies you have. Then there is no need to look for evil; it will find you!

“Another suspicious package found…” says a Bloomberg headline this morning.

Sticking with round numbers, the War on Terror has cost about $350 billion a year over the last 15 years. Like the pyramids, the project absorbs much of the nation’s surplus output.

But wait. Where did the feds get so much money? Were taxes raised to cover it? Was spending cut in other areas?

Nope.

How was it financed?

With debt, borrowed at the lowest interest rates since Ramses and Amenhotep.

At current yields and current inflation, the U.S. federal government can borrow at almost no cost. It is free money.

But that, too, is a myth…

Regards,

Bill

Market Insight

Attention, tech investors…

Today’s chart tracks the performance of America’s big tech stocks by way of the Technology Select Sector ETF (XLK).

And it compares it to the performance of the big S&P 500-tracking ETF, the SPDR S&P 500 ETF Trust (SPY).

|

As you can see, starting in July, tech stocks have exploded higher, relative to the broader market.

BY CHRIS LOWE, EDITOR AT LARGE, BONNER & PARTNERS

Deutsche Bank and Commerzbank are presently discussing merger talks. The fact that these meetings are occurring, is a signal that Germany’s banking troubles are indeed accelerating.

They are desperately seeking ways in order to cut costs and improve profitability. These plans include restructuring and job cuts using most highly unconventional measures. Last June 2016, Reuters cited anonymous sources as saying that Commerzbank was exploring the option of hoarding billions of euros, in vaults, as a way of avoiding paying a penalty to the European Central Bank which is due to negative interest rates.

Their main problems are derived mostly from both low and negative interest rates. These lenders are used to depending on interest rate margins for income while offering some services to depositors at either low or no cost. Low interest rates have significantly eroded these banks’ abilities to make money. It has become difficult for German banks to give incentives to their customers so as to keep their money in their financial institutions. These inefficiencies and the intense competition within the German banking sector have already led to serious financial difficulties. If one combines these factors with the new challenge of declining interest rates, what possible positive impact can they expect to incur?

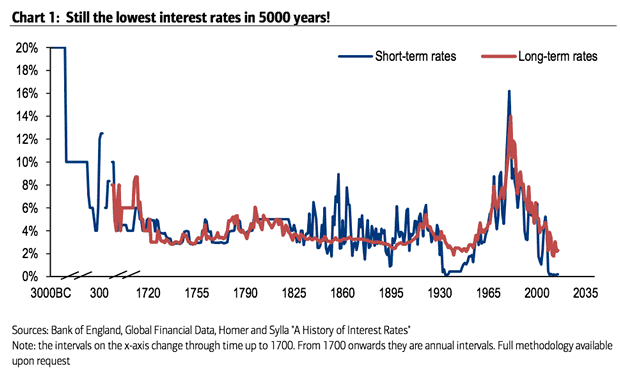

Interestingly, rates are not just low within the context of American history but they also happen to be at their lowest levels ever in over 5,000 years of civilization.

5,000 Years Of Interest Rates – Rates Lower Than 1930’s Depression Era

Deutsche Bank is not merely Germany’s biggest bank but the political role that it plays in Germany is unique when compared to other countries. Deutsche Bank’s importance to Germany is many times greater than that of an investment bank like Lehman Brothers was to the U.S., in 2008. Deutsche Bank is technically a private bank, however, it is informally tied to the government and formally tied to most major German corporations. The banks’ fate will have an impact on all of Germany.

The Italian banking crisis is not only Italy’s problem!

Italy’s non-performing loan issues have now become common knowledge. Who will be forced into dealing with the repercussions of settling Italy’s impaired debt? That is a political question, and the answer depends, in large measure, on who holds Italian bank debt.

The U.S banks are not shielded from these European Continental banking problems. There is a substantial amount of uncertainty and risk.

The consequences of these failures pyramid the crisis due to the European Unions’ regulations. The European Central Bank (ECB) and the Central Banks of member countries cannot bail out failing banks by recapitalizing them. The bail-in strategy is, in theory, a mechanism for ensuring fair competition and stability within the financial sector, across the Eurozone.

The bail-in process can potentially apply to any liabilities of the institution that is not backed by assets or collateral. The first 100,000 euros ($111,000), in deposits, are protected in the sense that they cannot be seized, whereas, any money above that amount can be.

Germany insisted that the bail-in process should prevail.

The Bank for International Settlements stated that German banks are the second most exposed to Italy, after France, with a total exposure of $92.7 billion. Demand for gold has increased!

Italy’s ongoing banking crisis is presenting yet another threat to the stability of the ECB.

Commerzbank’s financial statements revealed that their Italian sovereign debt exposure was 10.8 billion euros ($12.1 billion).

Deutsche Bank’s net credit risk exposure to Italy is 13.3 billion euros as of the end of December 2015. Its’ gross position in Italy is 35.4 billion euros. Deutsche Bank is sitting on $41.9 trillion worth of derivatives.

The consequences of large banks failures are significant

Gold Is The Only ‘Safe Haven’ Left in the World

Gold has remained as a form of currency for many centuries. Whenever countries followed a strict gold standard and used it as their currency, those economies were very stable. But, governments have always surpassed their means, with their costly spending, and have to leave their gold standard so as to fund their inefficiencies. Currently, gold is now beginning its’ multi-year “BULL MARKET”. Gold is the only ‘asset class’ which will maintain its’ ‘store of value’ during this impending crisis which is on the near horizon. The ‘Gold mania’ is about to be ‘unleashed’. While global Central Banks are now implementing ‘negative interest rates’, this is the perfect scenario for gold to surge much higher.

Gold does have a historical store of value characteristics. It is held by Central Banks and institutions as a reserve. They do not want to sell it; on the contrary, many of them want to buy still more and accumulate it. Therefore, gold’s characteristic role, in regards to sovereign reserves, is still intact even amid the fascinating evolution of Central Banking and institutional finance that we are witness to, today.

….related:

Featured guest Dennis Gartman is very bearish the Euro currency, Oil based on abundant supply and Stocks. The US election will have a significant impact on prices. Bottom line, he likes cash for the next six months, longer term…..

To listen to the entire show go HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair