Timing & trends

“A slowing Chinese economy, a flip-flopping Oil market, talk of an American recession and the future of the Euro Zone still up in the air, the World economy is plagued with insecurity. Is a global recession imminent, how steep will the downturn be and where is the safest place to invest today.” Jim Rogers interviewed on these topics in Moscow (interview 24 minutes):

…..related: Michael Campbell on – The Formula For Social Unrest & Political Upheaval

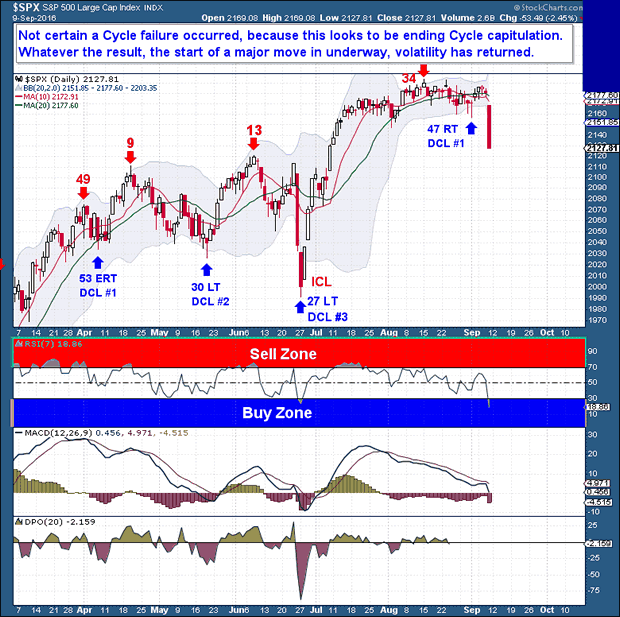

Friday’s 2% + decline in the equity markets was impressive. After a record run of low volatility and muted price action, equities suddenly awakened and exploded lower. This is exactly the sort of action I expected (although favoring upside price move) when I titled last week’s report Expecting Volatility. The market had been setting up for a big break for quite some time.

Extended periods of a lifeless, low volume trading range usually give way to volatility and significant moves in price. Going forward, at least over the short term, I expect we will see a series of 1% (plus or minus) moves in the daily indices. Although Friday’s break has significant bearish technical implications, it is too early to assume that the next extended move will be lower. What we canassume, and with a high degree of confidence, is that the next major market move has started.

The primary problem with being more definitive on direction is uncertainty around the Daily Cycle (DC). In a traditional DC (40-45 days), the low on September 1st – day 47 – could easily mark the DCL, especially with price subsequently jumping back above the 10 and 20-day moving averages. On the other hand, the September 1st low was not particularly deep, nor was the following rally of any real strength or duration. Further, a move back above the 10-dma was no big feat; the lack of a significant preceding drop and the sideways consolidation meant that the 10-dma bar was very low. Moreover, Friday’s drop appears to embody the sort of capitulation that we’d expect at the end of a DC.

For a number of weeks, I’ve maintained that a major market move was coming. Based on Friday’s action alone, I believe the move has started, so we need to be prepared for some serious volatility. The million-dollar question, of course, is whether the eventual move will be higher or lower.

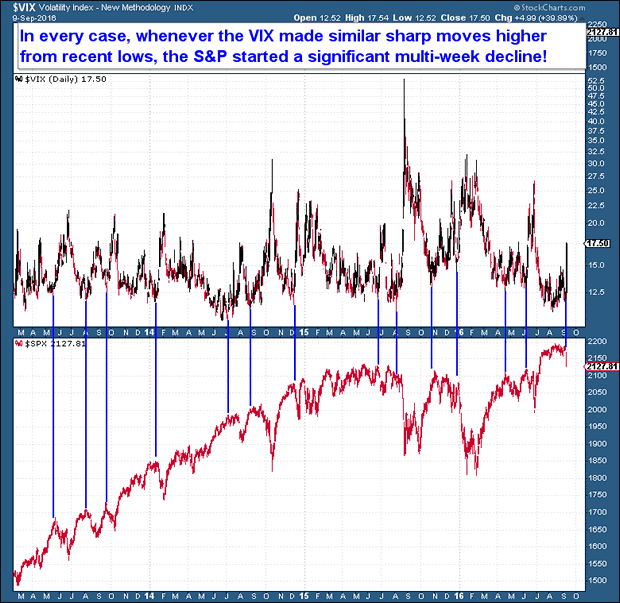

Turning to the VIX, my research uncovered an interesting, and potentially telling, relationship. Whenever the VIX reached a low and then spiked higher, it appears that a) volatility continued to expand, and b) the S&P topped and began a move lower toward a DCL or ICL.

If the above chart holds, we should probably assume that the markets have entered a corrective mode. That doesn’t mean that a major selloff is necessarily at hand, but we should expect a decline that spans more than just a single trading session.

So the Daily Cycle question becomes important. If we are seeing an extended Daily Cycle that capitulates for a few days before bottoming, the longer term move could be higher. On the weekly chart, we would likely see a back test of the breakout, with the rising 10-week moving average as the floor.

The bearish case, however, is a new Daily Cycle, one that will cascade lower out of the recent tight trading range. This would leave behind a very clear week-7 IC Top and a comfortably Left Translated IC that would have cyclical bear market implications.

An except from the Financial Tap Weekend Report – See here for more detail & a Full 14 day, no risk, money back Trial

….also:

SWOT Analysis: Are Gold and Silver Stocks the Best Area for “New Money Right Now”?

Quotable

“Surely nobody would be a charlatan, who could afford to be sincere.”

Ralph Waldo Emerson

There seems to be a lot of confusion about the US dollar reserve currency status. The biggest fallacy is the belief the US $’s reserve status bestows some great benefits on the US economy. It doesn’t. In fact it’s quite detrimental. I am penning this piece now because I noticed the snake oil salesmen (aka pundits and gurus who like to scare people using the dollar as their boogeyman) are out in force yet again.

In their never-ending series of dollar doom (DD) forecasts, predictions, confusions, hallucinations, lies, and manipulations (I will let you pick which of the words you wish to attach to your favorite double-D guru) I must say the latest incarnation they are peddling from the back of their wagon is a real whopper.

The DD punditry is now providing not only a specific reason why (“world money” will replace the dollar), but an exact date (the end of this month) to their crystal-ball-ology. I am not making this up— really. Of course the go to trade, once again, is gold. $10,000 an ounce on the way…again!

I’d like to share a few reality bites in effort to help you understand why you need not fear the Charlatan Choo-Choo of DD which seems to be racing down the tracks of gullibility…

Rationale/Fallacy #1: The dollar will be confiscated by international authoritieswho will be issuing “world money” and sending dollars back to the US in shipping containers. LOL…Now seriously, if I have to explain why this is total crap, you shouldn’t be wasting your time reading Currency Currents anyway. And don’t think this forecast is based on some miraculous issuance of International Monetary Fund Special Drawing Rights (SDR). SDRs are a claim on currency (they are not currency); and there is only a miniscule amount available anyway relative to the needs of the global monetary system. And guess what: The US dollar is the largest weight of the currency basket on which said SDRs are based. [Could one-day the SDR play a bigger role in the global monetary system? You bet. Is that one-day anytime soon? No way, as evidenced by the complete fecklessness of the G-20. Would a bigger role for the SDR be bad for the US economy—nope…in fact it would be very good for the US economy, which leads us to fallacy #2…

Rationale/Fallacy #2: The US dollar world reserve currency status will be challenged. This is one of the most consistent “go to” snake oil salesman rationales in the book. Every DD worth his weight in yuan pulls this one out of their basket of confusion when needed. But then again, most of the PhD’s in economics buy into this fallacy (no surprise there I guess).

Let’s use the US-Chinese relationship as our standard for understanding the detrimental role of the reserve currency at it relates to excess foreign reserves invested in US Treasuries:

Remember these key contentions. Foreign buying of US Treasuries…

-

Doesn’t help out the fiscal deficit in the US, but in fact makes it worse.

-

Doesn’t help push interest rates in the US down, but in fact pressures rates higher if anything.

-

Doesn’t help US employment, but in fact hurts it.

Okay, here we go with the example, I will do this in bullet point format in order to help simplify because it is confusing (balance of payments accounting is supposed be so simple):

-

China has excess savings and it shows up in its current account surplus as such. (Now we need to make a clear distinction between a country’s savings and individual savings—they are two different animals). Excess savings is another way of saying production exceeds consumption; or domestic demand cannot handle all the production therefore China has to find it elsewhere. Thus, China exports these savings in the form of purchasing US Treasuries, as said in order to grab demand from the US.

-

So let’s look at the equation….

– China buys US$’s; then buys US Treasuries with those dollars…

– $ buying by China forces up the relative value of the US$ compared to the Chinese yuan.

– An appreciating US$ (and falling Chinese yuan) tends to put downward pressure on US manufacturing, as the goods manufactured become relatively less competitive …

– Pressure on manufacturing puts downward pressure on employment, i.e. it increases unemployment and it in turn creates a feedback loop of lower relative investment from manufacturers in the US.

• Now, one of two things can happen:

- Chinese investment in Treasuries can be borrowed by businesses for investment purposes and to a degree negates impact of a lower dollar on employment; i.e. business investment creates new jobs (a positive outcome). But, as indicated above, this doesn’t usually happen because the rising US dollar makes manufacturing relatively less competitive and the feedback loop of lower employment reduces domestic demand.

- Government increases the supply of bonds to mitigate impact falling tax receipts. The US government attempts to mitigate the negative impact of China grabbing US demand, as described, through increased borrowing and spending to help alleviate impact of unemployment (falling tax receipts from workers and manufacturing sector); in short more government spending in order to replace lost local demand because of Chinese buying Treasury bonds. This is usually the case.

Now, it is precisely this additional borrowing by the US government which increases the supply of bonds which in turn pressures interest rates higher. [Additional private borrowing to support the prior standard of living also creates problems of its own as this borrowing is primarily spent on consumption and/or real estate—neither of which produce a cash flow to retire the debt.]

To simplify, remember that a rising current account deficit means lower tax receipts to government.

Summary:

Net foreign buying of US bonds

- Slows US growth

- Increases debt

- It does not lower interest rates

- Foreign buying increases fiscal deficits

- Adds to the current account deficit

So, where is the great privilege here? Why do other countries get so worked up when someone starts buying their bonds, as they buy US bonds? For example Japan makes sure it sterilizes any impact of China buying its bonds by turning around and buying a similar amount of US Treasuries to neutralize the impact. If this reserve status was so great why would Japan not embrace China’s buying of its bonds?

A French finance minister, Valéry Giscard d’Estaing, coined the phrase “exorbitant privilege” to explain the role of the US dollar in the global monetary system (even though the French, and the rest of Europe for that matter, piggybacked on artificially low exchange rates relative to the dollar after the War and never revalued—talk about no good turn goes unpunished.)

But Mr. Giscard should have known better. He would have had he read anything from economist Robert Triffin who expressed this warning about a US dollar replacing gold in the monetary system:

In 1960, Triffin testified before the United States Congress and warned of serious flaws in the Bretton Woods system. His theory was based on observing the dollar glut, or the accumulation of the United States dollar outside the US. Under the Bretton Woods system, the US had pledged to convert dollars into gold, but by the early 1960s, the glut had caused more dollars to be available outside the US than gold was in its Treasury. As a result, the US had to run deficits on the current account of the balance of payments to supply the world with dollar reserves that kept liquidity for their increased wealth.

Despite the end of Bretton Woods, the dollar’s role is still hugely dominant as the reserve currency. And guess what: the US runs a large and chronic current account deficit with the rest of world.

So, if another country took on the burden of reserve currency status, or some incarnation of Keynes idea at the Bretton Woods conference—the bancor—is reincarnated, the US economy will be much better off.

So, the next time Mr. Snakeoil tries to scare you with the usual “loss of reserve currency status” canard, tell them: That’s great! I am investing in America.

Thank you.

Jack Crooks

President, Black Swan Capital

www.blackswantrading.com

Strengths

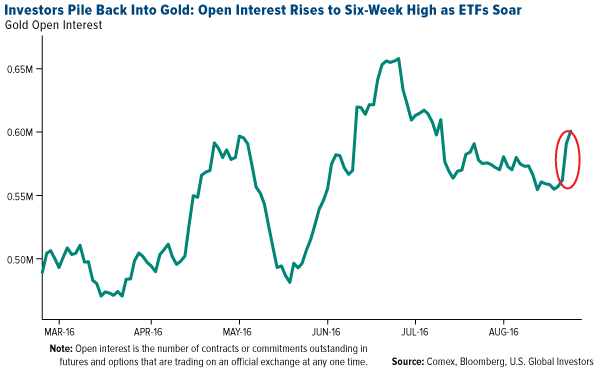

- The best performing precious metal for the week was gold, up 0.22 percent. According to Bloomberg, gold traders and analysts were bullish for the first time in three weeks on the back of the Federal Reserve outlook. In fact, holdings in ETFs backed by the metal climbed by 13.8 metric tons in the first two days of the week, as seen in the chart below.

- On the back of Friday’s jobs numbers, gold and silver have reversed back to the upside and the sector has new buy signals in daily momentum gauges, reports Bloomberg. Stocks related to both gold and silver remain the best area for “new money right now,” according to BMO analyst Russ Visch. BullionVault’s Gold Investor Index agrees with Visch’s analysis—the gauge measuring the balance of client buyers against sellers rose to 56 versus 53.4 in July.

- Pure Gold Mining reported a drill intersect of 50.2 grams per tonne over four meters at its McVeigh Horizon, Madsen Gold Project this week. In addition, mineralization is now extended to a vertical depth of 370 meters. The four drill rig exploration program is designed to expand the high-grade gold resource in close proximity to the existing permitted infrastructure, the company reported.

Weaknesses

- Silver was the worst performing precious metal for the week, down 2.03 percent. Precious metals showed signs of slowing a recent advance, with silver halting a five-day winning streak, reports Bloomberg, and gold trading little changed after the biggest advance since June.

- One of the top gold forecasters, ABN Amro, cut its outlook for gold prices at year-end, reports Bloomberg. The bank lowered its price forecast to $1,325 per ounce compared to a previous estimate of $1,350 per ounce. “We had expected a larger Brexit fallout on financial markets reflected in negative investor sentiment,” ABN Amro analyst Georgette Boele said.

- Gold imports by India slumped in August to the lowest level in five months, reports Bloomberg, as increasing prices reduced spending on the yellow metal. Inbound shipments slumped 85 percent to 21.6 metric tons from a year ago, the article continues, but foreign purchases could recover this month due to festival season.

Opportunities

- Andrew Quail of Goldman Sachs notes that over the past two years, gold miners have adapted well to the new gold price environment. He says companies have executed on the “shrink to profitability” strategy by: 1) lowering operating costs, 2) reducing financial leverage and 3) prudently allocating scarce capital resources. So what now? Quail says the next steps include a focus on productivity, growth and dividends.

- ICBC Standard Bank sees gold rising above $1,400 an ounce in the coming weeks, reports Bloomberg. “There is little prospect that the U.S. Fed will raise rates in September, and most likely not in December either,” the bank said in an email on Thursday.

- The Federal Reserve Bank of Atlanta publishes a special inflation index called, in the words of MarketExclusive.com’s Rafi Farber, the “Sticky-Price CPI.” This index measures prices for goods and services that do not normally experience wild swings. Currently this index is at the highest level since April 2009, which, according to Farber, has “big implications for gold and especially gold mining stocks” because gold usually rises quickly when inflation fears become mainstream. The Sticky-Price CPO has been trending up since 2009, while the flexible CPI has been negative since October 2014. If inflation starts to become obvious—and, according to the Sticky-Price CPI, this could happen soon—Farber writes that “any upside revaluation in the price of gold is likely to be quick and intense.”

Threats

- According to a recent note from BCA Research, the recent “Fedspeak” has hinted strongly at a rate hike later this year. Although a September rate hike is still a possibility, the note goes on to point out the recent batch of disappointing U.S. economic data, combined with lackluster inflation readings and election uncertainty—all suggesting that a December hike is more probable.

- According to the National Australia Bank, the outlook for gold is “mildly bearish” over the rest of 2016. The bank states that central to this outlook are assumptions that the Fed will lift rates in December by 25 basis points and Hillary Clinton will win the U.S. presidential election, reports Bloomberg. The European Central Bank (ECB) can also have an effect on the yellow metal, according to gold traders this week, who saw bullion swing between gains and losses. Investors and traders assessed the outlook for economic stimulus after the ECB president said officials will look at redesigning the quantitative easing program. With no new measures being announced, gold languished for the rest of the week.

- New Gold underperformed as much as 7.6 percent in Canada this week, lagging its gold peers, reports Bloomberg. The drop came after Rainy River capex rose “yet again” by $105 million along with a downgrade of New Gold by Canaccord to hold versus buy. Earlier reports by management have suggested capital requirements would rise by just $35 million due to the need to redesign the tailing containment structures.

…..related:

I don’t think anyone in the commentariat shows any sign of understanding what is revealed by the two political quotes below. The first quote is my favorite because it sums up my sentiments.

I don’t think anyone in the commentariat shows any sign of understanding what is revealed by the two political quotes below. The first quote is my favorite because it sums up my sentiments.About Michael Campbell, Host & Publisher, MONEYTALKS

One of Canada`s most respected business analyst, Michael is best known as the host of Canada’s top rated syndicated business radio show MoneyTalks, and Senior Business Analyst for BCTV News on Global. His outstanding investing track record has been recognized by internationally renowned analysts like James Dines, Martin Armstrong, Peter Grandich, Greg Weldon and many more. Michael`s Inside Edge subscribers have made, and perhaps more importantly, saved money based on his analysis of market trends and opportunities. Including advocating picking up blue-chip dividend paying stocks in every major dip since 2011, getting out of gold in September of 2012, recommending $US denominated assets in Dec of 2013, and getting out of oil stocks in Jan of 2014.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair