Timing & trends

Via Simon Black:

Excerpts from this year’s Templeton Prize recipient. A succinct and fantastic summation of WHY the West is in such decline.

This is not some message of doom and gloom by a tin-foil-hat-wearing conspiracy theorist.

On the contrary, it’s an inspiring look at what made the West great to begin with. And, maybe, just maybe, how it might be once again.

Excerpts below:

This is a fateful moment in history. Wherever we look, politically, religiously, economically, environmentally, there is insecurity and instability.

It is not too much to say that the future of the West and the unique form of freedom it has pioneered for the past four centuries is altogether at risk. . .

To mention just a few [risks:]. . .

Artificially low interest rates that encourage borrowing and debt and discourage saving and investment.

Wildly inflated CEO pay.

The lowering of living standards, first of the working class, then of the middle class.

The insecurity of employment, even for graduates.

The inability of young families to afford a home. . .

The collapse of birthrates throughout Europe, leading to unprecedented levels of immigration that are now the only way the West can sustain its population, and the systemic failure to integrate some of these groups.

The loss of family, community and identity, that once gave us the strength to survive unstable times.

And there are others.

Why have they proved insoluble?

First, because they are global, and governments are only national.

Second, because they are long term while the market and liberal democratic politics are short term.

Third, because they depend on changing habits of behavior, which neither the market nor the liberal democratic state are mandated to do.

Above all, though, because they can’t be solved by the market and the state alone.

You can’t outsource conscience. You can’t delegate moral responsibility away.

When you do, you raise expectations that cannot be met.

And when, inevitably, they are not met, society becomes freighted with disappointment, anger, fear, resentment and blame.

People start to take refuge in magical thinking, which today takes one of four forms: the far right, the far left, religious extremism and aggressive secularism.

The far right seeks a return to a golden past that never was.

The far left seeks a utopian future that will never be.

Religious extremists believe you can bring salvation by terror.

Aggressive secularists believe that if you get rid of religion there will be peace.

These are all fantasies, and pursuing them will endanger the very foundations of freedom.

Yet we have seen, even in mainstream British and American politics, forms of ugliness and irrationality I never thought I would see in my lifetime.

We have seen on university campuses in Britain and America the abandonment of academic freedom in the name of the right not to be offended by being confronted by views with which I disagree.

Most societies, for most of history, have been either tradition-directed or inner-directed. People do what they do, either because that is how they have always been done, or because that’s what other people do.

Inner-directed types are different. They become the pioneers, the innovators and the survivors.

They have an internalized satellite navigation system, so they aren’t fazed by uncharted territory.

They have a strong sense of duty to others. . . . They take daring but carefully calculated risks. When they fail, they have rapid recovery times.

They have discipline. They enjoy tough challenges and hard work. They play it long.

They are more interested in sustainability than quick profits.

They know they have to be responsible to customers, employees and shareholders, as well as to the wider public, because only thus will they survive in the long run.

They don’t do foolish things like creative accounting, subprime mortgages, and falsified emissions data, because they know you can’t fake it forever.

They don’t consume the present at the cost of the future, because they have a sense of responsibility for the future. . .

Cultures like that stay young. They defeat the entropy, the loss of energy, that has spelled the decline and fall of every other empire and superpower in history.

But the West has, in the immortal words of Queen Elsa in Frozen, let it go.

It’s externalized what it once internalized. It has outsourced responsibility. It’s reduced ethics to economics and politics.

Which means we are dependent on the market and the state, forces we can do little to control.

And one day our descendants will look back and ask, How did the West lose what once made it great?

Every observer of the grand sweep of history, from the prophets of Israel to the Islamic sage ibn Khaldun, from Giambattista Vico to John Stuart Mill, and Bertrand Russell to Will Durant, has said essentially the same thing: that civilizations begin to die when they lose the moral passion that brought them into being in the first place.

It happened to Greece and Rome, and it can happen to the West.

The sure signs are these: a falling birthrate, moral decay, growing inequalities, a loss of trust in social institutions, self-indulgence on the part of the rich, hopelessness on the part of the poor, unintegrated minorities, a failure to make sacrifices in the present for the sake of the future, a loss of faith in old beliefs and no new vision to take their place.

These are the danger signals and they are flashing now. . .

We owe it to our children and grandchildren not to throw away what once made the West great, and not for the sake of some idealized past, but for the sake of a demanding and deeply challenging future.

If we do simply let it go, if we continue to forget that a free society is a moral achievement that depends on habits of responsibility and restraint, then what will come next – be it Russia, China, ISIS or Iran – will be neither liberal nor democratic, and it will certainly not be free. . .

The Templeton Prize is named after legendary investor Sir John Templeton, who passed away in 2008.

In addition to being an enormously successful asset manager, Templeton was an unparalleled philanthropist.

He even renounced his US citizenship in 1964 during the Vietnam War, which saved him over $100 million in taxes that would have gone to fund a destructive war.

Instead, that money went to fund charitable efforts around the world.

This year’s recipient of the Templeton Prize is a British rabbi and philosopher named Jonathan Sacks.

The excerpts above are from his recent acceptance speech.

[Editor’s note: You can read the full speech here.]

Until tomorrow,

Simon Black

Founder, SovereignMan.com

What do graphene, batteries, artificial intelligence, nanosensors, and the blockchain have in common?

They are all emerging technologies that are expected to make it big this year.

Learn about 10 game-changing technologies that will impact your future in today’s graphic.

….view Top 10 Emerging Technologies of 2016 (larger images)

Michael interviews one of his favorites, Paul Beattie, founding partner at BT GLobal Growth Fund. Paul brings his bracing and refreshing insights right off the bat starting out the interview with his frustration at missing some great investments in this complicated market. If you haven’t heard Paul before you are in for a treat. No punches pulled, no fools unchallenged and no sacred market cows allowed!

Be sure to listen to Mike’s Saturday Comment – The Dominant Driver of Capital World Wide

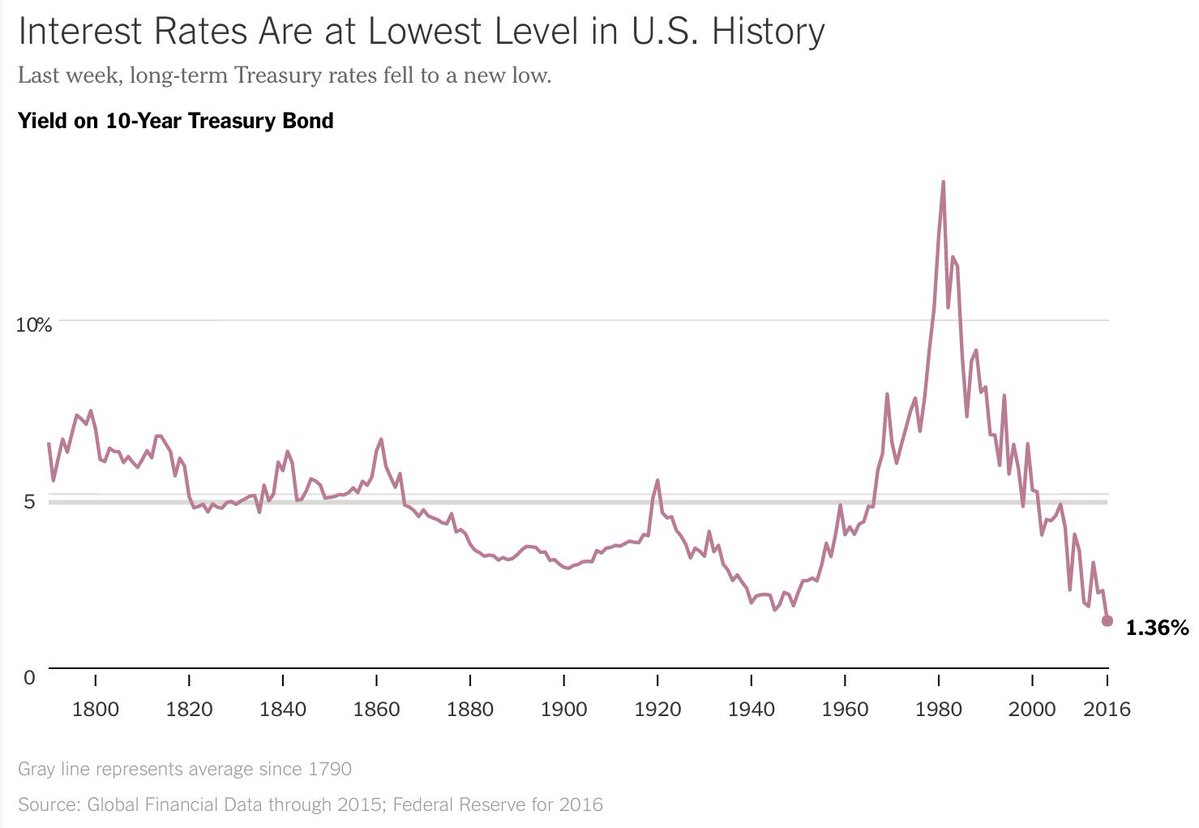

Interest rates are now hitting record-lows while stocks hit record-highs; this has never happened before. Nor should it ever happen.

You see, changes in interest rates are typically a very good economic indicator, forecasting future growth and inflation. In recently plunging to new, all-time lows, they have taken out the lows set during the Great Depression. In other words, the bond market is saying the prospects for the economy are not very good and possibly very dire.

also:

Michael Campbell’s commentary on The Dominant Driver of Capital World Wide

The S&P 500 is trading near an all-time record high. But investors should not take this as the all clear signal. According to most indicators, the market is now more overvalued than ever before.

The Cyclically Adjusted Price to Earnings Ratio analyzes the value of the S&P 500 Index with the 10-year average of “real” (inflation-adjusted) earnings as the denominator to determine if the market as a whole is overvalued or undervalued. Today this ratio sits at 26.73, close to the short-term high of 27.2 seen in 2007 and well above its historic average of around 16.

Then we have the Q ratio, developed by James Tobin. This metric takes the total price of the market divided by the replacement cost of all its companies’ assets. The average Q ratio is .68, but the latest estimate of the Q ratio .98. This suggests that the S&P 500 is currently dramatically above the mean.

Adding to this, the total market cap of U.S. stocks is now 122.5% of GDP. This is the highest level since mid-2000, which was during the NASDAQ bubble. This measure reached its peak at 142%, before crashing back to the more traditional level of just 70% by 2002.

And last we have the Price to Sales Ratio of the S&P 500. It is a measure of the Index’s value compared to its sales. The most recent Price to Sales is estimated at 1.91, in December of 2015 it was 1.81 and in 2007 it was 1.43. This metric shows the market is vastly overvalued compared to firms’ revenue.

All these indicators demonstrate that the S&P 500 is sitting in nosebleed territory. However, while the market marches to ten-year highs, the Ten-year Note yield is hitting historic lows. Bonds and stocks historically have an inverse relationship. This is leading investors to question what the bond market knows that equity investors do not and vice versa. But the correct answer to this seeming conundrum is that both stocks and bonds are in a bubble, which is the direct result of unprecedented central bank credit creation.

The condition of record low bond yields should be the result of a record low deficit and debt to GDP ratios, strong economic growth, which would increase the credit quality of the issuers, and historically low central bank balance sheets.

But today, low bond yields are all about central bank manipulation of bond prices. For instance, the last time the 10-year note was anywhere near this neighborhood was when it reached 2.29 percent in April 1954, during the Eisenhower era. As I noted in my book “The Coming Bond Market Collapse”, during the 1950’s the United States held most of the world’s gold and manufacturing base. The National debt was high but was falling precipitously in relation to the economy; meanwhile, household debt was very low. Also, a strong dollar backed by a partial gold standard and robust economy led to a healthy Treasury market. Bond yields were not a result of central banks manipulating currencies in a frenzied search of inflation to perpetuate a growth fallacy.

But the longer Central Banks stay in the game of thwarting market prices the greater the divergence between economic growth, equity markets, and bond yields will become. This game can last a lot longer than most believe. However, reality will eventually take hold and cause a cataclysmic global bond market collapse.

This is because all asset prices are a function of the so-called “risk-free” rate of return on sovereign debt. Record low and even negative, bond yields have forced yield-starved investors far out along the risk curve in search of a positive return. Therefore, the worldwide sovereign bond bubble has infected; Collateralized Loan Obligations, Mortgage Backed Securities, Municipal Bonds, Real Estate Investment Trusts, Junk Bonds, and Equities…just to name a few of the assets warped by this unprecedented phenomenon.

What will be the sign that equity prices will crash back to reality? The answer in one word is inflation. If, or rather when, these maniacal central bankers achieve “success” in forcing inflation upon the masses; whatever is left of the free market will run for the narrow door to exit all of the assets listed above. Thus, exacerbating the global economic meltdown that must follow the faltering of government debt throughout the developed world.

One more warning for equity holders to heed: As we are all aware, the U.S. housing bubble collapsed back in 2008 and caused a global financial crisis. However, unlike what most market pundits will tell you, a fairly localized Real Estate meltdown cannot be worse than having the entire global sovereign debt market collapse. Blindly riding out this bull market without appropriately hedging your investments is extremely dangerous. Indeed, economic savvy and vigilance have never been more important for your financial health.

related:

Michael Campbell’s commentary on The Dominant Driver of Capital World Wide

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair