Timing & trends

‘A person who has never made a mistake has never tried anything new.’

– Albert Einstein

Invest In Yourself

Several months ago, I wrote an article on why I believe your best investment is in yourself. I gave a personal example from the beginning of my career of how I invested the equivalent of $100,000 in my education at a time when I was driving a car I bought for $55 and had not purchased new clothes in two years. I knew the material things would come only after I built the skills necessary to create value in the marketplace. This early investment in myself launched me into a successful 25-year career as a C-level corporate executive, investor and business owner.

While it’s always wise for a young person to invest in a quality education and job ready skills, today it is even more critical as the world changes dramatically on multiple fronts. The rate of economic, technological, political and demographic change is staggering, and the cumulative impact is permanently altering the future in ways that are hard to imagine. Economically, for instance, the US Federal Funds Rate from 1954 to 2008 averaged 4.96%. However, it has dropped dramatically to an average of 0.14% since 2008, creating massive market distortions that will have significant long-term impacts.

Technological change, driven largely by information technology and innovation, is disrupting existing industries and institutions, simultaneously creating economic opportunity and displacement, winners and losers. Political change, in the form of rising nationalism and anti-establishment sentiment, is gaining steam, particularly among young people. Finally, demographic change driven by millennials (people between the ages of 18 and 35), is remaking society and the economy, while creating a new, large, economic and political force. According to PEW Research Centre, in 2016 millennials will make up 35% of the US workforce and quickly surpass the baby boomers to make up 50% of the workforce in 2025.

The Changing World of Millennials

Millennials are entering a world where many of the rules of their parents no longer apply, and the skills required to be successful need to be developed fast! It is a 24-hour per day, globally connected world of unlimited information and unlimited competition. The philosophy of ‘just work hard and get a good job’ taught by parents and the school system will not be enough to succeed. It will take a fundamentally different approach to building skills, adapting to change and making money, for millennials to thrive in this new world.

Already, millennials are at some risk. According to a recent study by the Princeton-based Educational Testing Service (ETS), ‘despite having the highest levels of educational attainment of any previous American generation, these young adults (millennials) on average demonstrate relatively weak skills in literacy, numeracy, and problem-solving in technology-rich environments compared to their international peers.’ The study found that US millennials scored in the bottom half of the 22 country study on the basic numeracy and literacy skills necessary to be effective in the workplace.

Therefore, to survive and then thrive in this new, emerging world, more than ever young people will need to invest in themselves in order to build skills, create value in the marketplace and increase their incomes, before they think about traditional investing like their parents. They need to focus on themselves as an asset and consistently invest in that asset until it is productive and able to generate good income and create value.

The Nine Critical Skills

To achieve this, I believe millennials need to focus on investing in the development of three categories of skills: basic skills, adaptability skills, and money making skills. I am referring specifically to skills, not talents or interests, but hard skills that can be learned; an expertise that will give you the ability to do something well.

Basic Skills: There will be too much competition in the future workforce to allow anyone without fundamental numeracy skills and literacy skills to succeed. The ability to express yourself well in a world driven by communications and information technology is valuable, transferable and necessary for long-term success. In addition, sound financial and investment skills are necessary to understand how economics impact daily life and the how to take advantage of that impact.

Adaptability Skills: Due to the significant changes millennials can expect to experience over their career, the ability to adapt to change will be important in order to avoid obsolescence and downward mobility. This starts with developing self-awareness skills, or the ability to see yourself as you really are, not as you think you are. Then, to embark on a program of systematic self-improvement skills development, in order to correct your deficiencies and make the changes necessary to adapt. Finally, developing problem-solving skills so you can help employers (or customers) rapidly remove stubborn obstacles and create value in the marketplace.

Money Making Skills: The last time I checked, there was not a course called Making Money 101 in high school or university, though there should be! As the sun sets on the industrial age and rises on the information age, the ability to make money will be critical in order to stay ahead. This starts with developing sales skills which you need to promote yourself and your value in all aspects of life, not just business. It will be important to have a strong second language skill, particularly Mandarin, as the economic influence of China will grow for decades. The final money making skill will be negotiating skills, as most millennials will be freelancers when they compete with technology and a global workforce for jobs.

How to Invest in Building the Nine Critical Skills

Quality Education: Invest in a quality education at the post-secondary level. Focus on what you will actually learn, not in just getting a diploma. I am a particularly strong advocate of vocational institutions, as well as professional studies in the fields of science, engineering, technology, design, and health.

Standardized Testing: The truth is not always pleasant, but best to find it out first and fast. Consider taking standardized tests or assessments to find your weak points. Then face reality and work on fixing these weaknesses.

Company Training: Many large companies offer excellent training and skills development programs for new grads and employees. It can be a good place to start a career. Take everything offered and treat it seriously.

Continuing Education: Never stop learning. Constantly take webinars, online courses such as Massive Open Online Learning (MOOCs), seminars and workshops. Focus on specific skills, as I mentioned above.

Get Good Mentors: Seek out people in your industry that are 10 times more successful than you and ask them to help you develop skills. Treat the relationship with respect and focus on one or two specific skills. Return the favor.

Fail Well: You learn by trying, making a mistake and doing it better next time, aka, failing. Embrace failing as a chance to learn, fail fast but learn from failure.

Learn From Others: There is not enough time to make all the mistakes yourself, so learn from others. Read good books, download worthy podcasts, attend conferences and keep an open mind.

Good investing is about buying something of value that pays a dividend and continues to grow. For a young person today, an investment in yourself will pay back many times over the course of your life. It will help you build the skills, confidence and then income necessary to live a fulfilling, productive and worthwhile life in our changing and new world.

Eamonn Percy has more than 25 years of business experience in helping companies transform and grow. He is a problem solver, board member, investor, speaker, and columnist on the topics of business growth and leadership. He is the Founder and President of The Percy Group Capital + Business Advisors, a business performance improvement firm which helps determined leaders permanently solve problems, accelerate performance and achieve results.

Eamonn is the author of the upcoming book The 1% Solution – How Small Daily Improvements Produce Massive Long-term Results. Get free, early notification of it here.

Eamonn is the author of the upcoming book The 1% Solution – How Small Daily Improvements Produce Massive Long-term Results. Get free, early notification of it here.

Subscribe to his free weekly newsletter, Growth by Design

1. A Textbook Historical Moment

1. A Textbook Historical Moment

by Michael Campbell

The Brexit vote in Europe is just a part of a major trend sweeping in the world as waves of capital are set to flee the European welfare state and the fallout will effect every market in the world as capital seeks safety.

2. Marc Faber: Hillary Will Destroy The World

“US economy is like botox , looks good on the outside but rotten on the inside and Hillary Clintor will destroy the world “.

“Well, if you look at her period during which she was Secretary of State, the U.S. committed several aggression’s in the Middle East, including, also, the invasion of Libya. Libya, which was probably, the only properly functioning African Economy. So, I would say that her achievements with nation building have been a catastrophe.

…..continue reading or listening HERE

3. Sell Off Coming!

In short, the major trends of all asset classes which have been in place for several years are coming to an end. The majority of investors have no idea what is starting to take place and will do what the masses do every time a new bear market takes place.

The gold mining stocks continue to defy any bearish price action or perceived bearish development. Pundits first warned because of the “bearish” CoT data. The commercials are always right and a big decline is coming! Then we heard the miners were too overbought and would have to correct 20%. (I thought this once or twice!) Next we heard Gold was forming a head and shoulders top. Conventional analysis is failing in trying to predict or even explain what is happening and why. A look at history helps explain why the gold mining sector has remained extremely strong and almost immune to any sustained correction. Simply put, history shows that epic bears give birth to bull markets that in their first year do not experience any significant correction or retracement.

The Nasdaq, which is comprised of mostly tech stocks crashed 78% during its bear market from 2000 to 2002. That epic bear followed a full blown mania and a strong recovery followed that epic collapse. The Nasdaq rebounded by 94% in 15 months and only endured one significant correction during the recovery. That 17% correction occurred while the market was in a bottoming process. Once the Nasdaq exceeded 1400 it enjoyed smooth sailing to 2100 over the next nine months.

The next chart plots the S&P 500 and the Nasdaq from 2008 to 2011. The bear market in price terms was the worst for the S&P 500 since World War II. Its recovery was equally as spectacular as the index gained 83% in 13 months without correcting more than 9%. During the same period, the Nasdaq doubled and did not shed more than 10%!

Speaking of World War II, it kicked off the best buying opportunity of all time as the stock market enjoyed fabulous returns over the next year, three years, five years, 10 years and 15 years. The stock market declined 60% over the previous five years. It was the longest bear market in modern times and the second worst in terms of price. During the ensuing recovery, the S&P 500 gained 70% in 14 months and did not correct more than 5%! It also held above its 50-day moving average nearly the entire time!

While the gold mining space is a very tiny sector and its own animal compared to the stock market, its current recovery can be accurately depicted in a strikingly similar context. The recovery has been extremely strong in terms of price and the lack of declines. The gold stock indices are up over 100% and have yet to correct even 20%! It makes perfect sense considering gold stocks are following their worst bear market ever and in January were perhaps at their own 1942 moment.

The gold stocks are following a history that suggests potentially another six to nine months of steady gains without a major correction or retracement. In looking at both the gold stocks and Gold (chart below), we can see potential six to nine month upside targets of HUI 365 and Gold $1500-$1550. The HUI has overhead resistance to overcome while Gold has $1300 and $1400 to overcome.

We’ve said it before and we will say it again. It is hard to be bullish when something is so overbought and trading so much higher than in recent months. However, the one time to be bullish amid that context is when the market at hand has emerged from a brutal bear market. The gold mining sector is only five months into this new bull market. The historical pattern that gold stocks are currently following suggests potentially another six to nine months of upside before a major correction or retracement. It is difficult to be bullish or be a buyer here but our research suggests it is the correct posture. As we noted last week, +10% weakness could be a good buying opportunity.

Jordan Roy-Byrne, CMT

Jordan@TheDailyGold.com Consider learning more about our premium service

related: Gold The Battle For $1307

Like an oak slowly growing in a stand of pines, the outgrowth of sentiment extremes become visible through major market inflection points. The irony, however, is seeing them. This is because on both sides of a market cycle there is a natural tendency for conditions otherwise thought abnormal to become commonplace. As much as we try to anchor our baseline expectations with history, inevitably, paradigm creep sets in as markets and sentiment slowly become stretched beyond more rational assumptions.

Like an oak slowly growing in a stand of pines, the outgrowth of sentiment extremes become visible through major market inflection points. The irony, however, is seeing them. This is because on both sides of a market cycle there is a natural tendency for conditions otherwise thought abnormal to become commonplace. As much as we try to anchor our baseline expectations with history, inevitably, paradigm creep sets in as markets and sentiment slowly become stretched beyond more rational assumptions. They couldn’t see the trees for the forest – until the forest caught fire.

In the late 1990’s as venture capital was seeding manic entrepreneurs with otherwise outrageous business plans, perspective was forsaken for the chance to become the next internet giant. A short time down that road, the pursuit of Amazon quickly gave way to the likes of Clickmango, your one-stop shop for all of your succulent produce desires and LifeJacketStore.com – well, for your many recreation flotation demands…

The reality is it’s been a “Costanza” market since that time and we see no reason to believe conventional wisdom will get it right today.

George: “My life is the complete opposite of everything I want it to be. Every instinct I have in every aspect of life, be it something to wear, something to eat… It’s often wrong.”

George: “My life is the complete opposite of everything I want it to be. Every instinct I have in every aspect of life, be it something to wear, something to eat… It’s often wrong.”

Jerry: ”If every instinct you have is wrong, then the opposite would have to be right.”

– Seinfeld, “The Opposite” (1994)

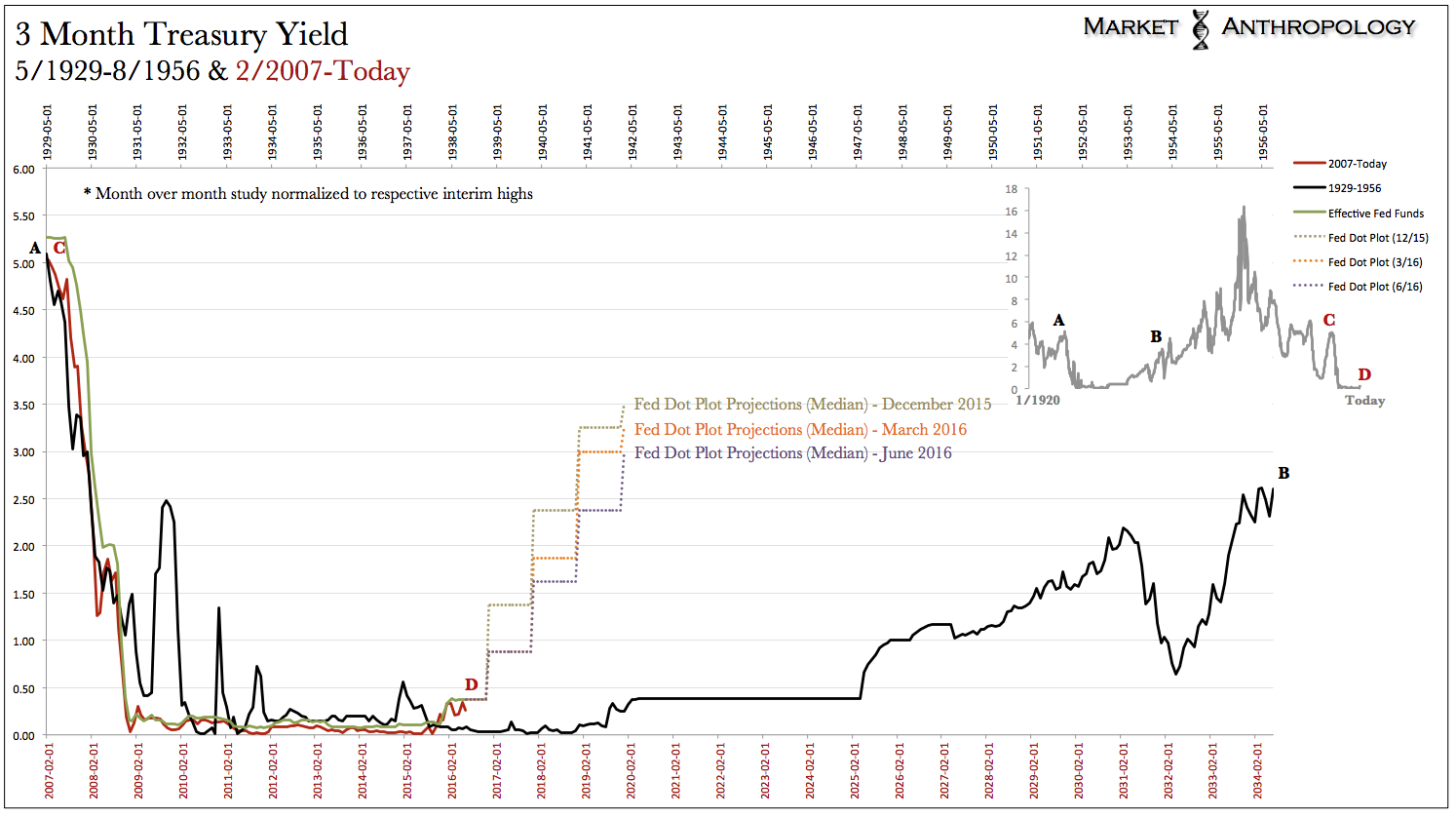

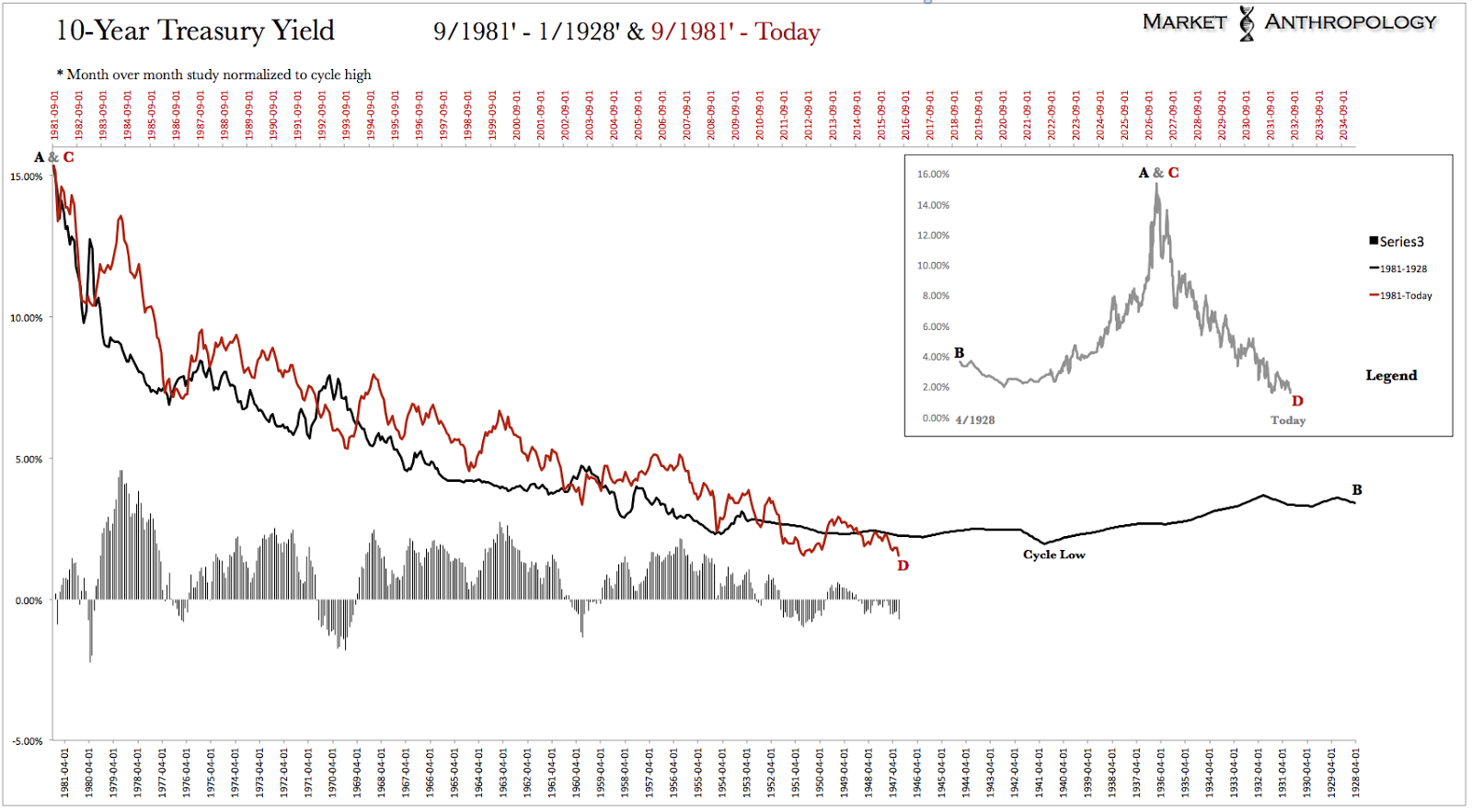

Do we expect a return to “normal” where the 10-year yields over 4 percent or the fed funds rate is materially above 2 percent? No. Expectations were pushed too high over the past two years and as seen yesterday with the Fed’s new dot-plot projections for June, have continued to drift lower as expected. Moreover – and as shown below with our comparative profile of the last time yields fell into the long-term cycle trough in the 1930’s and 1940’s, they still have a ways to go in aligning expectations with reality.

The twist, however, is long-term yields have now been pushed to the bottom of the range by the latent reflexive move. Our best guess – and an opinion we have held since the end of 2013, is that the 10-year yield will remain range bound between 1.5 and 3 percent for the foreseeable future, as markets and economies work across the transitional divide to the next major secular growth cycle.

With precious metals continuing to lead the move higher in the commodity sector this year and with the US dollar poised to fall further (see Here), the inflation vane continues to points higher – despite the Costanza concerns with disinflation and deflation today. All things considered (see Here), we would conservatively speculate that the 10-year yield will snap back to the return profile of the long-term cycle around 2.25 percent.

The British are coming! The British are coming! The British are coming!

With the Brexit vote on tap for next Thursday, we see a resolution for the markets heightened anxieties and not a revolution to leave the EU. Over the past few weeks, concerns have snowballed that Britain will choose to leave. Our best guesstimate is they’re widely off the mark, and expect a strong snap-back reaction to develop in the markets next week. Broad brush, over the short-term this would likely be bullish for equities and bearish for bonds and gold.

Taking a speculative swing with potentially longer-term opportunities, we cautiously like the prospects for higher beta equity markets over the short-term, such as Spain’s IBEX. Moreover, our momentum comparative that we’ve followed over the past three years for the IBEX points towards an interim low, with the possibility that its cyclical decline has run its course. With the euro finding a foothold in today’s session, we like the iShares MSCI Spain ETF – EWP, that would also benefit from a stronger euro. For potential longer-term investors, the ETF pays a hefty 4.25 percent dividend.

The US dollar index, which we had expected to retrace lower coming into June, continues to flirt with the bottom of the range (~93) of the broad top it has traded in over the past two years. Should the vote in Britain fail next week, we’d expect the euro to find strength and the US dollar index to weaken. Our dollar index comparative from 2009 also points towards further weakness and a breakdown below support of its broad top.

The Federal Reserve failed to inspire confidence that they have a handle on what is happening in the global economy. Fed Chair Janet Yellen, in a press conference, seemed to be more defensive about misleading the market explaining why she and other officials said this meeting was a live meeting and then doubled down by saying a July interest rate increase is not “impossible.”

The Federal Reserve failed to inspire confidence that they have a handle on what is happening in the global economy. Fed Chair Janet Yellen, in a press conference, seemed to be more defensive about misleading the market explaining why she and other officials said this meeting was a live meeting and then doubled down by saying a July interest rate increase is not “impossible.”

Global markets are already losing confidence in the Fed and other central banks around the globe as it is looking more likely that they really are unsure of what to do next. It is looking more likely that the UK will vote to leave the Euro Zone and instead of providing the market confidence and cover, the markets showed disappointment after Yellen’s press conference that she and the Fed really have a handle on just what the heck is going on.

also:

This financial bubble is 8 times bigger than the 2008 subprime crisis

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair