Timing & trends

Experts worry about stock, bond and real estate market excesses. But a bubble is forming that dwarfs them all: in pension plans. Millions of Americans and Canadians who are counting on pension benefits to fund their retirements risk being severely disappointed.

Experts worry about stock, bond and real estate market excesses. But a bubble is forming that dwarfs them all: in pension plans. Millions of Americans and Canadians who are counting on pension benefits to fund their retirements risk being severely disappointed.

The hard money community has, of course, been aware of this for some time. However in recent years, even the elites have been taking notice.

One such group, the International Forum of the America’s will be holding its fourth annual pension conference in Montreal next Monday.

There politicians, financiers and monetary policy officials, will discuss the declining rates of return in public and private sector pension plans.

The picture they will paint is increasingly grim.

Pension funds, which have been issuing over-optimistic revenue forecasts for years, aren’t going to earn nearly enough money to pay the benefits recipients expect.

Much of this relates to secular stagnation in the economy.

Bonds, which from a major part of most plans’ holdings earn next to nothing in interest.

Stocks, which are trading at record levels, despite falling corporate earnings, look to have more downside risk than upside potential.

Worse, if bond returns average 2%, balanced portfolios projecting 7% to 8% annual returns, have to earn 12% to 14% on equities investments to make up the difference. That’s unlikely to happen.

At least private sector plans have some money in them – public sector plans are in even in worse shape.

Governments have almost nothing put aside to fund future retirees – and they don’t even fully list their debts.

That process of “cooking the books” ramped up in a major way during Bill Clinton’s administration, whom Hillary Clinton, the current Democratic Presidential nominee has promised to “put in charge of the economy.”

The upshot is that most Americans and Canadians have no clue how far in debt their countries are. Researchers such as Laurence Kotlikoff , a professor at Boston University, suggest that unfunded pension and other liabilities run into the tens of trillions of dollars in the United States. The Fraser Institute has shown that Canada isn’t much better.

Backing off commitments

Ironically, the biggest challenge facing government bureaucrats and private fund administrators has nothing to do with paying back pensioners. They have known for some time that would not be possible.

Their key challenge, will be to ensure that shortfalls occur on someone else’s watch.

As such, these defaults will occur at a gradual pace. The first stages, already well under way, include steps such as raising eligibility requirements, increasing the tax burden on “wealthier” recipients and so on.

Congress, which teamed up to cut benefits during the Reagan administration, has been trying to find a way to do it a second time. Once the November elections are over they will likely give it another shot.

A likely model will be Canada, where, in 2012, the late Jim Flaherty, a political master, camouflaged the Harper Government’s raising the eligibility requirements for Old Age Security from 65 to 67, by delaying implementation for ten years.

Flaherty further deflected media attention from the default by simultaneously banning the penny. Canadian journalists, fell for the bait and spent the next week writing stories about the pennies, never for a second realizing that Flaherty had slipped one by them.

House prices up 12%, food prices 3.7%. Pensions up 1.3%.

Another tactic used by government officials and pension fund managers to avoid paying out pensioners, is to inflate away the problem. As John Maynard Keynes, the great economist, noted: inflation is an excellent way to extract wealth, because not one man in a hundred will understand how it was done.

Here is how it works: governments promise pensioners that their benefits will be indexed to protect beneficiaries against rising prices. But they then use selected or massaged statistics to back out.

In Canada, federal (CPP) pension plan recipients will see their benefits rise by 1.3% during 2016. But food prices, according to Statistics Canada rose by 3.7% last year. House prices rose by 12% up to December 2015 according to the Canadian Real Estate Association.

The controversial John Williams of Shadow Statistics provides credible research about how the data massaging works in the United States.

The effects of prices rising faster than benefits, over time, can be dramatic. If prices rise by 2% faster than pensions each year, then by the 20th year of retirement, beneficiaries will be losing 40% of their purchasing power (I am calculating using a straight line basis for simplicity).

In short, most pensioners won’t have a clue what hit them.

Outright defaults

Seniors vote – and there are a lot of them. So outright defaults on pension obligations will be a last resort of politicians and private sector plan managers.

However, it is starting to happen.

The ongoing saga of the US Central States Pension Fund, whose 400,000 beneficiaries were recently offered cuts of up to 60% in the amounts they receive, provides an excellent warning.

Amazingly the Central States Pension Fund, which manages funds for retirees from a number of companies in 37 states, actually has $18 billion in funds. Managers from those companies simply over-promised workers how much money they would get.

Pensioners in a variety of public plans including Detroit’s – which went bankrupt – and Illinois – which is insolvent – haven’t been much luckier. Many more will suffer the same fate.

Governments still have some time to manage the fallout. So do taxpayers who are counting on those plans to fund their retirements.

For them, the time to plan is now.

Two thirds of the families in the US are now invested in the stock market compared to three percent in the great crash of 1929. When the economic crash comes, retirement accounts, mutual funds and most paper wealth will be wiped out. Most people making a living on the service sector of our economy will be unemployed. Prices on everything made in this country will either deflate or paper money will lose most of its value. The resultant depression will affect everyone and it will be the worst that this nation has ever known.

Two thirds of the families in the US are now invested in the stock market compared to three percent in the great crash of 1929. When the economic crash comes, retirement accounts, mutual funds and most paper wealth will be wiped out. Most people making a living on the service sector of our economy will be unemployed. Prices on everything made in this country will either deflate or paper money will lose most of its value. The resultant depression will affect everyone and it will be the worst that this nation has ever known.

Stop me if you’ve heard this one before: A Fed official walks into a bar and says the economy is improving and rate hikes are appropriate. The patrons order another round to celebrate. Then disappointing data comes out, the high fives stop, and the Fed official ducks out the back…only to come back the next day saying the same thing. Anyone who pays even the smallest attention to the financial media has experienced versions of this joke dozens of times. Yet every time the gag gets underway, we raise our glasses and expect the punch line to be different. But it never is. Last week was just the latest re-telling.

Stop me if you’ve heard this one before: A Fed official walks into a bar and says the economy is improving and rate hikes are appropriate. The patrons order another round to celebrate. Then disappointing data comes out, the high fives stop, and the Fed official ducks out the back…only to come back the next day saying the same thing. Anyone who pays even the smallest attention to the financial media has experienced versions of this joke dozens of times. Yet every time the gag gets underway, we raise our glasses and expect the punch line to be different. But it never is. Last week was just the latest re-telling.

For nearly a month the Fed’s bullish statements stoked optimism on the economy and raised expectations, based particularly on the most recent FOMC minutes, for a summer rate hike. But these hopes were dashed by the May non-farm payroll report, which reported the creation of only 38,000 jobs in May, the worst monthly performance in six years, based on data from the Bureau of Labor Statistics (BLS). The number missed Wall Street’s estimate by a staggering 120,000 jobs. If not for the 37,000 downward revision reported for April (160,000 jobs down to 123,000), May could have shown a contraction. This would have constituted a major black eye to the Obama Administration’s favorite talking point that its policies have led to 75 months of continuous job gains. (6/3/16, Democratic Policy & Communications Center).

To make the report even stranger, the plunge in hiring was accompanied by a drop in the unemployment rate to just 4.7%. Of course the fall in the unemployment rate was a function of another major drop in the labor force participation rate to just 62.6%, matching the June 2015 rate, which was the lowest level since the late 1970s (BLS). So the unemployment rate did not fall because the unemployed found jobs, but because they stopped looking. The market reaction was swift and sharp, as it always has been when a fresh shot of cold water has been thrown in the face of market boosters. The dollar fell hard and gold rose sharply.

But we can rest assured that despite any embarrassment that the Fed may be experiencing for having so gloriously misdiagnosed the current economic health, it will be right back at it in a few days, telling us about all the positive economic signs that are emerging and how it is ready and willing to start raising interest rates at the earliest opportune moment. Boston Fed president Eric Rosengren waited exactly 48 hours to start that campaign as he sounded bullish notes in a Monday speech in Finland. (6/6/16, Greg Robb, MarketWatch)

Given how many times this scenario has unfolded, leading to the point where even reliable Fed apologists like CNBC’s Steve Liesman have begun questioning the Fed’s credibility, one wonders what the Fed hopes to achieve by continuously walking into the bar with a new smile. But this performance is the only policy tool it has left. The Fed appears to believe that perception makes reality, so it will never stop trying to create the rosiest perception possible. It may view its own credibility as expendable.

There is also the possibility, however unlikely, that the Fed officials are not just trying to create growth through open-mouth operations, but that they actually believe that their policies are working, or are about to work. This would be as dogged a commitment to policy as medieval doctors had for bloodletting, which they thought was a useful therapy for a variety of ailments. Doctors at that time had all kinds of seemingly plausible reasons why the technique was effective. If the patient did improve after draining blood, it was taken as a sign of validation. But they would continue to apply the leeches even if the patient did not improve. Failure was simply a sign that that more blood needed to be drained. Similarly, central bankers consider ultra-low, and even negative, interest rates as an ambiguous stimulant that will create growth when applied in large enough doses.

But what if modern central bankers, much like medieval doctors, are operating on a wrong set of assumptions? We know now that draining blood creates conditions that actually decrease a patient’s ability to fight infection and recover. Perhaps, one day, bankers will come to a similarly delayed conclusion about how zero and negative interest rates have prevented a real recovery that would otherwise have naturally taken place.

That’s because artificially low interest rates send false signals to the economy, prevent savings and investment, and encourage reckless borrowing and needless spending. They prevent the type of business and capital investment that is needed to create real and lasting economic growth. But don’t expect bankers, or their cheerleaders on Wall Street, the financial media, government, or academia, to ever make this admission. They do not believe in the power of free markets. They believe in government. Such a leap is simply beyond their powers of comprehension.

But there is another cycle here that is much more influential on the current market dynamic and should be much easier to spot. When the Fed talks up the economy and promises rate increases, the dollar usually rallies. When the dollar rallies, U.S. multi-national corporate profits take a hit, and the market falls. When the market falls, economic confidence falls and puts pressure on the Fed to maintain easy policy. This is a loop that the Fed does not have the stomach to break.

Because the Fed waited more than seven years to lift rates from zero, the cyclical “recovery” is already nearing its historical limit, if it’s not already over. This could put the Fed into a position of raising rates into a weakening economy. Normally it does so when the economy is accelerating. Some identify this delay as the Fed’s only policy error. But had it moved earlier, the recession would have simply arrived that much sooner. The Fed’s actual policy error was thinking it could build a “recovery” on the twin supports of zero percent interest rates and QE, and then remove those props without toppling the “recovery.”

But despite all this, there are those who still believe that the Fed will deliver two more rate hikes this year. Given the anemic growth over the past two quarters, the recent plunges in both the manufacturing and service sectors, average monthly non-farm payroll gains of only 116,000 over the past three months (most low-wage, and part-time) and the stakes contained in the election that is just six months away, such a conclusion is hard to reach. Instead, I expect we will get the same bar gag we have been getting for the past year. Many of those who now concede that a June hike is off the table still believe July to be a possibility. I believe the Fed will go along with that hype until it can no longer get away with it…then it will start bluffing about September, or perhaps December.

The Fed has to keep talking about rate hikes so it can pretend that its policies actually worked. But the truth is that the Fed policies have not only failed, they have made the problems they were trying to solve worse, and raising interest rates will prove it. So the Fed resorts to talking about rate hikes, to maintain the pretense that its policies worked, without actually raising them and proving the reverse. This can only continue as long as the markets let the Fed get away with it or until the numbers get so bad that the Fed has to admit that we have returned to recession. That is the point where the Fed’s real problems begin.

Peter’s podcasts are available on The Peter Schiff Channel on Youtube.

Somehow in the last few months I found myself going from merely concerned about developed-world markets to outright advocating defensive positions. I thought some of the presentations at my Strategic Investment Conference would cheer me up. They did not.

In fact, what I heard from economists, portfolio strategists, analysts, and hedge fund managers made me even more bearish. Yes, this conference by its nature tends to dwell on risks. The people I invite are successful precisely because they know how to spot (and avoid) macroeconomic risks.

This year’s crowd was generally gloomy (with some notable and vigorous exceptions), though I didn’t sense any panic. It was more frustration at the lack of clarity and choices, coupled with general concern that there is a major central bank policy error brewing. One of my associates captured the mood with this tweet on the second day.

https://twitter.com/PatrickW/status/735582566762336256

(We had several excellent sponsors, but I didn’t think to invite any antidepressant companies. We may do that next year.)

Now, you could take a contrarian view and say that “bad” is actually bullish. You might even be right – but I don’t think so. Bullish/bearish isn’t a binary state. There are alwaysshades of gray. You can be bullish on some assets and bearish on others. You can think the stock market is generally overpriced but still see value in certain stocks. You can be positive on some countries and negative on others.

In fact, most speakers had at least one if not several investment classes they were quite bullish on rather than US stocks. Mark Yusko asked the three ETF portfolio construction panelists to name their favorite country ETF. I was actually surprised when all three answered with the same country – India. There were several very positive comments on Mexico and the business climate and opportunities there. There was even a mention (by former Dallas Fed president Richard Fisher) of how efficient their regulators and bureaucracies were. Not something we hear about the US or Europe.

I think we are often pessimistic because we want easy answers. We want to either buy stocks or sell them and then do something else. Successful investing isn’t so simple. You have to observe, analyze, and consider the alternatives before you come up with the right solutions.

Sometimes you can go through that process and still end up bearish on almost everything. Richard Fisher seems to be in that camp. Asked in our final wrap-up panel Friday morning how his own portfolio was positioned, Fisher answered with one word: “Fetal.” And while his answer got a general laugh and a lot of pushback on the final panel from Niall Ferguson, who thinks he sees the beginning of an inflection point, it seemed a pretty good summary of the conference. I think most people walked away trying to think how they could position their portfolios more defensively.

My own suggestion was to diversify among trading strategies rather than among long-only asset classes, a theme that we will explore in a future letter.

You don’t often hear such candor from people like Fisher. He’s been in the banking system’s top tier for a long time and is hardly a permabear. He earned his reputation as a monetary hawk because he thought the economy was strong enough to handle higher interest rates.

Fisher also has a good bubble-spotting record. I discussed one of his speeches in a 2006 letter I called “Honey, I Created a Bubble.” Even then, he talked about the housing market entering a correction. We only later learned how painful a bubble’s bursting could be.

More recently, Fisher earned headlines last January when he claimed that the Fed had “front-loaded a tremendous market rally” in 2009. Here is a three-minute video you should watch.

Fisher’s SIC comments were broadly consistent with what you hear in the video. He thinks the markets will take a long time to digest the Fed-driven bubble, and in the meantime he is very cautious. Markets are fragile, and any kind of shock could get ugly. I believe that is what he meant by the “fetal” comment.

We will get into what those shocks might possibly be in a moment, but this seems to be a good time to bring up today’s job report. It indicated a shockingly disappointing 38,000 new jobs, with a downward revision of 59,000 jobs to the two prior month’s reports.

Some 458,000 people left the job market, which is what pushed the unemployment rate down to 4.7%. The 3-month average is now just 116,000 versus the 6-month average of 170,000 and the 12-month average of ~200,000.

The Federal Reserve had been making noises as though they might finally raise rates at the June meeting or at the July meeting at latest. It is very hard for me now to imagine them doing so. We’re watching the unfolding one of the greatest policy errors in central banking history. Not having taken the opportunity to raise rates during 2014 when new jobs were averaging 250,000, the Fed may now have waited too long, such that any rate increase, no matter how trivial, becomes a shock.

This was actually one of the main points of my own speech, that during the next global recession we’re going to see the most massive combined policy errors by central banks ever witnessed. All will not end well.

If somehow (in a world turned upside down) a President Donald Trump asked me for my recommendation as to a new Federal Reserve chairman, Richard Fisher would be on my very short list. I’m not certain he is masochistic enough to want to do it, but he is patriotic enough that he might step once more into the breach for the good of the country. (My suggestion would be the same to a President Hillary Clinton, but I would bet that the European Central Bank’s raising rates next month into positive territory is lots more likely than my ever being approached by a Democratic president on economic policy.)

What might the shocks be that Richard Fisher was alluding to? Anatole Kaletsky of Gavekal listed three global economic risk factors in his SIC remarks. Annoyingly, all three are political. I say “annoyingly” because I’m old enough to remember when governments did not pretend to control the world economy. Now governments everywhere are bigger and more ambitious, as are central banks. They still can’t control the economy, but leaders think they can, and their attempts usually make things worse.

You can watch the short video above, but in summary Anatole’s potential trouble spots are

- The June 23 “Brexit” vote in the UK

- US elections on November 7

- German elections in mid-2017.

Any one of these has the potential to spark major economic disruption. Richard Fisher said most people underestimate Brexit’s consequences. Departing from the European Union would force the UK to renegotiate hundreds of treaty agreements on everything from airport landing rights to bank settlements. Currently the UK is one of the developed world’s strongest economies. A win by the “leave” side could stop that trend, even if Brexit ultimately works out for the best.

I have friends on both sides of Brexit, by the way; and as an American I don’t get to vote. Nor does Richard Fisher. I will respect whatever decision the UK voters make. Their house, their rules. Regardless, their choice will affect the whole world. Just as many international readers are unsettled by the concept of a Donald Trump presidency, my English readers should understand the concerns of those who look upon the Brexit vote in much the same way. Brexit will bring changes to the system, if it happens, and we’re not sure how those changes will affect us and whether they will be good.

The same is true, possibly more so, if American voters send Donald Trump to the White House. Whatever you think about Hillary Clinton (and I will admit I don’t think much), she is at least a known quantity. Nothing she does is likely to rattle the markets. Trump, should he win, will bring an entirely new way for Washington to operate (and that is not necessarily bad). His trade, immigration, tax, and foreign policies could be quite unlike what anyone alive today has seen before.

David Rosenberg, for his part, thinks Trump will be good for the economy but bad for Wall Street. Watch this:

While we’re talking about Trump, you might also like these clips from George Friedman and Pippa Malmgren.

Eurasian Headache

George Friedman was as geopolitically negative as some of the other speakers were on the economy. He thinks the Eurasian landmass, home to most of the human race, is falling apart. The European “Union” is a troubled relationship at best and could soon see an ugly breakup. Russia is struggling to find balance in a post-Soviet, post-oil world. China has to make a tough transition away from its export boom years and build a sustainable domestic economy. And Middle East problems continue to foment.

The German problem Anatole Kaletsky listed as a key risk is on Friedman’s radar screen, too. Friedman believes Germany is far too dependent on exports that are now dwindling as its customers tighten their belts – and that is before we enter a global recession. The situation might be manageable if other challenges weren’t also demanding attention.

- Merkel may have successfully papered over the Greek debt problem, but she won’t be so lucky with much larger Italy. The banking system there is completely unsustainable. (George and I have shared notes and discussions on this topic. The picture in Italy is much more serious than the mainstream media is portraying).

- The refugee crisis is going to get worse before it gets better, and frictions will likely strengthen Germany’s right-wing and nativist political parties. Presently they are no threat to Merkel’s leadership but could well become so after 2017 elections.

- A renewed NATO Cold War against Russia is forcing Germany to increase defense spending and devote more attention to foreign policy at the precise time it really needs to get its home situation straight.

- As pessimistic as George was on Eurasia, he was almost equally positive on the New World. He thinks the Canada/US/Mexico trade zone is the world’s economic center of gravity. No one else has the same combination of domestic demand, technology, innovation, innovation, and political stability. Yes, we have problems, not least of which is the massive debt we accrued in the course of reaching this dominant position. Other than Brazil (and the distressingly sad case of Venezuela), however, the Americas are in far better shape than Europe, Asia, or Africa.

After the first day’s generally negative talks by analysts and economists, everyone was ready for a real-world view. How did someone who actually manages real money see the situation? We had several panels and speakers on that topic. Let’s focus on one – my good friend Mark Yusko, who heads Morgan Creek Capital Management. He manages billions and pioneered the endowment approach many universities now take with their portfolios. Surely, you might think, someone in his position would have a more enlightened view than those bearish economists.

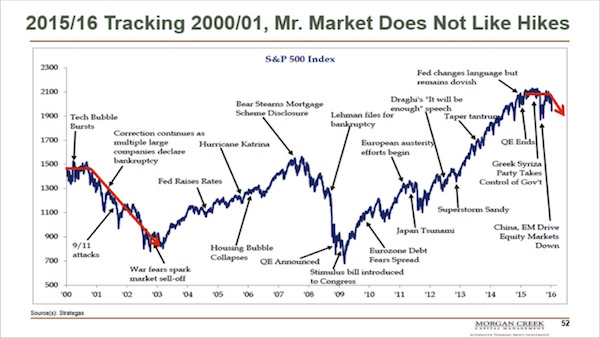

Enlightened, yes, but hardly bullish. Mark poured cold water on whatever bullishly warm feelings the audience may have clung to. He listed not one but ten plausible scenarios that could send markets down to the basement. I will focus on his “Surprise #6: Déjà vu, Welcome to #2000.2.0.”

That’s right: Mark says it’s year 2000 all over again. That was when the tech bubble popped and sparked an ugly bear market and recession.

This theme resonated for me because this very newsletter actually grew out of my late-1990s updates on the Y2K problem. In a sea of pundits forecasting either doomsday or no problems at all, I was firmly in the middle and believed that the combination of economic imbalances (including the tech bubble) and computer glitches would land us in a recession. All my research told me we would see some problems and disruptions but not the collapse of civilization. That call turned out to be right. Even more amazingly, the portfolios I suggested in my book at the time, The Y2K Recession, turned out to be right on target. I don’t think I have ever been as lucky with my prognostications since that time.

Among the disruptions, however, was the Federal Reserve’s move to withdraw the liquidity it had pumped into the system for those who expected a payment system breakdown and thus hoarded physical cash. Alan Greenspan took the fed funds rate from 5.4% on Y2K day to 6.5% in October 2000.

(Younger readers will do a double-take on those numbers. Yes, borrowing overnight money once cost more than 6%. Furthermore, the Fed is perfectly capable of hiking rates 100 basis points or more in less than a year. Or at least it used to be.)

The bear market that followed was, at the time, the most significant anyone had seen since the early 1980s. High-flying tech stocks crashed, one after the other; and Bill Clinton’s move to release Human Genome Project data sent the biotechnology sector up in flames. It was a painful time that no one who lived through it wishes to repeat – but Mark Yusko thinks we will repeat it, starting now. Here’s one of the 100 or so slides from his presentation.

In the 2000–2003 period we had the tech bubble bursting, corporate scandals like Enron, the 9/11 attacks, and an honest-to-God, old-fashioned, job-killing recession. I remember at the time how everyone kept thinking, “Ok, this has been bad, but it’s over now.” But it wasn’t over. After repeated fake-outs and final capitulation, we finally emerged from the muck (just in time to start an unsustainable housing bubble, but that’s another story). It was at the end of that recession that I coined the term Muddle-Through Economy.

One thing people forget is that we had a very accommodative Fed during that time. As I said above, Greenspan pushed short rates up to 6.5% in September 2000. Just a year later, he had them down to 3% and ultimately to 1% in mid-2003. That Fed was willing to move at light speed if it thought it necessary, unlike more recent regimes.

Another eerie parallel Mark noted was in corporate earnings. Observe the red dashed line in this chart.

The shaded areas are the last two recessions. We see that earnings peaked a few quarters ahead of each recessionary period, then slid deeply into negative territory before recovering as the recession ended.

This time around we seem to be about halfway down to the trough. It’s entirely possible we are in a recession right now and don’t know it yet. The start date is discernible only in hindsight.

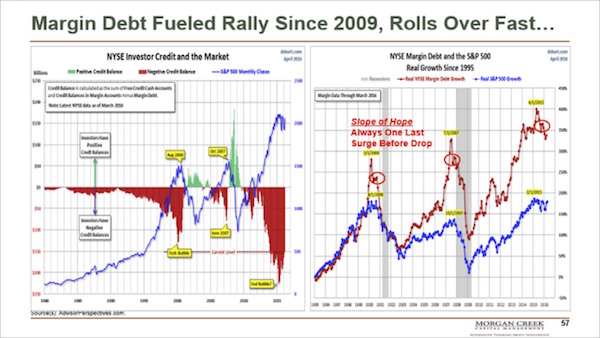

Margin debt is another bad sign. The red area in the left chart below shows how debit balances build up right along with market peaks.

Again, right now we appear to be in a place much like the early stages of the last two bear markets.

Finally, 2016 also marks the eighth year of the presidential cycle. The average stock return for the eighth year of all US presidential terms since 1901 is -14%. So if you liked 2000 and 2008, you should love the way 2016 ends (gulp). (By the way, I admit that there are not many data points to actually determine whether there is anything to the eighth year of the presidential cycle. The chart might just be data mining to make your bearish argument look good. Then again…)

So where in all this do we find any hope? Mark explained in his voluminous quarterly outlook (read it here, and please note that you have to get to page 27 before you actually begin the analysis. The first part is a comparison of Prince and Shakespeare to the markets. Fun reading, though…)

In the equity markets, gains most often happen slowly and losses usually happen quickly. You can see this in the numbers, as the average bull market is much longer than the average bear market (more than five times longer at 97 months versus 18 months). Therefore, it is critical to always be looking for long opportunities, especially during the brief corrective periods (when things go on sale). To reiterate a point we have discussed in prior letters which was a paraphrase of the line from The Merry Wives of Windsor, “The essential problem that we highlighted last quarter is that when it comes to bubbles and crises, you can be a few hours early, but you can’t be one minute late.”

To use another old quote, the time to buy is when blood is running in the streets. If, like Mark Yusko, you are already in defensive positions (or in Richard Fisher’s fetal position), you will soon have some excellent buying opportunities. Those with less foresight are going to dump some valuable assets, not because they want to but because they have no choice. They’ll need the liquidity.

What should you buy? That’s not entirely clear yet, nor will we be able to catch the precise bottom. As they say, no one will ring a bell. But if Mark Yusko is right, the chance ought to arrive in the next year or so.

I could go on for another hundred pages sharing the new information we heard at SIC. I think you have a lot to chew on, though, plus some videos to watch and re-watch, so I’ll leave it there. More next week.

A funny thing about the fetal position: babies eventually find their way out of the darkness and into the real world. They encounter pain and tears on the journey but are always glad they made it.

We who go through the coming economic rebirth will likewise feel some pain. Yet the pain will have a purpose. It will end in due course, and we’ll have a new world to enjoy.

John Mauldin

subscribers@mauldineconomics.com

Given the correction Rambus Chartology has an excellent take on Gold Stocks: Be Prepared

With crude oil surging 2.3 percent as the Dow moved toward the 18,000 level and gold and silver consolidated recent gains, today James Turk told King World News that what we just witnessed was a huge wakeup call for the world.

With crude oil surging 2.3 percent as the Dow moved toward the 18,000 level and gold and silver consolidated recent gains, today James Turk told King World News that what we just witnessed was a huge wakeup call for the world.

James Turk: “Commodities are moving back to center stage, Eric. Last Friday’s unemployment report was a huge wakeup call…continue reading HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair