Timing & trends

Over the last couple of weeks, the market has been working off the overbought condition that accrued from the surge off the February lows. As I wrote recently:

“With the markets still extremely overbought from the previous advance, the easiest path for prices currently is lower. The clearest support for the markets short-term is where the 50 and 200-day moving averages are crossing. I currently have my stop losses set just below this level as a violation of this support leaves the markets vulnerable to a retest of February lows.”

“On a short-term (daily) basis, the current correction is still within the confines of a more normal “profit-taking” process and does not immediately suggests a reversal of previous actions. As shown in the chart above, support currently resides at 2020 & 2040 with the 50-day moving average now trading above the 200-day. “

The yellow band in the chart above is the ongoing trading range the market has remained mired in since May of 2014.

As I have stated in the past, by the time a rally occurs that is strong enough to reverse bearish signals, the market is generally extremely overbought. The market must then work off that overbought condition before the next advance can occur.

“The current correction was not unexpected. It was a function of time before the extreme short-term extension of the market corrected. Like stretching a rubber band to its limits, it must be relaxed before it is stretched again. The question is whether this is simply a “relaxation of the extension” OR is this a resumption of the ongoing topping and correction process?”

Should I Stay Or Go?

It is the last part of the statement above that I want to address this week.

Is this just a correction within the confines of a bullish advance OR is the recent market action just a continuation, and eventual completion, of a market topping process?

The answer: It depends on your investment time frame.

If you are a trader with a time horizon that is from days to a couple of months, the backdrop to the markets are currently more bullish than bearish. As shown below, the number of advancing stocks has broken out of recent downtrends which has historically related to more bullish underpinnings.

However, if you are a longer-term investor, particularly within a couple of years of retirement, market dynamics are still exceedingly negative. As shown below, despite the recent surge in the market, not unlike that seen in Oct 2014 and 2015, is still contained within a topping process as witnessed during the peaks of the previous two bull markets.

As Michael Kahn penned this past week in Barron’s:

“Like life, the stock market is rarely black or white. Right now, however, the outlook is particularly muddled. In technical analysis, when moving averages cross over each other to the downside we call it black. When they cross to the upside we call it golden. Now, the market is giving off mixed signals, making it no more than a bland beige.”

This is a problem for investors, who despite saying they are long-term investors are always driven by short-term market swings which impact emotional biases. He concludes:

“There is a good argument that stocks are ripe for a correction after a sharp rally, but with the undercurrents in sectors, interest rates, and breadth there is not enough evidence to hand the reins over the bears. Bulls, however, do not have much room for error. The falling U.S. dollar may be the handwriting on the wall, and the Fed better be very careful with its decision at next month’s meeting.”

It is this ongoing “limbo” that continues to weigh on investor sentiment. While the “bulls” have once again emerged onto the field, there is not enough “evidence” currently to suggest an aggressive risk posture in portfolios.

As Bill Henry once quipped: “It is better to be out of a bull market than fully invested in a bear market.”

…read Lance’s “It’s all Connected and the Monday Morning Call HERE (scroll Down)

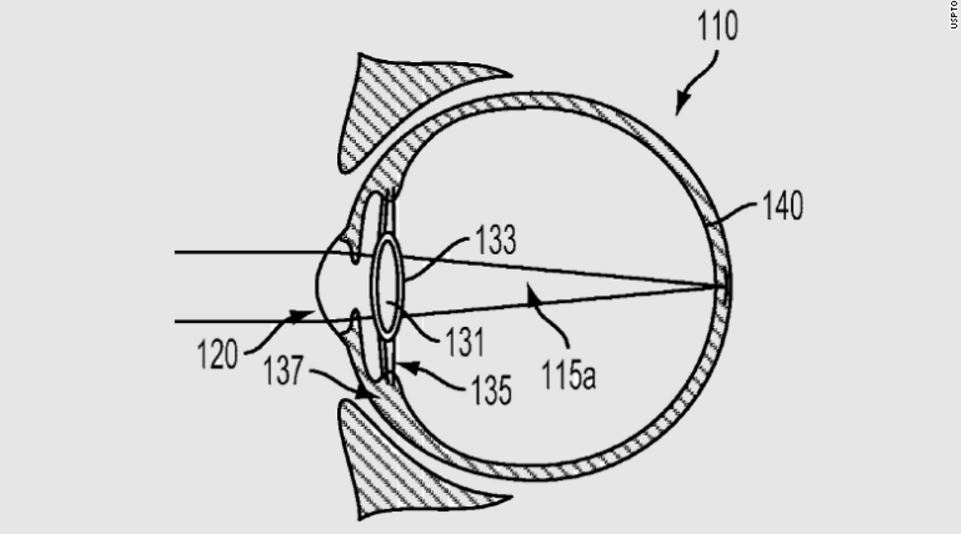

Are you ready for this one? Google was approved for a patent where they can remove the lenses in your eye, fill it with fluid, and then place a device in there. You will no longer need to wear glasses with the device, and you no longer need a camera since it comes equipped with a camera and video recorder. I suppose the government will figure out a way to include an x-ray feature so that they can walk down the street and see who has money on them.

also from Martin:

Many people do not realize that the global warming/climate change deals in Europe will eliminate gasoline and diesel cars on the streets come 2020…..continue reading HERE

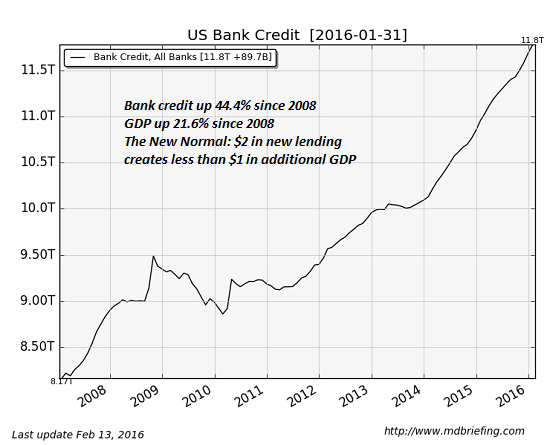

But the New Normal is anything but normal; all the readings of artificial life-support and manipulation are off the charts. If the New Normal were indeed a return to normalcy, we’d see a rapid and sustained decline in official life-support of the economy.

to view all 8 charts and commentary..continue reading HERE

Within this there is an industry that is fabulously successful with unlimited potential. Make sure to listen to Mark Leibovit’s interview with Michael Campbell

Donald Trump’s critics have heaped scorn on his calls for protective tariffs to deal with America’s widening trade imbalance and the resulting loss of higher-paying blue color jobs. Some have accused him of trying to turn back the clock in pursuit of a cheap populist ploy and have said that he simply refuses to acknowledge that America is now an information and service economy for which large trade deficits are the new normal. But voters are sensing that The Donald is right to sound alarm bells, and that something radical needs to be done to revive manufacturing to make America great again. But his tariff solution is hardly the best medicine. To be honest, given the even worse solutions that are being offered by the left, Trump’s instincts may be preferable.

Donald Trump’s critics have heaped scorn on his calls for protective tariffs to deal with America’s widening trade imbalance and the resulting loss of higher-paying blue color jobs. Some have accused him of trying to turn back the clock in pursuit of a cheap populist ploy and have said that he simply refuses to acknowledge that America is now an information and service economy for which large trade deficits are the new normal. But voters are sensing that The Donald is right to sound alarm bells, and that something radical needs to be done to revive manufacturing to make America great again. But his tariff solution is hardly the best medicine. To be honest, given the even worse solutions that are being offered by the left, Trump’s instincts may be preferable.

Ironically, in the late 19th and early 20th Centuries, the elimination of tariffs was a populist issue. A little more than a century later, the polls have reversed completely. Prior to the introduction of the income tax in 1913, tariffs were the Federal Government’s principal source of revenue. During the long and contentious campaign to enact the 16th Amendment (which allowed the government to tax incomes for the first time since the emergency Civil War-era 3% to 10% income tax), proponents argued that the passage of a “soak the rich” income tax would allow the government to repeal the tariffs and thereby transfer the tax burden from the working class, who paid the tariffs through higher prices on imports, to the ultra-wealthy, who were the sole target of the income tax as it was originally conceived, packaged and sold.

(The tax originally imposed rates from 1% to 7%, and only applied to fewer than 1% of Americans. The 99% supported its enactment solely because they believed they were getting something for nothing, in this case, government services paid for by the rich. In fact, in 1895, when the Supreme Court bravely declared the government’s first attempt to replace tariffs with an income tax unconstitutional, the justices were personally vilified as defenders of the rich.)

But once the Federal Government got its foot in the door, it rapidly raised the tax rates and expanded the base of taxpayers, ultimately subjecting the middle class to rates far higher than anything originally contemplated for the Rockefellers, Carnegies, or Vanderbilts. If this does not provide a sterling example to the legions of Democrats “Feeling the Bern” of how class warfare can backfire on the class waging the war, I don’t know what does. Ironically, no single tax has done more harm to the middle class than the income tax.

So while the populist movement of the early 20th Century demanded the removal of tariffs, the populist movement of today wants to bring them back. But Trump is not talking about replacing income taxes with tariffs. He simply wants to add tariffs to the existing tax structure (though he does want to lower the rates). This will only compound our problems and make our economy far less competitive. It will not bring back our jobs; it will only increase the tax burden on the American economy, destroying even more jobs. If we want to undo the deal we made with the devil over 100 years ago, we need to repeal the income tax as well.

If that substitution were on the table, I would argue that tariffs offer the lessor burden. Tariffs are a much simpler form of taxation that do not require armies of accountants, lawyers, and tax preparers, who are needed to comply. And while we are repealing the income tax, we should repeal most of the other federal taxes (particularly the payroll and estate taxes) and laws enacted since then as well. But that is not what is being discussed.

Our trade deficits do not result from bad deals but bad laws. Put simply, the amount of taxation and regulation that have been layered on our business owners and their employees have made it impossible for American firms to compete with foreign rivals. Contrary to the currently popular talking points, low wages are not the only means to establish successful trade balances. America became the dominant exporter in the world in the 19th and 20th centuries while our currency was strengthening, we were paying the highest wages, and our workers enjoyed the world’s highest living standards.

Germany is doing so today. Strong economies compete with quality, innovation, efficiency, and flexibility. Those capacities have been stifled by government policies that have nothing to do with trade agreements and have everything to do with domestic policies. We need to repeal those laws. Trade deficits are not the problem. They are the consequence of the problem. The problem is big government, financed largely by the income tax, which has made America uncompetitive.

But it is unlikely that tariffs alone, or even a broad-based national sales or value-added tax, could bring in all the revenue generated by the direct taxes we should eliminate. To survive on excise taxes, as the founding fathers envisioned, requires making the Federal Government a lot smaller.

But Trump is not promising to make government smaller. If anything, he is promising to make it even bigger. He has made no promises to cut government spending across the board, including popular “entitlements” like social security, which Trump has promised not to touch.

To make America great again, we need to recreate the free-market environment that made her great in the first place. It’s not just oppressive direct taxes that must go. It’s all the regulations that have driven up the cost of doing business, and labor laws that make employing workers so expensive and risky that business does all it can to create as few jobs as possible.

But contrary to Trump’s stump speeches, our trading partners are not taking advantage of us; we are taking advantage of them. They give us their products and we give them nothing but our debt. They expend scare resources (land, labor and capital) to create consumer products for us to enjoy, while we just conjure intrinsically worthless dollars out of thin air. But years of excessive regulation and taxation have resulted in an accumulation of trade deficits that has transformed America from the world’s largest creditor to its largest debtor. Our once mighty savings financed a high-wage industrial economy that has been hollowed out, replaced by a weak, debt-financed, low-wage service sector economy.

Trump is right. This is a big problem and it needs big solutions. If tariffs were offered as a replacement to our ridiculous and destructive personal and corporate tax, and payroll and estate taxes, then America may become more competitive and our greater efficiency may even allow us to overcome the tariffs that other countries would likely impose on us in response. But slapping tariffs on imports, while doing nothing to improve the conditions for business efficiency, simply means that prices for American consumers will rise significantly, without sparking a revitalization of American manufacturing prowess. Don’t forget the global market contains over 7 billion consumers, the U.S. market just under 320 million. Insulating our manufacturers from this larger marketplace guarantees that we will never become globally competitive.

Tariffs or sales taxes will drive up the cost of goods for consumers, a fact that Trump seems to ignore. If he would acknowledge this issue, he could offer the counter argument that if we could couple tariffs with income tax relief that Americans would also have higher incomes to pay those higher prices. But even if incomes rise, higher prices will inevitably lead to less consumption and more savings, especially if we allow interest rates to be set by the free market rather than the Federal Reserve. More savings and less spending is exactly what we need if we want the capital to rebuild our industry. Protective tariffs alone will not work, especially when there is little industry left to protect.

So instead of criticizing Trump for his misguided advocacy of tariffs as a panacea, we should at least give him credit for recognizing a serious problem that so many others ignore. The real criticism should be directed at those who would allow America to continue down this self-destructive path.

Read the original article at Euro Pacific Capital

Best Selling author Peter Schiff is the CEO and Chief Global Strategist of Euro Pacific Capital. His podcasts are available on The Peter Schiff Channel on

The stock price of Tesla Motors (TSLA) has soared along with the recent announcement that pre-orders (i.e. a fully-refundable $1k deposit) for its Model 3 are approaching 400,000 units. The Model 3 is purported to sell eventually for an estimated $35,000; and is Silicon Valley’s inexpensive electric vehicle (EV) offering that appears to be affordable for everyone; except Tesla that is.

The stock price of Tesla Motors (TSLA) has soared along with the recent announcement that pre-orders (i.e. a fully-refundable $1k deposit) for its Model 3 are approaching 400,000 units. The Model 3 is purported to sell eventually for an estimated $35,000; and is Silicon Valley’s inexpensive electric vehicle (EV) offering that appears to be affordable for everyone; except Tesla that is.

After all, Tesla loses more than $4,000 on each of its high-end Model S electric sedans; and that model’s cost is between $70 and $108k. With margins like that one has to assume a $35k Model 3 can’t be the answer to solving Tesla’s red ink.

Tesla’s income statement reveals the company is hemorrhaging cash at a robust clip. Furthermore, according to “The Street Ratings”, their net profit margin of -26.38% is significantly below that of the industry average. The company has a quick ratio of 0.49, which means they have .49 cents in available cash to pay every $1 of current liabilities.

Worse than its lousy earnings and cash flow, Tesla is grossly overvalued compared to its peers. Tesla’s market cap is $33 billion, compared to Fiat Chrysler (FCAU) at just $10 billion and Ferrari at $8 billion. Being valued at 3x more than FCAU–an established and profitable company–looks especially absurd when considering FCAU produces annual sales of over $120 billion while TSLA produces revenue of only $4 billion.

Furthermore, Tesla’s market cap is 66% of General Motors market cap. This is despite the fact that General Motors has a history of selling ten million cars at a profit each year and Tesla sold less than one hundred thousand cars last year at a loss. They would have to sell 6.6 million cars this year to justify its current valuation. With less than 400,000 cars on pre-order that doesn’t appear likely anytime soon. And those orders for the Model 3 are fading fast. During the first week of reservations Mr. Musk indicated there were 325k pre-orders. In week two the company claimed it received pre-orders that were “approaching” 400k. And in week number three, Tesla reported the total number of orders were “almost” 400k. At that rate it will be hard to imagine it could reach that 6.6 million vehicles sold benchmark.

But perhaps Tesla isn’t about current profitability or cash flow; Tesla is all about the man and the company’s future… after all, Elan Musk landed a rocket on a barge.

But those who actually know the auto industry are not so sure. In a February interview with CNBC’s Squawk Box, Former GM executive Bob Lutz notes that “[TSLA] costs have always been higher than their revenue…They always have to get more capital. Then they burn through it.”

First, he notes that on the back of falling oil prices demand for electric vehicles (EVs) is slowing. Second, there is growing competition that will cut into Tesla’s margins as prices for EVs fall. Tesla has a lot of competition over the next few years. The industry is already awaiting the Apple car with baited breath that is set to launch in four years. And GM’s Chevy Bolt is similarly priced with a similar range and is set to come out this year. And then we have the Nissan Leaf expected to more competitive in the coming months and years. And add to that first generation vehicles like the BMW i3.

And in China, they have the EV Company LeEco, which recently unveiled its very first electric car that includes self-driving and self-parking capability using voice commands via a mobile app. Besides LeEco, there is another Chinese EV automaker that sold more electric cars last year than Tesla, Nissan or GM, it’s called BYD Co. and is now targeting the U.S. market.

Lutz believes that competition from industry heavyweights like these could “kill” Tesla in the future. “The major OEMs like GM, Ford, Toyota, Volkswagen, etc…they have to build electric cars, a certain number, in order to satisfy the requirements in about half of the states. Those have to be jammed into the marketplace, otherwise they can no longer sell SUVs and full-size pickups and the stuff that they really make money on. So that is going to generically depress the prices of electric vehicles,” Lutz warns.

Lutz also explains that companies such as General Motors will not be making any money on their “Tesla killer”. They are making these vehicles to appease Washington. Luz notes, “The majors are going to accept the losses on the electric vehicles as a necessary cost of doing business in order to sell the big gasoline stuff that people really want. Well, Tesla does not have that option,”

But Musk has a strategy for driving down the cost of his electric car that hinges on achieving economies of scale, bringing down the production cost of the battery pack by 30%. This hinges on the success of their future Nevada home called the “Gigafactory”.

The Gigafactory is a one-stop shopping in battery pack production. The company currently buys battery packs through a deal with Panasonic and has partnered with Panasonic in this venture. Production volume at the Gigafactory is anticipated be the equivalent of 30 gigawatt-hours per year; this would mean the Gigafactory would produce more storage than all the lithium battery factories in the world combined. The $5 billion dollar plant is as big as the Pentagon Tesla, and Tesla is hoping to produce 500,000 lithium ion batteries annually.

Musk recently laid out his Energy-branded battery ambition in rock star glory. At the event spectacle, Musk declared that his batteries would someday render the world’s energy grid obsolete. “We are talking about trying to change the fundamental energy infrastructure of the world,” he said.

Musk envisions his affordable, clean energy will one day power the remote villages of underdeveloped countries as well as allowing the average homeowner in industrial nations to go off the grid.

But before you sever your ties with your electrical company, it’s worth noting that not everyone thinks Musk’s plans are achievable – at least not in the time frame he envisions.

Panasonic, the supplier of the lithium-ion cells that form the foundation of Tesla’s batteries, and partner on the company’s forthcoming battery factory – calls Musk’s claims a lot of hyperbole.

Phil Hermann, chief energy engineer at Panasonic Eco Solutions, notes: “We are at the very beginning in energy storage in general.” “Most of the projects currently going on are either demo projects or learning experiences for the utilities. There is very little direct commercial stuff going on.” “Elon Musk is out there saying you can do things now that the rest of us are hearing and going, ‘really?’ We wish we could, but it’s not really possible yet.”

And far from the grand stage with little fanfare buried in their November 10Q Tesla also sought to tamper investor’s expectations: “Given the size and complexity of this undertaking, the cost of building and operating the Gigafactory could exceed our current expectations, we may have difficulty signing up additional partners, and the Gigafactory may take longer to bring online than we anticipate.”

With a company saddled with debt and cash-strapped, who is going to shoulder the burden of a delay in the Gigafactory realizing its full potential? That would be shareholders through stock dilution or the American tax payer – but most likely a combination of both. There are those who believe that Musk’s real genius is in following government subsidies.

According to the Los Angeles Times, all of Musk’s ventures: Tesla Motors Inc., SolarCity Corp. and Space Exploration Technologies Corp., known as SpaceX, together have benefited from an estimated $4.9 billion in government support. The figure underscores a common theme running through his emerging empire: a public-private financing model underpinning long-shot start-ups.

Tesla’s model relies strongly on a “green” administration. In a recent filing they note:” We currently benefit from certain government and economic incentives supporting the development and adoption of electric vehicles. In the United States and abroad, such incentives include, among other things, tax credits or rebates that encourage the purchase of electric vehicles. Nevertheless, even the limited benefits from such programs could be reduced, eliminated or exhausted…” In certain circumstances, there is pressure from the oil and gas lobby or related special interests to bring about such developments, which could have some negative impact on demand for our vehicles.”

The promise is that the Tesla stockholders and the tax subsidizing public will greatly benefit from major pollution reductions as electric cars break through as viable alternative and gain access to mass-market production.

But are electric cars really good for the environment?

First, it’s important to note that at this time, these cars don’t power themselves – they are plugged into an outlet in your garage that connects to an electric power plant, and there is a good chance that you may be one of the 33% of Americans whose power plant is burning the dirtiest fossil fuel of all…coal. So in effect, you may as well be filling up your gas tank with coal, and coal-burning power plants emit not only CO2 but also other venomous gases such as nitrogen oxides and sulfur dioxide in greater quantities than traditional gas-powered cars.

Furthermore, there are a lot of environmental questions about the lithium battery itself. In a 2012 study titled “Science for Environment Policy” published by the European Union, a comparison was made of the lithium ion batteries to other types of batteries available such as; lead-acid, nickel-cadmium, nickel-metal-hydride and sodium Sulphur. They concluded that the lithium ion batteries have the largest impact on metal depletion, making recycling more complicated. Lithium ion batteries are also the most energy consuming technologies requiring an equivalent of 1.6kg of oil per kg of battery produced. Furthermore, they ranked the worst in greenhouse gas emissions with up to 12.5kg of CO2 equivalent emitted per kg of battery.

Next, you need to understand how lithium is mined. Lithium, in its purest form, must be mined through hard rock or salar brines. According to Friends of the Earth, an environmental group, salar brines, the most economical way of obtaining lithium, destroys the environment. They state: “The extraction of lithium has significant environmental and social impacts, especially due to water pollution and depletion. In addition, toxic chemicals are needed to process lithium. The release of such chemicals through leaching, spills or air emissions can harm communities, ecosystems and food production. Moreover, lithium extraction inevitably harms the soil and also causes air contamination.”

Simply stated, batteries such as Panasonic’s automotive grade li-ion batteries that are developed jointly by Panasonic and Tesla and are in the Model S have a substantially negative effect on health and the environment.

The plain truth is owning a Tesla is not as green as Elon Musk would like you to believe. And for environmentalists to put all of their faith on Evs to cut down on greenhouse gases could end up diverting attention from greener alternatives to power autos. And although Musk is a genius and a visionary; it is also true that Tesla has an unproven business model and a stock that is massively overpriced. According to industry experts, Musk will find it improbable ever to turn a profit with its mass-produced Model 3. Even if some year in the distant future there exists the charging infrastructure and pricing available to make Electric Vehicles conducive to supplant the internal combustion engine, Tesla faces an onslaught of competition that will most likely drive its profit margins further into the red for years to come. Avoiding TSLA stock at the current mindless valuation could not only benefit the environment…but also end up saving your retirement as well.

also: Be sure to listen to Mark Leibovit on Fabulous Opportunities & “Unprecedented in Potential Demand”

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair