Timing & trends

Thoughts from our recent conversation with Alec Ross on his new book, Industries of the Future, which can be listened to on the Newshour podcast page here or on iTunes here.

Thoughts from our recent conversation with Alec Ross on his new book, Industries of the Future, which can be listened to on the Newshour podcast page here or on iTunes here.

We frequently hear about automation and artificial intelligence encroaching on paid labor, and many of us want to know about the future of work. Recently, Alec Ross joined Financial Sense to discuss his new book,The Industries of the Future, a number one best-seller on Amazon.

33 Facts About Women in Technology

Today’s infographic covers almost everything you ever wanted to know about women in tech.

It highlights the world’s most successful women tech entrepreneurs, the workforce composition of major tech companies, and the most powerful female CEOs and venture capitalists.

There’s no shortage of information in today’s graphic.

View 33 Facts About Women in Technology

It’s possible that the EdTech sector has arrived at the much vaunted inflection point. Every year it seems that there are more and more companies with revenue and sustainable business models. This is different than in years past. This is happening for a variety of reasons; according to EdSurge the three biggest ones are:

It’s possible that the EdTech sector has arrived at the much vaunted inflection point. Every year it seems that there are more and more companies with revenue and sustainable business models. This is different than in years past. This is happening for a variety of reasons; according to EdSurge the three biggest ones are:

More accountability: There is more scrutiny of K-12 and postsecondary institutions to improve performance.

Infrastructure: Mary Meeker’s 2015 State of the Internet report identifies education as a market in which the impact of the Internet is “just beginning.” A recent Houghton Mifflin Harcourt survey of educators reveals that only 23% of students are using a laptop or desktop daily to do class work (and only 9% on tablets). This is changing as one-to-one adoption gathers steam.

Streamlined distribution models are emerging that enable smaller entrants to elbow their way into domain historically dominated by larger companies that rely on “feet on the street” distribution models.

But how does this translate into quantifiable performance for investors? Let’s examine some of the recent successes (or failures) of both private and public EdTech and education companies.

Private EdTech Companies

In order to assess the strength of private companies, we used CB Insights’ Company Mosaic score, which uses public data and predictive algorithms to analyze the global education technology startups.

First on their list is Duolingo, a US-based language-learning website. It raised a total of $83.3M and is backed by investors such as New Enterprise Associates and Kleiner Perkins. Second is another US-based startup, Udemy, which offers online courses. It has received $113M in financing and is backed by Insight Venture Partners and Norwest Venture Partners, among others. But two of the companies, Descomplica and Toppr, are focused on Brazil and India, respectively. And news reports state that China is Coursera’s second-biggest market.

There have been plenty of predictions lately that all this investment would result in exits – that is, IPOs, mergers, and acquisitions – that would “defy historical trends” and all of the recent deal flow has certainly been indicative of that.

Public Education Companies

If you’ve read our second installment in this series – Who Is Investing In Education Technology? – then you’d know that 2015 was actually a record-setting year for EdTech investment if you look at the total dollar figures. CB Insights noted, “the period from 2010 to 2014 saw more than a 503% growth in investment dollars.” So how does this translate to the capital markets? Click on the links below for charts of the stock performance (select weekly for longer term performance) from various for-profit education (they are NOT necessarily EdTech companies because there weren’t really any pure plays that we could find) companies:

NASDAQ: TWOU (2U INC.)

NYSE: CHGG (CHEGG INC.)

NYSE: EDU (NEW ORIENTAL EDUCATION & TECH GROUP)

NASDAQ: APOL (APOLLO EDUCATION GROUP INC.)

NYSE: BPI (BRIDGEPOINT EDUCATION INC.)

NASDAQ: CPLA (CAPELLA EDUCATION COMPANY)

NYSE: DV (DEVRY EDUCATION GROUP INC.)

NASDAQ: STRA (STRAYER EDUCATION INC.)

NYSE: LRN (K12 INC.)

NYSE: PSO (PEARSON PLC)

Honestly, it is quite underwhelming over a five-year period when examining the group as a whole. That said, this is largely a group of public education companies, not distinctly EdTech companies. I’d like to believe that this poor performance can largely be attributed to new EdTech startups entering the space displacing the incumbents’ respective market share promulgated by recent industry developments, namely: more accountability; infrastructure; and streamlined distribution models.

Robb Doub, general partner with New Markets Venture Partners in Fulton, told The Baltimore Sun his firm has focused on EdTech for the past eight years with steady successes. Its local portfolio has included Calvert Education Services, a distance-learning venture sold to a private equity-led investment group in 2013, and Moodlerooms, an open-source education software company sold to Blackboard Inc. in 2012. He said he sees more successes ahead for EdTech investors. “We think there’s a lot of opportunity and the education space is ripe for change and innovation,” Doub said. “We continue to look aggressively at EdTech both in the region and across the country.”

While education companies may not experience Uber’s hockey stick growth, an argument could be made that they are less volatile and have more predictable and proven business models and customers. Furthermore, EdTech companies offer investors self-gratification knowing that they are impressing a large social impact with their dollars. So, when evaluating making an investment in an EdTech company please consider some of the following:

- Comparable technology/valuations

- Capital efficiency

- How they balance cost-effective growth with monetization to build a sustainable business

- Look for those that have gotten rid of the same old top-down, boots on the ground monetization strategy (it is slow, expensive and sales cycles can be infamously bureaucratic)

- Look for those whom have identified the potential of the “consumerization of IT” movement by recognizing that the voice of the end user (in this case, teachers) has become more and more influential when determining where budgets get allocated

- Ability to scale their revenues without having to build massive sales teams and/or deploy “boots on the ground”

- Consider a diversified portfolio that takes into account the rapidly growing U.S. market, as well as in China where EdTech is booming and other emerging markets

Not all education companies are created equal. Through our analysis we have found that private EdTech companies greatly outperformed the for-profit public education companies. That said, there are exceptions to the rule. Lingo Media (chart) achieved the greatest appreciation in both share price, gaining 745%, and in market capitalization, gaining 992%, amongst all 2016 TSX Venture companies. With ideal market conditions now coalescing, knowing how to execute is the really difficult part and also where Lingo Media prides itself.

Please visit us on our website at www.lingomedia.com to learn even more about investing in EdTech. Lingo Media is Changing the Way the World Learns English. There’s a market, a real problem and a real solution – be part of that solution today.

An ounce of patience is worth a pound of brains.

Dutch Proverb

Throughout this bull-run, a plethora of reasons has been laid out to indicate why this bull should have ended years ago. Mind you most of those reasons are valid, but that is where the bucket stops. Being right does not equate to making money on Wall Street. In fact, the opposite usually applies. The Fed recreated all the rules by flooding the markets with money and creating and maintaining an environment that fosters speculation.

The reason this is the most hated bull market in history is because there is no logical reason to justify it. In 2008-2009 volume on the NYSE was in the 8-11 billion ranges and sometimes it surged to 12 billion. Before that, every year, the volume continued to rise, this indicates market participation. From early 2010 volume just vanished, it dropped to the 2-3 billion ranges and even lower on some days. Hence, all market technicians and students of the markets assumed that the markets would tank as markets cannot trend higher on low volume and that is where they erred.

We were and still are in a new paradigm; the US government stepped in and started to support the market directly that is why volume dropped so dramatically. However as there were no sellers, the markets drifted upwards. Later on, they got the corporate world in on the scam. They set up the environment that propelled corporations to buy back their shares by borrowing money for next to nothing and then using this trick to inflate t EPS (earnings per share), without doing any work or even increasing the profitability of the company.

In between a few minor corrections were allowed to transpire almost all of which took place on ever lower volume, to create the illusion that there was some semblance of free market forces at play. The current correction is the only one since 2011 that is real in nature, and it could prove to be a precursor to a larger upward move. If you recall, the dot.com era, the markets corrected strongly in 1998, it looked like the end was near but then the NASDAQ had its best year ever in 1999. It had tacked on gains of roughly 100%. The chart below highlights this dramatic reversal.

Finally, we also have something known as dark pools, this, in essence, allows institutions to purchase large blocks of shares without leaving any tracks. Dark pools now account for over 40% of all U.S stock trades. Theoretically, it provides the government via the PPT (plunge protection team) an avenue to manipulate the markets without leaving any evidence of foul play.

Game Plan

The Fed is hell bent on forcing everyone to speculate, and that is why we have moved into the next stage of the currency war games; the era of negative interest rates. Negative rates will eventually force the most conservative of players to take their money out of the banks and speculate. This process will be akin to another massive stimulus and will provide the bedrock for another monstrous rally.

Make a list of stocks that you would like to own and use strong pullbacks to add to or open new positions in blue chip companies or companies with strong growth rates.

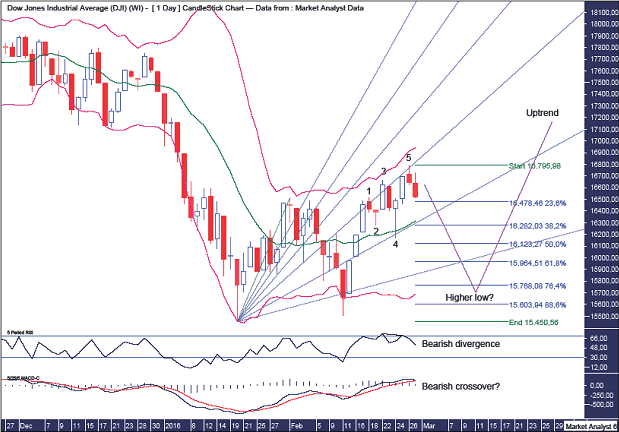

Ahh, the Ides of March. This is a time when stock market participants get the heebie-jeebies and it is my expectation that the first part of the month will play into this superstitious claptrap. However, once an expected higher low is in place, then a big move to the upside will be witnessed that sees March end impressively in the green.

The January analysis outlined the expectation of a move down to put in a higher low. Bingo. The February analysis outlined the expectation of another downside test that puts in another higher low. Bingo again. In this March analysis, I’m gunning for the jackpot prize in calling for one final downside test to put in yet another higher low before price launches higher big time.

Let’s begin the analysis with the daily chart to get an idea of how I believe price is set to trade.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair