Timing & trends

The bulls sure have been on the ropes so far in 2016. In fact, the Dow Jones Industrial Average just suffered its worst start to ANY year since Charles Dow first constructed the index in 1896.

The bulls sure have been on the ropes so far in 2016. In fact, the Dow Jones Industrial Average just suffered its worst start to ANY year since Charles Dow first constructed the index in 1896.

The credit markets? They had their second-worst start to a year ever. The only worse year was 2008, which you probably don’t need me to remind you was a disaster for investors.

It looked like they caught a break overnight when the Chinese market stabilized. Then at 8:30 a.m., the Labor Department released some “hot” jobs figures.

The details:

– The economy added 292,000 jobs in December, well above the average forecast for 200,000. The readings for October and November were also revised higher by a combined 50,000 jobs. That pushed full-year additions to 2.65 million, down from 3.1 million in 2014 but still a solid result.

– By industry, construction added 45,000 jobs, health care added 52,600, and even manufacturing added 8,000 positions. Temporary help jobs rose by 34,000. But mining shed another 8,000 jobs, bringing total 2015 losses to 129,000.

– By industry, construction added 45,000 jobs, health care added 52,600, and even manufacturing added 8,000 positions. Temporary help jobs rose by 34,000. But mining shed another 8,000 jobs, bringing total 2015 losses to 129,000.

– On the flip side, the unemployment rate held at 5% rather than improved further. Wages went nowhere too, with average hourly earnings unchanged from the prior month. The year-over-year rate of improvement (2.5%) missed forecasts by two-tenths of a percentage point.

Dow futures surged to as much as +220 or so after the figures came out. But they started fading shortly thereafter. After attempting a midday bounce, the Dow plunged into the close, finishing down 167 points.

Not only that, but many of the financial stocks I watch suffered huge technical breaks earlier in the week … then

took out yesterday’s lows today. The Russell 2000 Index also sank to yet another 15-month low. And several corners of the credit market continue to behave as if something bad lurks.

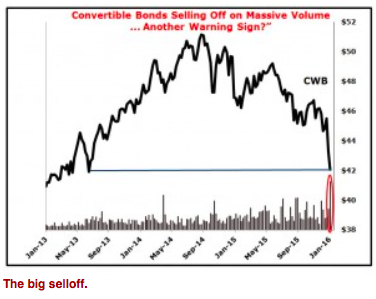

Just look at the SPDR Barclays Convertible Securities ETF (CWB), a benchmark ETF that tracks the convert market. Those are hybrid securities that share some characteristics of both stocks and bonds.

CWB’s top holdings are in sectors like pharmaceuticals, banks, techs and autos, NOT energy. In fact, energy only represents 5% of its portfolio. Yet it’s getting hammered by heavy liquidation. Excluding an anomalous “flash crash” print back in the August market chaos, it hasn’t been this low since June 2013.

So sure, the jobs figures were strong. The auto sales figures we got earlier in the week were, too.

So sure, the jobs figures were strong. The auto sales figures we got earlier in the week were, too.

But the market reaction to those news items suggests a couple of things to me: A) The problems in China, and throughout the emerging markets, are so severe, they offset U.S. domestic economic strength and B) Investors are placing bets that this is “as good as it gets,” and that the economy here will weaken later in 2016.

We won’t know for sure if those judgments are correct until later. But I think they probably are. Indeed, I’ve been worried sick about where markets are headed since last spring — and nothing I’m seeing now tells me that stance is wrong.

Just be sure to buckle up and take protective action. Specifically…

- Carry a higher percentage of cash than you did in 2009-early 2015.

- Hedge or target downside profits with select inverse ETF and option positions (at the right time).

- If you’re going to own stocks, favor non-economically sensitive stocks over growth and industrial names.

- And keep your eye on those sickly financials and the action in the credit markets. They could hold the key to where we go next.

Other Developments of the Day

– Saudi Arabia is out there floating the idea of selling shares in its national oil company, Saudi Aramco. It reportedly may list a percentage of its shares, a portion of its businesses, or otherwise take the company public in a limited fashion.

But it’s hard to see investors stepping up to the plate and buying aggressively given the fact oil prices are at 11-year lows. There’s also a lot of skepticism about Saudi Arabia’s willingness to list on major worldwide exchanges, and provide the detailed financial and reserve data it would have to in that case. Aramco has historically played its cards very close to the vest.

– European authorities believe they found the location where the Paris bombers constructed their deadly explosive devices. Belgian officials say they found materials used to put together the bombers’ suicide belts in a Brussels apartment, and have a man in custody who rented the unit.

– Chinese stocks rallied around 2% overnight after officials refrained from devaluing the yuan currency for one day, and after the government made state-backed funds buy Chinese equities.

But many investors say they’re losing faith in China’s competence, given all the flip-flopping on policy and the belief officials are just throwing things at the wall to see what sticks. Said one emerging market fund manager in a Bloomberg story: “They are changing the rules all the time now … The risks seem to have increased.”

So what do you think? Would you buy into the world’s largest oil company here? Will Europe get a better handle on terrorism in the coming months? Is China finally getting ahead of the market turmoil, or is this just a temporary respite?

Until next time,

Mike Larson

Happy New Year! I hope you had a wonderful holiday with friends and family. And, most of all, here’s to a healthy, wealthy and prosperous 2016!

Happy New Year! I hope you had a wonderful holiday with friends and family. And, most of all, here’s to a healthy, wealthy and prosperous 2016!

Today I’m going to cut right to the chase. My Real Wealth Reportmembers already have my detailed top forecasts for 2016 and naturally, they will get all of my recommendations. Here, I can only give you a sneak peek of what I expect this year.

Mind you, I’m not an alarmist. I simply tell it like it is. How I see things unfolding based on my economic models. How I see the markets developing. So heed my views in this very important first column of the new year.

By doing so, you’ll be better prepared for what’s coming: One heck of a wild and wooly year in the markets, loaded with dangers and profit opportunities.

Let’s get started …

Sneak Peek #1:

Destructive economic winds continue to

steadily pick up, in almost every conceivable way.

Europe’s economy continues to slide, all with worsening sovereign debt-to-GDP ratios … unemployment starting to rise again … industrial production starting to slump again … and deflation worsening almost monthly.

And throughout Europe, currencies are swooning. Not the least of which is the euro, down a whopping 21.3% since its high in May 2014. Also sliding, the Czech koruna, down 6.2% in 2015. Hungary’s forint, down 8.27%. Poland’s zloty, down 9.87%.

Then there’s Russia, with GDP having plunged 4.1%. The Russian ruble has crashed 21.6%.

And just since early October, we have also seen Japan’s economy start to teeter again, with sovereign debts skyrocketing … the economy barely muddling along … and Bank of Japan officials getting ready to print even more yen.

And just since early October, we have also seen Japan’s economy start to teeter again, with sovereign debts skyrocketing … the economy barely muddling along … and Bank of Japan officials getting ready to print even more yen.

Worse will be the increasing geopolitical stress — domestically and internationally — that is now coming true, sadly, in spades. ISIS, Boko Haram, the deadly Paris attacks. And now, Saudi Arabia and Iran, causing global equity markets to plunge on the very first trading day of the new year.

In fact, according to the Institute for Economics & Peace’s recent report on its 2015 Global Terrorism Index — deaths from terrorism increased 80% in 2014 alone to its highest level ever.

Sneak Peek #2:

Another bull run higher for the dollar.

And collapse in the euro.

Yes, someday, most likely by the end of 2020, the dollar will lose its almost singular reserve currency status …

Not because it will crash and burn. But because it will eventually become so strong that it breaks the back of almost every country that has dollar denominated debt — including our own government.

Sure, there will be short-term setbacks for the dollar, but overall, the dollar is headed higher in 2016, possibly much higher.

The forces are easy to see:

- Europe. It’s sure to go even further down the drain in 2016. The European economy will continue to slow, debts will continue to pile up and on top of all that, the Syrian refugee crisis will take its toll on European budgets, not to mention precipitate even more domestic unrest, cultural conflict, and terrorism.

- Moreover, Mario Draghi will be forced to print even more euros and keep interest rates even more negative in the European Union. Meanwhile …

- Economic growth, though modest at best in the U.S., will continue to attract capital inflows into the U.S. dollar.

- Geopolitical tensions and rising terrorism, also will benefit the dollar, as will … surprisingly …

- China’s yuan. Yes, to the surprise of many except for you and those reading my Real Wealth Report and related services … since the International Monetary Fund (IMF) admitted China’s yuan as a reserve currency on Nov. 30, the yuan started plunging, falling as much as 2.4%. So much so that authorities in Beijing are now worried about an outright tsunami of yuan leaving the country.

And they should be. Chinese investors will be among the first to diversify their assets now that the currency is becoming freely convertible. But that’s the part of the story almost no one told you about, unless again, you were one of my subscribers.

Remember, wherever the global economy slows, whenever there are troubled spots in any part of the world, not to mention rising geopolitical conflict and terrorism …

Dollars get bought to either buy assets or pay down debt, and the dollar rallies.

It’s that simple.

Yet despite a stronger dollar …

Sneak Peek #3:

A rolling thunder of commodity bottoms and new bull markets are right around the corner.

I have shown you some of my forecast charts in recent columns. Gold, silver, platinum and palladium have all followed my forecasts to the tee, plunging throughout 2015, reaching new lows for their bear markets nearly right on time in November and December.

But it’s not just precious metals that are bottoming and should soon start awakening in new bull markets.

It’s also oil, natural gas, grain markets, and yes, oil and gas exploration companies and mining shares — where more money will be made in the next few years than any other asset class out there.

The commodity markets are coming together in a way that hasn’t been seen since the middle of the Great Depression …

Where despite deflation and all the problems in the world, commodities — as tangible assets — came roaring back into favor amongst the savvy … rightfully concerned that entire governments would be collapsing.

Stay tuned and stay safe,

Larry

2015 was a year where nearly every asset class failed to provide any returns at all. If fact, the S&P 500 hasn’t gone anywhere in about the past 400 days. An analysis of that Index’s performance at the end of the 3rd quarter by S&P Capital IQ showed that over 250 stocks were down more than 20% from their 2015 highs and 25% of the S&P 500 Index had plummeted more than 30%.

2015 was a year where nearly every asset class failed to provide any returns at all. If fact, the S&P 500 hasn’t gone anywhere in about the past 400 days. An analysis of that Index’s performance at the end of the 3rd quarter by S&P Capital IQ showed that over 250 stocks were down more than 20% from their 2015 highs and 25% of the S&P 500 Index had plummeted more than 30%.

The 30-year Treasury bond has fallen over 2.0%, cash in money market accounts have returned just +0.11% (so after taxes and inflation your return was solidly negative), and the CRB index is down nearly 25%.

So what should investors do with their money when nothing is working? Before I get to that I want to very briefly explain why nothing has worked for so long. The global economy has become debt disabled and market prices have been massively distorted by governments and central banks. The Free market has been eviscerated and supplanted by money printing and deficit spending on an unprecedented scale. The bottom line is that there is now a historic and humongous gap between stock prices and economic fundamentals. And a gigantic gap between fixed income yields in relation to the underlying credit quality.

Evidence of the crumbling economic foundation can be found everywhere you look.

The US manufacturing sector is now clearly in a recession. The latest confirmation of this came from the Dallas Fed survey, which was announced this past Monday, showing a drop of -20.1. Commodity prices, junk bond spreads and money supply growth all indicate the global economy is not only weakening but approaching the Great Recession levels realized in early 2009. After all, investors would have to believe that commodity prices, taken in aggregate, which are trading at prices reached during the nadir of the Great Recession, say nothing about global demand in order to maintain the economy isn’t in serious trouble.

So here are a few of my predictions and trading strategies for next year:

-

The S&P 500 falls more than 20% as it finally succumbs to the incipient global recession

-

Janet Yellen states in the 1st half of 2016 that the Fed will not increase the Fed Funds Rate any further and hints at another round of QE before year’s end.

-

The inability to normalize interest rates is taken as a tacit admission by the Fed that it has utterly failed to save the economy from the Great Recession, and as a result the US Dollar crashes below 90 on the DXY.

-

Gold and the miners will be the major winners next year as they will be the primary beneficiary from continued low nominal interest rates, negative real interest rates and a watershed turn in the value of the USD–the yellow metal reaches a high of $1,250 next year.

-

The Ten-year Note yield falls below 2% by June on pervading recession concerns.

-

Continue to short high-yield debt and own put options on high-flying NASDAQ momentum stocks that are trading at monstrous PE ratios and whose prices should collapse given a deceleration in the US economy.

-

Finally, after the dust settles from this anticipated huge selloff, there will be a tremendous opportunity from owning high-divided paying foreign stocks, which have already been mercilessly beaten down during the commodity bear market of the last few years.

Why will 2016 bring about the long overdue equity bear market? It is not just because the Fed has finally started to raise interest rates and will continue to slowly do so until the US economic recession fully manifests. But also the catalyst for this imminent recession is that debt levels and asset prices have increased to a level that can no longer be supported by incomes and underlying economic growth. Any additional increase in the cost of money will only expedite and exacerbate this condition. Q4 2015 GDP growth is predicted to post a reading that is barely above 1%, according to the Atlanta Fed model. Therefore, we don’t have much room left below before the economy enters contraction mode; and the trend is solidly in that direction.

I cannot stress how important this watershed change in US monetary policy will be for markets in early 2016. The major markets (meaning currencies, bonds and equities) have been anticipating a graceful exit from QE and the trillions of dollars’ worth of deficit spending that have been deployed since 2008. In other words, global capital markets have been banking on the success of central banks. In the vanguard of this belief has been the universal carry trade of going long the US dollar and equities, while shorting precious metals.

I believe in realities not fantasies. I’m betting that you cannot solve the debt crisis evident during the Great Recession by taking on a record amount of debt. And that you cannot fix the asset bubbles evident during the Great Recession by artificially pushing them to record high prices through QE and ZIRP. It is this reality that will take its vengeance in 2016. And it is the unraveling of this delusion that is the basis of Pento Portfolio Strategies’ investment model and is the opportunity we are prepared to profit from.

Ils viennent jusque dans vos bras / They’re coming right into your arms

Égorger vos fils, vos compagnes! / To cut the throats of your sons, your women!

Aux armes, citoyens / To arms, citizens

Formez vos bataillons / Form your battalions

Marchons, marchons! / Let’s march, let’s march!

Qu’un sang impur / Let an impure blood

Abreuve nos sillons! / Soak our fields

– “La Marseillaise”

PARIS – And so the old year ended…

The Closerie des Lilacs brasserie was packed. Every table was taken.

On the corner of the Boulevard de Montparnasse and the Boulevard Saint-Michel, this was one of Hemingway’s favorite restaurants. It is now popular with tourists as well as locals.

Coming in, we heard familiar American accents behind us, but almost everyone else appeared to be native to the city.

It was bright, the way brasseries are supposed to be…

Choppy Waters

“The way things are supposed to be” is our beat at the Diary. The way they really are is beyond us.

Far too complex. Infinitely nuanced. Mind-blowingly intricate.

“Is,” as President Clinton noted, is too high a standard. “Ought to be” is the best we can do.

Only the gods can know what is really going on. All we can do is to observe certain superficial patterns and rules – like waves on the surface of a deep sea – and wonder how they might slap against our little bark.

One observation: Markets bob up and down.

Yes, dear reader, it is a new year… and we face new conditions. New challenges. New threats.

But at least we know how the waves work… floating prices up one side and down the other.

And so let’s begin 2016 by looking at the choppy waters. Where are we? Are we on the upside? Or the downside?

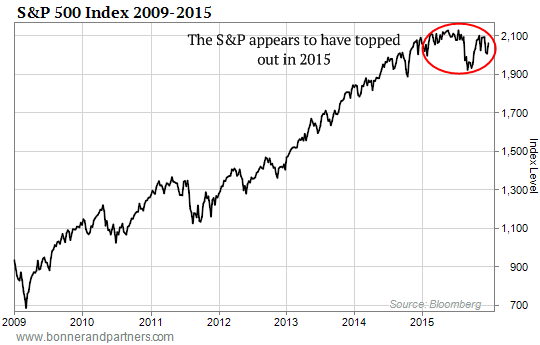

First, we note that both the Dow and S&P 500 ended down for the year in 2015 – the first down year since 2008.

Looking only at the broad indexes, the losses were modest. The Dow fell 2.2% and the S&P 500 fell 0.7%. But only a few stocks did well.

According to Bonner & Partners researcher Nick Rokke, on average, the 10 biggest stocks by market cap in the S&P 500 rose by a little less than 27% in 2015. On average, the bottom 490 were down by about 2%.

Those losses are especially remarkable because it was another near record year of stock buybacks.

Cheap debt financing is a major source of funds for share buybacks. And U.S. corporations rushed to abuse the Fed’s EZ credit while it was still available to them.

Low Expectations

Now, according to the Wall Street Journal, “Investors have low expectations for 2016.”

Why?

MarketWatch reports “earnings season misery.” U.S. corporate earnings dropped 3.5% in the fourth quarter.

That’s one reason.

Another reason is that the chart below of the S&P 500 looks a lot like the wave we described above – with prices rising between 2009 and 2014… and then topping out in 2015.

Meanwhile, the Chinese economy is still slowing… and stocks there are still extremely volatile. (See more below in today’s Market Insight.)

World trade – as indicated by shipping costs as well as import and export figures – is falling.

Railcar and heavy truck orders are at a standstill. Construction equipment sales have collapsed. Capital investment, generally, is depressed. And in dollar terms, the entire world economy is in recession.

And after more than 20 years of excessively easy money… and seven years of the lowest short-term interest rates in history… the Fed has started to raise interest rates.

Remember, this is an economy that lives on credit. The world depends on it. Take it away, and you’ve got trouble. Here’s economist and author Richard Duncan of Macro Watch:

Between 1952 and 2008, every time credit growth (adjusted for inflation) fell below 2%, the U.S. went into recession. During that period, the ratio of total credit to GDP rose from 150% to 380%. In other words, credit growth drove economic growth; and when credit did not grow, neither did the economy.

The feds have offered so much cheap financing that the economy can no longer live without it. Which is why we don’t think the Fed won’t raise rates by much more.

As soon as the economy shows signs of palsy, it will back off. Duncan:

Credit growth looks likely to fall back below the 2% recession threshold next year. If the Fed’s inflation forecasts are correct, then credit growth (adjusted for inflation) could fall to 1.6% [in 2016] and to only 1.0% in 2017.

This makes the economy vulnerable to recession… and stocks vulnerable to a sell-off. That’s the way we think it is supposed to work. Will it actually work that way?

We don’t know…

Getting into the Spirit

So, we return to the scene on New Year’s Eve… to the brasserie, with brass fixtures and rails reflecting the light onto the leather seats and tiled floor.

There was a band of four people. A violinist. A guitarist. An accordionist. And a singer in a tight red dress. They mostly played the French classics, with a special fondness for Edith Piaf.

We were there with four of our children and two of their friends.

“Normally we probably wouldn’t have been able to get a table on such short notice,” said Sophie, one of the friends – a beautiful woman with curly dark hair.

“But Paris is empty. After the terrorist attack last month, tourists canceled their plans to spend the holidays here. Especially Americans. Americans seem to be most worried about terrorism, which is odd, because they have the least to worry about…”

Since attacks by Islamic State on Paris last November, there have been no further incidents. Despite being surrounded by about 2 million Muslims – who tend to live in the suburbs of Paris – the city has, so far, been spared further violence.

“My son is a gendarme,” said a neighbor after the church service last week.

“He is stationed near Paris. On Christmas Eve, he was sent to guard [the cathedral] Notre Dame. They were afraid terrorists would attack during midnight Mass. Can you imagine the huge tragedy that might have happened?

“They had hundreds of policemen there. But all you’d have to do is to make the sound of a gun going off in the cathedral and there could have been panic… with hundreds of people dead in the stampede.”

There must be a million soft targets here in Paris. Anyone could blow up a metro station, a bar, or a church – with a fair chance of getting away. And yet, as far as we can tell, things have gone back to normal… the way they are supposed to be.

“Dix… neuf… huit… sept…” the singer had begun the final countdown of the year.

“Six… cinq…quatre… trois… deux… un… Bonne Année!”

We cheered. We clapped. We rose from our seats and embraced one another.

The band struck up what must have been the French equivalent of “Auld Lang Syne.” We didn’t know it.

But then came the familiar notes of the French national anthem, “La Marseillaise.”

The French are not a patriotic people by American standards. They do not hang out flags. They do not put bumper stickers on their cars telling others how proud they are to be French.

Like thinking people everywhere, they are more often embarrassed by their government than proud of it. And it is practically unheard of to sing the French national anthem in restaurants.

But after the November attacks people seem to be getting in the spirit of it. So, we all sang with gusto… idling through the unknown verses and opening up full throttle for the chorus.

And so 2015 is over… and 2016 begins… just like it is supposed to.

Regards,

Bill

Further Reading: With credit growth set to slow below the crucial 2% level in 2016 and 2017, the major credit collapse Bill has been predicting may not be far off…

So you can be prepared for what’s coming – and so you can protect yourself and your money – Bill has released a critical investor presentation. Watch it here now.

Five Key Questions About The US Dollar: Did the USD make an important double top the 1st week of December 2015? If so, is the USD beginning a “tradable correction?” If so, how deep could it be? If so, what are the best trades to make? If it’s NOT beginning a correction then how much higher can it go and what are the best trades to make?

Comment: For the past few years I’ve maintained that, “It’s all about the US Dollar!” It’s not that the CAD went down…it’s that the USD went up. It’s not that Crude went down…it’s that the USD went up…etc. The USD is the “other side” of so many markets…so the most important thing is to get the USD right!

Question #1: did the USD make an important double top the first week of December 2015? So far the answer is “Yes.”

The market made a new 12 year high (just barely taking out the March high) and then made a classic Weekly Key Reversal (WKR) down…often a signal that a market has made an important trend change. The USD has now remained below its 12 year high for 3 weeks…adding to the significance of the WKR down. However…it’s Christmastime…trading volumes are thin…and technical signals may be less “valid”…so watch what happens when the currency markets come back “full force” the first week of January… a break below the November lows (~9660) would reinforce the “important double top” theory…and point to lower prices.

Question #2: Is the USD beginning a “tradable correction?” Maybe. I believe that the USD bull market began May 2011 and ran for 4 years to March 2015…up ~37%…with most (~80%) of that gain coming in the 11 month period from May 2014 to March 2015. The USD dipped ~7% to the mid-August lows…then rallied back to (barely) make new highs the first week of December.

The long USD trade is described as the most “over-crowded” trade in the market today (CFTC COT data show USD long positions near record highs the first week of December.) Commodities, currencies and especially commodity currencies have sold off hard against the rising USD. The “Weak Loonie” story was “front page news” in the Globe and Mail. Major American corporations regularly cite the strong USD as the reason for poor international revenues. IF…and this is the BIG IF…market psychology begins to believe that the USD bull market has “run its course” then the “over crowdedness” of the Long Dollar trade could cause it to have a swift correction.

Question #3: How deep could the correction be? An obvious target would be the August 2015 lows (~9260)…almost exactly the 38% Fibo retracement of the powerful rally from May 2014 to March 2015.

A deeper target would be the (~8990) highs of 2009/2010 (what was once resistance become support)…almost exactly the 50% Fibo retracement of the May 2014 to March 2015 rally(see above chart)…and almost exactly the 38% Fibo retracement of the full rally from the 2011 low to the 2015 high (see chart below.)

Question #4: If the USD is going to have a correction what are the best trades to make? 1) Keeping it simple…short the USD. 2) Buy those markets that got hit the hardest because of the strong USD…especially those markets that are vulnerable to a “short-covering” rally…for instance…the Euro. 3) Buy commodities. 4) Buy commodity currencies. 5) Buy companies that were hit “extra-hard” because they were leveraged in favour of a weak USD…for instance…shares of resource producing companies (the Teck Resources chart below is an example of the “double wammy” effect of a rising USD and falling commodities.)

Comment: The “long USD trade” is “over-crowded” because there are very powerful reasons to be long the USD (divergent central bank policies…safety and opportunity…the Euro is fundamentally unstable…leads and lags in capital flows…massive unhedged USD borrowings…etc.) but remember when a trade gets “over-crowded” the least little thing can cause a correction.

Question #5: If the USD is NOT going to have a tradable correction how much higher can it go? My principle trading theme over the past few years has been that the USD is in a multi-year bull trend…therefore my current “preferred scenario” is EITHER that the USD has a correction here and then goes on to make new highs…OR…the 3% set back in December WAS the correction…and it breaks out above the 100 level in early 2016 and REALLY picks up speed to the upside as the market “capitulates” to the strong USD idea. If I HAD to “lock up” my personal assets for the next 2 years EITHER 100% long USD or 100% short USD I would choose long. I don’t have to make that choice…but it does illustrate how TIME impacts my decision making.

How much higher can the USD go? I don’t know…but probably much further than we can imagine. (Consider the inverse of this quote from my friend Dennis Gartman, “When a market is going down you have no idea how far down, down is.”) One thing I’ve learned from trading currencies for 40 years is that currency trends go WAY further than seems to make any sense…(and then they “turn on a dime” and go the other way…which is actually further evidence that they went WAY too far in the first place!)

Question #5b: What are the best trades to make if the USD goes higher? 1) Again…to keep it simple…buy the USD. You could simply “swap” your currency for US Dollars. 2) If your base currency is the USD (or if you want to be more aggressive) then look for ways to leverage your position…for instance…buy US Dollar futures (which gives you a long USD position against a basket of other currencies.) 3) Short other currencies and commodities in a manner that fits your risk tolerance. 4) Short stocks and credit instruments that are vulnerable to a rising USD. Realize that whatever you do is a “spread” bet in favour of the USD…for instance…buy a basket of American stocks that generate their income within the USA and sell a basket of American stocks that generate a significant part of their revenues overseas.

Historical perspective: When you look at the chart below you might ask yourself, “Does price action from 20 or 30 years ago have any meaningful impact on today’s prices?” I think it does…especially in the context of “those who do not learn from history are doomed to repeat it!” Depending upon your “preconceived notions” when you look at this chart you might see a market that has been trending lower…on balance…for the past 44 years…OR…you might see a market that has just begun to break out to new highs from a multi-year base building phase.

Bottom line: For my short term trading I REALLY pay attention to market psychology and how it creates “positioning risk.” Right now I believe the market is “over-long” the USD and at risk of a tradable correction. I’ll structure my short term trades with that in mind…but if my trades don’t work I’ll close them out / reverse them quickly because I think the USD is ultimately headed higher.

____________________

DISCLAIMER

Due to the security risks involved in sending information over the Internet, PI Financial Corp. cannot be held responsible for ensuring the confidentiality and integrity of this e-mail message. This message is only intended for the use of the addressee and any other use is strictly unauthorized. Any opinions or recommendations expressed herein do not necessarily reflect those of PI Financial Corp. PI Financial Corp. cannot accept any orders via e-mail as the timely receipt of e-mail messages, or their integrity over the Internet, cannot be guaranteed.

NOTICE REGARDING PRIVACY AND CONFIDENTIALITY PI Financial Corp. and its subsidiaries may, at their discretion, monitor and review the content of all email communications.

PI Financial Corp.| www.pifinancialcorp.com

Vancouver Head Office: 1900-666 Burrard Street, Vancouver, BC V6C 3N1; tel (604) 664-2900

Calgary: 1560-300 5th Avenue SW, Calgary, AB T2P 3C4; tel (403) 543-2900

Regina: 102-2022 Cornwall Street, Regina, SK S4P 2K5; tel (306) 565 4464

Toronto: 40 King Street West, Toronto, ON M5H 3Y4; tel (416) 883 9040

Victoria: 620-880 Douglas Street , Victoria, BC V8W 2B7; tel (250) 405 2900

Winnipeg: 1520-360 Main Street, Winnipeg, MB R3C 3Z3, tel (204) 987 7220

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair