Timing & trends

Many gold market analysts focus on irrelevant, but catchy factors, such as mining production or jewelry demand. Others think gold is a simple inflation or stock market hedge. It is a bit strange that the relationship between the bond and gold markets is not commonly examined, given that bond market is much bigger than stock market, while real interest rates are one of the main drivers of the price of gold. The negative relationship between gold and interest rates imply positive correlations with bond prices, since the price of bonds is negatively related to the yields they offer.

Why should the price of gold rise in tandem with bond prices? Well, think of gold as a substitute for Treasuries, especially when yields are near zero. In such an environment, investors may simply prefer to buy gold rather than bonds (that practically pays zero). Yeah, the precious metals do not yield any income at all, but at least they are not made of paper and U.S. government cannot issue them. Hence, there may be a positive relationship between gold and bonds due to the opportunity costs and capital flow from bonds to gold, when prices of bonds become too high (yields become too low). There may be also capital flows in the opposite direction (from gold to bonds) when bond yields increase (bond prices decrease) and provide a better alternative than gold. This is especially true in the case of U.S. Treasuries. They are considered as a safe-haven – but one which pays a yield. In other words, “fear trade” may increase demand for both gold and bonds. The latter are generally anti-cyclical, while gold is noncyclical, but both asset classes may sometimes move in tandem responding to changes in the stock market, as a non-confidence vote in the U.S. economy (this is why people invested in gold and bonds during the last financial crisis). Moreover, the Fed typically increases the money supply by purchasing government bonds and pushing their prices higher. If such purchases are considered as a signal that the U.S. economy is weak (e.g. as in the case of first quantitative easing), the price of gold may rise simultaneously with bond prices.

There is one problem with this reasoning: the data does not confirm the positive relationship between gold and the bond market. The chart below presents the price of gold and the 10-Year Treasury constant maturity rate (the 10-Year Treasury is considered as a benchmark in the bond market, or at least in the long-term part of it, as it is one of the most widely held fixed income securities in the world). The rates are in reverse order to show the trend in bond prices (which are inversely related to yields).

Chart 1: 10-Year Treasury Constant Maturity Rate (in percent, green line, left scale, values in reverse order) and the price of gold (yellow line, right scale, London P.M. Fixing)

As one can see, the price of gold was rising in the 70s, despite the fact that bond prices were falling and rates were surging. Since the 1980s, there has been a long upward trend in bond prices, seemingly not related to changes in the gold market, as the shiny metal was in a bear market during the 1980s, the 1990s and in the last few years, and in a bull market during the 2000s. This visual analysis is confirmed by more sophisticated research conducted by Baur and Lucey in their academic paper “Is Gold a Hedge or a Safe Haven? An Analysis of Stocks, Bonds and Gold”, where they found that gold is neither a hedge nor a safe haven for bonds.

Why is there no clear relationship between bond prices and the shiny metal? First, high and accelerating inflation rate affects gold and bonds differently. Usually, when inflation was considered a threat, long-term bonds rates rose and their prices fell. Conversely, many investors buy gold to hedge against inflation. This explains the behavior of bonds and gold in the 1970s. The high and accelerating inflation rate hit the bond market and undermined the confidence in the U.S. dollar, whilst gold was boosted.

Investors should remember that what really matters for gold are real interest rates, not nominal yields. The chart below shows a significant positive correlation between the price of 10-year inflation-indexed Treasury and the price of gold, or negative relationship with real interest rates (10-year inflation indexed Treasury rate is a proxy of U.S. long-term real interest rate). The rates in the chart are in reverse order to show the trend in bond prices (which are inversely related to yields).

Chart 2: 10-Year Inflation-Indexed Treasury Rate (in percent, green line, left scale, values in reverse order) and the price of gold (yellow line, right scale, London P.M. Fixing)

Second, the rise in demand for the U.S. bonds from foreigners (e.g. due to the global woes) would increase not only bond prices, but also the U.S. dollar exchange rate. If the greenback gets stronger, the price of gold should decline. This is probably why gold was in a bear market in the 1980s and 1990s, while bond prices were rising. Third, if investors fear that U.S. debts become unsustainable, they will sell bonds and buy gold. Given the probable bubble in the bond market, its burst could lead to declines in bond prices and a rising price of gold. In other words, gold and Treasury bonds are often substitutable safe-haven assets (this is why gold prices move more in tandem with bond prices more than they do with stocks). Except the situations when investors lose faith in the U.S. economy – then gold is superior to Treasuries (like in the 1970s or the 2000s, when the ratio of gold to bond prices significantly increased).

To sum up, as in the case of stocks and gold, there is no simple causal link between bond and gold prices. The sometimes observed positive correlation between bond prices and the shiny metal results from substituting bonds with gold and vice versa due to opportunity costs. Another reason is changes in confidence in the fiat dollar-denominated system, which prompts investors to switch funds from the stock market to gold and bonds. The fact that the yellow metal price is not driven by stocks or bonds confirms the thesis that gold is a good portfolio diversifier, and that it should be considered not as an asset class, but rather as a special non-fiat currency – a non-confidence vote in the U.S. economy.

If you enjoyed the above analysis and would you like to know more about the most important factors influencing the price of gold, we invite you to read the November Market Overview report. If you’re interested in the detailed price analysis and price projections with targets, we invite you to sign up for our Gold & Silver Trading Alerts. If you’re not ready to subscribe at this time, we invite you to sign up for our gold newsletter and stay up-to-date with our latest free articles. It’s free and you can unsubscribe anytime.

Thank you.

Arkadiusz Sieron

Sunshine Profits‘ Gold News Monitor and Market Overview Editor

Gold News Monitor

Gold Trading Alerts

Gold Market Overview

Crude oil has turned up in September when price broke out of a triangle placed in wave (b) so wave (c) was final with wave 4 pullback that reached 50.50 resistance from where sell-off occurred in October. As such, we suspect that WTI made a new swing now that will send price down into wave 5 back to 37.70. Broken corrective channel also suggests more weakness ahead,but after wave (ii) is complete.

Crude OIL, Daily

Crude Oil bounced sharply in the last few days, but so far only with three waves that made a reversal down yesterday from around trend line resistance and 61.8% Fibonacci level. That was ideal zone for a weakness, so ideally crude accomplished rally from 42.64 and that new weakness is now udnerway. If we are correct, then price will break beneath October lows.

Crude OIL, 4H

If you like our trading analysis, you can visit our website at –> www.ew-forecast.com

If you’re like most investors, traders and analysts, then you’re enamored with the strength in the Dow Industrials, the S&P 500, and the Nasdaq and you expect them to simply keep on soaring.

You’d be adding to your stock holdings, chasing hot tips and dreaming of riches.

Yet as always, counting your chickens before they’re hatched is a big mistake. Even more so because all available evidence tells me that U.S. and European stock markets are now a recipe for disaster.

All you have to do is look beyond the illusion of the major indices to see why. Since the August low in global stock markets, the rally that has occurred …

FIRST, has been accompanied by declining volume. When a market rises and volume simultaneously declines, it’s a bearish sign.

SECOND, most stocks traded — both here and in Europe — are actually declining. There are very few leaders pushing the major indices higher. In fact, as I pen this column, here in the U.S. …

Of all publicly traded stocks …

— 44.63% or fully 6,442 are now down at least 10% year-to-date.

— While a whopping 36.9% or 5,204 are down more than 15%.

And only 32.5% are actually up for the year.

Put another way, 77.5% of all publicly traded U.S. stocks are either flat for the year or down more than 10%.

THIRD, of the stocks that are actually advancing, their numbers are also shrinking. Also a very bearish omen.

FOURTH, most other indices are actually down for the year. The Dow Transports are down 10.2%. The Dow Utilities, down 3.5%. The Russell 2000, down 2.5%.

Meanwhile …

FIFTH, total margin buying of U.S. equities — according to latest data (Sept. 30) — stands at a whopping $454 billion, just a tad below record highs.

Given the internally fractured soul of the markets, enumerated above, such massive leverage by investors and institutions is a recipe for disaster. Even the slightest move down can end up causing panic liquidation.

SIXTH, earnings expectations are largely being slashed, the dollar is starting to soar (a negative for corporate earnings going forward) and several other indicators I monitor …

SIXTH, earnings expectations are largely being slashed, the dollar is starting to soar (a negative for corporate earnings going forward) and several other indicators I monitor …

All tell me the stock market is about as risky now as it ever gets.

The thing is, I’m telling you this despite the fact that I am long-term bullish on the market.

I fully expect the Dow Industrials, for instance, to move up to over 31,000 in the years ahead.

But I won’t touch any stocks here now. No way. Because I know how markets work. And if the Dow Industrials is going to move above Dow 31,000 in the years ahead — which it will do …

It will NOT do so unless it first collapses and scares the dickens out of nearly everyone.

Bottom line: In my opinion, no one in their right mind should be heavily invested in stocks right now.

So what should you do then if you are heavily invested?

What about if you aren’t invested?

Here are my answers:

A. If you’re heavily invested, just get out now. If you cannot get out, for whatever reason, consider hedging your holdings with inverse ETFs, such as the Short Dow 30 ETF (DOG), Short S&P 500 ETF (SH), or Short QQQ ETF (PSQ).

B. If you are not invested, then great. But do consider the potential for some rich capital gains by purchasing the above inverse ETFs, or for even more leverage, their equivalent double and triple leveraged inverse ETFs.

It’s that simple.

Now, to another market dear to many: Gold.

Gold’s latest rally has failed, miserably, and as expected. That’s music to my ears. As I have said all along, this month is an important cyclical target for both gold and silver. It should produce a major low.

How low? It’s too early to say. Ideally, gold will soon close below the $1,138 and $1,133 levels. If it does, then gold should slide to a new low this month, below $1,073.

Let’s keep our fingers crossed …

Best wishes,

Larry

Bigger than Apple, Amazon and Priceline Combined

I was so impressed with Jon Markman’s research on the Internet of Things presented here last week, I decided to scan the field myself. And I promptly discovered three things:

I was so impressed with Jon Markman’s research on the Internet of Things presented here last week, I decided to scan the field myself. And I promptly discovered three things:

Number one: He’s right on the money. All over the world, enormous amounts of human resources, brainpower, technology and capital are moving into this new Super-Internet that connects people to devices and devices to each other.

Number two: The estimates he quotes regarding how dramatically the Internet of Things can grow – bigger than the sectors associated with Google, Apple, Facebook, Priceline and Amazon combined — may actually be understated.

And number three: The Internet of Things is not a single industry or sector. Rather, it’s a force that’s already sweeping across nearly all technologies and industries. That includes:

Electric utilities already mass-deploying smart meters that provide detailed data on energy usage, virtually eliminating the need for on-site visits.

Auto insurers setting premiums for commercial and fleet customers through the Internet of Things. Rather than rely on broad indicators like the driver’s age and gender, they’re installing devices in the vehicles to track how many miles drivers have driven, where they go and how safely they drive.

Train manufacturers outfitting trains with systems that can predict and prevent accidents.

Construction and mining industries rushing to equip hard-hat workers with wearable devices that scan the environment to signal when they’re in danger.

Security companies connecting video cameras, alarms, door locks, motion sensors and tracking devices all into one integrated network.

At least 14 car manufacturers, accounting for 80 percent of the worldwide auto market, deploying strategies for transforming their cars into Internet-of-Things devices.

And much more.

Moreover, none of this is speculation. It’s all starting here and now. In fact, at just one company (Verizon), last year’s growth in this field was 83% for their customers in transportation and distribution, 88% in retail and hospitality, 89% in home monitoring, 120% in media, 128% in finance, and a whopping 204% in the manufacturing industry.

The key question: How to profit?

I feel the best person to provide the answer is Jon Markman himself.

For decades, Jon has forecast and reported on nearly every major technology trend, including the rise of the PC, the popularity of the iPod, the mobile expansion of the Internet, and the dominance of the cloud.

Jon was the founding managing editor of MSN Money. He helped develop the first online stock screening system. And he earned shares of two patents at Microsoft for his contributions to the development of portfolio management systems.

Here are his answers …

How investors can get richer

as everyday objects get smarter.

by Jon Markman

Usually I’m happy if I find one or two great investments in a new sector of the economy, especially one with such rapid growth potential.

But it’s rare that I see so many investing opportunities that I can construct an entire investing portfolio from just one disruptive technology! That’s the situation we have now with the Internet of Things.

Moreover, the wide array of choices makes it easier for me to cherry-pick the ones offering the highest returns with the lowest risk.

That’s because the applications for the Internet of Things are virtually limitless. It’s because industry experts, companies, and research firms are throwing trillion-dollar market estimates around like they’re chump change.

- Recently, GE estimated the Internet of Things could add an additional $10 trillion to $15 trillion to global GDP over the next two decades.

- Networking equipment giant Cisco estimates the Internet of Things could add $19 trillion to the worldwide economy by 2020.

- And that’s on top of the already $1.9 trillion global market for the Internet of Things in 2013.

The estimates may vary, but one thing is abundantly clear: We are entering a decade of immense technological change. And history has shown that any technology that can disrupt the world so thoroughly can also make investors so incredibly wealthy.

Consider smart phones. It was only eight years ago that Apple launched the iPhone.

I will never forget flying into the Dallas airport in 2008 about a year later. I looked around and couldn’t believe that almost everyone I saw was already using one.

But I also realized this transformation was not yet reflected in Apple’s stock price. Most investors had no idea how massive the transformation really was.

If you had understood the power of the smart phone technology, you could have watched your wealth skyrocket 579.5% following the iPhone launch. Every $10,000 invested in Apple at that time is now worth $67,950 today.

Just last year alone, over 1.2 billion smartphones were sold, for a total global market of $300 billion. And that’s just a drop in the bucket compared to the coming $19 trillion Internet of Things Shockwave.

If you thought Amazon was just a

bookstore, you missed out on 9,362% gains.

Today we assume that we can find, buy, and ship just about anything to anywhere over the Internet.

But we often forget that this is actually a very recent phenomenon: Back in 2001, most people still thought of Amazon.com as just a bookstore. What most investors didn’t grasp was that it wasn’t about books at all, or at least not only about books.

Amazon wanted to transform the way that Americans bought everything.

The problem was most investors were too terrified to buy into Jeff Bezos’ vision — especially smack in the middle of the 2001 tech bear market.

But if you had understood the massive upheaval Amazon was creating in the retail market and jumped on the stock, you could have racked up a fortune-making 9,362% return.

Think about it: A modest $10,000 investment in Amazon in 2003 would be worth $946,200 today — and that’s in spite of another big bear market in 2008.

This summer, Amazon officially became the biggest retailer in the world — with a market cap of over $246 billion, surpassing Wal-Mart’s $230 billion.

And even at $246 billion, Amazon’s success is just a fraction of the total $19 trillion potential for the Internet of Things.

If you didn’t realize that most travel agents were headed the way of the dodo bird, you missed out on 19,034% gains.

Consider Priceline.com. Yes, it was the poster-child for the dot.com bust. And yes, it crashed in value in the two years after its IPO.

But despite that crash, Priceline continued to ride a massive wave of change in the travel industry.

Seriously, who even uses a travel agent anymore? You just jump on line and bargain shop for the best deals on hotels, airlines, rental cars, and more.

It may seem obvious now, but very few people saw the transformation in the travel industry coming back in 2000. Priceline did. And they not only survived, they thrived after the bust.

If you had the chutzpah and the foresight to invest in Priceline at that time, you could have banked an incredible 19,034% gain over the past fifteen years. Every $10,000 invested turned into $1.9 million.

Here’s the key: The technology stocks tied to the Internet of Things are riding a major wave of innovation greater than Amazon’s, Apple’s and Priceline’s combined.

Priceline generated a whopping $8.44 billion in revenues in 2014.

But according to Cisco, the Internet of Things will generate over two thousand times that much.

It’s not about building a better mouse trap.

It’s about building a better world.

So I repeat: If you missed investing in Intel, Microsoft, Apple, Priceline, Google and others in the past years, that’s okay.

Because you have one more chance in your life to ride a technology shockwave from its infancy all the way to maturity.

In fact, it may be the final opportunity you have in your life to grow a family fortune, to secure a comfortable retirement and to leave a sizeable inheritance to your children and grandchildren.

The Internet of things is automation on steroids.

There are already over 12 billion smart devices interconnected with each other and the Internet right now.

I’m not just talking about iPhones and computers. I’m talking about things like traffic monitors, roadways, pacemakers, manufacturing equipment, street lights and much more.

Estimates are for 50 billion more”things” or devices to be connected by 2020. But I think that estimate is low.

Why so much, so fast?

Here’s why: Right now, there are three major tipping points catapulting the Internet of Things to a global scale not seen since the dawn of the industrial revolution.

Tipping Point #1

Rapidly Declining Costs

For any new technological revolution to succeed, production costs must drop, allowing mass commercialization to emerge. This is true for the Internet of Things as well.

Fortunately, sensor prices have already dropped more than half from $1.30 to 60 cents. And I expect to see continued drops — by half and half again — in the coming years. In fact, I wouldn’t be surprised to see sensors ultimately fall to less than a penny each, propelling a massive surge in usage.

Meanwhile, we’ve already seen processing costs decline nearly 60 times over the past decade. And we’ve seen far cheaper bandwidth and networking costs – down by a factor of nearly 40 times in just 10 years.

Tipping Point #2

Virtually Unlimited Wi-Fi

Stop by your local coffee shop. Chances are it offers wireless Internet access.

You think nothing of it. It’s the way things are, right?

Now? Yes. Just a few years ago? No way! It used to cost you a pretty penny to hook up to the Internet.

Then came Starbucks. In 2010, they began offering free unlimited Wi-Fi to customers. Other merchants quickly followed suit. Airports soon joined the bandwagon. Now, even entire cities offer free Wi-Fi.

Tipping Point #3

Advanced Network Connections

Today, network connections are faster, smarter and more automatic.

They connect nearly everyone and everything to the cloud.

And most important, the cloud is everywhere.

So now, mankind can expand the Internet of Things into nearly every nook and cranny of our lives.

Now, thanks to these three powerful triggers, you’re going to see an explosion of new applications for smart cars, smart homes, smart businesses and smart cities.

And that means an explosion of new profit opportunities for investors in the know.

Jon Markman

To get Jon Markman’s to 5 Investments in this area Click HERE

Originally published October 31st, 2015.

It was ironic that when Dr Watson complained to his companion Sherlock Homes that he had a stomach ache, Holmes clarified the situation at once by saying “Alimentary, my dear Watson”. More generally, the legendary sleuth of Victorian London would make light of his accomplishments after solving cases that baffled the police, by remarking “Elementary, my dear Watson”. Doubtless this expression was deeply irritating to his arch-enemy Moriarty.

Today we are going make light of what to other analysts may be abstruse and possibly baffling, by “joining the dots” to demonstrate the linear connection between an extremely bearish silver COT and an imminent crashing euro, so that by the conclusion of this article, you, dear reader, will have a clear understanding of what is set to unfold, and will be able to explain to other confused souls that it really is elementary.

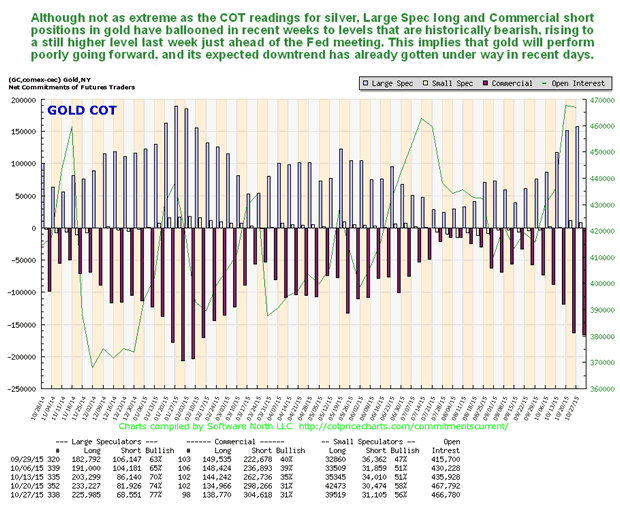

We will start by looking immediately at our most important piece of evidence, the latest silver COT, which is very bearish indeed, because the Commercials now have their biggest short position since 2008. This makes a big drop in silver very likely soon, and it is expected to make new lows, probably heading to the $10 area. Doubt that this is true? – then look at what happened to silver over the past year on its 1-year chart placed directly below the COT chart, when the Commercials had a high short position – I rest my case.

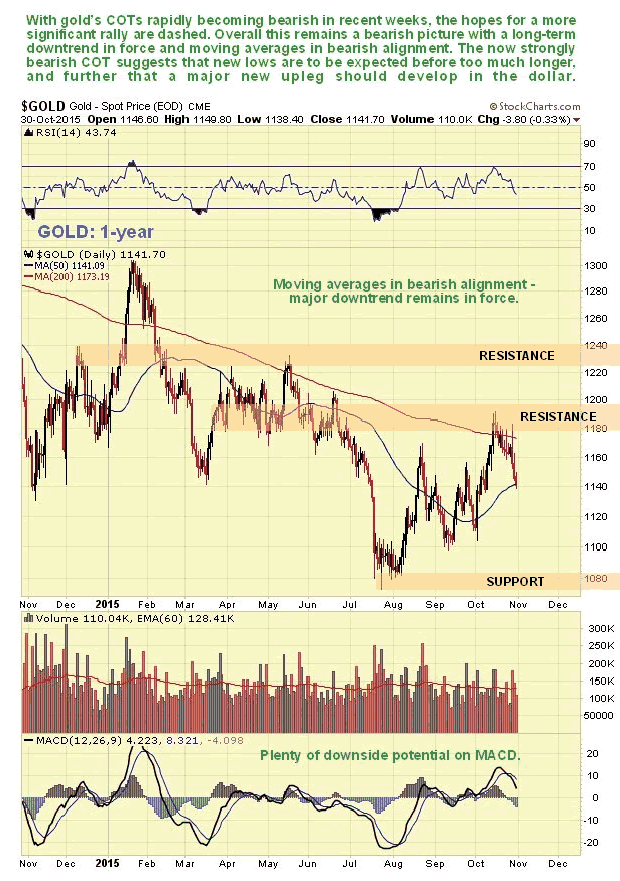

Next we look at gold’s latest COT, with its 1-year chart placed directly below for comparison. It’s similar, although not so extreme as silver, but the conclusion is the same.

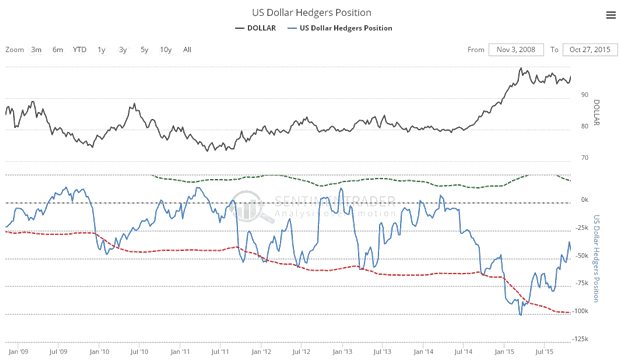

So, gold and silver are going to drop a lot – what does that mean for the dollar? – it means the dollar is going to rally, and rally a lot, and on its 3-year chart we can see that it is in position to do just that. Following its dramatic rally from July of last year to March of this year, the dollar index has been stuck in a large triangular trading range, which could be either a consolidation pattern or a top. It has already started to break out upside from this pattern on the Fed meeting this past week, and it wouldn’t take much to swing its moving averages into bullish alignment. If it succeeds in breaking out upside from this pattern and following through, it is likely to mount an advance of similar magnitude to the one preceding the consolidation pattern, which means it will target the 114 – 116 area, a big move indeed.

COTs for the US dollar are in middling ground, but have certainly eased enough to permit a big advance, as shown by the latest Hedgers chart, which is a form of COT chart…

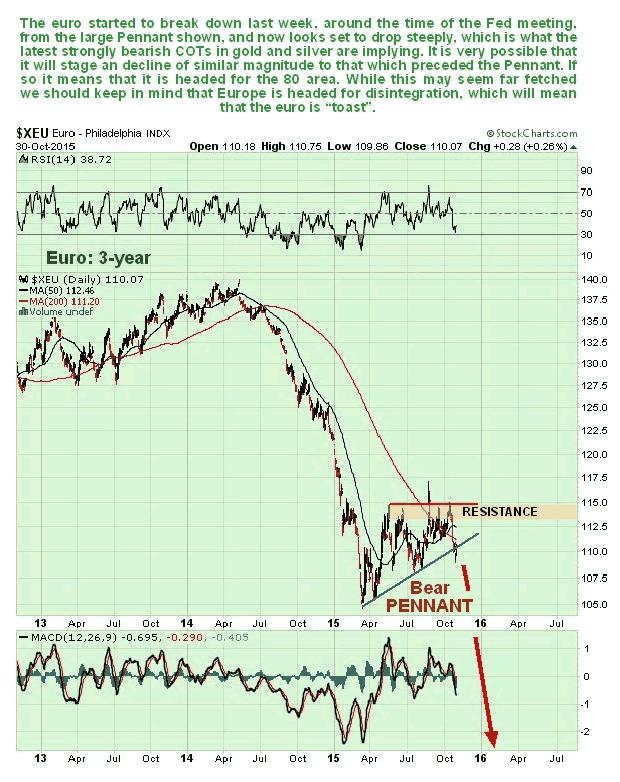

If the Fed starts an interest rate rise cycle, it would of course bolster the dollar, but as we know there is precious little scope for them to do so without triggering an economic cataclysm, because of the frightening levels of debt that now exist. So what else could cause the dollar index to rise? the euro, that’s what. Don’t forget that the dollar index is some 57% composed of the euro, and with Europe threatening to fall to bits, crippled as it is by ruinous debts and with political differences between member states being aggravated by differences over how to handle the massive influx of migrants, the euro is really on the ropes and looks like it is starting another major downleg on its road to eventual oblivion. With regards to the migrant crisis, Europe is reaping what it has sown, by joining forces as an obsequious sidekick with the US in its destabilizing rampage around the Mid-East. It’s alright for the US, the migrant’s rubber boats can’t make it across the Atlantic, but they sure can make the 20 km crossing from Bodrum to Kos.

Let’s look at the latest euro chart now. As we just saw, the dollar index is starting to break out upside to start another major upleg, so we can expect to see the opposite occurring in the euro, a major downleg just starting, and that is exactly what we do see. With Europe blighted by huge debts, Germany weakening rapidly as its export markets shrink, its reputation tarnished by the VW scandal, and beset by hordes of immigrants with their hands out so that it looks set to fall to the ground, a constitutional crisis looms for the EU, especially if Britain votes to leave, and the euro is threatened with extinction, so it is not hard to see why the next downleg in the euro could easily be as bad as the one from the Summer of 2014 through the Spring of this year, and if it is, we are looking at the euro dropping to 80 or lower.

If the euro fell this far it means that we will see another huge ramp in the dollar index, which would be expected to trigger a big drop in both gold and silver to new lows. Now you should be able to grasp why the Commercials are piling on the gold and silver shorts – it’s elementary, my dear reader.

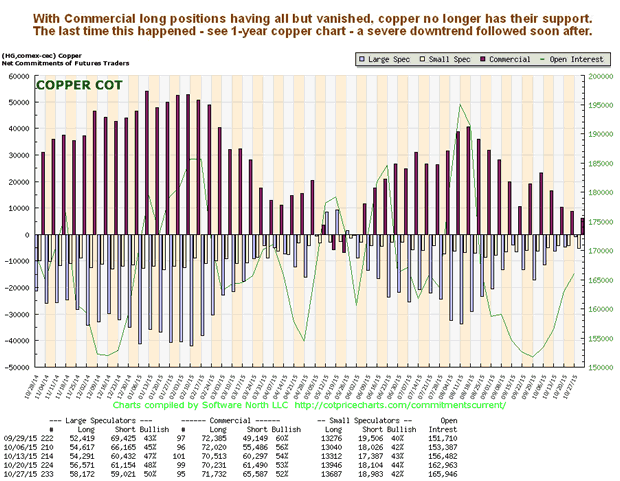

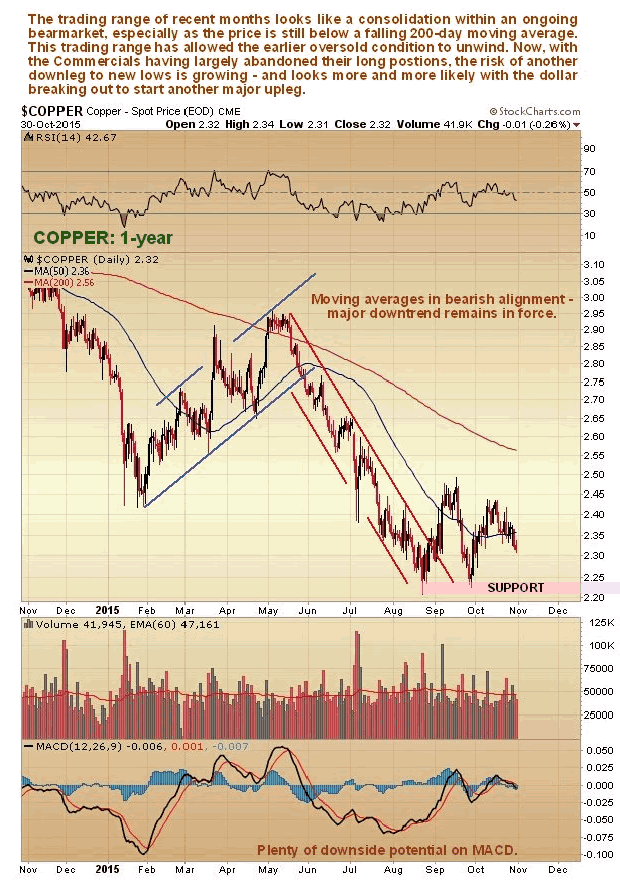

If a big ramp in the dollar ensues it is logical to suppose that many other commodities, apart from gold and silver, will get whacked down again. So let’s take a look at copper and its COT as we would expect this to get hit too. As we can see on the latest COT chart, the Commercials have been “jumping ship” in recent weeks, scaling down their long positions to a very low level. The last time this happened, back in May, a severe downtrend followed as we can see on copper’s 1-year chart, shown directly below the COT chart.

On clivemaund.com we are not going to stand around staring blankly as gold and silver drop away to new lows. This is an opportunity to make big gains on the short side in the PM sector, and we will be looking at a range of vehicles which we can use to do just that, some of which we have already bought over the last week or two.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair