Timing & trends

Of course, this has huge implications for every part of the Internet food chain.

- Social media connectors: Facebook, Twitter, LinkedIn

- Content providers: Yahoo, Netflix, Google

- Smartphone manufacturers: Apple, Samsung

- E-tailers: Priceline, eBay, Amazon

- Infrastructure: Cisco, Juniper Networks

And don’t forget about the Chinese Internet giants either, like Tencent Holdings Ltd. (TCEHY), Baidu, Inc. (BIDU), Rakuten, Inc. (RKUNY), NetEase, Inc. (NTES), Sina Corporation (SINA), Alibaba Group Holding Ltd. (BABA), Weibo Corporation (WB), Ctrip.com International Ltd. (CTRP), and Sohu.com, Inc. (SOHU).

Prediction: I bet the above Chinese stocks will deliver TWICE the gains you can make on the above-listed American Internet kings.

….read entire article HERE

In a reminder that the world doesn’t revolve around Federal Reserve dot plots or the machination of Greek bailout negotiations in Brussels, there has been a surge of merger news as companies quietly go on doing the good work of capitalism: Expanding, buying, selling, and trying everything possible to boost profits and maximize shareholder wealth.

Homebuilders Standard Pacific (SPF) and Ryland (RYL) last week agreed to a $5.2 billion marriage to create the country’s fourth-largest company in its industry. RYL builds homes targeted to entry-level buyers as well as first- and second-time move-up buyers. SPF is more focused on move-up buyers in metropolitan areas in California, Florida, the Carolinas, Texas, Arizona and Colorado. Geographic and product diversification were given as the justification for the tie up.

This is a sign of confidence in the health of the housing market, something that was corroborated by an increase in homebuilder sentiment to the best level since September.

Next up, Dealertrack (TRAK) agreed to be acquired by Cox Automotive for $4 billion. TRAK is a leading provider of software and services for car dealerships while Cox operates Kelley Blue Book and Autotrader among its businesses. With auto sales running at the best pace in 10 years, this is also a sign of confidence in the industry.

In the retail space, Target (TGT) sold its pharmacy and clinics business — with more than 1,660 pharmacies and 80 clinics — to CVS Health (CVS) for $1.9 billion. The deal benefits both as CVS is suddenly free of the specter of developing a large number of new pharmacies while the cash will be immediately accretive to TGT’s bottom line.

Merger activity is also red-hot in the managed care arena with Cigna (CI) reportedly turning down a $175 a share offer from Anthem (ANTM). UnitedHealth (UNH) reportedly has an interest in both Cigna and Aetna (AET). And both Anthem and Aetna are reportedly considering bid offers for Humana (HUM).

All this goes to show that even if investors are frightened by the prospect of the start of higher interest rates or a Greek debt

default, corporate cash balances will remain a strong supporter of stock market valuations for the foreseeable future. CFOs are in a shopping mood, both in buybacks of their own stocks, and now their rivals’ stocks.

You can see this in the chart above from FactSet research showing the swelling average price-to-earnings multiple of M&A deals. At present the health care and tech industries are the main beneficiaries, but in the future I would expect to see much more in other areas, such as tech and regional banks.

* *

Thinking About Value

Let’s say that we can all agree — yes, I’m voting on your behalf — that once this whole Greek thing is put to bed people will look around and realize that euro-zone stocks are too cheap. Doesn’t it make sense to start considering right here, right now, which ones or which countries should rebound best?

When you think about it, once the Greek thing blows over, the euro zone will still be pumping money into the Continent via quantitative easing. As the ECB grows its balance sheet, euro-zone stocks should wake up and benefit.

This line of thinking, sparked by comments by TIS Group analysts, got me musing about the whole concept of value. The U.S. is up 210% from its lows of 2009, but Europe and India are only up 75%, Japan is up 125% and China is up around 145%. Brazil, a very nice country with beautiful beaches and stunning commodity riches, has fared much worse, as are most other emerging markets.

Areas of the market that are cheap are also the most hated and the least respected. That’s how they got cheap. Expectations are low. If I say that now is the time to add iShares Brazil (EWZ), I’m sure you would give me a big eye roll. The idea that it might turn around seems ludicrous as “everyone knows” that corruption, an over-reliance on energy and agricultural commodities, and an anti-capital government will forever keep the country down. Expectations are low, in other words.

On the opposite side of the spectrum are ideas that most investors agree are fair and true. A few are: Central banks always get their way, so QE will always work; interest rates will be low for years; biotech has entered a new era of long-term strength without bounds; and mergers always create value.

The chart above shows how a love for Brazil and abhorrence for biotech dominated the nine years from 2002 to 2011. More recently the tables have completely reversed. Will the new love of biotech and hatred for Brazil persist, or could it reverse when no one is looking? Something to ponder.

Best wishes,

Jon Markman

Despite the greatest government rescue operations of all time, the U.S. economic recovery has been one of the weakest in history. Most Americans continue to suffer through tough times. And new dangers loom.

Despite the greatest government rescue operations of all time, the U.S. economic recovery has been one of the weakest in history. Most Americans continue to suffer through tough times. And new dangers loom.

Indeed, the pattern of the past 15 years is now clear: First a great speculative bubble … then a great bust … followed by massive government stimulus, bailouts and money printing … and then … still another, even greater bubble.

Invariably, when the dust settles from each bubble-and-bust cycle, some people make fortunes. But millions of average hard-working people lose their jobs, sink deeper into debt, and even risk abject poverty.

Right now, a series of time bombs, planted years ago, are beginning to explode all over the world

Fourteen years minus three months ago, a small group of terrorists attacked the very heart of our nation. They killed almost 3,000 people. They caused at least $10 billion in damage.

They set off a tragic chain of events that have continued to ricochet through time, with a tremendous cost in life — and treasure: The U.S. invasion of Iraq. The fall of Saddam Hussein. The emergence of al Qaeda in Iraq. And now, the rise of the Islamic State, the most brutal, most powerful terrorist organization of all time.

This chain of events has greatly weakened our nation’s leadership in the world. It has propelled our government to spy on us. And it has now brought us around full circle to the danger of larger terrorist attacks than 9-11.

At the same time, in parallel to the global war on terror, we’ve also had a global war on financial crises.

Fifteen years and six months ago, well before al-Qaeda’s first attacks on America, our tech stocks began to crumble, only to crash even further after 9-11.

Over $5 trillion in equity value was wiped out. Our entire economy was temporarily paralyzed. And that crisis also set off a tragic chain of economic events that continue to ricochet through time: Radical interest-rate cuts by Fed Chairman Greenspan.

A great housing bubble — and bust. The implosion of major Wall Street firms. The emergence of a deadly debt crisis. And the most risky and largest Fed money-printing operation of all time, under Fed Chairmen Bernanke and Yellen, pumping $4 trillion into the U.S. banking system.

This chain of events has been a big factor in the recovery of the American economy. But it has also propelled many investors to take unprecedented risks. And it’s likely to bring us around full circle to the brink of another, potentially bigger, financial crisis.

The global war on terror. The global war on financial crisis. Two parallel and powerful historical sequences that are gaining momentum and reaching a crescendo.

The global war on terror. The global war on financial crisis. Two parallel and powerful historical sequences that are gaining momentum and reaching a crescendo.

But they are only two of the global crises now smoldering and spreading globally. So let me show you some maps that tell the story in a nutshell.

Here are all the countries of the world today where the Islamic State has conquered territory, has mounted massive brutal attacks on the local population or has successfully enlisted affiliate organizations that conquer and attack — much of the Middle East, North Africa and Asia. And that’s just the Islamic State.

These are the countries involved in some kind of civil or international wars. Look at how the red has virtually taken over the globe.

And while we’re talking about red ink, here are the countries burdened with heavy debts and big deficits, many of which they will never be able to pay. That includes all of North America, most of Europe, plus the two most populous countries of the world — China and Japan.

All this sounds very bad, doesn’t it?

Well, it is. But there’s also a silver lining, especially for the United States. Of all the countries on all these maps, the only one that combines a powerful military, a stable government, a huge economy and, most important, giant liquid financial markets is the United States.

Despite America’s big debts, government gridlock, and past stumbles, it is now viewed as the last remaining large safe haven on the planet.

As a result, the geopolitical and financial troubles overseas are driving huge amounts of money into U.S. markets. In fact, based on data from the IMF and OECD, total foreign ownership of U.S. assets rose from $16.6 trillion in 2009 to nearly $27 trillion in 2014. That’s a total of $10 trillion that has flowed into U.S. investments from abroad.

As a result, the geopolitical and financial troubles overseas are driving huge amounts of money into U.S. markets. In fact, based on data from the IMF and OECD, total foreign ownership of U.S. assets rose from $16.6 trillion in 2009 to nearly $27 trillion in 2014. That’s a total of $10 trillion that has flowed into U.S. investments from abroad.

Again, remember the great sequence of events of our times:

Extreme easy money in the 1990s, leading to a tech bubble and the Great Tech Wreck …

Even more extreme easy money in the early 2000s, leading to the housing bubble and the Great Debt Crisis …

And now, the most extreme easy money of all time, leading to an unprecedented bubble in bond markets and government debt, the subject of my column next week.

Good luck and God bless!

Martin

1. Stratfor Has 11 Chilling Predictions For What the World Will Look Like a Decade From Now

1. Stratfor Has 11 Chilling Predictions For What the World Will Look Like a Decade From Now

2. War Cycles Will Affect Everything!

by Larry Edelson

“Not since the mid- and late-1800s have so many different war cycles converged together at the same time.”

3. The Skeptical Investor – June 2015

Here are today’s videos and charts (double click to enlarge):

Gold Blastoff Video Analysis (& US Dollar Sell Signal Chart)

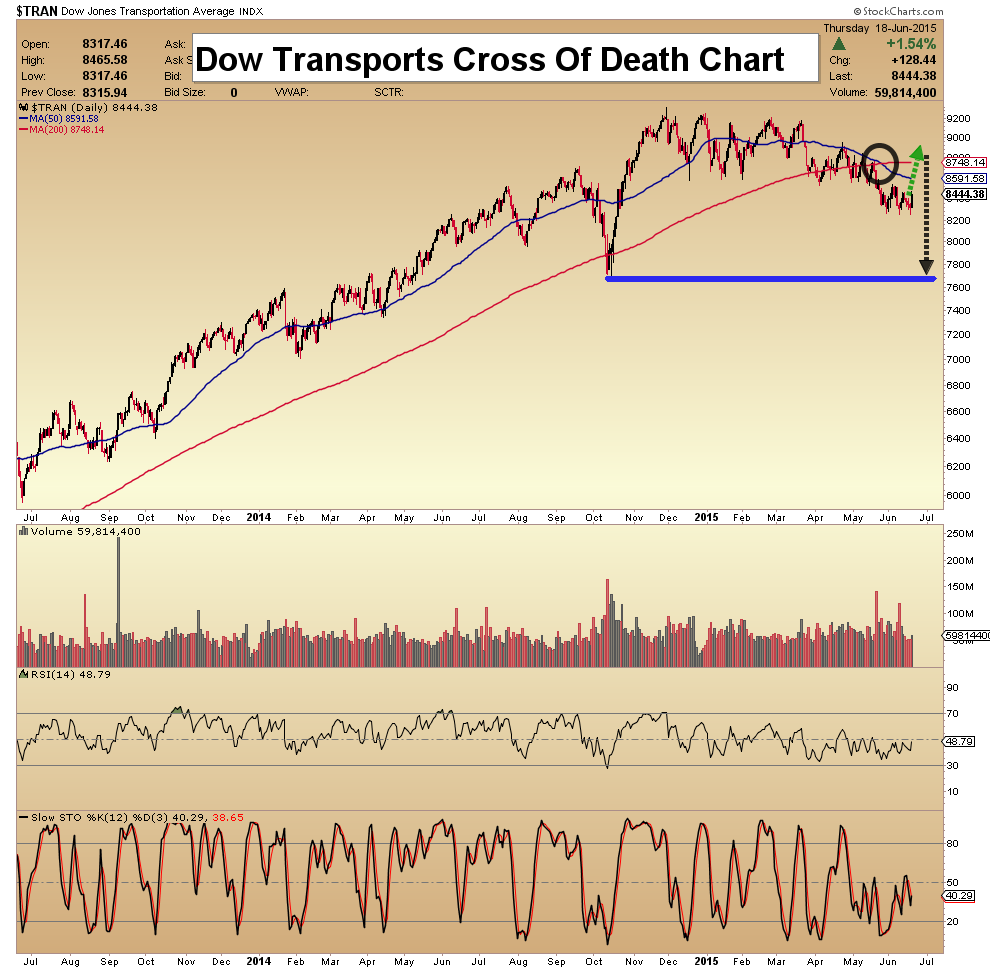

Dow Industrials & Dow Transports Video Analysis

GDX, GDXJ, & SIL Blastoff Video Analysis

{kind=link}

Gold & Silver Stocks Blastoff Video Analysis

Here is a further look at some junior precious metal sector stocks that are showing some important price and volume action:

More Great Junior Gold & Silver Stocks Video Analysis

Thanks,

Morris

Friday, Jun 19, 2015 Super Force Signals special offer for Money Talks Readers:

Send an email to trading@superforcesignals.com and I’ll send you 3 of my next Super Force Surge Signals free of charge, as I send them to paid subscribers. Thank you!

The SuperForce Proprietary SURGE index SIGNALS:

25 Surge Index Buy or 25 Surge Index Sell: Solid Power.

50 Surge Index Buy or 50 Surge Index Sell: Stronger Power.

75 Surge Index Buy or 75 Surge Index Sell: Maximum Power.

100 Surge Index Buy or 100 Surge Index Sell: “Over The Top” Power.

Stay alert for our surge signals, sent by email to subscribers, for both the daily charts on Super Force Signals at www.superforcesignals.com and for the 60 minute charts at www.superforce60.com

About Super Force Signals:

Our Surge Index Signals are created thru our proprietary blend of the highest quality technical analysis and many years of successful business building. We are two business owners with excellent synergy. We understand risk and reward. Our subscribers are generally successfully business owners, people like yourself with speculative funds, looking for serious management of your risk and reward in the market.

Frank Johnson: Executive Editor, Macro Risk Manager.

Morris Hubbartt: Chief Market Analyst, Trading Risk Specialist.

website: www.superforcesignals.com

email: trading@superforcesignals.com

email: trading@superforce60.com

SFS Web Services

1170 Bay Street, Suite #143

Toronto, Ontario, M5S 2B4

Canada

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair