Timing & trends

“Signs of Fear are Starting to Show” –

Week after week, the news is filled with reports of law-breaking by institutions and individuals that hold positions of trust in society. Last week, FIFA, the body that rules the multi-billion dollar business of soccer, was hit by indictments of many of its senior officials who were charged with running a multi-year corruption scheme.

The week ended with former Speaker of the House of Representatives, Dennis Hastert – who for 8 years was the second in line to the presidency – being indicted for violating banking laws in connection with a scheme to pay hush money to a man with whom he had an illicit sexual relationship thirty years ago.

A week ago, several of the largest banks in the world agreed to pay $5.6 billion to settle charges that they manipulated foreign exchange rates. All of these institutions were serial offenders who had previously admitted to committing other serious financial crimes.

On top of it all, the U.S. presidential campaign is being conducted under the cloud of allegations that the presumptive Democratic nominee, Hillary Clinton, used her family’s charitable foundation to solicit huge donations from foreign businesses and countries. And there are serious questions emerging about her tenure as Secretary of State and her independence from foreign influence were she to enter the White House.

There is something profoundly wrong with a world where those entrusted with power are consistently found to be corrupt. But it is even more disturbing that this corruption is treated as “business as usual” in the media and the markets.

Apathy Creates Stagnation

In a world now home to more than $200 trillion of debt, which has no hope of ever being repaid, there is a desperate need for leaders with character, intelligence and courage to forge solutions to intractable economic challenges. This need is compounded by a seriously deteriorating geopolitical situation abroad and rising violence on the streets of America.

Yet Americans are exhibiting a high degree of complacency about the world around them. This mass delusion comes at precisely the time when they should be crying out for radical change in their leaders and the policies that are bringing the world to its knees.

Financial markets continue to inhabit a universe dictated by the reckless and misguided policies of central banks who continue to print money like drunken sailors. Here in the U.S., the Federal Reserve continues to dither over raising interest rates after keeping them at zero for eight years and refuses to recognize that these low rates are themselves suppressing growth.

In Europe, Japan and China, central banks are printing trillions of dollars’ worth of money to stimulate economies that already have too much debt. Meanwhile, what doesn’t happen are much needed, pro-growth tax, labor and regulatory reforms.

Rather than acknowledge the fundamental reality, stock market investors only see free money. Stock prices are driven higher, and there is no thought given to the fact that these high share prices are being levitated by nothing more than funny money.

When You Can’t Grow, You Merge and Acquire

One of the key indicators of an overvalued market is a boom in M&A. Last week was typical of what we have seen thus far in 2015, as a number of large and expensive mergers were announced. Charter Communications (Nasdaq: CHTR) agreed to buy Time-Warner Cable (NYSE: TWC) in a $79 billion deal – a much higher price than it offered to pay a couple of years ago -while Avago Technologies (Nasdaq: AVGO) agreed to buy Broadcom (Nasdaq: BRCM) in a $37 billion deal that valued BRCM at 19x cash flow. Late in the week, healthcare giant Humana (NYSE: HUM) was reported to have put itself up for sale.

Some believe that M&A is an indication of optimism on the part of corporate executives, but it usually signals that companies are running out of organic growth and are looking outside for new sources of growth. These deals inevitably lead to large layoffs and other cost cuts that are negative for economic growth.

Most deals fail to generate the synergies they promise; instead they line the pockets of corporate executives and shareholders. I would not be surprised to see the stock prices of the surviving companies much lower a year or two from now.

Signs of Fear are Starting to Show

Last week stocks took a breather after first quarter GDP was revised lower to a -0.7%. The Dow Jones Industrial Average lost 221 points or 1.2% to close at 18,010.68 while the S&P 500 fell 19 points or 0.9% to end the week at 2107.39. The Nasdaq Composite Index fell by 19 points or 0.4% to 5070.03.

The Dow Transportation Average fell 2.2%, which is considered a bad omen by those who adhere to Dow Theory, which holds that the Transports hold the key to the direction of the market. A faltering economy, which the GDP numbers point to, indicates that America’s economic engine is sputtering. While there is an active debate about whether first quarter GDP was as weak as the -0.7% number indicates, it appears indisputable that first half growth is going to be disappointing.

The Atlanta Fed’s real-time tracking of second quarter GDP is still showing growth at under 1%, so something is clearly dragging on the U.S. economy – most likely the ever-rising mountain of debt at every level of the economy, rising healthcare costs, and the inexorable weight of regulation burying businesses in needless paperwork.

But there is something else holding back the economy… The world has become a dangerous and uncertain place. Headlines matter and the headlines are ugly. Markets are driven by psychology. Complacency is still running high but it can shift on a dime. Nobody knows when it will reach a tipping point but there is enough bad news out there to cause such a shift. Investors should pay attention to potential sell-off triggers and, as always, proceed with caution.

I am going to take a little detour this weekend from the usual macroeconomic/market analysis to dispel a few “Wall Street” myths about long-term investing.

1) The Market Has Generated 10% Annual Returns

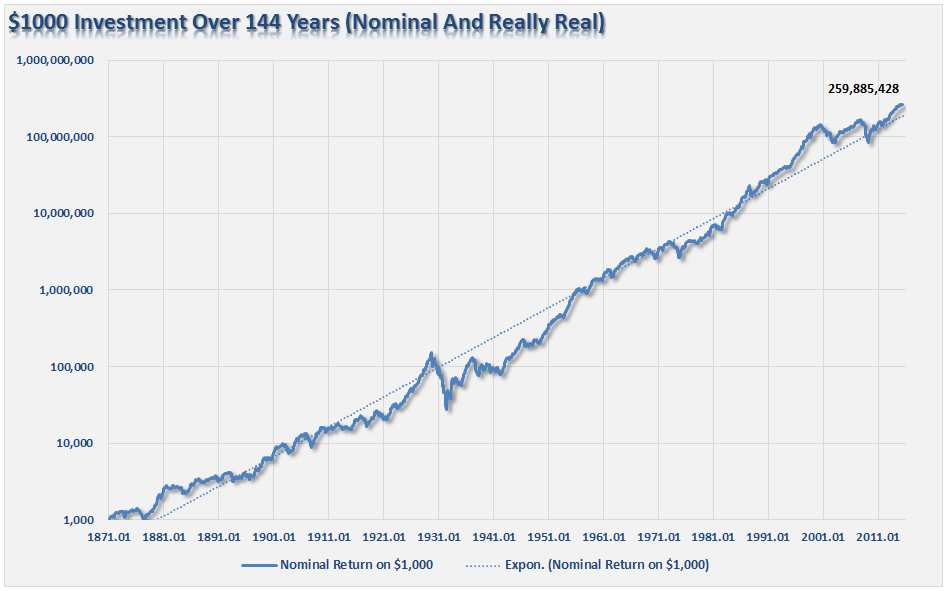

One of the biggest myths perpetrated by Wall Street on investors is showing individuals the following chart and telling them over the “long-term” the stock market has generated a 10% annualized total return.

The statement is not entirely false. Since 1900, stock market appreciation plus dividends have provided investors with

an AVERAGE return of 10% per year. Historically, 4%, or 40% of the total return, came from dividends alone. The other 60% came from capital appreciation that averaged 6% and equated to the long-term growth rate of the economy.

However, there are several fallacies with the notion that if you invest in the markets long-term you will continue to accrue a 10% annualized rate of return.

1) The market does not return 10% every year. There are many years where market returns have been sharply higher and significantly lower.

2) The analysis does not include the real world effects of inflation, taxes, fees and other expenses that subtract from total returns over the long-term.

3) You don’t have 144 years to invest and save.

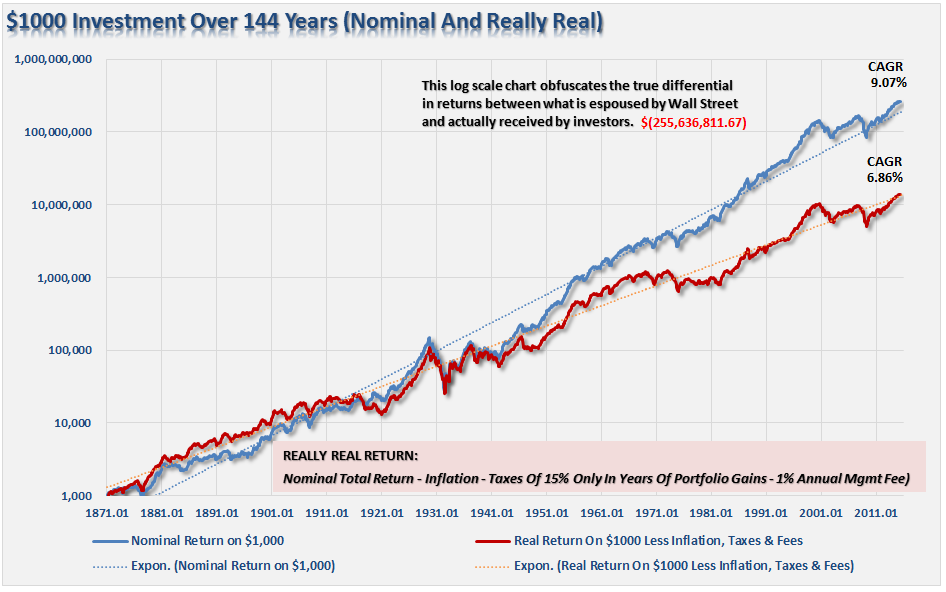

The chart below shows what happens to a $1000 investment from 1871 to present including the effects of inflation, taxes, and fees. (Assumptions: I have used a 15% tax rate on years the portfolio advanced in value, CPI as the benchmark for inflation and a 1% annual expense ratio. In reality, all of these assumptions are quite likely on the low side.)

As you can see, there is a dramatic difference in outcomes over the long-term.

From 1871 to present the total nominal return was 9.07% versus just 6.86% on a “real” basis. While the percentages may not seem like much, over such a long period the ending value of the original $1000 investment was lower by an astounding $260 million dollars.

Importantly, as stated previously, and as I will discuss more in a moment, the return that investors receive from the financial markets is more dependent on the “WHEN” you begin investing.

2) I Can Beat/Outperform The Stock Market

4) If You’re Not In, You’re Missing Out

5) You Can’t Time The Market – Just Buy And Hold

1. Why I’m Looking Forward to the Next Big Crash

by Bill Bonner

….who basically wants the whole intensely corrupt system to fall apart in a quick deep dirty depression/Crash. Wash everything clean. Then start over.

Industry the world over is trying to hide the lack of demand for their Cars by parking them brand new to rot and die in huge areas around the world. To the right is just a few of the thousands upon thousands of unsold cars at Sheerness. The other photo is the Port of Valencia in Spain where the cars have been sitting there since 2014.

Industry the world over is trying to hide the lack of demand for their Cars by parking them brand new to rot and die in huge areas around the world. To the right is just a few of the thousands upon thousands of unsold cars at Sheerness. The other photo is the Port of Valencia in Spain where the cars have been sitting there since 2014.

In baseball and football, making the cover of Sports Illustrated is the Holy Grail recognition achievement.

In modeling, it’s the cover of Vogue.

And in the world of innovation, making the cover of Popular Science gives you top bragging rights. And we’ve found a company that just has…

The Fastest Jet Ever Designed for Speed and Profit

Aerospace giant Lockheed Martin (NYSE: LMT) – operator of the famed “Skunk Works” unit that developed such “black project” winners as the supersonic SR-71 Blackbird, the high-flying U-2 reconnaissance aircraft, and the enemy airspace-penetrating F-117 Nighthawk – scored the latest Pop Science cover with the new spy plane the company is proposing for the U.S. Air Force.

The story – “America’s Secret Spyplane: Inside the Fastest Strike Jet Ever Designed” – graces the cover of the magazine’s June issue. The report focuses on an aircraft that Lockheed is referring to as the SR-72 – and that some writers have referred to as “Son of Blackbird” for its similarities to the now-retired SR-71.

We told our Private Briefing readers about this new spy plane in our Nov. 18, 2013, in our report,” Look Who’s Building America’s Next Spyplane.” We chose to focus on the jet because one of the partners in the development program is Aerojet Rocketdyne Holdings Inc. (NYSE: ARJD), a company whose stock we recommended at $11.40 a share back in February 2013, when it was still known as GenCorp Inc.

We told our Private Briefing readers about this new spy plane in our Nov. 18, 2013, in our report,” Look Who’s Building America’s Next Spyplane.” We chose to focus on the jet because one of the partners in the development program is Aerojet Rocketdyne Holdings Inc. (NYSE: ARJD), a company whose stock we recommended at $11.40 a share back in February 2013, when it was still known as GenCorp Inc.

We said the shares would double, and that’s just what they did: Shares of the maker of engines for rockets and missiles ran up more than 100% to peak at $24.99 a share.

But we continue to like the stock – a point we made in the April report “Missiles of October, Missiles of Pyongyang – and the One Stock to Buy.”

The fact that Popular Science saw fit to make this spy plane its cover story underscores the project’s importance.

That’s why I wanted to give you an update today.

Let’s start with a bit of historical context.

Blackbird, Fly

One of the reasons the “Son of Blackbird” is getting so much attention – aside from its stunning expected performance – is the stunning record of its predecessor, the SR-71.

From the time it became operational in 1964 until it was retired in 1989 (and then retired again in 1998), the SR-71 Blackbird spy plane was unparalleled it its ability to fly fast, fly high, and literally outrun the missiles enemy defenders fired to bring it down.

In fact, during its entire operational career – 3,551 mission sorties totaling 11,000 hours (including 2,750 mission hours being flown at Mach 3) – no Blackbird was ever felled by enemy fire.

That’s no surprise, of course: You can’t hit what you can’t catch.

The needle-nosed black jet cruised easily at Mach 3.2 and flew its missions at 85,000 feet – right at the edge of outer space. That extreme performance, and the spy plane’s 2,900-mile mission range, meant the Blackbird could “overfly” potential “hot spots” in North Korea and Vietnam – or even a nuclear test site deep inside China – and bring back “the goods” that U.S. military decision-makers desperately needed in order to act.

Spy satellites, for all their benefits, lacked the flexibility of a supersonic spy plane.

Jets, you see, can be directed to a specific target at a desired point in time – while satellites are shackled to their orbiting tracks. In fact, in cases where the president or military decision-makers need to look at a specific target, it can take as long as 24 hours before a satellite can be in the proper orbit – much longer than it takes to plan and launch a spy-plane mission. And because the overflights of satellites can be predicted, a targeted enemy can camouflage or in some other manner hide the assets our military leaders want to see.

These shortcomings quickly became apparent when Congress forced the Blackbird’s first retirement in 1989. Just four months later, with Operation Desert Storm swirling, U.S. Gen. “Stormin’ Norman” Schwarzkopf Jr. was told that the expedited reconnaissance the Blackbird could have given him was no longer available.

In part because of that lesson – and several others like it – several SR-71s were brought out of retirement in 1993. But the program was killed for good in 1998, leaving a gap in America’s strategic reconnaissance capabilities that new drone-type aircraft are just beginning to fill.

With that, Congress notched an achievement that had forever eluded our enemies.

It brought down the Blackbird.

Seventeen years later, America’s spy-plane saga is about to enter a new phase.

In November 2013 – when we first brought this story your way – Lockheed unveiled plans for the SR-72.

Lockheed is a storied aviation firm.

In World War II, it designed and built the P-38 Lightning, a twin-engine, twin-boom fighter that German Luftwaffe pilots referred to as der Gabelschwanz-Teufel (the “fork-tailed devil”). Indeed, it was the P-38 that America’s two top aces of all time flew – Army Air Force Pacific Theater of Operations (PTO) rivals Maj. Richard “Dick” Bong (40 victories) and Maj. Thomas McGuire (38 victories). It was also the plane used in April 1943 for the successful long-range interception of Japanese Adm. Isoroku Yamamoto, the architect of the attack on Pearl Harbor.

Lockheed has received the Collier Trophy six times, including in 2001 for being part of developing the X-35/F-35B LiftFan Propulsion System, and again in 2006 for heading the team that developed the F-22 Raptor jet fighter. It’s currently working on the F-35 Lightning II.

But it’s usually Lockheed’s “Skunk Works” unit – which developed all those super-secret jets – that generates the most awe from observers.

The “Son of Blackbird” could be the Skunk Works’ next big achievement. That’s the aircraft that we’re focusing on here – and that Popular Science spotlighted in its cover story.

Anatomy of a Spy Plane

Ever since the SR-71 was mothballed, aviation journalists, analysts, and other experts have speculated about a replacement aircraft. Most figured there was a “black” project successor that was being flown but not publicly revealed. The long-rumored (but never proven) “Aurora” was probably the most talked about candidate. But there were others, too.

In early November 2013, after years of unanswered queries, the Skunk Works disclosed the details of a longstanding project it described as an “affordable” hypersonic “intelligence, surveillance and reconnaissance” (ISR) jet the company believes could reach “demonstrator” status by 2018 and that could be deployed by 2030.

Aerojet Rocketdyne will provide the two revolutionary engines that keep the SR-72 affordable, while still enabling it to fly at Mach 6 – twice the speed of its unstoppable predecessor.

Armed versions of the unmanned aircraft will be able to launch strikes against the targets that it is surveilling – before they can hide. And here’s the kicker: The SR-72 will be unmanned – making it a drone, or unmanned aerial vehicle (UAV). But it will still be the fastest military jet on the planet.

The SR-72 “will require a hybrid propulsion system – a conventional off-the-shelf turbo jet that can take the plane from runway to Mach 3, and a hypersonic ramjet/scramjet that will push it the rest of the way,” writer Clay Dillow said in the Pop Science cover story. “Its body will have to withstand the extreme heat of hypersonic flight, when air friction alone could melt steel. Its bombs will have to hit targets from possibly 80,000 feet… once it is [deployed], the plane’s ability to cover one mile per second means it could reach any location on any continent in an hour – not that you’ll see it coming” because of its speed and stealthy cross-section.

This is a weapons capability that the U.S. military has wanted for some time. In the early 1990s, after the Blackbird was retired the first time – and as worries about North Korea and the Middle East had really started to spiral – U.S. Navy Adm. Richard C. Macke told the Senate Armed Services Committee that even a blanket of satellites wouldn’t negate the need for a spy plane like the SR-71.

“From the operator’s perspective, what I need is something that will not give me just a spot in time but will give me a track of what is happening,” Adm. Macke explained. “When we are trying to find out if the Serbs are taking arms, moving tanks or artillery into Bosnia, we can get a picture of them stacked up on the Serbian side of the bridge. We do not know whether they then went on to move across that bridge. We need the [data] that a tactical [vehicle like] an SR-71 [or] a U-2, or an unmanned vehicle of some sort, will give us, in addition to, not in replacement of, the ability of the satellites to go around and check not only that spot but a lot of other spots around the world for us. It is the integration of strategic and tactical.”

Yes, the military has wanted a jet like this for years.

But cost has been the problem.

The U.S. military has new drones. And some will have supersonic capability.

But none will have the hypersonic speed potential of the SR-71, which allowed it to avoid radar and outrun the surface-to-air missiles (or “SAMs,” in pilot-speak) that defend enemy airspace and are especially lethal around high-value targets.

It’s not just a matter of worrying about the loss of the aircraft. It’s also the fact that the loss of the aircraft often means that the badly needed information isn’t obtained.

“Hypersonic is the new stealth,” Brad Leland, portfolio manager for air-breathing hypersonic technologies at Lockheed Martin, told Aviation Week & Space Technology. “Your adversaries cannot hide or move their critical assets. They will be found. That becomes a game-changer.”

The reason no successor was developed was a combination of cost and capabilities.

Aircraft that fly at supersonic speeds – especially for extended periods – are subject to incredible temperatures. In fact, because the Blackbird was designed to fly so fast, the aircraft’s “skin” was built to expand as the jet’s surfaces heated up. As a result, it was notorious for leaking lots of jet fuel while sitting on the ground – the seams would close up when the surfaces reached their usual operating temperatures. That’s why the SR-71 was built from a heat-resistant alloy of titanium – one of the more expensive metals on Earth.

For a “hypersonic” aircraft designed to fly at Mach 6, the technical challenges and potential costs increase substantially. The stealth capabilities and new-technology avionics of today have soared in cost compared to what was used in the Blackbird.

But it’s the power plant – the aircraft’s engines – that would have been the most cost-prohibitive.

By devising a revolutionary solution, a Lockheed project director said the development team made that a moot issue.

“The Skunk Works has been working with Aerojet Rocketdyne for the past seven years to develop a method to integrate an off-the-shelf turbine with a scramjet to power the aircraft from standstill to Mach 6 plus,” Lockheed’s Leland said.

And the answer the team came up with is as simple as it is elegant – and literally opened the door for this remarkable new aircraft.

A Revolutionary Solution

The revolutionary approach – and I’m oversimplifying it here – involves mating the kind of high-speed-turbine engine you’d find in a supersonic jet fighter with a ramjet/scramjet. The turbine will take the aircraft from a standing start all the way up to about Mach 3 – where the ramjet/scramjet takes over. The design also allows the power plant to traverse what the development team refers to as the “thrust chasm” at about Mach 3.

The use of what is basically an off-the-shelf fighter-jet turbine with some modifications both to it and the ramjet makes the package much more affordable. The team believes it could have a demonstrator ready to fly in 2018 and an optionally piloted flight-research vehicle in the air by 2023.

If that goes well, the SR-72 program could be launched soon after and be in service by 2030. This timetable also dovetails with an Air Force plan to support development of a hypersonic strike weapon by 2020.

Don’t be depressed by the seemingly long time line: This is good news for GenCorp, a noted maker of high-speed motors that added to its offerings with the $550 million purchase of Pratt & Whitney’s Rocketdyne unit in June 2013.

Even before the sale, Lockheed’s Skunk Works unit had been collaborating on the SR-72 with the P&W Rocketdyne unit.

Once the sale went through, GenCorp combined Rocketdyne with its existing Aerojet rocket-motor business to create the bigger Aerojet Rocketdyne division.

And earlier this year, to reflect the shift in focus, the company changed its name to Aerojet Rocketdyne.

As we’ve told you in many reports – thanks to the proliferation of missile systems with intercontinental ranges – we’re forecasting a big uptick in demand for antiballistic missile systems (ballistic-missile interceptors). That was already bullish for Aerojet Rocketdyne.

The SR-72 project means that GenCorp’s rocket engine continues to get in on the new-and-futuristic growth opportunities in the military/aerospace sector.

As we’ve also said from the outset, the rocket-motor business isn’t the only undervalued asset GenCorp has. It also has some prime highway-frontage property in the Sacramento, Calif., area – carried on its books at the price it was bought for in the 1950s. The company is looking to divest that land in the next few years, and the windfall could power the stock to as much as $23 to $27 a share, we told you in a report back in 2013.

The “Son of Blackbird” program is one we’ll certainly be keeping an eye on: Thanks to Aerojet Rocketdyne, we believe it’s one of those stories that is as intriguing as it is profitable.

Everywhere I go I’m asked, “Will there be inflation or deflation? Are we in a bull or bear market? Is the bond bull market over and will interest rates rise?”

The flippant answer to all those questions is “Yes.” And that can be the correct answer as well, but it depends on what your time frame is and what tools you use to measure the markets and inflation. One of the newer members of the Mauldin Economics team is Jawad Mian, who writes a powerful global macro letter from his base in Dubai. He has been making the case for the “end of the deflation trade” (or more properly the return of a reflationary period) and the knock-on effects that would cause. Longtime readers know that I am in the secular deflation camp and ask me why there’s such a seeming difference my views and Jawad’s.

The answer is that Jawad and I are more or less on the same page over the longer term; the difference lies in the time frame of our perspective writings. I tend to think and forecast about longer periods of time, whereas Jawad’s main audience is portfolio managers and traders who are focused on the next 6 to 18 months. I tend to think in secular cycles, while Jawad is focused on the cyclical horizon. When you read the section below that Jawad writes, you will find a fairly upbeat analysis.

And that difference opens up a very important discussion for this week’s letter. I will start off by explaining why I think we are still in a long-term secular bear market in US stocks, even while I can clearly see that we are also in a powerful cyclical bull market. It is important to know both, because there are quite different investment approaches that are appropriate for different combinations of secular and cyclical cycles.

Then we turn to Jawad, who will discuss why we could see a reflationary macro regime emerge in much of the developed world and where the resulting opportunities might lie. I will finish up with why I think that this reflationary period will be temporary, with a potential for a serious round of deflation further out in the future, even though I readily acknowledge that “temporary” could mean a few years. But the looming reality over the longer term is that the coming war over a return of deflation will be fought by central banks everywhere. It will truly be World War D.

Why start with equity markets when we are talking about deflation and inflation? Because we need to see the connections!

I first wrote about a coming secular bear market in 1999. I was early, of course. The market went up (a lot!) for the next year. Over the next few years I began to do some work looking at secular bear markets not in terms of price but in terms of valuations. My now very good friend Ed Easterling of Crestmont Research was doing similar analysis, and we compared notes. Then we published a series of reports in this letter, which I later adapted in two chapters (co-authored by Ed) of my book Bull’s Eye Investing in 2003.

I believe secular bull and bear markets should be seen in terms of valuation, and cyclical bull and bear markets in terms of price. A secular bull market should be approached with a more aggressive, relative return style of trading, while a secular bear should have an absolute return focus with appropriate risk controls. That difference in trading style is necessary because of how valuations will trend in the two different types of markets.

Let’s look at the updated charts that Ed sent me over the weekend from his fabulous, data-rich website. In general, secular cycles are long-term trends in valuation. These cycles include numerous interim surges and falls in price that reflect shorter-term psychology and economics. The long-term secular cycles can be seen in this first graph, with secular bears represented in red and secular bulls shaded green. The driver of these cycles is the relative valuation of the stock market as reflected in the price/earnings ratio (P/E). When P/E trends higher, it multiplies earnings growth and generates periods of above-average returns. When P/E trends lower, it offsets some or all of earnings growth and delivers periods of below-average returns. P/E is the blue line underlying the secular cycles on the chart.

The P/E segments for all of the red-bar secular bears can be overlaid on a chart with time in years across the bottom and the level of P/E on the side (see chart below). First, secular bears tend to start in the red zone of high P/Es and decline to the green zone of low P/Es. This downshift into a secular bear is caused by a trend in the inflation rate from low, stable inflation to levels of either high inflation or deflation.

Second, this chart includes red and green arrow-lines that highlight the shorter-term cyclical bears and bulls during the current secular bear. The chart demonstrates that longer-term secular periods have cyclical bears and bulls within them, offering very profitable trading opportunities.

Third, the current level of the market P/E indicates that the stock market is fairly high. It is now well above the peaks of past secular bears and nowhere near the levels needed for a secular bull market start.

Even after more than 15 years in a secular bear market, the current secular trend has a ways to go to reach lower valuation levels. How can that be true after such a long period? In part, it’s because this secular bear started at such high levels. The current secular bear has experienced the same amount of P/E decline that many of the past secular bears experienced over longer and shorter periods, but the current secular bear started at twice the historical highs.

Bears start where bulls end and vice versa. As the secular bull market version of the previous chart shows, the late 1990s bubble took that secular bull market to unprecedented heights. A return from a period of either high inflation or deflation to low, stable levels of inflation will result in a rising trend in P/E during secular bull markets .

The “difference” between Jawad’s and my view on the inflation/deflation question is so important because turns within cycles have a major impact on pricing and valuations.

Yet even though we are in a secular bear that has come a long way with quite a ways to go, this secular bear looks and acts like previous secular bears. For example, here’s the daily graph for the previous secular bear in the 1960s and ’70s.

The cycles are very evident. Note the dramatic magnitude of their swings. Here’s the same format of chart for the current secular bear. Notice there are very similar patterns and magnitude… and new highs in the middle of the secular period.

Right now, many of you are scratching your heads and wondering how we get to lower valuations. Maybe this time is different! Or perhaps we’ll see a longer secular bear market until we return to a “normal” economic environment; and then earnings, prices, and valuations will begin to more closely resemble historical patterns. Remember, rising periods of inflation have historically compressed valuations.

While deflation fears have persisted since the 2008 meltdown, they intensified last year, with global inflation readings falling to their lowest level since 2009. The collapse in oil prices, combined with generally soft macro data and a rising dollar, is aggravating concerns about the inflation outlook. Inflation expectations have plunged, and sovereign bond markets have rallied sharply, with yields of less than zero in parts of Europe. Negative-yield bonds now account for some €1.5 trillion of debt issued by governments in the euro area, equivalent to almost 30% of the total outstanding. Many expect even more of the global bond market to fall into negative yield territory. Half of all government bonds in the world today yield less than 1%.

Many fear that the current deflation outbreak will turn into a “vicious circle of deflation,” in which consumption is postponed and investment plans are curtailed in anticipation of lower prices. These behaviors contribute to a further drop in demand and additional reductions in prices. The burden of debt increases, since falling incomes make it more difficult to service existing debt as real interest rates rise. Thus, economic growth slows and inflation declines further, hurting consumption and investment even more – hence, the vicious deflationary spiral.

As Christine Lagarde warned in January 2014, “Deflation is the ogre that must be fought decisively.” It is no surprise then that global short-term nominal interest rates are reaching the zero lower bound. Oil-price-induced weak inflation readings have forced aggressive reactions from policymakers, with at least 24 central banks already engaging in some form of monetary easing in 2015. According to my friend David Rosenberg, nearly 90% of the industrialized world economy is presently anchored by zero rates. There is a global focus on fighting deflation.

Why is inflation still nonexistent? And what do we make of all this unprecedented monetary policy? Is debt deflation the biggest risk to the global economy? What are some of the major implications for investors? In the next section Jawad parses the economic data and surveys the macro landscape to offer his cyclical (1 to 2 years) outlook, and then I consider the secular (5 to 10 years) outlook, with a particular emphasis on the threat of deflation.

A Little Less Deflation, A Little More Reflation, Please

By Jawad Mian

Deflation is not always sinister.

I believe the deflation scare of 2014 will give way to a global economic surprise in 2015. The type of deflation likely to be observed this year will benefit the global economy and provide a welcome boost to real household incomes. In my mind, the collapse in oil prices is good deflation; a decline in demand, wages, or forward expectations causes bad deflation. Once the shock of the speed of the recent drop in oil prices is overcome, cheaper oil will undoubtedly be an important net positive for the world economy later in the year.

There is little evidence that expectations of future price declines are suppressing employment, wages, consumer spending intentions, or even global manufacturing activity. Global recruitment difficulties are back at 2006 levels, and there is mounting evidence that wage gains should begin to accelerate where they are needed most: the US, Germany, and Japan.

The US created nearly 3 million jobs in 2014, and real wages have risen more over the past year than at any other point since 2009. Strong momentum in the labor market, ongoing recovery in the US housing market, positive wealth effects from a buoyant stock market, and declines in energy prices should all combine to generate strong consumer-led growth.

It is getting more difficult to attract and retain labor. The tighter labor market has led Walmart, the nation’s largest private employer, to increase wages for 500,000 of its most poorly paid workers. The company plans to spend about $1 billion a year to raise the pay of all employees (1.3 million) to at least $9 an hour, and to at least $10 an hour by next February. I believe Walmart’s bold initiative will lead to higher wages being set for entry-level jobs throughout the retail sector, a trend that may impact over 15 million people.

A look at interest rates, currency values, and reduced energy costs suggests that Europe and Japan will receive a significant reflationary boost. Europe’s economic turnaround is in its early stages and could provide a positive growth surprise over the next two years. The liquidity spigots are wide open, and the largely recapitalized banking system is responding to credit demand, as indicated by the latest ECB bank lending survey. Money supply and bank lending have continued to recover, with loan growth in the euro area about to turn positive for the first time since 2012.

The recent German consumer confidence reading was the highest it has been since 2001. German unemployment is near post-reunification lows, and real wages are growing at the fastest pace in over 20 years. IG Metall, Germany’s largest union, just settled on a 3.4% annual pay rise for its workers in southern Germany. More importantly, the deal is seen as a bellwether for salary negotiations in the rest of the country. Reports suggest that 32 regional contracts (covering seven unions and about 6.5 million workers) expire this year.

This is an essential part of euro-area rebalancing that should support growth in neighboring countries by way of a competitive boost. The Spanish labor market has enjoyed its best year since 2007, and the eurozone’s overall unemployment rate has fallen to a 33-month low.

Deflation is in the process of ending in Japan. The Bank of Japan has successfully cheapened the yen to its most competitive level since 1973 on a real effective exchange-rate basis. Export volumes are rising, and Japan’s balance of payments on tourism has turned positive for the first time in a long time. According to Peter Tasker, in terms of discretionary spending, the tourist boom is equivalent to an increase in the Japanese population of 1.4 million.

With the jobless rate down to 3.4%, Japan should be able to finally achieve some real wage growth this year. Just as Prime Minister Abe has been able to produce a genuine shift in the corporate governance climate in Japan, I firmly believe that Abe will be able to cajole corporate leaders to hike salaries as well, so as to “spread the warm winds of economic recovery to everyone throughout the country.” Last month, Toyota granted its employees their largest wage increase in more than a decade.

The global manufacturing sector has expanded for 28 consecutive months. Based on Markit’s recent Global Purchasing Managers Index (PMI) survey, the rate of output growth accelerated as companies scaled up production to meet rising levels of new work and new export orders. As US economic growth should now be driven more by consumption (which represents two-thirds of the US economy) rather than capital expenditures (capex), this implies stronger global trade, a wider US trade deficit, and a softer US dollar going forward.

The cyclical path of least resistance for commodities may also turn up later this year. A pickup in global PMIs suggests that we may have seen the worst of commodity price deflation. Oil excess supply remains elevated, but prices appear to have bottomed. According to Aurelija Augulyte, a senior analyst at Nordea Markets, even if you hold the dollar and oil prices at current levels, the base effects will effortlessly push the inflation up in the second half of this year.

Global core inflation appears to have already troughed. The number of nations where CPI fell month-over-month has collapsed from 23 in December and 33 in January to just 9 in February. I suspect downside pressure on global inflation readings will soon be exhausted.

In the US, core inflation has surprised positively three months in a row. The core CPI held at 1.8% year on year in April, up from 1.6% in January. Core CPI was at a 2.3% annual rate in the first quarter, up from a 1.6% pace in 2014. The Fed’s preferred measure of inflation (core personal consumption expenditure index) has been roughly stable for two years, around 1.5%.

Forward-looking indicators suggest that core inflation in Europe should also soon turn positive and begin to trend higher. It will become difficult for policymakers to maintain their ultra-dovish tone, with economic momentum improving and inflation rising later in the year. The cyclical upswing will dial back central bank aggression, in my view. Interest rates around the world will remain low, however, to help reduce the budget costs of a large public debt burden.

Source: Ned Davis Research

The clouds of deflation will part.

Even though headline inflation may continue lower in the months ahead, given the extent of the decline in the price of oil, I find reassuring evidence that core inflation in major economic blocs will stabilize as we approach mid-year.

I believe the basic assessment of deflation expectations will completely change, and the market will slowly recognize that there is another economic equilibrium that is very far from the current state.

There are green shoots of economic improvement around the world that augur well for the inflation outlook, but most investors remain too blinded by the oil crash to even notice them. James Paulsen, chief investment strategist at Wells Capital Management, provides an insightful take on our cultural obsession with deflation. I quote (with some edits for brevity):

Today, after more than three decades of disinflation, chronic deflation in the dominant technology sector, and a world which hovers near zero inflation, most are increasingly obsessed with the potential for a deflationary spiral. Despite universal expectations of falling inflation or deflation, however, several forces are emerging which likely ensure serious deflation will not result.

First, emerging world economies were primarily a supply story adding to disinflationary forces in the last decade. However, emerging economies are rapidly transitioning toward a major demand story which will probably prove much larger than the post-war baby boom. Second, balance sheets within the US have been significantly retrofitted since the 2008 crisis. Banks have perhaps never been as strongly capitalized as they are today and have unprecedented lending capacity. Corporate profits are at record highs, business balance sheets are strong, and cash flows are immense. US household net worth is almost 20% higher than its previous record and the debt service burden is at a new low. Household and corporate pent-up demands are considerable (due to the pause in spending during the crises of the 2000s) and the credit creation process is just beginning to revive.… Finally, a cultural obsession with depression and deflation evident since the 2008 crisis has produced unprecedented and massive economic policy stimulus despite a continuous economic recovery in the US for more than five years. When a culture becomes universally obsessed with a problem, it generally solves it!

The reason central bank action has been insufficient to overwhelm the forces of deflation thus far is that government deficits globally have been contracting since 2010.

When central banks have had loose monetary conditions in previous economic cycles, governments have been keen to spend this money to boost growth (and thus inflation); however, in this cycle, we have seen governments retrench their spending. In other words, fiscal tightening has acted as a counterweight to unprecedented monetary easing.

Emergency measures to reduce government borrowing have actually worsened the debt arithmetic and prolonged the economic malaise felt in major regions of the world. The romantic fixation with balanced budgets is counterproductive when deflationary pressures are building. When the private sector is deleveraging, the public sector must increase its borrowing and spend fortuitously to restore economic balance and boost aggregate demand. The main lesson from our recent travails is that lowering interest rates and engaging in QE is no panacea for growth in a low-inflation world, especially when fiscal policy is pulling in the opposite direction.

The IMF estimates that the effect of the fiscal multiplier at the zero lower bound exceeds the “normal times” multiplier by a large margin. Budget cuts of 0.5%–1% of GDP typically act as an economic drag of around two to four times that amount, so a reversal of fiscal austerity should prove very stimulative. In my view, investors are grossly underestimating the potential for favorable fiscal policies to boost growth in a very easy monetary policy environment.

Budget plans for the world’s major economies in 2015 show that, for the first time since 2009, fiscal policy won’t be a drag, according to Jeffrey Kleintop of Charles Schwab.

He highlights a few recent examples of changes in global fiscal policy:

- Japan has postponed the planned 2015 consumption tax increase.

- China has started to announce new spending projects intended to keep the economy from slowing more sharply.

- In the US, federal spending has increased for five straight months after being flat for five years, rising 5.5% year-over-year in October.

- France and Italy have been given more time by the European Commission to meet their deficit reduction targets, which means they won’t need to implement substantial spending cuts (tax cuts in France and Italy are more likely this year).

- Germany should ramp up spending after initially proposing to balance its budget in 2015, while…

- Europe will likely approve and begin to implement some version of President Juncker’s plan to provide more than €300 billion in spending initiatives.

I view the gradual move toward greater fiscal expenditure as a paradigm shift that will upset deflation expectations and overly subdued growth estimates in the developed world.

The market is a composite personality, and right now investors have developed a “collective consciousness” that is still agonizing over the threat of deflation, even as the inflation environment has been changing substantially. It may not seem like it now, but I believe monetary authorities have overcome the threat of deflation on a cyclical horizon. They have been successful in changing people’s perceptions and breaking the deflationary mindset, even if this shift is not yet reflected in the level of global government bond yields.

Government bonds in the major economies remain unattractive from a long-run valuation perspective. Globally, bond yields have fallen to levels not seen for centuries. How long can bond yields remain in their current prostrate position in the face of better economic health in 2015 and possibly into 2016?

I can imagine the world looking very different from the way the market currently expects it to. Since 2008, the global economy has never looked as good as it does today. We are finally entering a growth environment where no region of the world acts as a considerable drag (particularly in the case of Europe and Japan). The expanding strength in numerous international equity markets could be an important signal heralding far more durable global economic growth prospects.

Since 2011, we have seen deflationary trends dominate: the US dollar rising, global growth slowing, commodities crashing, inflation falling, global bond yields declining, and US stocks outperforming the rest of the world. If I am correct in thinking that the market’s deeply entrenched macro concerns regarding deflation will dissipate, all these trends should reverse. A global capital-rotation already appears to be underway that favors markets that have been long-time laggards versus the US stock market. I believe global equity market leadership might be inclined to shift to Europe and Asia.

I also think there is a major revaluation risk to owning government bonds at this stage of the investment cycle. With macro risks waning and inflation expectations slowly rising, I suspect global bond returns have probably crested. As the world emerges from the perceived threat of deflation, bond yields should rise toward equilibrium levels.

To learn more about Jawad and to receive his letter, Stray Reflections, click here.

It’s All About That Debt, ’Bout that Debt, ’Bout that Debt

John again. Now that you have explored Jawad’s thinking on global prospects for a reflationary period, I am going to summarize why I think we have not seen the end of deflation. (I have written about this theme before and will likely delve into it again – it’s important.)

First, normally, financial crises such as we had in 2008–09 bring about a period of deleveraging. This time, there been no debt reduction, and debt levels have skyrocketed throughout the world. Only in a few countries where there were housing bubbles have we even seen consumers retrench. The world is awash in debt! And ironically, the demand for even more debt seems to be insatiable, driving down yields.

In countries all over the world, debt is rising faster than global GDP, which means that at some point the carry cost of that debt is going to have to be reconciled. That is an economic law that was first noticed when the Medes were trading with the Persians. That is true for individuals, corporations, and governments. Of course, governments can monetize that debt if it is in a currency they control, but that course will typically weaken currencies (and thus buying power and value), which is default by another name.

All this was best articulated by Irving Fisher in his writing in the ’30s on the connection between debt and deflation.

The presence of too much debt, as Lacy Hunt and others have demonstrated, will slow the potential growth of GDP, which makes paying off that debt more difficult.

At some point, there will be another recession, with the accompanying bear market; and if there has been no resolution of the debt burden, there will be another debt crisis, and it will be massively deflationary. Central banks will respond with more QE than anyone can possibly imagine today. When will this happen? Two years? Three? Five? No one knows, but this eventuality is baked into the debt cycle.

Given what we have learned about the reaction of central banks and given that the debt problem is global, this next crisis will be unlike anything we have experienced.

I expect US rates to sink to new lows in a period that is also likely to see the final drop in yields of the 30+ year-long bond bull market.

In the meantime, we trade the cyclical cycles and look for yield and safety where we can.

One last point. Inflation, as I have written about in detail, is an artificial construct, and we have changed the way we measure it over the years. The CPI is just one method, and it is not used universally. If the US used the same measuring tools that Europe does, our central bankers would be having heart palpitations right now, as using the Eurozone definition of inflation would show the US in outright deflation.

Look at these charts from my friend Albert Edwards, from a few months ago. The difference in the formula for how you figure inflation in the US and the Eurozone is largely how you deal with the housing component. Today, the same definition shows the US to be in a deflationary zone. By the way, that same measure would have meant that Greenspan should have been a LOT more aggressive in raising rates. It is likely we would have avoided the housing bubble had he done so, or at least it would have been not so big. But that’s a guess.

So, it makes a difference what measures you use, what index methodology you choose, and how you account for value. If you can change the data, you can make it say what you want it to say and support your case, whatever that might be.

Secular versus cyclical matters. We invest mostly in the shorter cyclical term, but the secular patterns tell us where the tail risk lies.

Here and There, New York, New Hampshire, Vermont, and NYC

I am on the road, making a few one-day business trips. Tomorrow I go to Virginia Beach to see my old friend Mark Finn for the afternoon, before taking a late flight to Dallas. Sunday I go to New York City, where I will be for five days, before going to New Hampshire for a speech and then on to Vermont Sunday afternoon to be with my partners and the management team of Mauldin Economics. Then it’s back to Dallas, where I’m trying to put the rest of my summer together. I know I will be heading up to New England later in August and of course there is the annual fishing trip the first Friday of August in Maine.

For what it’s worth, I will be at the NYSE next Monday to be part of the closing bell ceremony, where Monty Bennett, the chairman of a new public company whose board I am on, Ashford Inc., will ring the bell before we go over to Bobby Van’s and hang with the Friends of Fermentation. I see steaks. Ashford Inc. is involved in the hotel business and managing REITS. I have to admit I am learning a great deal more than I think I am contributing. Getting into the nitty gritty of this company has been a fascinating learning experience about a simple idea – renting a hotel room – that is a very complex business to do right. And, diving deep into Ashford’s numbers, I see all sorts of correlations with other economic data. Intriguing.

By way of a short teaser, I’ve been reading the galleys for my latest book, which should be out in a few weeks. We are going to be offering this book in a slightly different manner than previous books as part of a marketing experiment. I’m quite proud of it and look forward to sharing it with you.

Again, if you’d like to know more about what Jawad writes, you can go here. Jawad has attracted a lot of interest from serious traders and investors around the world, and deservedly so. He left a successful career as a portfolio manager to follow his passion for independent macro research and trading. As he often reminds me, “There is nothing more important to investment success than the freedom to express your own views.” I am really pleased that he wanted to join our team, and I enjoy my frequent interchanges with him. I always learn a lot.

It’s time to hit the send button. I’m in Boston tonight and see Legal Seafood in my near future. Looking over the harbor on this beautiful day, I see sailboats and ferries scurrying everywhere. Back in Texas it is raining and flooding, although Dallas seems to be avoiding the real problems. Houston, however, was built on a swamp, and swamps flood. Not much they can do about it. It was a problem when I lived there in the late ’60s as a student at Rice, and it will still be a problem in another 40 years. Some of us wish we could shift that rain out West, and most wouldn’t even mind if some hit California. Last year at this time there were open worries about many of our lakes drying up. Now the water is over the dams. But that’s Texas for you.

Next week I am going to get a little controversial. I recently had a well-received op-ed in the Investors Business Daily on what policies the US needs to implement to spur economic growth. I am going to develop that theme here. There will be something to please and annoy everyone. Have a great week!

Your never seeming to get to slow down analyst,

John Mauldin

subscribers@mauldineconomics.com

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair