Timing & trends

With all the hype and noise built in to daily and weekly market management, sometimes it is worthwhile to dial out, calm things down and touch base with markets on the big picture. Here are views on various markets (with limited commentary) by way of some NFTRH monthly charts.

Let’s start with currencies, since they are a reflection upon global policy making, which has been unprecedented in its direct market interference over the last few years.

Nominal Charts – Currency

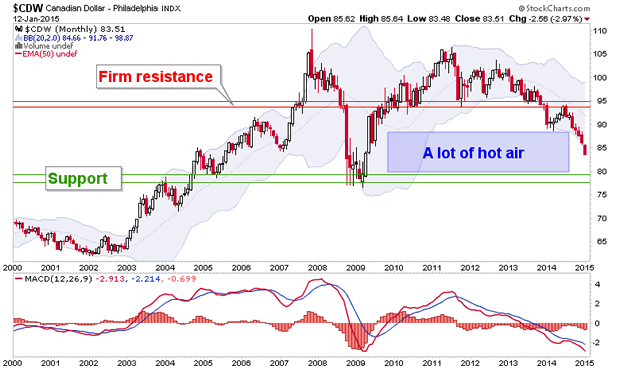

We noted the hot air patch in the Canada dollar last year. I had thought CDW might stop and find support at 85, which is a measurement from the topping pattern; but so far, no dice.

Larger Image

…continue reading & viewing another 36 charts with Larger views HERE

Just take a moment and read this list – it’s full of cool stuff and essential information.

Just take a moment and read this list – it’s full of cool stuff and essential information.

– By the end of this year Amazon will have put 10,000 robots in their warehouses. The robots are integrated into the delivery system and are estimated to save them between $400 million and $900 million annually as well as decrease customer delivery time.

– In November Arizona’s Local Motors built the first fully-functional 3D-printed electric car. It only took two days to construct. The car is made up of 49 parts, which pales in comparisons to all the nuts and bolts that make up your metallic car. The company aims to sell it for about $17,000.

– Last spring, a software algorithm wrote a breaking news article about an earthquake that The Los Angeles Times published.

– Morgan Stanley predicts that widespread adoption of self driving vehicles will contribute $1.3 trillion to the U.S. economy through cost savings from reduced fuel consumption and accidents, including $507 billion in productivity gains because people could work while commuting instead of driving.

– Robots now deliver fresh towels at the Aloft Hotel in Cupertino, California while an automated anesthesiologist, called Sedasys is increasingly employed in hospitals. Microsoft’s Kinect can recognize a person’s movements and correct them while doing exercise or physical therapy thereby aiding (or replacing?) physiotherapists.

You Can’t Ignore The Financial Opportunities

– Smartwatches are expected to ship 10.8 million units in 2015, up 400% plus from 2014 according to Shawn DuBravac, chief economist of the Consumer Electronics Association.

– 1.3 million units of ultra high definition 4K TVs sold in the US last year, up from 77,000 in 2013. The number is expected to grow over 300% this year to 4 million units and then jump another 250% in 2016 to 10 million units.

– Revenues for drones were up 50 percent in 2014. Global revenue for drone sales in 2015 is expected to be $130 million.

No matter what I say it will not do justice to the revolutionary changes and the massive opportunities in technology that are taking place. This is THE good news story of next generation but it’s surprising how many people don’t appreciate it – including virtually every current affairs commentator in the media.

The tech revolution has the potential to overcome the litany of bad news stories that threaten to overwhelm us like sovereign debt, geopolitical unrest, unfunded entitlement promises and financially incompetent governments.

For example, tech innovation has already resulted in significant improvements in fuel efficiency. As Bloomberg News reports, the amount of oil consumed per day in the US, for every $1 billion of economic activity, is down 33% from 20 years ago. The University of Michigan’s Transportation Research Institute reports that since 2007 the average car gets 28% better mileage.

Tech is the #1 driver of economic and investment growth

Most of us now understand the importance of 3D printers. Granted, on the investment side, I recommended taking profits in 3D stocks over a year ago – but that wasn’t because I doubt about the massive growth potential. It was because I saw more immediate downside risk than upside potential.

I still feel it’s too early to re-enter the 3D arena but I’m on the look-out for a bottom. In the meantime, new applications and new materials as well as a rapid expansion of the market are making the best 3D stocks even more interesting. There are going to be some monster winners in this area – Hewlitt Packard, Stratasys, 3D Printing and others are vying for leadership.

But 3D printers are just one example. Picking the winning robotics companies will make investors a heck of a lot of money. At the Consumer Electronics Show a week ago in Las Vegas, personal robots were the rage.

Maybe Intel is poised to be a big winner with its RealSense Technology, which offers the ability for electronic devices to understand and interact with the world in three dimensions. Intel is teaming up with iRobot to create a robot butler or maid, which will have a high level of dexterity and be able to navigate difficult environments. The technology is complicated but the end result is not. Real freaking robots in the home doing my chores!

I am very interested in the suppliers for the smart phone industry. Apple introduces its first smart watch this year and its suppliers are going to see their revenues explode.

The incredible opportunities in tech – and the societal change it is fostering is why I read everything I can get detailing the advancements in nanotechnology, biotech, telecommunications and artificial intelligence, all driven by the explosion in information technology.

And some of the stock moves are incredible in tech related companies. Three years ago in Keystone’s World Outlook portfolio, Ryan Irvin recommended Enghouse Systems at the $8.00 level. The company’s software services a variety of segments in a number of industries including traditional call centres and online help desks. Today it trades just above $41 – a 414% capital gain not including a good dividend.

There’s also real action in small tech companies like Canadian based Firan Technology Group, which supplies aerospace and defense electronic products, specializing in quick turn around production runs for some large corporate clients. The stock was up 120% between Jan 1, 2014 and the first week of December.

Big names like Go Pro are still up over 170% from their IPO while Truecar is up about 160%.

And as I mentioned above with the high flying 3D stocks – there are definitely some companies that have become over hyped and over priced. King Digital, maker of Candy Crush is off about 40% since it first traded in March.

Choosing the right tech is essential

There are literally hundreds of examples of innovative companies changing our future and making major moves in the market but that’s the point. The next 10 years will witness more technological change than the last 100 years combined. Investors are going to have a huge array of opportunities. Forgive the cliché but this is where the action is if you’re looking for growth.

Big Change At The World Outlook Conference

This year we are going to feature a specific program for all things tech – called InvesTech. In a nutshell, this will be fun. Not only are we going to demonstrate some of the latest tech gadgets, I will be joined by three well known industry experts to share their expertise. Eamonn Percy, President of The Percy Group joins Brent Holliday, CEO of Garibaldi Capital Advisors and Patrick Cox, John Mauldin’s top tech analyst to talk about the most important investment opportunities.

As I said, whatever I write won’t do justice to the importance of the tech revolution but luckily these experts will go a long way to rectify that. Better still, you get a chance to meet both Brent, Eamonn and other tech experts and ask them your personal investment questions.

Finally

I am unequivocal in stating that each one of us needs to get familiar with the tech revolution. The World Outlook Financial Conference is your chance to not only hear renowned analysts like Martin Armstrong, Lance Roberts (just confirmed), Don Coxe, Greg Weldon and to see Ryan Irvine’s World Outlook Small Cap Portfolio 2015. It’s also an opportunity to get familiar with the most important investment opportunities of the next generation.

I hope to see you there.

Sincerely,

Mike,

Host of Money Talks

Conference Details

Where: Westin Bayshore, Downtown Vancouver

When: Friday, Jan 30th 1pm – 8pm and Saturday, Jan 31st 8:30m – 4pm

To book Your Ticket: go to http://moneytalks.net/events/world-outlook-financial-conference.html

Cost: $129 for a General Admission two day pass

When China celebrates its new year next month, we will transition into the Year of the Ram, also known as the Year of the Goat or Sheep. If you believe in luck, this could be a good sign. The ram comes eighth in the 12-zodiac cycle, and in Mandarin, “eight” sounds very similar to the words meaning “prosper,” “wealth” or, in some dialects, “fortune.” As you might imagine, the Chinese consider the number to be very lucky.

When China celebrates its new year next month, we will transition into the Year of the Ram, also known as the Year of the Goat or Sheep. If you believe in luck, this could be a good sign. The ram comes eighth in the 12-zodiac cycle, and in Mandarin, “eight” sounds very similar to the words meaning “prosper,” “wealth” or, in some dialects, “fortune.” As you might imagine, the Chinese consider the number to be very lucky.

But of course successful investing involves so much more than luck. In a time when not only China but much of the rest of the world is trying to get its groove back, it’s important to be cognizant of the factors that shape the markets, including changing government policy. We often say that government policy is a precursor to change, so it’s important to follow the money.

With that in mind, I asked Xian Liang, portfolio manager of our China Region Fund (USCOX), to outline a few of the most compelling cases to remain bullish on the Asian giant.

Below are some highlights from our discussion.

A Healthy Balance Between Monetary and Fiscal Support

A Healthy Balance Between Monetary and Fiscal Support

Back in October, I pointed out that one of the main contributors to the European Union’s sluggish growth is its inability to balance its monetary and fiscal policies. It has been eager to tax everything and everyone who moves. Waiting for European Central Bank (ECB) President Mario Draghi to act often feels a little like waiting for Godot. Investors’ patience is wearing thin.

China, on the other hand, is much more responsive and actively committed to making full use of both policies in its arsenal to spur its cooling economy.

On the monetary side, according to Xian, are interest rate cuts and a loosening of reserve requirements for certain deposits. The goal is to ease access to loans for businesses and individuals seeking to purchase big-ticket items such as homes. As a result, Chinese entrepreneurs have increasingly been able to start more businesses.

Jobs growth has been so robust, in fact, that the government has managed to attain its job creation target outlined in its current Five-Year period ahead of schedule and by a wide margin. The country has grown millions of jobs with great efficiency, even as GDP sags.

Although the Chinese housing market has stagnated in recent months, these new monetary measures will help it pick up steam. Already we’re seeing some improvement, with home property stocks moving higher.

Regulations are an indirect taxation of the economy, whereas deregulation unleashes entrepreneurial spirit.

On the fiscal front, the government is reportedly planning to spend $1.6 trillion over the next two years on infrastructure projects in various industries—300 separate infrastructure programs, to be exact, according to BCA Research.

As I pointed out last month, many of these projects will largely involve high-speed rail,both domestically and abroad. China has already secured multiple construction deals with countries ranging from Brazil, South Africa, Nigeria, India, Russia, the U.S. and others.

Government to Remain Accommodative

There are a couple of reasons the Chinese government has accelerated support to capital markets, according to Xian: “One, a significant deflationary threat has been driven by slumping energy prices. And two, there are potentially lower exports to commodity producing nations.”

Indeed, sluggish global demand has contributed to China’s weak December purchasing managers’ index (PMI), which dropped to an 18-month low of 50.1. China has been quick to respond to lower PMI data with a drop in interest rates.

But Where There’s Bad News, Good News Is Often Not Far Behind

The silver lining to falling commodity prices is that since China is a net-importer of raw materials—crude oil especially—the country has been able to save tremendously on its oil and gas bills. Back in November, I reported that for every dollar the price of a barrel of oil drops, China’s economy saves about $2 billion annually. From its peak in June, crude has slipped close to $50—you do the math. This has served as a major wealth transfer from oil-producing countries into China’s coffers.

Oil Sinks, Airlines Take Flight

Speaking of crude, declining oil prices have been good for airlines, Chinese companies included. As you can see, there’s been a clear inverse relationship between crude oil returns and airline stocks.

China is the largest investor in U.S. government bonds. The country has accumulated close to $1.3 trillion, so a strong dollar and falling oil prices benefit its economic flexibility.

More middle-class Chinese might be able to afford to travel abroad, specifically here to the U.S., where inevitably they will spend their money.

According to Carl Weinberg, founder and chief economist of High Frequency Economics:

Chinese President Xi Jinping has estimated that there will be more than a half-billion Chinese tourists traveling to the West in the next 10 years. You can work out the impact if all of them came to New York and spent $2,000 or $3,000 each. That would be enough to add a half-percentage point to U.S. GDP every year over the next decade.

Reasonable Stock Valuation

Chinese stocks are currently valued below their own historical averages as well as those among other global emerging markets, making them both attractive and competitive.

“Odds favor mean reversion to continue,” Xian says. “The better the Chinese markets perform, the more global liquidity they might attract.”

Chinese stocks, as expressed in the MSCI China Index, are currently a much better value than those in the S&P 500 Index, trading at 10 times earnings whereas the U.S. is trading at 18 times.

A-Shares Still a Huge Draw

Chinese A-Shares surprised the market by breaking out last summer, having delivered 66 percent for the 12-month period. It looks like a breakout from the long-term bear market.

What’s more, the upside is unlikely to have been exhausted. Although they aren’t as stellar of a bargain as they once were, they’re not yet overvalued, and retail and institutional investors might accumulate on pullbacks.

What’s more, the upside is unlikely to have been exhausted. Although they aren’t as stellar of a bargain as they once were, they’re not yet overvalued, and retail and institutional investors might accumulate on pullbacks.

For the A-Shares market, USCOX has recently added exposure to A-Shares to capture more attractive valuation. In today’s environment, we believe the safer bets are investable H-Shares, which are driven by A-Shares and, in 2014, returned 15.5 percent. H-Shares comprise the vast majority of the fund’s exposure to Chinese equities, with further exposure gained through A-Shares exchange-traded funds (ETFs).

To the right you can see merely a sampling of the ever-popular emerging markets periodic tables, which will soon be available exclusively to subscribers of our award-winning Investor Alert.

The Ram Is the New Bull

As GARP (growth at a reasonable price) hunters, we’re prudently optimistic about the upcoming year and anticipate great things out of the world’s second-largest economy. China’s government and central bank are committed to jobs and manufacturing growth as well as policy easing. Its stocks are reasonably valued, and low commodity prices should continue to offset slowing global demand.

As Xian eloquently put it last month:

China’s leadership appears to be delivering on the promises it made in November 2013 at the Third Plenary Session, specifically the liberalization of the financial sector and reform of the role capital markets play in allocating resources. This leadership is determined and committed to putting China on the right path.

A Special Announcement

Please mark your calendars for January 21, as we will be conducting our first webcast of the year. We will be discussing the state of commodities, and as a loyal subscriber, you’ll be first to receive the registration this week. We’ll be following up with an emerging markets webcast on February 18 that will focus on China and Emerging Europe.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by

Past performance does not guarantee future results.

Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. By investing in a specific geographic region, a regional fund’s returns and share price may be more volatile than those of a less concentrated portfolio.

The HSBC China Services PMI is based on data compiled from monthly replies to questionnaires sent to purchasing executives at more than 400 private service-sector companies.

The MSCI China Free Index is a capitalization weighted index that monitors the performance of stocks from the country of China.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

Standard deviation is a measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. Standard deviation is also known as historical volatility.

Fund portfolios are actively managed, and holdings may change daily. Holdings are reported as of the most recent quarter-end. Holdings in the China Region Fund as a percentage of net assets as of 9/30/2014: Air China Ltd. 0.00%, China Eastern Airlines 0.00%, China Southern Airlines Co. 0.00%.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

We think financial markets are beginning to have second thoughts about the Fed…a month ago “everybody knew” that the Fed was going to start raising interest rates in 2015…but now we see signs that “some people” aren’t so sure…if these second thoughts become more wide spread then the US Dollar will take a hit…and other markets will react to that.

At the beginning of 2014 “everybody” was forecasting that interest rates would rise…they didn’t…and Treasuries out-performed stocks by a mile. At the beginning of 2015 “everybody” is forecasting that the US Dollar will keep rising. One of the KEY components of the USD bullish forecasts is “divergent” central bank policies…the Fed is expected to tighten while other central banks either sit on their hands or ease.

But since mid-December US credit markets have been “backing away” from their conviction that the Fed will tighten in 2015. Economic weakness outside the USA, falling commodity prices, a strong US Dollar and falling domestic wage growth may cause the Fed to reconsider.

The December 2015 Eurodollar: has rallied ~20 basis points since mid-December…meaning that…come December 2015…the market is expecting 90 day Eurodollar rates to be ~20 basis points lower than what was expected 3 weeks ago. (The Eurodollar contract trades at a discount to par…rising prices signify lower interest rates)

The Euro Currency: We think that the sell-off in the Euro is over-done…it has fallen for 7 consecutive months… it’s at 9 year lows…virtually all currency analysts are lowering their year-end forecasts to Par or worse…bad news for the Euro is everywhere and speculators hold record sized short positions…we are in a “Buy the Rumor / Sell the News” mood. If there is a correction in the USD and the Euro starts to rally then short-covering could easily drive prices to the 125 level. We remain long-term bearish the Euro but we sense a short-term bounce may be at hand.

We took an initial position betting on a USD correction last week…we bought OTM Euro calls…our thinking was that IF the USD is going to correct then the Euro would likely have the steepest rally of all the currencies. If we see signs that the Euro is turning higher we will get more aggressive. If the Euro doesn’t rally we will limit our losses to ~50% of the option premium.

The Canadian Dollar: closed last week at 5 ½ year lows. The more Crude Oil falls the more intense the pressure on CAD…we have added to our long-term hedges on CAD the past couple of months…it’s been hard to sell more CAD at 5 year lows but we felt under-hedged being short only ~30% of our net worth. If the USD corrects lower then we expect all currencies will rally…but CAD probably less than others…unless there is a BIG bounce in Crude. We have no short-term trading position in CAD…but would probably look to get short if it rallies on any USD weakness.

WTI Crude Oil: traded to a new 5 ½ year low last week…closing lower for 14 of the last 15 weeks as it fell from ~$95 to ~$47. Crude seems to be extremely over-sold and it might rally if…the USD shows signs of correcting. We have no current position…BUT…

WTI Crude Oil option volatility: has more than tripled from multi-year lows made in July. We have no current position in Crude…but…we would certainly consider writing OTM puts if we thought that the breathless decline was going to pause…or reverse.

Gold: we bought gold in early December…we were impressed with the $80 rally off the lows on December 1…and we added to our position last week. We like the way gold has traded even as Crude has tumbled and the USD has soared. We note that gold stocks have out-performed gold. We see serious chart resistance at ~$1250…a rally through that level would be impressive. Given that we expect a USD correction we like our long gold position and would look to add on a rally through $1250.

The S+P 500: traded to All Time Highs after Christmas…then sold off into January 6. For our short-term trading accounts…trading on nothing more than market action…we bought OTM calls last Wednesday and loved the big Thursday rally ahead of the Friday UE report. We sold the calls early Friday morning and late in the day we took a new position shorting OTM puts. We obviously think the market is going higher but would abandon our short puts if Thursday’s lows were convincingly broken.

The investment climate is being shaped by four forces:

- De-synchronized business cycle with the U.S. ahead of the pack.

- The prospects of sovereign bond purchases by the ECB, amid political uncertainty sparked by Geece’s snap election.

- The continued drop in energy prices is a stimulative writ large but poses challenges for oil producers and the leveraged eco-system that has been built on the premise of high oil prices forever.

- Rather than a race to the bottom, as many saw it previously, several emerging market countries are resisting further depreciation of their currencies.

1. De-synchronized business cycle: This is the meaning of divergence. The U.S. policy response to the financial crisis, and the flexibility of the U.S. institutions bolsters the world’s largest economy. The U.S. economy expanded more in Q3 (5% annualized) than the euro zone (less than 1%) and Japan (less than 0.5%) in 2014 put together. China, the world’s second largest economy, is slowing.

While the euro zone, Japan, and China provide more stimulus for their economies, the U.S. is expected to lift rates around the middle of the year. This anticipation underpins the U.S. dollar. Given the importance of exchange rates (foreign exchange variability can be 2/3 of the return on international fixed income portfolios and 1/3 of the return of international equity portfolios), the prospects of a stronger dollar also make U.S. assets more attractive for non-dollar-based investors. Interest rate differentials are also moving in the U.S. direction.

Even though the above trend growth in the U.S. is not sustainable, employment and consumption can still expand. The U.S. reports the December jobs data at the end of the week and another 200k+ report is expected. Although it will likely not match the November 331k increase, such a number is still healthy, and the internals are also improving.

Auto sales will be interesting. The decline in the price of gasoline, easy and low financing, and the improving labor market underpin a strong year of sales. Manufacturer incentives also help. Industry figures suggest there was an average $2,894 in incentives or discounts during the month. This is almost a 6% increase from a year ago. The consensus expects a 16.9 mln unit pace down slightly from the 17.03 mln pace in November. It would put the entire year sales around 16.4 mln, the strongest in a decade. This compares with 15.5 mln vehicle sales in 2013 and 14.4 mln in 2012.

Strong sales are behind the strong production figures. The industry is integrated on a continental basis. Output in North America is projected to have risen by 7% in 2014 to a little more than 17.2 mln vehicles. To put this in perspective, consider that the peak was in 2000 at 17.3 mln vehicles.

2. Eurozone: January is shaping up to be a very important month for EMU. On January 14, the European Court of Justice will issue a non-binding opinion on ECB’s OMT (Outright Market Transaction facility), under which the central bank would buy sovereign bonds in the secondary market to aid a country provided the country met four requirements:

- The country was on an EFSF/ESM support program, which could include a precautionary line of credit.

- It had signed a memorandum of understanding, which is the policy adjustments the country would be expected to make.

- The country had access to the capital markets, which means able to issue 10-year bonds.

- Its bond yields were higher than fundamentally justified.

Recall that the Bundesbank testified against OMT, even though it appeared to have Berlin’s support. Although the ECJ opinion is non-binding, it is likely to be consistent with the final ruling. The facility has not been triggered. There is some thought that any conditions the ECJ cites may influence next steps of the ECB. On January 22, the ECB meets. It is the first meeting under the new regime of less frequent meetings, rotating voting scheme. Some record (minutes) of the meeting may be published for the first time 3-5 weeks after the meeting.

It is possible that the ECB announces that it will increase the speed at which it will increase its balance sheet by buying a broader range of assets, including sovereign bonds. If the ECB waits for its next meeting (March 5 in Cyprus), which at his December press conference Draghi hinted was a possibility, the peripheral bonds (and other so-called risk assets in Europe) could sell-off in disappointment. This will be especially true if this week’s flash CPI for the euro zone shows its first negative print as the consensus expects.

[Listen to: Brian Pretti: Central Banks Are Afraid to Let Asset Prices Fall]

Given that the current programs, which include the TLTRO, ABS and covered bond purchases, are projected to increase the ECB’s balance sheet by 400-500 bln euros, the sovereign bond buying program is likely to be modest compared with the programs in the U.S., UK and Japan. A sovereign bond buying program of around 500-600 bln euros might be sufficient to reach the ECB’s balance sheet goal. The modest size and limit could help secure support for such a plan. Also, allowing the national central banks to execute the purchases and to hold the assets on their respective balance sheets (as opposed to the ECB’s balance sheet) may also make the scheme more acceptable.

The Greek election will be held on January 25, three days after the ECB meeting. Polls currently suggest that no party will secure a majority. The party with a plurality, currently looking like Syriza, will be given the first chance to form a government. If it cannot do so in three days, the party with the second highest votes, now the New Democracy, would be given a chance. If it fails to secure a majority of votes in parliament, it will go to the third party and if it too fails there will be new elections, which is what happened in 2012. See our analysis of Greek politics here and why we expect Greece will remain in the monetary union.

3. Drop in energy prices: Oil prices have been more than halved over the past six months, but a significant low remains elusive. Additional losses are likely. An unscientific survey indicates that many see 2/3-3/4 of the decline is being driven by supply considerations. A quarter to a third of the decline is a function of weak demand. Demand may take some time to improve. China, as we noted, is slowing. Large swathes of Europe are stagnant.

Supply is also slow to respond. In addition to the weekly inventory data, investors will be closely watching Baker-Hughes weekly rig count figures that are reported on Fridays. The most recent data covers the last full week of December. The oil rig count declined by 37 in the week ending December 26, leaving 1499 onshore oil rigs. This is the least since April. Over the latest three week period, 76 rigs have been taken out of production. These are the least productive rigs. Output remains high despite the rig count decline. The U.S. produced 9.13 mln barrels a day in the week ending December 19, just off the modest record pace of 9.14 mln barrels the previous week.

[Analysis: Joseph Dancy: Crude Oil Markets Surprise Analysts and Investors]

Saudi Arabia shows no sign that it will reconsider its decision not to cut output. The latest figures show Russia and Iraq may have increased production, which is the only way to preserve revenue in a falling price market. Other high cost producers, such as the UK and Canada are feeling the squeeze. Canada may fare better with the help of the U.S. Senate (now in Republican hands), which will likely approve the Keystone Pipeline. The U.S. is also moving toward allowing greater exports of condensate (lightly processed), and could move toward lifting the ban on crude exports.

The drop in energy prices will lower measures of headline inflation. The secondary impact could seep into core measures. At the same time, it will help boost the disposable income of many and help lift consumption. On the other hand, there are some regions, such as Texas and North Dakota that will be adversely impacted from the decline in energy prices. Investors will be watching these states weekly initial jobless claim figures and regional surveys, such as the Dallas Fed survey, which at the end of December was reported at 4.1, less than half of the consensus expectation.

4. Currency wars and the lack thereof. We have long found the claims of currency wars to be hyperbolic; often confusing an analogy with the real thing, juxtaposing means and ends, with limited explanatory ability, and even less predictive power. U.S. officials have not objected to the dollar’s strength or expressed much misgivings about the policy thrust of the euro area (Germany is a different matter) or Japan, and neither have other global financial officials.

Although many observers talk about the race to the bottom, none have proclaimed victory for Russia, which saw a 46% decline in the ruble in 2014, or Argentina, which saw a 23% decline in the peso. Nor is it true that many emerging market countries are simply hell-bent on currency depreciation for mercantilist reasons.

In a weak dollar environment, it is true that many countries seek to slow their currencies’ appreciation. Reserves tend to grow in a weak dollar environment and central banks fill the void left by private sector investors. However, the dollar is strong now. Reserve growth typically slows in a strong dollar period. A number of countries seek to prevent or slow their currencies decline. This often requires the sales of dollars (and Treasuries, which the dollars are kept in, though it may also now include the sales of euros). Many emerging market countries, and especially their companies have taken on foreign currency debt. The decline of their currencies exposes a potentially destabilizing currency mismatch. Some countries may also seek to mitigate the inflationary implications of currency weakness.

[Hear: Axel Merk: Volatility the Big Issue in 2015 – Markets and the Dollar Could Weaken]

Turkey’s announcement on Saturday is a case in point. It hiked the foreign exchange reserve requirement for Turkish banks. Effective the middle of next month, banks will have to hold 18% reserves on foreign exchange deposits of one year, up from 13%. On two-year deposits, banks have to hold 13% in reserves, up from 11%. The central bank projects this measure is worth about $3.2 bln. In order to induce longer-term deposits, the central bank cut the reserves required on deposits of three-years to 8% from 11%. Officials also made technical adjustments in their reserve-option facility (allows banks to use dollars to meet their local currency reserve requirements) that the central bank projects will free up $2.4 bln in the banking system.

According to BIS data, at the end of Q3 ‘14, Turkey’s total foreign borrowing stood at near $400 bln, just below the record high reported for Q2. Just shy of two-thirds of the debt is from Turkish corporations, with local banks accounting for the remainder. We have highlighted the currency mismatch, especially among emerging market businesses as a vulnerability in the stronger dollar environment.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair