Timing & trends

There is a sense of déjà vu in the current stock market. Parabolic moves such as the current one are not that common. Yet over the past twenty years, the market is working on its third parabolic move. The refrain no doubt will be that “this time is different”. That refrain has been used repeatedly in the past to justify parabolic moves. But in the end it is the same. The market rises sharply then crashes.

The current parabolic up move has been steeper and longer than the previous two moves. The current up move got

underway from the depths of the 2008 financial crash following the bailout of some of the biggest banks in the world, slashing interest rates effectively to zero and instituting QE. While the pundits praise the recovery the reality is that growth has been narrowly based benefitting primarily the well-off (the 1%) and the professional classes while the rest of the economy has languished in unemployment, and low paying Wal-Mart type jobs or as one pundit pointed out the country has become a nation of waiters and bartenders. Growth in employment has been primarily part-time jobs with few if any benefits.

But the stock market has benefited as it did from 1995-2000 and 2002-2007 earlier periods of low interest rates and rapidly growing money supply as was the case 1995-2000 and a sea of liquidity plus low interest rates as was seen from 2002-2007. While the current run has gone on longer – 68 months to date vs. 63 months 1995-2000 and 60 months 2002-2007, the gain has thus far fallen short of 1995-2000. To date the market as represented by the S&P 500 is up 208% vs. 251% from 1995-2000 and only 105% from 2002-2007. Once again, a period of ultra-low interest rates has characterized the period along with QE 1, 2 and 3.

More important is what happened once the market stopped going up. The 2000-2002 high tech/internet bear saw the S&P 500 fall 50%. The financial crash of 2007-2009 was worse as the S&P 500 fell 58%. The 2000-2002 collapse was drawn out taking 31 months to complete. The 2007-2009 crash was all over in 17 months.

Market crashes of 50% or more don’t happen very often. Yet in the space of roughly eight years, there were two of them. In looking back over the history of the Dow Jones Industrials (DJI) there were only three others that I could find and they all happened in the early part of the previous century. From November 1903 to January 1906, a period of 44 months the DJI rose 144%. What followed was the panic of 1907 when the stock market fell 49% over a period of 22 months from January 1906 to November 1907. The granddaddy of them all was the “Roaring Twenties” bull market that got underway in October 1923 and topped out in August 1929 (actual date was September 3, 1929) a period of 70 months. The gain was 349%. What followed was the “Great Depression” crash and the DJI collapsed 89% over the next 35 months bottoming in July 1932.

The market did recover from the great crash of 1929-1932 and from July 1932 to the top in March 1937 the market was up 382% a run that actually surpassed the “Roaring Twenties”. Nonetheless it remained well off the highs of 1929. The highs of 1929 were not taken out until 1954. What followed was another devastating crash. First, there was the panic of 1937 that bottomed in March 1938 as the DJI fell 50%. The recovery over the next year was feeble and as war broke out in 1939/1940, the market started a secondary decline. The bottom didn’t come until April 1942 and by that time, the market had lost 53% from the highs of March 1937.

There have been other sharp up moves in the stock markets but few as impressive as the 1923-1929 run and the 1932-1937 run. Then again, they weren’t followed by a devastating 50% market collapse either. The 1982-1987 bull market did see the DJI gain 256% and it lasted 60 months. But the subsequent crash was merely a flash as it lasted only about two months and lost 36%.

Argumentively one could say that the up move from March 2009 has not just been straight up with few interruptions. A parabolic move never is just straight up. The correction that occurred April 2011 to October 2011 did see the DJI fall about 17%. To date that has been the only serious correction since the bull got underway in March 2009. But generally this could be considered a parabolic move or as some would call a bubble market. In a bubble market greed and euphoria is high and complacency is low. In other words “this time it’s different”.

The market pundits call it “climbing a wall of worry”. That may be right but then they don’t normally last this long. At 68 months, this bull has run almost as long as the 1923-1929 market. And everyone knows how that one ended. The current rise has also been the steepest. By comparison, the 2002-2007 bull appears as almost a gentle rise. Still the RSI indicator has not been in overbought territory as long as it was from 1995-2000. That period saw the RSI remain almost exclusively above 70 the entire time. Today’s market has seen the RSI remain above 70 longer than it did during any of the 1903-1907, 1923-1929 and 1932-1937 rises.

An overbought RSI is not the only negative sign. Currently the S&P 500 is 13.7% above the 23 month exponential MA. That is not as bad as it was in 2000 when the S&P 500 was more than 18% over the 23 month MA. But it is higher than the 10% over at the 2007 peak. Those overages are actually “pikers”. At the heights in 1906, the DJI was 41.6% over the 23 EMA. In 1929, the peak was 37.7% over and in 1937 the top was 20.6% over the 23 month EMA. By comparison, today’s market is a gentle rise.

While the US stock markets have been making new highs for the most part no one else is. European stock markets remain below their highs as does most Asian markets. The small cap Russell 2000 remains below its all-time high. Markets should be making highs together or at least confirming each other. Only the large cap US markets appear to be making weekly and daily new highs. This is a divergence that needs to be resolved.

There should also be concern about the growing spread between high yield bonds (junk) and US Treasuries. This spread has been widening of late although it is still nowhere near where it was during the 2008 financial crash nor is it at levels that should raise alarms. Nonetheless, the widening spread is to be at least noted. As the stock markets were making their highs in 2007, the yield spread between high yield and US Treasuries had already begun to widen. Once again, the stock markets are making new highs as the yield spread widens. During the 2011 correction, the yield spread widened as the market fell so the two were in tandem.

Could the stock market really take off in a blow off? The simple answer is yes it could. But it may not do that until at least a correction of some magnitude completes. It may only be a 10% pullback but as long as 1,800 holds for the S&P 500 then the market can remain in a bull mode. Even a break under 1,800 would have to be confirmed. But given the length of time that this market has been moving higher in a parabolic mode and warning signs flashing of impending danger this may not be the time to be re-loading looking for another big upside move.

It has been unusual that there has been three parabolic moves to the upside over the past twenty years. Two of them ended badly. Odds are that this one may not end so well either. The bottom of that channel is currently down around 600. That is a long way from today’s level.

Signs of The Times

“U.S. Companies are turning more to the bond market to fund expansion than at any time since 2008.”

– Bloomberg, November 4.

“Crashing Oil Prices Won’t Kill The US Economy”

– Business Insider, November 4.

“Mr. Kuroda promised to ‘drastically convert the deflationary mindset’.”

– Financial Times, November 5.

“If the ECB tries to press ahead with QE, Germany’s central bank chief will resign.”

– Telegraph, November 5.

“The Republican wave that swept over the state left Democrats at their weakest point since the 1920s.”

– National Conference of State Legislatures, November 5.

“Global Warming Community in Panic Over Republican Takeover of Senate”

– Examiner, November 7.

One can’t help but wonder how all of the apparatchiks, functionaries, intelligentsia and central planners who were dining at the public trough in Soviet Russia felt when the Berlin Wall came down in November 9, 1989.

Perspective

The US election indicates a profound change in political direction and we have frequently described Obama’s policy moves as being the regulatory equivalent of building the Berlin Wall. This was being accomplished through a mainstream media that abandoned its critical faculties and started cheerleading massive intrusions upon basic freedoms.

The towering intellects of Nancy Pelosi, Harry Reid and Obama’s teleprompter have been bypassed by the commonsense of many voters. What’s left of Obama’s term is being described as a “Lame Duck Presidency”. Yeah, a duck with the teeth and tenacity of a piranha.

Political dissatisfaction during periods of rampant inflation can turn into murderous revolutions. The two greatest examples are the French Revolution that in the 1790s turned into the Reign of Terror. And then there was the Russian Revolution and another reign of terror that began in 1917. The fall of the Berlin Wall can be described as a great reformation. Putin’s attempts to restore the Soviet can be described as a counterreformation.

Obama has no specific ideology other than the lust for power and control with the Rules For Radials being equivalent to Mao’s Little Red Book.

In just the last one hundred years there has been some dramatic setbacks to the long experiment in authoritarian government. These have turned with the end of a boom. One of the most outstanding commodity booms blew out in 1920 and collapsed. Soviet Russia turned from pure communism to sort of a socialism. In the US, John Moody explained the wonders of the 1929 boom as due to America’s turn from socialism and nationalized railroads.

The boom radiating out of Tokyo in the late 1980s fostered outstanding speculation in commodities and global real estate (remember “Trophy” items such as Pebble Beach Golf Course). As recorded by the Nikkei, the peak was at the end of December 1989 and the Wall came down in November.

The “Glorious Revolution” of 1688 occurred during a deflationary period as did the American Revolution. Both were essentially conducted by the middle classes who avoided neurotic intellectuals that prevailed during the nasty revolutions.

The White House has been overrun by anxious intellectuals and it is time for another reformation conducted by the middle classes.

Stock Markets

As we have been noting, the “oversold” of mid-October determined that the setback was a “correction”. With huge amounts of central bank promises (Japan’s was remarkable) and a very refreshing election the rebound set new highs for the senior indexes.

Last week, we listed a number of the key “plusses” that were in the market. Forgot to include that over the past few weeks financial news programs have been talking up the favourable October to May seasonal tendency.

We will stay with our list of accomplished stages:

Exuberance, Divergence and Volatility got us to the big swings into and out of October.

Resolution to excessive speculation has yet to be discovered.

We thought that Small Caps (RUT) and the STOXX were leading on the way to the “correction”. RUT set its high at 1213 in July with the Daily RSI at 70. The October low was 1040 and down to 30 on the RSI. The rebound has made it to 1186. This is at a resistance level and has reached an RSI of 70.

Recording the action in Europe, the STOXX set its high at 3325 in June with a Daily RSI at 72. The October low was 2789 with the Daily RSI down to 26. The rebound high was 3142 last week and is not overbought.

The NY Composite (NYA) set its momentum high at 11106 in July and declined to 10557 in August. The September high was 11108 and the October low was 9886 and oversold at the RSI of 28. So far the high has been 10911 and at the RSI that ended the September rally.

As noted above, inspired by a number of really good stories the stock market has enjoyed a vigorous rebound. Our work in mid-October had Springboard Buys on the S&P and JNK. It is uncertain how long this rally may last.

It is worth checking commodities and credit markets for some guidance.

Credit Markets

Lower-grade bonds have been volatile. JNK slumped into a Springboard Buy on October 14th and the rebound was sufficient to register the opposite on the following week. JNK (without the interest payment) reached the 50-Day ma and has been following it down. At 40 now, taking out the October low of 38.93 would extend the downtrend.

Out of the October hit, spreads briefly narrowed and the widening trend has resumed. The chart showing new “wides” follows.

It is worth keeping in mind that as commodities decline so does the ability to maintain prices at the retail level. This reduces general earnings power and the ability to service debt (chart follows). Then credit-rating agencies get busy with downgrades and eventually junk issues live up to the worst descriptions in their prospectuses.

Last week we thought that on the next slide in the stock market the bond future would rally. The loss of liquidity in the world’s most liquid market on October 15 was without precedent. That drove the future up five points at the opening to a price of almost 148.

The low was 140.5 on Friday and it has firmed to 141.25. The high needs to be tested and that becomes our target.

The Russian note needed to rise above 10.22% to exend the trend. It did it at 10.24% today.

Central bank recklessness reminds of hanging out with a Martini-drinking crowd some years ago. The cocktail was referred to as “Martins” or “Electric Waters”. There were certain levels of intoxication, but I can only remember the last one. You had become invisible. The reasoning was that you were doing such stupid things that it would be best to be invisible.

They called for transparency in central banking, but invisibility is too much.

Currencies

In 1980 we recall that as Reagan won some important primaries the dollar would firm up the next day. Upon taking office the DX rallied from 97 to 164. It was helped by commodities blowing out in the grandest fashion since 1920. Paul Volker had nothing to do with either event.

Reagan was one of the leaders that inspired the reform of excessive government that swept the world in the 1980s. Margaret Thatcher had a parliamentary majority and made huge advances. The equivalent by Reagan was denied by a Democratic Congress.

This time around, political change will be led by a reform-minded Congress and opposed by the Obama faction. Republicans will likely win the White House in 2016, when a massive reform can really get underway.

The dollar was expected to rally as the financial boom ran out of momentum. The DX broke out at 81 in July. After 85 was reached in September the jump to 88 was largely driven by offshore buying of US stocks and bonds. The DX has yet to have a strong rally based upon financial asset deflation.

On the near term, the DX rally reached a lofty 85 on the Weekly RSI and the index reached 88 last week. Perhaps this is the best on foreigners buying US paper.

Perhaps DX could correct some more. The next rally would likely be due to weakening asset prices and a minor start to political reform.

Precious Metals

In early September we thought that a buying opportunity would appear in the latter part of October. In the middle of that month we decided to wait for the “buy”. Our November 4th Special (Caveat Venditor) outlined how gold and silver really work during a credit cycle.

The key was that gold’s real price has been rising since what seems to be a cyclical low in June. This could be the early stages of a cyclical bull market for the real price. Improving profit margins will follow.

The November 7th ChartWorks noted that silver’s plunge had become severe enough to register a Downside Capitulation. A significant rally is pending.

The November 4th Chartworks “Gold Miners Bounce” called for that.

This and last week’s Pivot have been looking for gold stocks to begin outperforming the bullion price.

The HUI/GOLD ratio plunged from .44 in 2011 to .13 on November 4th. It has recovered a little and we would like to see some stability over a few weeks. The bear since 2011 has

been brutal and stability would provide the base for the start of a new bull market for the Precious Metals sector.

On the bigger picture, the recent collapse of HUI/GOLD seems similar to when the ratio plunged to .13 in late-November 2001. That cyclical bottom drove the Weekly RSI down to the low 20s, similar to now.

In the last two weeks of October, the HUI dropped from 185 to 146 on November 4th.

The bounce made it to 164 yesterday and the low needs a test.

Crude Oil and Recessions: Ten Years

- Note the “Peak Oil” peak in 2008.

- The current failure is becoming serious.

- Is it indicating technological revolution?

- Is it indicating global recession?

- Perhaps both.

Crude Oil and Recessions: 1970 to 2010

- Crude’s plot is rate of change.

- From 1970 until the mid-1990s there was great belief in the powers of OPEC, the erstwhile oil cartel.

- When OPEC was headed by Sheikh Yamani, it was said that he commanded all of the attention that is focused upon a cross-eyed javelin thrower at the Olympics.

Producer Price Index and Recessions: 1913 to Date

Larger Image

- The cyclical low was 168 in March 2009.

- The high for the move was set in April at 208.3.

- A double top was set at 208.3 in June.

- The latest posting is September’s at 206.5.

S&P Earnings and Commodities

Larger Image – Source: Yardeni.com

- This year’s high for the CRB was set in June at 313.

- The low for the year was set last week at 266.

- According to the chart, earnings should follow.

Credit Spreads: Now Worse Than On October 17th

Larger Image

- On the near-term, rising above 171 bps set on October 17th would extend the trend.

- This was accomplished on November 7th.

- It is now at 173 bps and stair-stepping up.

- Widening has taken out resistance at the March “high”.

The above is part of Pivotal Events that was published for our subscribers November 13, 2014.

Gold and silver prices have been trading in declining wedge patterns since 2011. Crude has traded in a flat to down wedge pattern for five years, and the S&P has been moving inexorably higher since early 2009 in a contracting wedge.

There are signs of a trend change. Examine the log scale weekly charts below.

….click HERE for larger Charts & more commentary

Summary

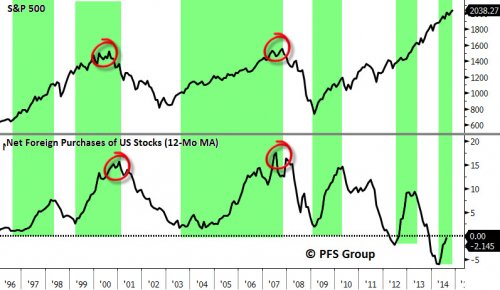

- Net foreign purchases of US stocks turning up

- Corporate buybacks also acting as a support for the market

- Large potential short squeeze to serve as another bid

- Taken collectively, still too soon to turn bearish

It’s always a good idea to periodically take a look at what the foreign community is doing in terms of net US equity purchases. The reason lies in the fact that they tend to buy at tops and sell at bottoms and can serve as a contrary indicator. We saw this not only in the 2000 and 2007 bull market peaks but also the 2003 and 2009 bear market bottoms.

So what do current levels of foreign purchases suggest for US stocks? They reflect more of a bottom than a top as net foreign purchases are coming off of multi-decade lows set earlier in the year and are close to moving into positive territory. Shown below is the S&P 500 on the top panel and the 1-year moving average of net foreign purchases on the bottom and you can clearly see that rising foreign purchases are associated with bullish moves in the stock market. Given the low level of current purchases we could continue to see an influx of foreign buying of US equities in the weeks and months ahead.

Source: Bloomberg

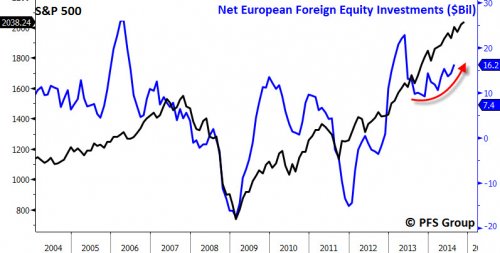

Part of the foreign inflows into US stocks is likely coming from Europe given the malaise of the region and the poor economic growth. Typically increases in net foreign stock purchases by the Eurozone translate into higher stock prices in the US with 2013 as a perfect example. Heading into 2013 net foreign equity purchases by the Eurozone were slowly declining but then surged strongly to nearly $25B a month by early summer before moderating back down to roughly $10B a month. Currently, European purchases of foreign stocks have picked and are likely serving a bid to our markets.

Source: Bloomberg

The market rally off the October bottoms has had a defensive feel to it as high quality stocks are outperforming low quality names. Foreigners typically buy large-cap strong balance sheet companies and so the outperformance of high quality stocks over low quality is likely an indicator of an increase of foreign inflows rather than a peak in the stock market often associated when lower quality names underperform.

Another widely known support for the markets currently as well is corporate buybacks, which, ironically, was also partially attributed for the October correction:

Is This the Beginning of a New Bear Market? Important Signs to Watch

Most corporations are precluded from buying back their shares during the five weeks before their earnings release and so the month before the onset of earnings releases typically show the lowest percentage of share buybacks seasonally. Peak earnings releases for the S&P 500 will be between October 13th and October 31st, which is significant as four to five weeks prior the S&P 500 peaked as a major buying source of the market dried up. Near the end of this month roughly 75% of the S&P 500 companies will have reported and will be able to restart their share buyback programs. According to Goldman Sachs data going back to 2007, roughly 25% of annual share repurchases occur in the last two months of the year with November being the largest month (14% of total annual share repurchases). This indicates corporations may be a significant marginal buyer of the stock market beginning in the next few weeks.

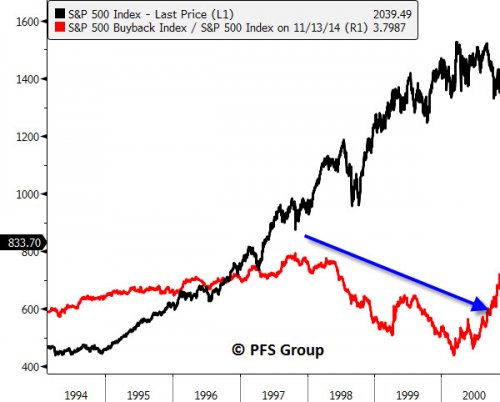

As mentioned in the excerpt above, according to Goldman Sachs roughly 25% of total annual share repurchases occur in the last two months of the year and suggests there is plenty of support for this market into year end. Tracking buybacks can be very helpful in identifying major market turning points since investors tend to sell stocks when the company is buying back their equities at rich valuations and then underperform the general stock market.

Because of this, tracking the relative performance of the S&P 500 Buyback Index to the S&P 500 can provide an early clue of an impending major market top. This was the case leading up to the 2000 bull market top in which companies with large buyback programs began to be penalized by investors beginning in 1997 as the S&P 500 Buyback Index underperformed the S&P 500 by a large degree in the last few years of the 1990s.

Source: Bloomberg

A similar situation was seen in 2007 when the market shot higher heading into the summer but the S&P 500 Buyback Index stopped outperforming the S&P 500 and then virtually collapsed in the last six months of the year as investors took companies to task for wasting shareholder money by buying back overly priced stocks.

Source: Bloomberg

When you look at the market today you do not see any of the glaring divergences above that were associated with the 2000 or 2007 tops and suggests we haven’t reached the peak of this bull market.

Source: Bloomberg

Another development to keep in mind is that short interest on the New York Stock Exchange is at levels that nearly match the March 2009 bottom and have eclipsed the levels that marked the 2010, 2011, and 2012 bottoms. As I’ve said before, the time to be bearish is when everyone is bullish – short interest levels do not convey this message at all.

Source: Bloomberg

There are some sentiment surveys that show elevated bullishness but I tend to put more value on data that follows what people are doing rather than what they are saying; actions speak louder than words and short interest levels are providing a bullish contrary signal.

Summary

The trends in net foreign purchases and the outperformance of the S&P 500 Buyback index suggests a major market top is not in the offing as neither are signaling a market peak as they did at the 2000 and 2007 tops. Additionally, the large net short interest levels on the New York Stock Exchange suggests a significant chance of a short covering rally that could lift the markets higher. Collectively, the data above cautions against turning overly bearish on the markets despite the strong run off the October lows. There still remains plenty of support underneath this market to carry it higher in the weeks and months ahead.

“we believe that stocks have been so beaten up that they are attractively priced with “ten bag” potential” – (Recommendations below MT-Ed)

Winter is coming. Drilling deeper into the record market levels, the US is unlikely to fully escape the global headwinds. Namely, in the past six months, the world’s major currencies have fallen more than ten percent against the dollar in a stealth currency war driven by expectations of higher rates in a race to the basement. Increasing anxiety is that the decline is reminiscent of the Depression era currency war when each country sought a competitive advantage in a period of slow growth. The recent tumble in financial markets also reignited fears about Europe and the chronic structural problems left over from the eurozone debt collapse. Twenty-five banks failed the so-called European Stress Test last year.

Geopolitical shocks in Ukraine and the Middle East have exacerbated the decline in currencies in a catastrophic chain of events. German industrial output suffered its biggest drop in five years, adding to a string of bad news. Italy’s position has worsened over the years with the ratio of Italian public sector debt to GDP increasing 150 percent according to Eurostat, a level where problems previously arose.

Russia has become the pariah of the world. The ruble has dropped to the lowest ever and $75 billion has left the country since yearend. Inflation has climbed aggravated by the self-imposed ban in western food imports. Interest rates are double digit and falling oil prices revived fears of a full blown currency crisis on the scale of 1998 or 2008. More significantly Western capital markets are closed to Russian firms which will need to repay $52 billion over the next six months, a tall order since over half of the country’s revenues is dependent on energy. Russia’s isolation is not temporary and the Western banks’ exposure, in particular Europeans have not yet dealt with this change. Markets are vulnerable to a big surprise. Winter is coming.

Quantitative Easing is Over… Long Live Quantitative Easing!

Central bankers are supposed to be stewards of our currency which is why pronouncements are watched for

hints over the course of the economy or when interest rates will change. What is clear, however is that central banks are all about creating money using financial engineering. After five years the world is awash with some $70 trillion, led by the Federal Reserve’s balance sheet that has ballooned to a record $5 trillion which represents a liability for the state. Money is a commodity whose creator is the state. Central bankers also control the money supply, which has grown in importance as the size of government deficits increase. This money has to go somewhere. A major beneficiary of course has been the Wall Street banks who benefited from near zero interest rates allowing them to take advantage of the “free money”, for arbing, leveraging and placing big bets on the casino-like markets, fueling bond and stock market bubbles. But now with the termination of quantitative easing, markets are worried as to what is next. Volatility is back and bubbles always burst.

Central bankers are caught in a “liquidity trap” of their own making. After printing more of the world’s reserve currency to pay for three rounds of bond buying over 37 consecutive months, this printed money no longer has any effect, sort of like “pushing on string”. Part of the reason is that the central bankers’ surrogates, Wall Street and “City” bankers are sitting on trillions of reserves due to new capital rules (“living will cash reserves”). The ECB, Bank of Japan and Peoples’ Bank of China are key participants in a currency re-alignment, the consequence of helicopter money and serial quantitative easing programs.

Stealth Currency Wars

And still despite a decade of zero growth, Japan has unveiled another round of money printing causing the yen to fall to an seven year low. The euro has fallen 10 percent against the dollar. China’s renminbi has slipped after nine years of appreciation against the dollar. Simply after exhausting their money printing ways , currency wars have become the central banks’ “policy du jour” in order to give their economies a boost allowing them to postpone needed structural reforms. As a percentage of GDP, G7 debt has exploded to 120 percent of GDP from 81 percent in 2007. Over the same period, US debt soared 90 percent to over 100 percent of GDP excluding unfunded liabilities. Despite the trillions created, global debt levels have increased almost four times GDP while GDP has not grown suggesting there are structural reasons for the deceleration in growth. The world has simply become more leveraged, while debt has grown to unsustainable levels. Currency-market volatility will spill over into other markets. Gold will be a good thing to have.

Currency manipulation is reminiscent of the mercantilist age of “beggar thy neighbour” currency protectionism. Then, the supply of currency was controlled by a cartel of central banks and exchange rates were manipulated for trade advantage. And today, the US Treasury has criticized its trading partners and allies like Germany and Japan over their exchange rate policies. A stealth currency war has heated up and America has become the target since global currencies float around the dollar whose value was set free by Nixon in 1973. Yet America’s creditors like China have built up $4 trillion of reserves and those creditors are looking for alternatives to the outdated dollar reserve currency regime. During the Asian crisis, China was burnt and this time instead of recycling their dollar hoard they are buying dollar denominated assets, such as real estate, companies, and gold. The dollar’s strength is not only temporary but illusory.

Debt Trap

With the debt overhang, there is growing concerning that growth is not enough. President Obama has out-Cartered Jimmy Carter, the last ineffectual leader whose approval sank to stubborn lows while still in office. And the Democrats’ loss of the Senate promises two years of dysfunctional government . This “hope” leader has a record of promising more than he can deliver and is now viewed as a liability with his cerebral approach to world problems failing. And after repeated red lines being drawn, he has reluctantly gone to war after a premature exit contributed substantially to the conditions that have forced him to return again. The larger question, will this war define his presidency as did Bush, particularly when the piggy bank is empty. Understandably, the Middle East’s rich powers and Asia should support the cause but Mr. Obama has antagonized those allies. In a term and half, America and Mr. Obama have been left isolated operating a wholly reckless financial system. This is unsustainable. As debt rises, investors will take flight, central bankers will weaken and – sooner rather than later – the dollar will collapse, joining the currency war.

To be sure, Europe’s outlook is also weak and getting weaker amidst rising tensions among its key members over Eurozone rules. Unlike Japan who owes much of its debt to itself, America owes more than half of its debt to foreigners. America’s borrowing binge has left some of its big creditors exposed and is not only too big to fail, but too big to bailout.

The World Order Has Changed

Europe and America seem to be unsuccessfully protecting the old world economic system or order. The European Union is threatened from internal divisions and the fact they are not tied together financially. The Middle East is divided along secular lines. The United States seems to leading from behind destined to two more years of legislative dysfunction. And within this power vacuum, the East has emerged from a regional power to a powerhouse with China’s emergence changing economic fortunes and shifting economic realities. The various orders are plotting divergent courses.

“Every battle is won before it is ever fought”. Sun Tzu’s Art of War written in the sixth century is an excellent primer on eastern strategy with application to wars, business and economics. Sun Tzu says, “know that to fight and conquer in all your battles is not supreme excellence”. It is better to conquer without fighting or destroying your enemy. To win, it is best to take over your enemy (or institution) than to destroy them.

China is flexing its economic muscle by becoming a net exporter of capital allowing them to become more assertive as an economic superpower, laying the foundations for a Sino-centric financial system. We’ve seen it before. America replaced British dominance in the late 18th century and America’s power and dollar has reigned for much of this century.

Sino-Centric Financial System?

Alibaba, Lenova and Industrial and Commercial Bank of China (ICBC) are now part of the West’s daily life. The Shanghai Gold Exchange (SGE) rivals Comex with trades settled in renminbi. We believe these moves are part of the internationalization of the renminbi, the natural competitor to the dollar. Another significant step is the currency swap agreements with the Bank of England and the European Central Bank.We believe China’s grand strategy is long term. A new global currency would allow China to circumvent Western dominated institutions. China is sitting on a massive hoard of dollars and needs not takeover the West. China only has to establish the financial entities and internationalize the renminbi (RMB), to grow and challenge the Western dollar-centric financial system.

A major plank is the establishment of the renminbi as a major international currency. The opening of the Shanghai-Hong Kong Stock Connect will give all foreign investors access to the Chinese market while also permitting mainland investors to buy Hong Kong listed stocks. Currently some dual listed Chinese shares trade at a whopping discount of 30 percent to the shares in Hong Kong and under the program, the link will arb this discount. Longer term, the China Securities Regulatory Commissions and Hong Kong are converging, opening the door to China’s equity market and liberalizing its capital markets.

Another plank is the establishment of multi-lateral institutions like the Asian Infrastructure Bank, which offer financing for badly needed infrastructure. The creation of an Asian Infrastructure Investment Bank rivals the World Bank. The post-economic world order has changed. The US government’s Export Import Bank has extended loans and guarantees of $590 billion over its 80 year history. By comparison, Chinese institutions in only two years have provided some $670 billion according to Fred Hochberg, Chairman of EXIM Bank. China wants a seat at the table.

The country has also set up renminbi hubs to clear and settle transactions in London, Frankfurt, Seoul, Hong Kong, Singapore and now Canada.

Gold’s Role in The Sino-Financial System

Meantime, America’s debt load is its Achilles heel. China is poised to take advantage of this. The foundations for a Sino-centric financial system have been laid with gold a major part of it. We believe resource dependant China has taken a page from Sun Tzu’s book, using its diplomatic and economic muscle to regain superpower status. China once reigned the world during the early fifteenth century when the Ming Dynasty sailed ships around the world, a whole century before Europeans found America. China consumes most of the world’s resources and sits on the largest cash reserves. Yet, the dollar and lack of global institutions limits its influence. That is changing.

China is the largest consumer of gold and producer of gold, buying most of the world’s gold. We believe building up its gold reserves would be a major step since the move would hedge China’s massive $4 trillion dollar stockpile and importantly solidify the renminbi’s role as one of the world’s reserve currencies. In one week alone, withdrawals from the Shanghai Gold Exchange spiked a whopping 68.4 tonnes. The Shanghai Gold Exchange is one of China’s source for physical bullion. China owns $1.3 trillion of US public debt. To date, China has been patient allowing America to spend more than it produces but how much longer will allow it to debase its currency and debts.

For China, gold is a hedge against a depreciating dollar and negative real interest rates. China knows that paper currencies can be debased and centuries ago, gold retained its value over paper currencies. Asia is awash with dollars. China has more dollars than they want. In addition, with central banks loaded with American sovereign debt, the notion that America can grow its way out of debt has lost credibility particular when the very same arguments in Europe ended in failure. Greece just paid nine percent for debt. Paul Krugman aside, history shows that the reliance on debt to boost consumption doesn’t work. America is just another example of the age old phenomenon in which debt increases due to a credit binge and its spending and quantitative easing has left debt piled on more debt. This is unsustainable. Still markets post daily highs and we are told that all is well. The inflection point, we believe has arrived when creditors worried about the greenback will rush for the exits. It is not so different this time.

The World Gold Council with the China Gold Association recently co-sponsored the first ever China Gold Congress in Beijing. At the conference it was reported that Chinese demand has been growing at almost 2,200 tonnes of gold in 2013, more than previously disclosed. China National Gold, the largest gold producer in China was co-sponsor of the Gold Conference and its president, Mr. Song Xin, endorsed full convertibility of the renminbi with gold as a major step to establishing the renminbi as a reserve currency. Mr. Song also said that accumulation of gold was in the national interest. Backing its currency with gold would accelerate that move.

China’s gold reserves were last reported in 2008 at 1,054 tonnes. This accounts for less than 2 percent of China’s massive $4 trillion of foreign exchange reserves. But where to store its gold? China has been building vault space to replace Western vaults in Switzerland, London and Fort Knox. Rather than depend on the West, China has opened up vaults in Shanghai, with storage capacity of 2,000 metric tons of gold. Recently, China announced plans to open a vault across from Hong Kong in Shenzhen with a storage capacity of 1,900 metric tons. Unlike Germany who must wait seven years to repatriate its gold from the vaults in Britain and the United States, China has been building its own vault space.

Recommendations

Recommendations

We believe the end of QE III (at last), the stealth currency war and China’s insatiable appetite for gold will revive interest in gold.’ The end of Obama’s QE programs and transition is unknown which is why the market players have headed for the exits. To be sure, higher rates and more uncertainty will follow.’ In this situation, we continue to believe gold will rally over $2,000 an ounce as investors seek its store of value. Currently, gold is very oversold having broken down from a year trading range. Meantime, the US dollar is technically overbought and vulnerable in the midst of a currency war. Russia continues to be a buyer of gold, holding 1,150 tonnes, up 72 percent making it the world’s sixth largest gold holder. Nineteen central banks bought gold last year. We believe that higher gold prices are in the offing based on the fundamentals including Chinese buying, a fiat US dollar and resultant spiraling currency war. Ironically, while the Western central bankers shed gold as an archaic metal that pays no interest and holds no use in today’s modern day economic order, China is steadily accumulating gold. China and gold have a long history, much longer than fiat currencies like the US dollar.

Gold prices fell 42 percent to a 4 ½ year low, crushing demand for gold stocks. The entire market cap of the TSX gold index is less than $100 billion or one third of Alibaba. Over a third of the industry is losing money today as they face pressure from declining prices. A split has occurred among the world’s largest gold miners with two tiers developing. One tier has those miners with low cost gold operations and the other tier comprises producers plagued with the legacy of overvalued acquisitions and high cost operations. In a race for growth, many expanded output at high cost and now find themselves losing money on every ounce of gold produced.

The latest round of quarterly earnings reflected this split with Barrick showing a major improvement but well-loved Goldcorp recording disappointing losses due to production problems at Penasquito and flagship Red Lake. Industry mining costs are still “out of control” and grades have deteriorated. Yamana shocked the street with a billion dollar write-down which was long overdue for its Latin American assets. Nonetheless, with many of the world’s largest producers trading at decade lows, we believe that stocks have been so beaten up that they are attractively priced with “ten bag” potential. Companies with low costs and a rising production profile are favoured such as Barrick Gold, Agnico Eagle Mines and Eldorado Gold. We would take profits on Goldcorp and Newmont, avoiding Kinross, Yamana and IAMGold, because those companies still have unresolved problems and further write-downs are expected.

Agnico-Eagle Mines

Agnico posted a solid quarter but earnings showed the difficulty of low commodity prices.

Production guidance was increased to 1.4 million ounces due to the acquisition of Canadian Malartic. Next year, Agnico is expected to produce 1.6 million ounces. The loss in the quarter was attributable to lower commodity prices and increased exploration spending. Agnico also closed the Cayden acquisition which is a prospect in Mexico and shareholder approval is expected by year end. Agnico has a stable of potential producers with the Amaruq maiden resource near Meadowbank expected next year. We like the shares here.

Allied Nevada Gold

Nevada-based Allied reported a big loss, due to a charge on the heap leach pile. Allied’s open-pit Hycroft mine produced only 50,000 ounces and half million ounces of silver in the latest quarter.

Working capital has declined. The Company unveiled a revised feasibility study to expand Hycroft costing $1.7 billion to process the huge sulphide resource. Allied has a huge debt load and will need a joint venture partner or a higher gold price to put the Hycroft expansion into production.

Barrick Gold Corp.

Barrick posted the best results of its peers, beating Street estimates. The results were due to a turnaround at African Barrick as well as the lowering of all in costs to $880 an ounce. Guidance was maintained between 6.1 million and 6.4 million ounces as operations were stabilized. Pascua Lama remains under “care and maintenance” with rumours that the Chinese have been invited on a joint-venture basis. Barrick is focusing on their core areas in Nevada with Cortez, Gold Rush and Turoquoise Ridge. John Thornton also upgraded its management ranks and the company is leaner and moving in the right direction. Barrick has the largest in situ reserves in the world. We like the shares here.

Detour Gold Corporation

Detour Gold reported a loss but produced 115,000 ounces in the quarter from its flagship Detour Lake Mine in northeastern Ontario. Mill throughput was lower than design capacity of 55,000 tonnes per day, which was 14 percent lower than targeted levels due to unplanned downtime.

The shortfall resulted in a loss, but the Company reaffirmed guidance for this year. Detour has a 15.5 million ounce resource. Average mine output will be down and production will meet the lower part of its guidance. We expect Detour to produce 460,000 ounces this year and 540,000 ounces next year. Cash is at almost $140 million. We like the shares down here, but Detour will need another few quarters to get up to design capacity.

Eldorado Gold Corp

Eldorado reported decent results in the quarter producing 196,000 ounces, a 20 percent increase over a year ago with all-in costs at $786 per ounce. Eldorado is a low cost operator with mining, development and explorations operations in Turkey, Greece, China, Romania and Brazil. The Company has a first rate balance sheet with almost a billion dollars’ worth of liquidity. Gold production was almost 200,000 ounces with higher production from Efemcukuro in Turkey due to improving mill throughput and grade. Cash operating costs were also lower in the quarter.

Eldorado’s Chinese Jinfeng and White Mountain performed well but the Company is still waiting for approval for Eastern Dragon from the government. Eastern Dragon is currently under care and maintenance and permitting is still on-going. Eldorado hopes for approval but this project has been delayed for some time raising speculation that Eldorado may sell Eastern Dragon or its Chinese operation. Eldorado has a growing development pipeline and the Company is known for its execution capabilities.. We like Eldorado here.

Goldcorp Inc.

Despite flat output, Goldcorp reported a loss of $44 million due to chronic problems at Penasquito mine which was hit with a $36 million writedown on its low grade stockpiles. Gold production was 651,700 ounces. Penasquito produced 129,000 ounces at an all in cost of $1,142 per ounce. Water remains a problem and won’t be solved until later but the poor results overshadowed pouring the first gold bar from Eleonore in Quebec. Cerro Negro in Argentina will be in commercial production in the quarter at a cost of $1.7 billion. Nonetheless a review of Goldcorp’s results shows that not only has Penasquito underperformed but flagship Red Lake had a disappointing quarter. Goldcorp threw in the towel and withdrew the EIA for El Morro in Chile. Goldcorp, one time was a high flier and priced to perfection however with the recent disappointing results, we believe that there is downside here.

Kinross Gold Corp.

Kinross reported a loss despite a good operating quarter. Kinross salvaged something from high grade Fruta Del Norte project in Ecuador through the sale of the project to Lundin Gold for $240 million. The project was stalled over negotiations with the government. Meantime, Kinross has not yet shelved problem-prone Tasiast gold project looking to finance this $1.6 billion project.

We believe the project does not make sense here. In addition, Kinross’ heavy exposure to Russia remains an overhang despite that Kupol is performing well. Kupol produced a record 195,000 ounces but Kinross’ exposure to Russia makes investment risky at this time. We would avoid the shares here.

New Gold Inc.

Intermediate producer, New Gold reported a good quarter, producing almost 94,000 ounces at an all in cost of less than $850 an ounce. New Gold has four producing mines and three development plays. Guidance was maintained and the fourth quarter should be New Gold’s strongest with contributions from New Afton and Peak Mines. Peak Mines’ grade improved which helped the quarter. New Gold has cash and cash equivalents of almost $400 million and the Company also has a $300 million revolving credit facility. New Gold is expanding New Afton and continues work at Rainy River which is a mammoth project awaiting improved capital markets. Both Blackwater and Rainy projects are huge and thus suitable for the next bull market.

Newmont Mining Corporation

Denver based Newmont reported lower earnings and production declined due to lower output at Carlin and Twin Creeks. Australian volumes were also down with copper output hit by the shutdown of Batu Hijau in Indonesia. Despite reserves of 88.4 million ounces, Newmont has very little on the horizon, except the new Merian mine in Suriname, which is a big low grade project. Newmont is also spending money at the Turf Vent Shaft in Nevada, Phoenix Copper Leach, Vista Vein and Yannacocha but near term the outlook is mediocre with the company in “harvest mode”. Production will be flat with all in cost about $1,050 per ounce. Newmont has $1.8 billion of cash on its balance sheet however. A merger with Barrick still makes sense.

Yamana Gold Inc.

Yamana produce 1.2 million gold equivalent ounces last year. Yamana had a rough quarter, taking a $1 billion writedown on C1, Santa Luz and Ernesto/Pau-a-pique. The poor results were largely due to an accounting charge as these assets are for sale. Dividends were also reduced.

Lower commodity prices also hurt results. Yamana is focusing on its “cornerstone assets” which include newly acquired Canadian Malartic and El Penon in Chile. Yamana financed Canadian Malartic with debt and it is this debt overhang that is causing Yamana’s shares to lag the market.

Sell.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair