Timing & trends

“The inflation is in junk bonds”

“Bond buyers have never paid so little to lend to the riskiest junk-rated companies, yet they’re gobbling up the debt at an accelerating rate.”

– Bloomberg, May 6

“Investors hungry for high yielding bonds are turning to one of the riskiest corners of the US corporate debt market.”

– Financial Times, May 9

“Continue to overweight high yield bonds.”

– BCA [Bank Credit Analyst], May 13

“In the leveraged loan market, strength has returned, in part because buyers are using more leverage. We do not expect any downside from the trend in 2014.”

– Barclays, May 16

“US industrial output posts biggest drop in more than 1-1/2 years”

– Reuters, May 15

“China’s bad loans rose for the 10th straight quarter to the highest level in more than five years.”

– Bloomberg, May 15

* * * * *

It seems that the best for the bull market that arose as the panic ended in the spring of 2009 is in. That bottom was accompanied by very bearish technical readings. Actually, numbers seen at cyclical bottoms. Spreads between high-grade and low-grade bonds were at panic “wides”.

February-March recorded the maximum celebration of this bull market. This accomplished the most outstanding sentiment and momentum numbers since 2007.

We noted that these only register at cyclical peaks. Credit spreads have narrowed, exceptionally.

Leadership as provided by the NDX peaked in early March and on the slump into April took out key support. The rebound to last week was the key test of the high and is now rolling over.

This leadership burned itself out.

Noteworthy, is that the banks (BKX) also peaked in March and have been acting worse than the NDX since. New lows were set this week.

The action in the S&P continued to last week. Perhaps the shift from “growth” to “value” had some influence. The shift is typical of this stage of a stock market. Ross used it as an indicator.

Tuesday’s decline was explained as weakness ahead of some Fed minutes.

For us, it was that spreads (JNK:TLT) broke down as the Greek bond jumped in yield – last Thursday.

There was some relief until Monday when spreads were again weak and the Spanish bond accomplished new highs in yield.

The cyclical bottom in 2009 was accompanied by dismal technical readings and was followed by a cyclical bull market. It stands to reason the that cyclically bullish readings would be followed by a cyclical bear.

This melancholy condition is becoming evident this week and prompts the question “How bad will it be?”.

We have long described conditions as the first business cycle and bull market out of a classic crash. Similar to the one that peaked in 1937, it was preceded and accompanied by massive policy intrusions. Zero short rates and lots of bond buying.

The other part of our position has been that economic and business numbers would be positive until the stock market peaked. As with the 2007 Bubble, the recession would start virtually with the bear market.

The old normal was that the stock market would lead the economy by some 12 months.

That was the case with the Dot-Com Bubble of 2000. If the recession starts with the bear, then the trading community will not have to suffer economists going on about how good things are as the senior indexes decline.

Back to how bad?

The inflation in central bank credit is without precedent. This official speculation has been allowed because of the massive speculation by private investors. It is worth recalling that the Fed became aggressive with the Bear Stearns failure in June 2007. Then even more ambitious as the contraction became more evident in 2008. Extraordinary easing did not prevent a classic crash.

Unwitting taxpayers and witting speculators and investors sponsored the Fed’s reckless adventure. And the latter groups have created a cyclical peak in both stock and bond markets.

Bear markets are always ugly, and the developing one will put policymakers in a very bad light.

The speech to the CMRE Spring Dinner includes the comment that the Fed was formed with the earnest belief that it would prevent the financial setbacks that initiate recessions.

The next one will be number 19. Of course, this has not been good for the resume. But not preventing two Classic Bubbles and Crashes has been a real clanger.

We have noted that the decline in yield for the Spanish bond had generated four weeks of Downside Exhaustion readings. This has been our proxy for the general Euro bond market. And the action was extreme going into the time-window when reversals can happen.

The low was 2.84% on May 14th and key resistance was at 3.11%, which was taken out with the surge to 3.14% last week.

Also last week, in a rush to join the action, the Italian bond registered a Weekly Downside Exhaustion. The yield has plunged from 7.08% reached in the 2011 Panic to 2.90% on May 14th. The rebound reached 3.28%, taking out key resistance at 3.20%.

The Greek bond set its best at 5.85% on April 8th and had fully reversed on May 16 at 6.86% yield.

The Spanish (our proxy for the sector), the Greek and Italian bonds represent different characteristics of the European Sovereign Debt Market. They all enjoyed outstanding and measurable dynamics going into the window when major reversals can happen.

The reversal has been accomplished and it will take some time to unwind the excesses.

Keep in mind that the action has had full government participation and that was the case going into a similar reversal in May-June of 1998 – the LTCM collapse.

This was mentioned last May and while most bond prices got whacked, spreads did not widen. Treasuries dropped with the market. The full five-year cycle had to run.

This time the excesses have been greater in lower-grades than in treasuries. On the latter our target of 136 to 138 has been reached, but the rise is not overbought on the Weekly.

As the above headlines indicate the action is mainly in the hands of highly-leveraged fund managers. Also there are stories that retail buying of junk funds has ended. But in recalling when the “odd-lotter” was a key technical measure in stock market research.

The odd-lotter was a small trader and considered as uninformed. However, as we recall he did get the market right – at important tops.

Who knows if it is still applicable but it is fun to mention some of the old tools.

As credit conditions deteriorate we expect that the investment demand for gold will increase. This would likely be accompanied by silver underperforming gold, which is an indicator of developing trouble.

This was signaled when the gold/silver ratio rose through 66 in April. The high was 67.7 at the end of April and today it is at 66.6.

Our conclusion last week was that the developing rise in gold would again make the world safe for fundamental supply/demand research. The next phase of the post-bubble contraction may not be safe for fundamental research on silver.

Every long post-bubble contraction has moved the gold/silver ratio up. This Pivot is being written in NYC and the files are not handy, but on the contraction into the 1840s the ratio rose to around 35.

Then there was the great Silver Corner attempt by the Hunt Brothers that blew out in January 1980. The ratio declined to 16, which was considered its natural level.

On that post-commodity bubble financial disaster the ratio soared to a little over 100 in December 1990 when Citi and Chase Manhattan became insolvent.

With the 2000 Bubble it declined to 42 and it rose to 83 with the subsequent collapse.

In the 2007 Classic Bubble the ratio declined to 46 and increased to 93 with the bust.

The decline in the ratio with the 2011 blow-off in precious metals was the most sensational since January 1980. We noted that the action had become “dangerous”.

Using history as a guide, the gold/silver ratio could increase to around 90 on the developing contraction.

Most gold and silver stocks could decline with global financial troubles.

- BCA’s advice on May 13 was “Continue to overweight high yield bonds”.

- Yields and the default rate are close to a cyclical minimum.

- Hedge funds are long and leveraged.

- The move from terror and panic to bliss and confidence has taken four years.

- This is the first such extreme reading in 10 years.

- Buying is compulsive.

- There are no concerns about adversity

- The rally from a little less than 56 in February to 64.12 has been outstanding.

- The action had big momentum and is running out of steam.

- The high on this issue was 99.33, back in the halcyon days of the housing mania.

- The low was 23.10 (no typo) in 2009.

- Note the reversal to widening spreads in May-June 2007.

- Our conclusions in June of that fateful year was that “The greatest train wreck in

- the history of credit” had started.

- Another run-a-way train is thundering down the track and is out of control.

- These have a tendency to be discovered in the May-June slot.

My daughters are getting older. One will be entering the third grade this fall and another — gulp! — is going into middle school. But I will always cherish the memories of when they were little, including reading to them before bed.

One of my favorite stories was called “The Napping House.” The basic plot? A bunch of human and animal characters are snoozing and snoring away, blissfully unaware of any possible threats or disturbances. Then a tiny flea decides to bite a mouse — and everything goes to heck in a handbasket!

I thought of that story this week for a simple reason: It’s investors who are snoozing right now. Bond investors. Stock investors. Foreign exchange and commodities traders. They’ve all been lulled into the deepest snooze I’ve ever seen.

You can see this by looking at measures of market volatility. Take the Chicago Board Options Exchange SPX Volatility Index, or “VIX” for short. It’s a measure of investor complacency and calm, as measured by the options market. The lower the VIX falls, the less risk of large swings (especially downside ones) that investors are pricing in.

Take a look at this monthly chart of the VIX and you’ll notice something. We’re trading around 11-12. That’s roughly half the long-term historical average, and at levels that signal maximum complacency.

The last time we saw anything like this? Late 2006-early 2007 … right before the housing, credit and stock markets began to collapse and volatility began to explode.

It’s not just stock traders who are dozing on the job, either. Volatility has collapsed in virtually every capital market on the planet.

Just look at the “MOVE” Index, which tracks Treasury bond market volatility. It has sunk all the way to around 55. We’ve only seen bond volatility fall to levels this low three other times in the 26-year history of the index:

Mid-1998 … right before the gun-slinging hedge fund Long-Term Capital Management collapsed. That forced the Federal Reserve to convene a meeting of all the major brokerage firms in New York City in order to arrange a multi-billion-dollar bailout. At the time, it was the biggest such bailout ever!

Mid-2007 … right before the credit market began to collapse. That implosion ultimately required hundreds of billions of dollars in bailouts for companies like AIG, Bear Stearns, Fannie Mae, Freddie Mac, Citigroup, and Bank of America — bailouts that made the LTCM collapse look like child’s play!

Mid-2013 … right before the first, massive “Taper Tantrum” that led to the biggest bond market rout in several years.

For investors like you, this lack of volatility has a couple of important implications:

First, it’s a key reason why CEOs, CFOs, and other officials from major bank and brokerage firms likeCitigroup (C), JPMorgan Chase (JPM), and Goldman Sachs Group (GS) have warned that trading revenue will continue to suffer. After all, as the Wall Street Journal noted on Tuesday, no volatility = much weaker profits. I continue to recommend you steer away from investing in most of these institutions as a result, and would note that they’re all underperforming the market.

Second, it’s a potential “yellow flag” for the markets overall. I’ve been helping my Safe Moneysubscribers generate nice gains from this low-volume, low-volatility rally. And I still like many of the sub-sectors they’re invested in, from domestic energy to aerospace.

If you’re one of them, great. I’ll have more on your positions in your next monthly issue, due out next week. If you’re not on board yet, but would like to join, all you have to do is click here.

But in light of the collapse in volatility, I’ve started harvesting gains on positions that have run up quite a bit. I’ve also gotten more selective in adding new equity exposure. Because just like the characters in “The Napping House,” many investors out there are acting like there are no potential “fleas” at all … something that makes the contrarian in me increasingly nervous and wary of hidden threats.

Until next time,

Mike

It’s not just the political system that’s rigged…

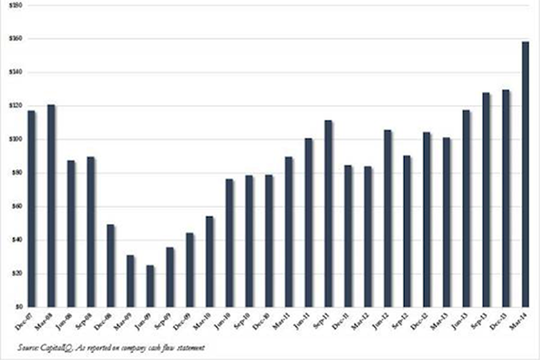

The biggest buyer of US stock in the first quarter of 2014 wasn’t pension funds… or mutual funds… or hedge funds… or banks… or poor old Mom & Pop.

No… The biggest buyers of US stocks between January and March of this year were S&P 500 companies. In total, they bought back $160 billion of their own stock.

Ed Note: Bottom Dates are from Dec 2007 thru Mar 2014, far right bar is at $160 Billion

What’s that you say? Stocks are expensive right now? Isn’t the point of buying stocks to get in at a low price and sell at a high price?

Well, you’d be right. Unless you were an S&P 500 company with access to the Fed’s zero-interest credit.

Want to buy back stocks at peak prices? No problem. All you need is to take on new debt at near-zero interest rates and shovel that money into stock buybacks.

Then through the magic of supply and demand, whatever outstanding stock you leave in the market will be worth more. Because now there’ll be less supply to meet demand. And prices will go up.

It’s been a popular way of goosing the market. Going back to 2012, total corporate debt issuance has been about $32 billion. And total stock buybacks have totaled $34 billion.

Aren’t companies supposed to invest in the growth of their businesses? Isn’t EPS (earnings per share) growth supposed to come from more “E,” not less “S”?

Not in a topsy-turvy world…

Take IBM, for example. In Q1, 2014, Big Blue spent $8 billion on share buybacks and $1 billion on capital expenditure (stuff like upgrading buildings and equipment).

But the biggest splurge by US companies on their own stock didn’t come in in 2014.

Looking at stock buybacks over the preceding 12-month period, that honor goes to 2007, when corporations bought $560 billion of their own stock back.

And you know what happened next…

P.S. If you are concerned about a peak in stocks… and another crash… you’ll want to read Bonner & Partners senior analyst Braden Copeland’s report on what to do when the next crash comes.

The behavior of markets (and of entire societies) depends on what everyone knows that everyone knows. Make sense? It didn’t to me, either, until Ben Hunt walked me through an example or two of the Common Knowledge Game in the piece you’re about to read.

Ben says the question he is asked most is “When?” When will this market break? When – to use Ben’s term – will the “Narrative of Central Bank Omnipotence” fail? He doesn’t so much answer the question as explain why he can’t answer it. But he doesn’t leave us empty-handed. In fact, Ben’s explanations of market behavior in terms of the narratives in which we all participate and thegames we all play, are among the most useful tools I have for surviving and thriving out here in unexplored and increasingly treacherous territory.

In other words, it may not be so important to know exactly when a major market narrative will fail (though I wouldn’t mind having a working crystal ball) as it is to know how and why it might fail. That way, we have some chance of detecting incipient signs of failure.

I find it fascinating that so much of market behavior happens silently, right inside our skulls – billions of brains, each working overtime to suss out what the rest might be thinking of doing. The “power of the crowd watching the crowd” is the “most potent behavioral force in human society,” says Ben – but the power wielded by those who can watch the crowd watching the crowd is more potent yet, because their perspective on the Common Knowledge Game lets them ask how the game may be about to change.

But what does it take for “what everyone knows that everyone knows” to shift, or even to flip, and for new common knowledge to assert itself and become entrenched? “Fortunately for us,” says Ben, “game theory provides exactly the right tool kit to unpack socially driven dynamic processes.” So let’s get to unpacking!

Ben confesses that there is “a fly in this glorious ointment” of gamesmanship, and that is the potential for major political shocks. Where, he asks, should we look for “a political shock that would be big enough to challenge the common knowledge that Central Banks are large and in charge, capable of bailing us out no matter what?”

I won’t tell you his answer (hint: it’s not Ukraine), I’ll make you dig for it; but on the way you’re going to unearth some real treasure.

Life is busy. We are getting ready to fly to Italy and then find a train to Tuscany and cars to Trequanda. I have dinner with Steve Cucchiara in Rome Friday night, then get up and meet George Gilder, who will be flying in from Boston and spending a week or so with us. We will both spend our days working on new books (although I might take a day to visit Sienna again). Other friends will be dropping by for periods of time. Dylan Grice will show up at some point next week, as will David Tice [of Prudent Bear fame] and Cliff Draughn from Excelsia in Savannah). And others! It will make for fun dinners.

I do somewhat pay attention to the markets and just shake my head in amazement. Who would have guessed an all-time S&P high of 1905 and 2.5% on the ten-year bond? REALLY? And as Doug Kass pointed out this morning, the VIX is back down to 2007 levels! But this next chart, sent to me by Meb Faber, is not so much ominous as just head-shaking funny. Dear gods, we humans have such short term memories. We always seem to believe it’s different this time.

Sell in May and go away? Not so far this May! Maybe we see a swoon in June? If this market action does not make you nervous, then you’re a better man than I am, Gunga Din.

This weekend’s Thoughts from the Frontline will come to you from Rome, but it will take us to China, a place that is even harder to figure than Italy! Have a great rest of the week.

Your wondering how I can lose weight in Italy analyst,

John Mauldin, Editor

Outside the Box

JohnMauldin@2000wave.com

“When Does the Story Break?”

By Ben Hunt, Ph.D.

Epsilon Theory

May 25, 2014

Until an hour before the Devil fell, God thought him beautiful in Heaven.

– Arthur Miller, “The Crucible”It’s always about timing. If it’s too soon, no one understands. If it’s too late, everyone’s forgotten.

– Anna WintourSaint Laurent has excellent taste. The more he copies me, the better taste he displays.

– Coco ChanelBeauty, to me, is about being comfortable in your own skin. That, or a kick-ass red lipstick.

– Gwyneth Paltrow

For, dear me, why abandon a belief Merely because it ceases to be true? Cling to it long enough, and not a doubt It will turn true again, for so it goes. Most of the change we think we see in life Is due to truths being in and out of favor.

–Robert Frost, “The Black Cottage”Lord I am so tired

How long can this go on?

– Devo, “Working in a Coal Mine”

He can’t think without his hat.

– Samuel Beckett, “Waiting for Godot”

Perhaps the most irrational fashion act of all was the male habit for 150 years of wearing wigs. Samuel Pepys, as with so many things, was in the vanguard, noting with some apprehension the purchase of a wig in 1663 when wigs were not yet common. It was such a novelty that he feared people would laugh at him in church; he was greatly relieved, and a little proud, to find that they did not. He also worried, not unreasonably, that the hair of wigs might come from plague victims. Perhaps nothing says more about the power of fashion than that Pepys continued wearing wigs even while wondering if they might kill him.

– Bill Bryson, “At Home: A Short History of Private Life”

The most common question I get from Epsilon Theory readers is when. When does the market break? When will the Narrative of Central Bank Omnipotence fail? To quote the immortal words of Devo, how long can this go on? Implicit (and sometimes explicit) in these questions is the belief that this – whatever this is – simply can’t go on much longer, that there is some natural law being violated in today’s markets that in the not-so-distant future will visit some terrible retribution on those who continue to flout it. There has never been a more unloved bull market or a more mistrusted stock market high.

It’s a lack of love and a lack of trust that I share. I believe that public markets today are essentially hollow, as what passes for volume and liquidity is primarily machines talking to other machines for portfolio “positioning” or ephemeral arbitrage rather than the human expression of a desire to own a fractional ownership share of a real-world company. I believe that today’s public market price levels primarily reflect the greatest monetary policy accommodation in human history rather than the real-world prospects of real-world companies. I believe that the political risks to both capital market structure and international trade (which are the twin engines of global growth, period, end of story) have not been this great since the 1930’s. Simply put, I believe we are being played like fiddles.

That does NOT mean, however, that I think anything has to change next week … or next month … or next year … or next decade. The human animal is a social animal in the biological sense, and as such we are cognitively evolved to maintain our beliefs and behaviors far beyond what is “true” in an objective sense. This is, in fact, the core argument of Epsilon Theory, that there is no such thing as Truth with a capital T when it comes to the institutions and the social organizations that we create. There’s nothing more “natural” about our market behaviors than there is around, say, our fashion behaviors … the way we wear our clothes or the way we cut our hair. For 150 years everyone knew that everyone knew that gentlemen wore wigs. This was the dominant common knowledge of its day in the fashion world, absolutely no different in any way, shape or form than the dominant common knowledge of today in the investing world … everyone know s that everyone knows that it’s central bank policy that determines market outcomes. And this market common knowledge could last for 150 years, too.

I’m not saying that a precipitous change in market beliefs and behaviors is impossible. I’m saying that it’s not inevitable. I’m saying that it’s NOT just a matter of when. I’m saying that understanding the timing of change in market behaviors is very similar to understanding the timing of change in fashion behaviors, because both are social constructions based on the Common Knowledge Game. It’s no accident that the most popular way to relate that game is the story of the Emperor’s New Clothes.

Here’s a photograph Margaret Bourke-White took of the Garment District in 1930. Every single person on the street is wearing a hat. How did THAT behavior change over time? How did the common knowledge that All Men Wear Hats, or wigs or whatever, change? Does it happen all at once? Smoothly over time? In fits and starts? Who or what sparks this sort of change and how do we know? To use a five dollar phrase, what is the dynamic process that underpins the timing of change in socially-constructed behaviors, whether that behavior is in the investing world or the fashion world?

Fortunately for us, game theory provides exactly the right tool kit to unpack socially driven dynamic processes. To start this exploration, we need to return to the classic thought experiment of the Common Knowledge Game – The Island of the Green-Eyed Tribe.

On the Island of the Green-Eyed Tribe, blue eyes are taboo. If you have blue eyes you must get in your canoe and leave the island the next morning.

On the Island of the Green-Eyed Tribe, blue eyes are taboo. If you have blue eyes you must get in your canoe and leave the island the next morning.

But there are no mirrors or reflective surfaces on the island, so you don’t know the color of your own eyes. It is also taboo to talk or otherwise communicate with each other about blue eyes, so when you see a fellow tribesman with blue eyes, you say nothing. As a result, even though everyone knows there are blue-eyed tribesmen, no one has ever left the island for this taboo.

A Missionary comes to the island and announces to everyone, “At least one of you has blue eyes.”

What happens?

Let’s take the trivial case of only one tribesman having blue eyes. He has seen everyone else’s eyes, and he knows that everyone else has green eyes. Immediately after the Missionary’s statement this poor fellow realizes, “Oh, no! I must be the one with blue eyes.” So the next morning he gets in his canoe and leaves the island.

But now let’s take the case of two tribesmen having blue eyes. The two blue-eyed tribesmen have seen each other, so each thinks, “Whew! That guy has blue eyes, so he must be the one that the Missionary is talking about.” But because neither blue-eyed tribesman believes that he has blue eyes himself, neither gets in his canoe the next morning and leaves the island. The next day, then, each is very surprised to see the other fellow still on the island, at which point each thinks, “Wait a second … if he didn’t leave the island, it must mean that he saw someone else with blue eyes. And since I know that everyone else has green eyes, that means … oh, no! I must have blue eyes, too.” So on the morning of the second day, both blue-eyed tribesmen get in their canoes and leave the island.

The generalized answer to the question of “what happens?” is that for any n tribesmen with blue eyes, they all leave simultaneously on the nth morning after the Missionary’s statement. Note that no one forces the blue-eyed tribesmen to leave the island. They leave voluntarily once public knowledge is inserted into the informational structure of the tribal taboo system, which is the hallmark of an equilibrium shift in any game. Given the tribal taboo system (the rules of the game) and its pre-Missionary informational structure, new information from the Missionary causes the players to update their assessments of where they stand within the informational structure and choose to move to a new equilibrium outcome.

Before the Missionary arrives, the Island is a pristine example of perfect private information. Everyone knows the eye color of everyone else, but that knowledge is locked up inside each tribesman’s own head, never to be made public. The Missionary does NOT turn private information into public information. He does not say, for example, that Tribesman Jones and Tribesman Smith have blue eyes. But he nonetheless transforms everyone’s private information into common knowledge. Common knowledge is not the same thing as public information. Common knowledge is simply information, public or private, that everyone believes is shared by everyone else. It’s the crowd of tribesmen looking around and seeing that the entire crowd heard the Missionary that unlocks the private information in their heads and turns it into common knowledge. This is the power of the crowd watching the crowd, and for my money it’s the most potent behavioral force in human society.

Prior Epsilon Theory notes have focused on the role of the Missionary, and I’ll return to that aspect of the game in a moment. But today my primary focus is on the role of time in this game, and here’s the key: no one thinks he’s on the wrong side of common knowledge at the outset of the game. It takes time for individual tribesmen to observe other tribesmen and process the fact that the other tribesmen have not changed their behavior. I know this sounds really weird, that it’s the LACK of behavioral change in other tribesmen who you believe should be changing their behavior that eventually gets you to realize that they are wondering the same thing about you and your lack of behavioral change, which ultimately gets ALL of you blue-eyed tribesmen to change your behavior in a sudden flurry of activity. But that’s exactly the dynamic here. Even though there is zero behavioral change by any individual tribesman for p erhaps a long period of time, such that an external observer might think that the Missionary’s statement had no impact at all, the truth is that an enormous amount of mental calculations and changes are taking place within each and every tribesman’s head as soon as the common knowledge is created.

I’ve written at length about the portfolio construction corollary to phenotype, or the physical expression of a genetic code, and genotype, or the genetic code itself. The former gets all of the attention because it’s visible, even though the latter is where all the action really is, and that’s a problem. In modern society it means that we place an enormous emphasis on skin color as a signifier of otherness or differentiation, when really it deserves almost no attention at all. In portfolio management it means that we place an enormous emphasis on style boxes and asset classes as a signifier of diversification, when really there are far more telling manifestations. The dynamic of the Common Knowledge Game is another variation on this theme. For almost the entire duration of the game, the activity is internal and invisible, not external and visible, but it’s there all the same, bubbling beneath the behavioral surface until it final ly erupts. The more tribesmen with blue eyes, the longer the game simmers. And the longer the game simmers the more everyone – blue-eyed or not – questions whether or not he has blue eyes. It’s a horribly draining game to play from a mental or emotional perspective, even if nothing much is happening externally and regardless of which side of the common knowledge you are “truly” on.

If you haven’t observed exactly this sort of dynamic taking place in markets over the past five years, with nothing, nothing, nothing despite what seems like lots of relevant news, and then – boom! – a big move up or down as if out of nowhere – I just don’t know what to say. And I don’t know a single market participant, no matter how successful, who’s not bone-tired from all the mental anguish involved with trying to navigate these unfamiliar waters. These punctuated moves don’t come out of nowhere. They are part and parcel of the Common Knowledge Game, no more and no less, and understandable as such.

What starts the clock ticking on the “simmering stage” of the Common Knowledge Game? The Missionary’s public statement that everyone hears, creating the new common knowledge that everyone believes that everyone believes. How long does the simmering stage last? That depends on a couple of factors. First, as described above, the more game players who are on the wrong side of the new common knowledge, the longer the game simmers. Second, the dynamic depends critically on the fame or public acclaim of the Missionary, as well as the power of his or her microphone. A system with a few dominant Missionaries and only a few big microphones will create a clearer common knowledge more quickly, reducing the simmering time. Whether it’s Anna Wintour and Vogue or Janet Yellen and the Wall Street Journal, the scope and pace of game-playing depends directly on who is creating the common knowledge and how that message is amplified by mass med ia. Fashion changes much more quickly today than in, say, the 1930’s, because the “arbiters of taste” – what I’m calling Missionaries – are fewer, more famous, and have stronger media microphones at their disposal. Ditto with the investment world.

But has the clock started ticking on new common knowledge to change the dominant investment game? Has there been a perception-changing public statement from a powerful Missionary to make us question Central Bank Omnipotence, to make us question the color of our eyes? No, there hasn’t. There are clearly new CK games being played in subsidiary common knowledge structures – what I call Narratives – but not in this core Narrative of the Fed’s control over market outcomes. So for example, the market can go down, and more than a little, as the common knowledge around the subsidiary Narrative of The Fed Has Got Your Back comes undone with a second derivative shift from easing to tightening. The Fed itself is the Missionary on this new common knowledge. But the market can’t break so long as the common knowledge of Central Bank Omnipotence remains intact. So long as everyone knows that everyone knows that market outcomes ultimately depen d on Fed policy, then the Yellen put is firmly in place. If things get really bad, then the Fed can save us. We might argue about timing and reaction functions and the like, but everyone believes that everyone believes that the Fed has this ability. And because it’s such strong common knowledge, this ability will never be tested and the market will never break. A nice trick if you can pull it off, and until a Missionary with the clout of the Fed comes out and challenges this core common knowledge it’s a fait accompliwithin the structure of the game. Who has this sort of clout? Only two people – Mario Draghi and Angela Merkel. That’s who I watch and who I listen to for any signs of a crack in the Omnipotence Narrative, and so far … nothing. On the contrary, Draghi and Merkel have been totally on board with the program. We’re all going to be wearing hats for a long time so long as all the investment arbiters of taste stick with their story.< /p> There is, of course, a fly in this glorious ointment, and it’s the single most important difference between the dynamic of fashion markets and financial markets: political shocks and political dislocations can trump common knowledge and precipitate an economic and market dislocation. Wars and coups and revolutions certainly influence fashion, but obviously in a far less immediate and pervasive manner than they influence financial markets. The fashion world is an almost purely self-contained Common Knowledge Game, and the investment world is not. Where am I looking for a political shock that would be big enough to challenge the common knowledge that Central Banks are large and in charge, capable of bailing us out no matter what? It’s not the Ukraine. On the contrary, events there are public enough to give Draghi an excuse to move forward with negative deposit rates or however he intends to implement greater monetary policy accommodation, but peripheral enou gh to any real economic impact so that the ECB’s competence to manufacture an outcome is not questioned. It’s China. If you don’t think that the territorial tussles with Vietnam and Japan matter, if you don’t think that the mutual accusations and arrests of American and Chinese citizens matter, if you don’t think that the HUGE natural gas deal between Russia and China matters, if you don’t think that the sea change in Chinese monetary policy matters … well, you’re just not paying attention. A political shock here is absolutely large enough to challenge the dominant market game, and that’s what I’ll be exploring in the next few Epsilon Theory notes.

|

||

|

Copyright 2014 Mauldin Economics. All Rights Reserved. |

||

|

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting http://www.mauldineconomics.com. To subscribe to John Mauldin’s e-letter, please click here: Outside the Box and MauldinEconomics.com is not an offering for any investment. It represents only the opinions of John Mauldin and those that he interviews. Any views expressed are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest and is not in any way a testimony of, or associated with, Mauldin’s other firms. John Mauldin is the Chairman of Mauldin Economics, LLC. He also is the President of Millennium Wave Advisors, LLC (MWA) which is an investment advisory firm registered with multiple states, President and registered representative of Millennium Wave Securities, LLC, (MWS) member FINRAand SIPC, through which securities may be offered. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Brok er (IB) and NFA Member. Millennium Wave Investments is a dba of MWA LLC and MWS LLC. This message may contain information that is confidential or privileged and is intended only for the individual or entity named above and does not constitute an offer for or advice about any alternative investment product. Such advice can only be made when accompanied by a prospectus or similar offering document. Past performance is not indicative of future performance. Please make sure to review important disclosures at the end of each article. Mauldin companies may have a marketing relationship with products and services mentioned in this letter for a fee. Note: Joining the Mauldin Circle is not an offering for any investment. It represents only the opinions of John Mauldin and Millennium Wave Investments. It is intended solely for investors who have registered with Millennium Wave Investments and its partners at www.MauldinCircle.com or directly related websites. The Mauldin Circle may send out material that is provided on a confidential basis, and subscribers to the Mauldin Circle are not to send this letter to anyone other than their professional investment counselors. Investors should discuss any investment with their personal investment counsel. John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as wel l as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private and non-private investment offerings with other independent firms such as Altegris Investments; Capital Management Group; Absolute Return Partners, LLP; Fynn Capital; Nicola Wealth Management; and Plexus Asset Management. Investment offerings recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor’s services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauld in receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements. PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER. Alternative investment performance can be volatile. An investor could lose all or a substantial amount of his or her investment. Often, alternative investment fund and account managers have t otal trading authority over their funds or accounts; the use of a single advisor applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. There is often no secondary market for an investor’s interest in alternative investments, and none is expected to develop. All material presented herein is believed to be reliable but we cannot attest to its accuracy. Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs may or may not have investments in any funds cited above as well as economic interest. John Mauldin can be reached at 800-829-7273. |

After decades of working with defense technology companies, I know the ebb and flow of military spending all too well.

I remember that when the Cold War came to an end, the nation’s political leaders were talking enthusiastically about the so-called “peace dividend.”

That’s Washington-speak for Pentagon budget cuts that always seem to come after a major conflict has ended.

Many investors believe that with our presence in Iraq largely gone, defense firms will offer mediocre returns at best.

I’m not buying into it. I think massive profit opportunities are there. And the market and the government are lining up behind them…

Not Just a Bull, a National Imperative

Fact is, earlier this decade, several key defense contractors saw there were tough times ahead and revamped operations to do well with lean budgets.

More to the point, as current dramatic news makes all too clear, the U.S. needs a strong global military presence with an army, navy, air force, and Marine Corps second to none.

The escalating conflict in Ukraine is a great example of why the U.S. must maintain a strong defense structure. It includes the ability to support NATO allies against incursions into Europe.

But that’s not the only global threat we face…

Look at how aggressive China has become in its demand to control the South China Sea. Not only that, but North Korea’s unstable regime remains a looming threat.

So, while many investors are looking at other sectors because of the ongoing Washington budget battles, defense stocks as a group have greatly outperformed the overall market.

Here’s the thing. I grew up in a military household and have followed defense technology my entire career as an analyst.

In fact, I was in the tech trenches during the 1980s when President Reagan broke new ground with his tech-centric Strategic Defense Initiative, more commonly known as his “Star Wars” program.

So, I have seen first-hand the Pentagon and its prime contractors adapt to budget cuts and come back stronger every time. And they are brimming with advanced technology that gives America defense superiority.

Back U.S. Defense and Reap Huge Gains

What we want to do is take advantage of the all the opportunities to profit from tech breakthroughs and weapons programs that will permeate the entire sector.

That’s why I think investors would do well to take a good look at PowerShares Aerospace & Defense (NYSE: PPA). This is a cost-effective ETF made up of 80% defense and aerospace stocks from companies who are proven leaders.’

The fund has a solid mix of companies, including cutting-edge small caps like FLIR Systems Inc. (Nasdaq: FLIR), the world’s predominant maker of commercial thermal-imaging cameras.

There’s also the advanced materials firm Hexcel Corp. (NYSE: HXL), which supplies honeycomb composites to some of the biggest names in the aerospace industry.

But the heart of this ETF play is found in its top 10 holdings.

They include many well-capitalized companies that have succeeded for decades regardless of Washington’s defense budget battles.

Raytheon Company (NYSE: RTN) is a full-spectrum company that provides the Pentagon with systems for electronic warfare, laser rangefinders, military training, and advanced radar.

Plus, the company’s intercept vehicles, radars, and space sensors work together to protect the U.S. and its allies against ballistic missiles, cruise missiles, aircraft, and other threats.

Raytheon was recently awarded an $8.5 million contract by the Office of Naval Research to develop a digital radar system that is thought to be the world’s most advanced.

In this year’s first quarter, earnings per share increased 3% from the year ago quarter to $1.57. New bookings grew 19% to $4.3 billion. Trading at $97 a share, Raytheon has a $30 billion market cap.

For its part, Lockheed Martin Corp. (NYSE: LMT) is well-known for making military aircraft. But the firm also supplies combat ships and ground vehicles as well as advanced radar and tactical communications.

Indeed, this is a company that illustrates what I’ve been talking about in terms of realigning to take advantages of the sector’s broad changes. The company’s history dates back more than 100 years, but the modern firm came together in a 1995 merger.

Lockheed Martin’s reach also includes space exploration, satellite systems, and climate monitoring. Moreover, the company has deep expertise in biometrics, cyber security, and the booming field of cloud computing.

The company recently secured two contracts from the U.S. Navy and Royal Canadian Air Force, combining for $34 million to develop laser-guided bombs.

In this year’s first quarter, sales fell 4% to $10.7 billion, but profits rose 23% to $933 million. The company forecasts higher sales, operating margins, and cash flow for the full year. Trading at $162 a share, Lockheed Martin has a $51 billion market cap.

And Northrop Grumman Corp. (NYSE: NOC) has a wide spectrum of operations that cover everything from advanced sensors to missile defense to cyber security.

The company makes manned and unmanned aircraft for defense applications. But it’s also collaborating with Yamaha to develop an autonomous helicopter with onboard intelligence gathering equipment for such civilian uses as search and rescue and forest fire observations.

Northrop Grumman also provides the military with electronic warfare and infrared countermeasures. In addition, the firm gives us a strong play on sensor technologies, advanced materials, and laser weapons systems.

For the first quarter of 2014, sales fell 5% from the year-ago period to $5.8 billion, but earnings per share rose 23% to $2.63. Trading at $120 a share, Northrop Grumman has a $26 billion market cap.

Thus, for tech investors PPA offers us access to some of the best and most advanced systems on earth – everything from robotics to sensors and space exploration.

It sells for just a fraction of some of its big-cap members. PPA trades at just $32, less than one-third the price of even the cheapest of the three big-cap defense firms we talked about today.

And it offers us superior returns. Over the past two years, PPA has gained some 74%. That’s more than two-thirds better than the S&P 500’s return over the period of 44%.

Setting Up Perfectly for the Short Term (and Long)

This also is a great long-term play. See, no matter what happens in Washington over the next several years, America’s role as the world’s only real superpower means we have little choice but to fund a strong defense system.

Plus, the U.S. will continue to push the boundaries of tech-centric warfare. No matter which party is in power after 2016, advanced technology will continue to get strong fiscal support.

All of which means both the big-cap contractors and the small-cap cutting edge firms stand to gain, which will only provide more support and price appreciation for PPA.

Michael Robinson’s Strategic Tech Investor puts you directly in touch with high-tech research, analysis… stock picks and strategies from a sector that can double, triple – even quadruple your retirement savings faster than any other sector on earth. Just click here, and you’ll get Strategic Tech Investor and all of Michael Robinson’s technology reports for free.]

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair